Oil prices extend losses as traders downplay Russia sanction risks

Introduction & Market Context

Northrop Grumman Corporation (NYSE:NOC) presented its second quarter 2025 earnings results on July 22, showing strong sequential growth and a significant recovery from its disappointing first quarter performance. The defense contractor’s shares rose 3% in premarket trading to $530.75, reflecting investor confidence in the company’s improved outlook.

The presentation, delivered by Chair and CEO Kathy Warden and CFO Ken Crews, highlighted accelerating topline momentum with sales increasing 9% sequentially from Q1, alongside margin expansion and increased full-year guidance for several key metrics.

This recovery comes after a challenging first quarter when Northrop Grumman missed earnings expectations by nearly 48%, posting an EPS of just $3.32 versus the forecasted $6.32, which had sent shares tumbling 11.3%.

Quarterly Performance Highlights

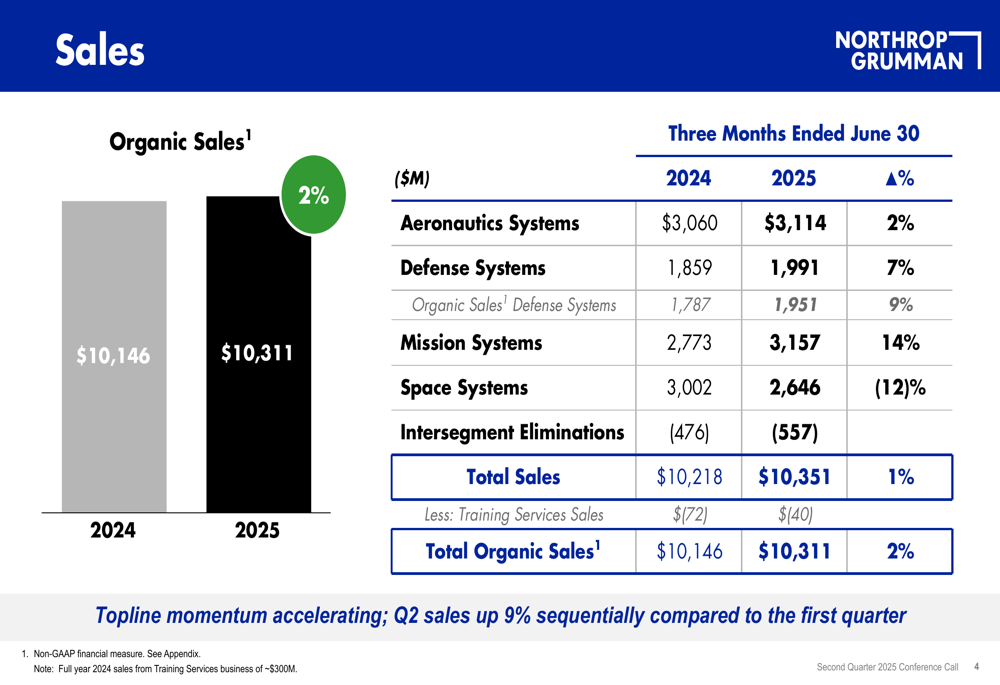

Northrop Grumman reported Q2 2025 sales of $10.35 billion, representing a 1% increase from the same period last year. Organic sales, which exclude the impact of acquisitions and divestitures, grew 2% year-over-year to $10.31 billion.

The company’s performance varied significantly across business segments. Mission Systems led growth with a 14% sales increase, while Defense Systems grew 7%. However, Space Systems experienced a 12% decline in sales compared to Q2 2024.

