S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Northpointe Bancshares, Inc. (NASDAQ:NPB) presented its second quarter 2025 earnings results on July 23, 2025, showcasing strong financial performance driven by its Mortgage Purchase Program (MPP) and digital banking initiatives. The company, which operates primarily through a digital platform with a single physical branch in Grand Rapids, Michigan, continues to expand its national mortgage purchase program while maintaining solid asset quality.

Trading at $14.95 as of July 22, 2025, Northpointe shares have shown resilience, currently trading near the higher end of their 52-week range of $11.43 to $15.50.

Quarterly Performance Highlights

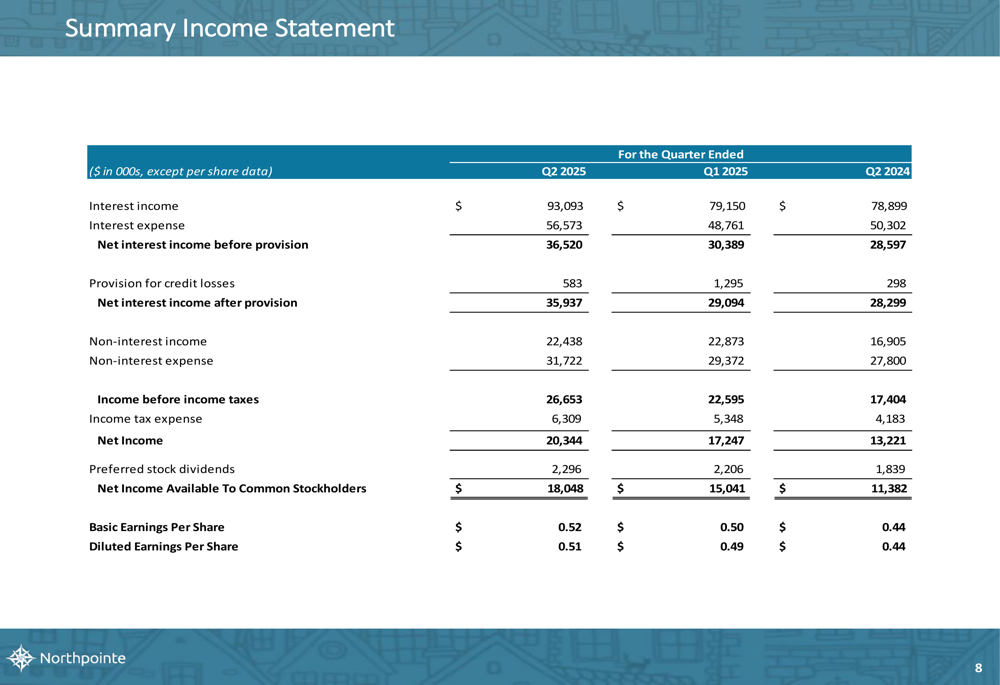

Northpointe reported net income available to common stockholders of $18.0 million or $0.51 per diluted share for Q2 2025, representing significant improvement over both the previous quarter ($15.0 million or $0.49 per share) and the same quarter last year ($11.4 million or $0.44 per share).

The company achieved strong performance metrics, including a 1.34% return on average assets, 13.60% return on average equity, and 14.49% return on average tangible common equity. The efficiency ratio improved to 53.80%, indicating better operational effectiveness.

As shown in the following income statement summary, Northpointe’s net interest income before provision increased to $36.5 million in Q2 2025, up from $30.4 million in Q1 2025 and $28.6 million in Q2 2024:

Total (EPA:TTEF) assets grew to $6.43 billion as of June 30, 2025, compared to $5.86 billion at the end of the previous quarter and $5.16 billion a year earlier. This growth was primarily driven by the expansion of the loan portfolio, particularly the Mortgage Purchase Program.