As shown in the following chart of quarterly sales performance by segment:

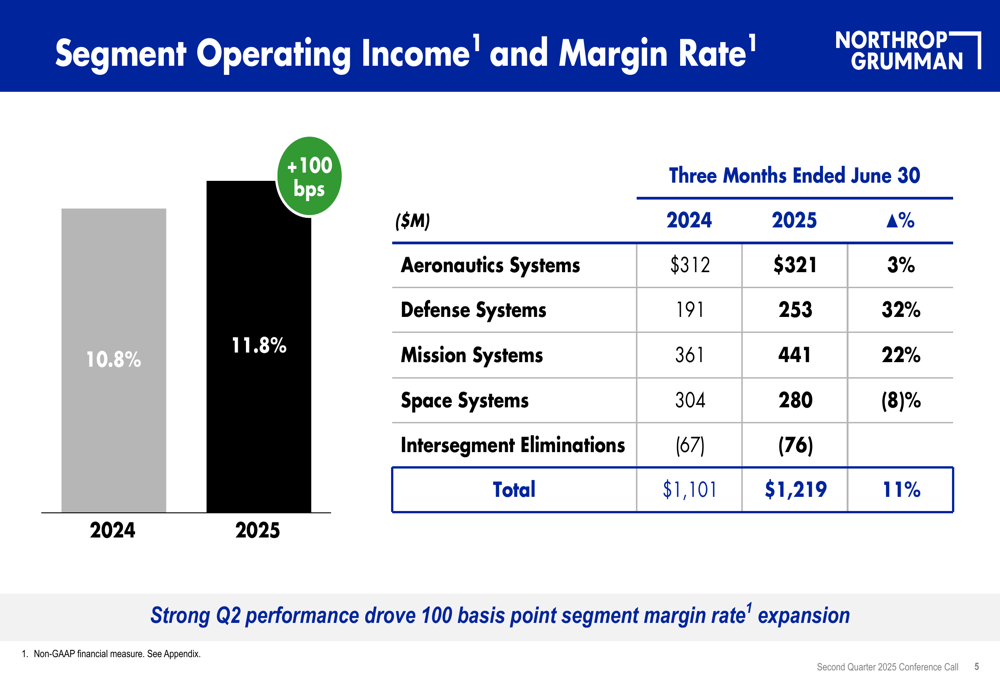

Segment operating income showed even stronger improvement, increasing 11% year-over-year to $1.22 billion. This growth was driven by exceptional performance in Defense Systems (+32%) and Mission Systems (+22%), which more than offset the 8% decline in Space Systems.

The following chart illustrates the segment operating income growth and margin expansion:

Detailed Financial Analysis

A key highlight of the quarter was Northrop Grumman’s significant margin expansion. The segment operating margin rate increased by 100 basis points to 11.8%, demonstrating improved operational efficiency across most business units.

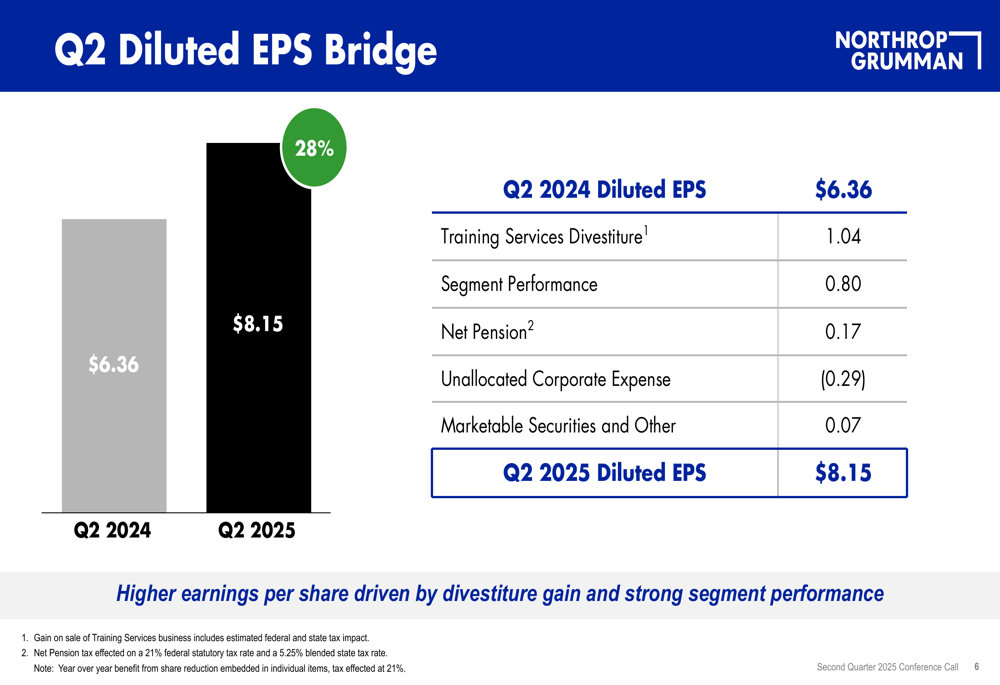

Diluted earnings per share surged 28% to $8.15 compared to $6.36 in Q2 2024. This substantial increase was driven by multiple factors, as shown in the following EPS bridge:

The largest contributor to EPS growth was a $1.04 gain from the Training Services divestiture, followed by $0.80 from improved segment performance. Net pension contributed an additional $0.17, while unallocated corporate expenses reduced EPS by $0.29.

Free cash flow for the quarter was $637 million, down from $1.1 billion in Q2 2024. However, the company expects stronger cash generation in the second half of the year, supporting its full-year guidance.