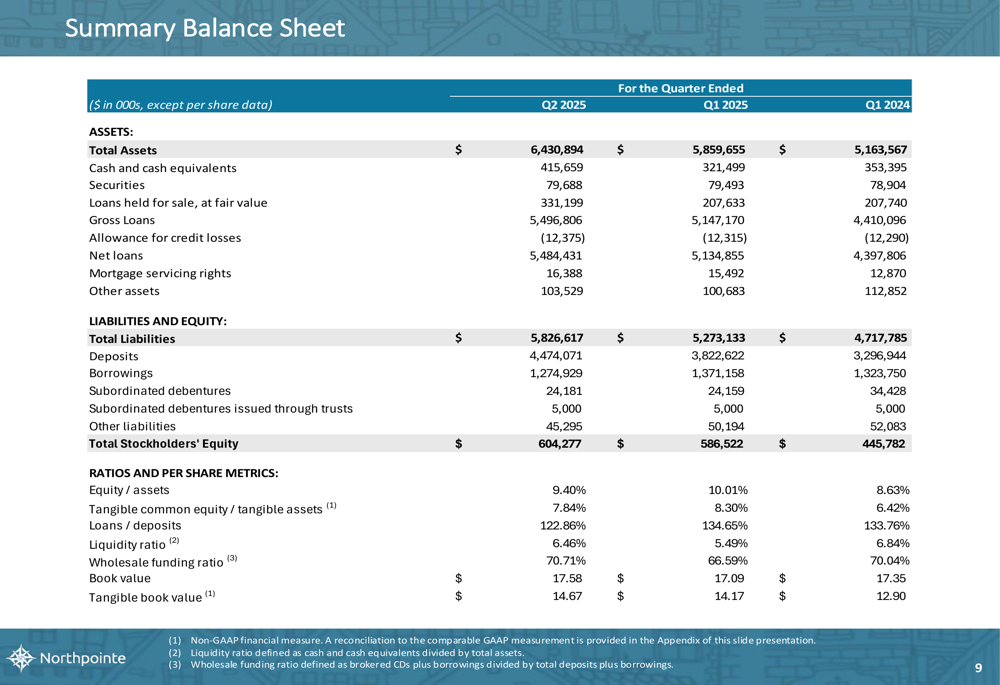

The following balance sheet summary highlights the company’s financial position:

Detailed Financial Analysis

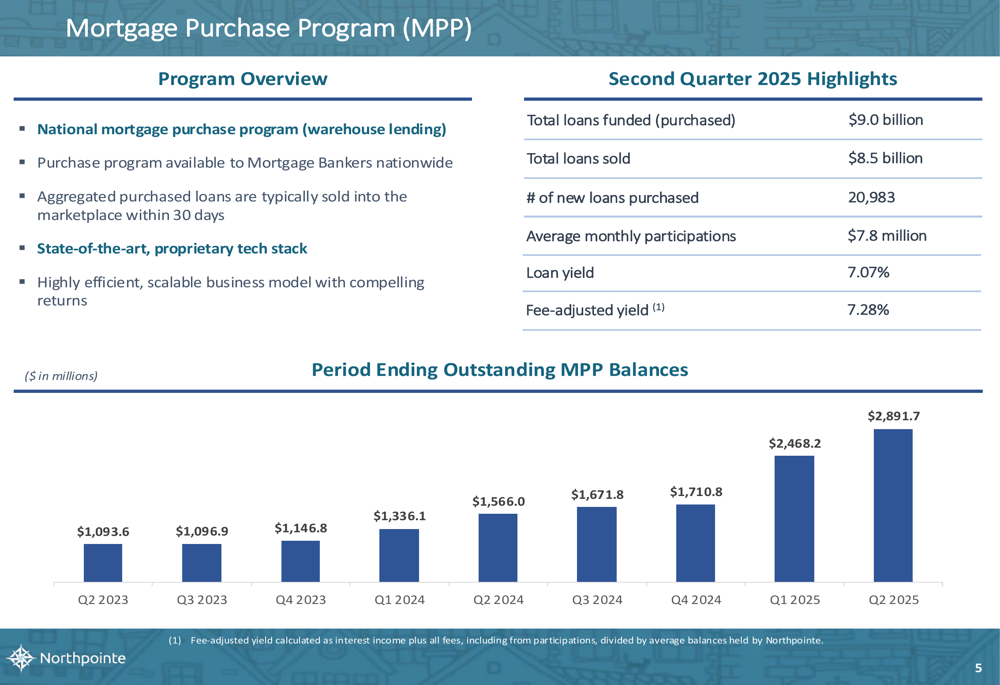

The Mortgage Purchase Program continues to be Northpointe’s primary growth driver, with outstanding balances reaching $2.89 billion in Q2 2025, representing a 69% annualized growth rate from the previous quarter. During Q2, the program funded $9.0 billion in loans and sold $8.5 billion, demonstrating the high-velocity nature of this business line.

The MPP’s impressive growth trajectory is illustrated in the following chart:

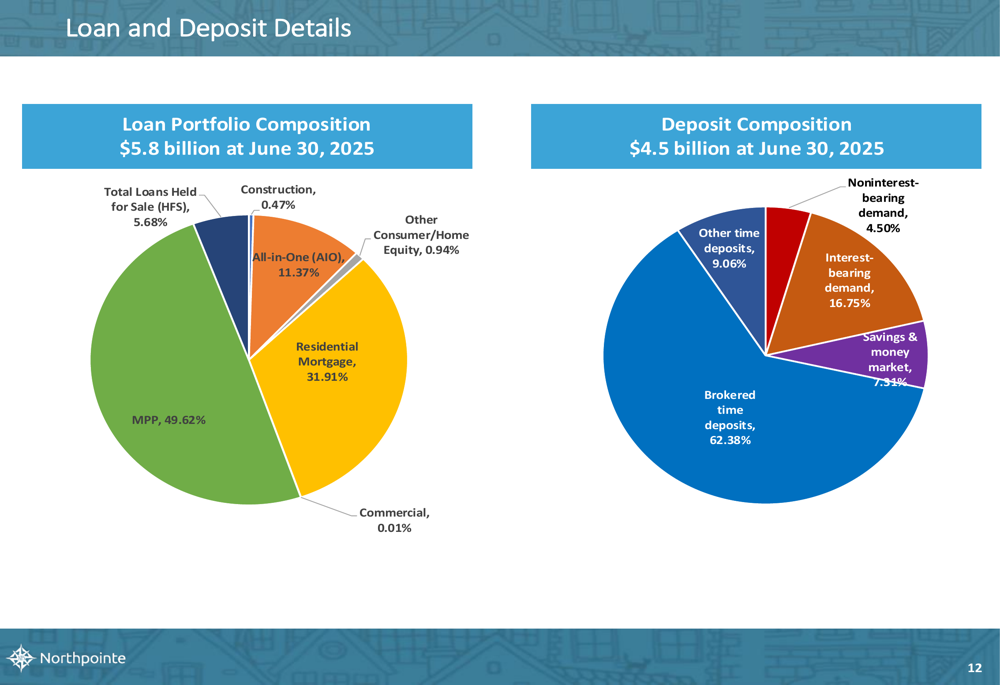

Deposit growth was equally robust, with total deposits increasing by $651.4 million during the quarter to reach $4.47 billion. This growth was primarily driven by brokered CDs, which now constitute 62.38% of the deposit base. Non-interest-bearing demand deposits represent 4.50% of total deposits, while interest-bearing demand accounts make up 16.75%.

The loan and deposit composition is detailed in the following charts:

Strategic Initiatives

Northpointe’s strategic focus remains on three core business segments: residential lending, digital deposit banking, and specialized mortgage servicing.

The residential lending segment, which operates as a national distributed retail mortgage franchise, generated $19.4 million in net gain on sale of loans during Q2 2025, with residential mortgage originations totaling $665.5 million. The company’s All-in-One loan product, which ties first-lien home equity lines to demand deposit sweep accounts, grew by $19.6 million (12% annualized) and maintained a strong yield of 7.57%.

The digital deposit banking platform continues to expand nationwide, with an average retail depositor balance of $34.7 thousand. The company’s liquidity ratio stood at 6.46% for the quarter.