Forward-Looking Statements

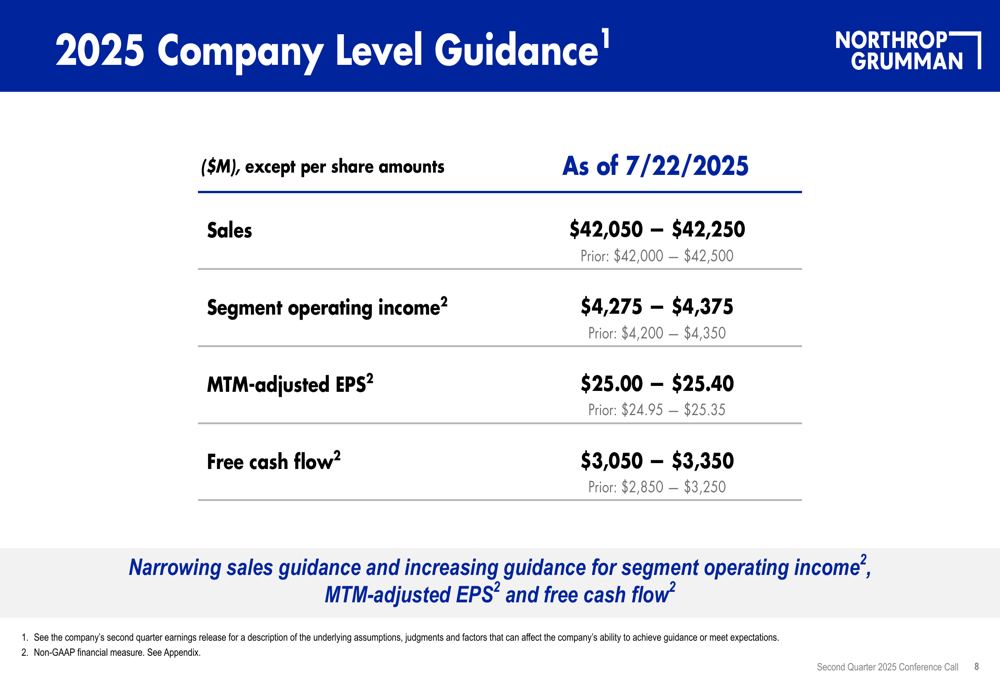

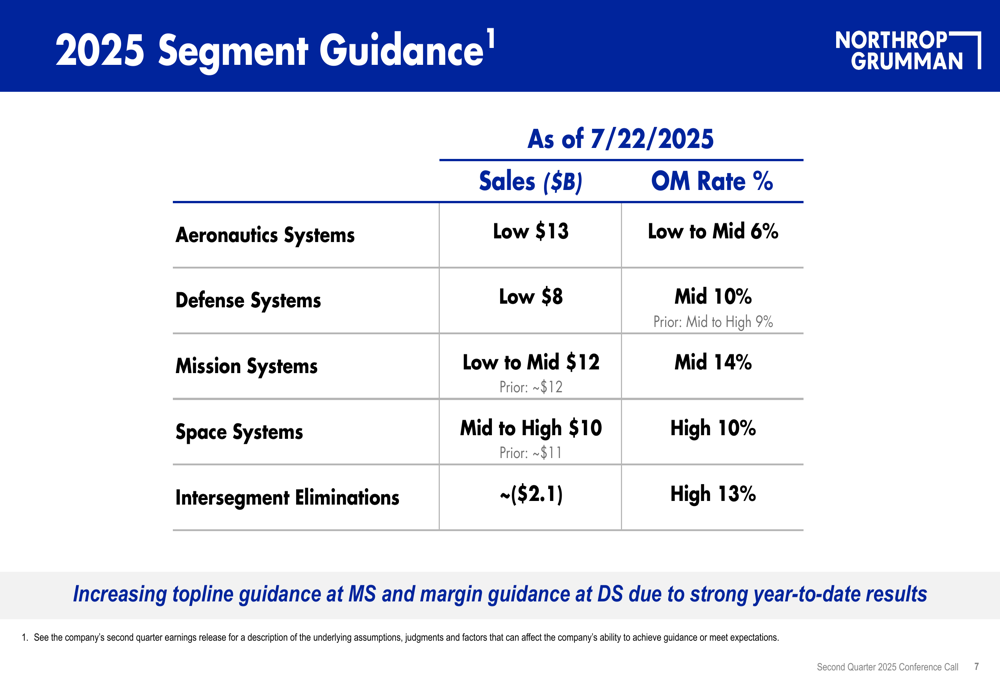

Based on strong year-to-date performance, Northrop Grumman raised guidance for several key metrics while narrowing its sales forecast. The updated company-level guidance is illustrated below:

The company now expects:

- Sales of $42.05-$42.25 billion (previously $42.0-$42.5 billion)

- Segment operating income of $4.28-$4.38 billion (up from $4.2-$4.35 billion)

- MTM-adjusted EPS of $25.00-$25.40 (increased from $24.95-$25.35)

- Free cash flow of $3.05-$3.35 billion (up from $2.85-$3.25 billion)

At the segment level, Northrop Grumman increased its operating margin rate guidance for Defense Systems to mid-10% (previously mid to high 9%) and adjusted sales guidance for Mission Systems to low to mid $12 billion (previously ~$12 billion) and Space Systems to mid to high $10 billion (previously ~$11 billion).

The company cited increasing global defense demand, particularly in missile defense, nuclear triad, and weapons systems, as a key driver of future growth opportunities. Management emphasized their commitment to accelerating development and production of new capabilities while maintaining focus on performance and financial commitments.

Strategic Initiatives

Northrop Grumman highlighted its balanced approach to capital deployment, with plans to return approximately 100% of free cash flow to shareholders in 2025 through dividends and share repurchases. This shareholder-friendly approach comes alongside continued investment in research and development to address evolving defense needs.

The presentation featured the company’s BEACON unmanned aircraft, underscoring Northrop Grumman’s continued focus on next-generation defense technologies. This aligns with management’s emphasis on innovation and speed in developing new capabilities for a dynamic global defense landscape.

The company’s recovery from its Q1 challenges demonstrates resilience in its business model and ability to address program-specific issues, such as the $477 million B-21 program adjustment that significantly impacted first quarter results. With sequential growth accelerating and guidance increased, Northrop Grumman appears well-positioned to achieve its full-year objectives despite the earlier setback.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.