In specialized mortgage servicing, Northpointe generated $1.5 million in loan servicing fees while servicing approximately 12,700 loans with an unpaid principal balance of $4.0 billion for others. Custodial deposits related to this business line amounted to $137.3 million.

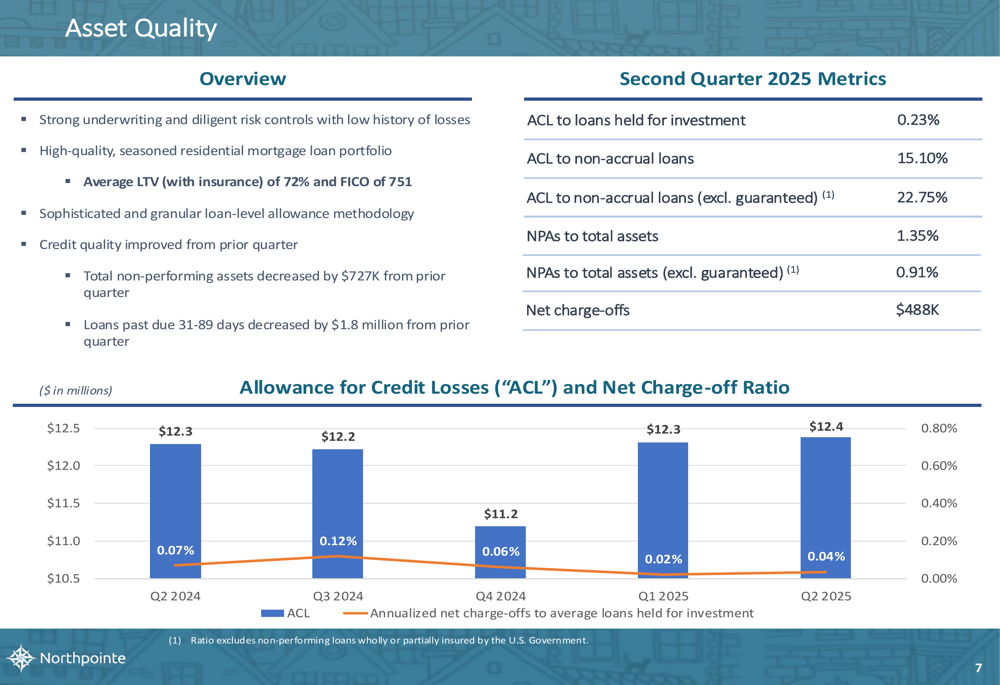

Asset Quality and Capital Position

Northpointe maintained strong asset quality metrics in Q2 2025, with the allowance for credit losses (ACL) at $12.4 million, representing 0.23% of loans held for investment. Net charge-offs for the quarter were minimal at $488,000, or 0.04% of average loans held for investment (annualized).

The following chart illustrates the company’s ACL and net charge-off trends:

The company’s capital position remains solid, with equity to assets at 9.40% and tangible common equity to tangible assets at 7.84%. Book value per share increased to $17.58, representing an annualized growth rate of 11.5%, while tangible book value per share grew to $14.67, up 14.1% on an annualized basis.

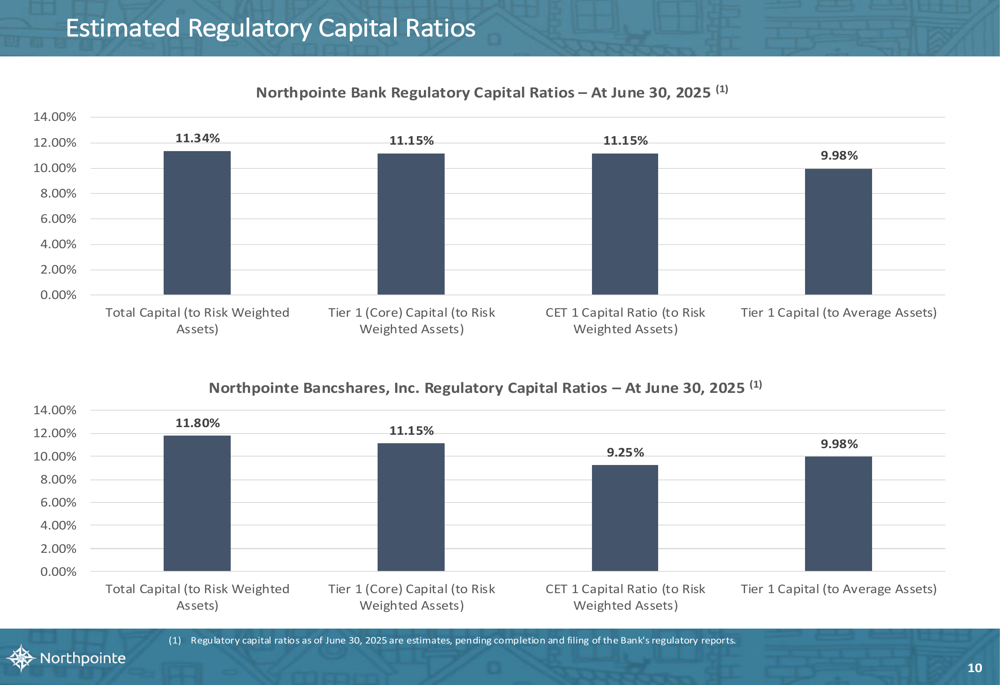

Regulatory capital ratios for both the bank and holding company remained well above minimum requirements, as shown in the following chart:

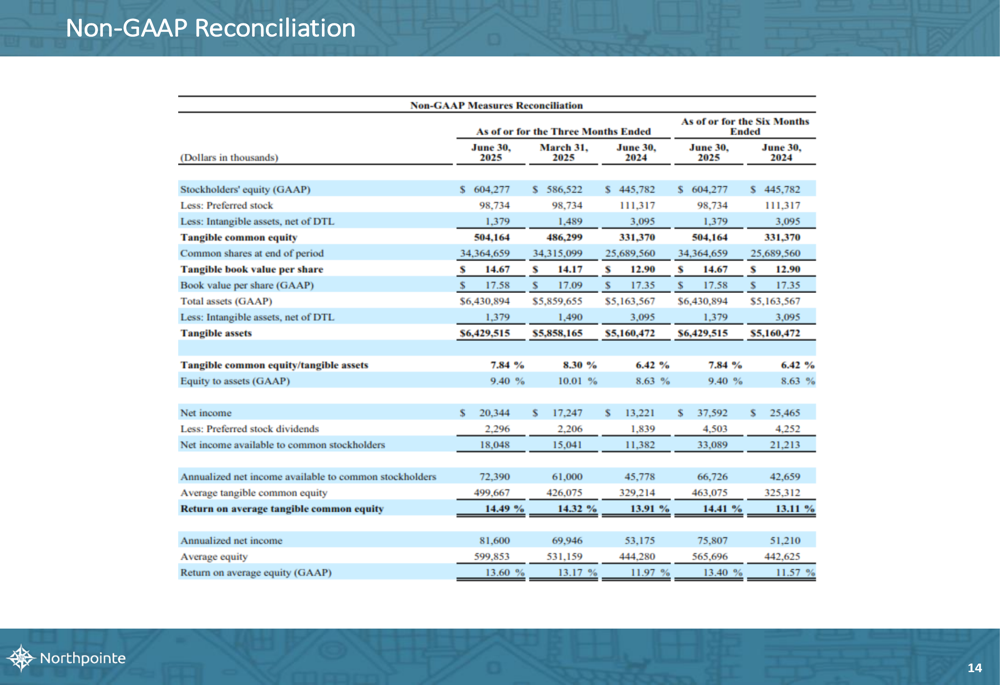

To provide a clearer picture of Northpointe’s financial position, the company included a reconciliation of GAAP to non-GAAP measures:

Overall, Northpointe Bancshares’ Q2 2025 presentation demonstrates continued momentum in its core business lines, with particularly strong growth in the Mortgage Purchase Program driving improved profitability while maintaining solid asset quality and capital positions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.