European shares fall: Trump threatens ’massive’ tariff increase on China

Introduction & Market Context

Northwest Natural Gas Co (NYSE:NWN) presented its second quarter 2025 earnings results on August 5, revealing substantial year-over-year growth driven by rate adjustments and strategic acquisitions. The utility company, which provides natural gas and water services, reported adjusted earnings per share of $2.28 for Q2 2025, a 42.5% increase from $1.60 in the prior year period. Despite these strong results, NWN stock closed at $40.20 on August 4, trading below its 52-week high of $44.38.

The company’s presentation highlighted its multi-utility strategy, with growing contributions from its gas utility operations in the Pacific Northwest and Texas, as well as its expanding water utility business. Management reaffirmed its full-year guidance, signaling confidence in continued execution of its growth strategy despite macroeconomic headwinds.

Quarterly Performance Highlights

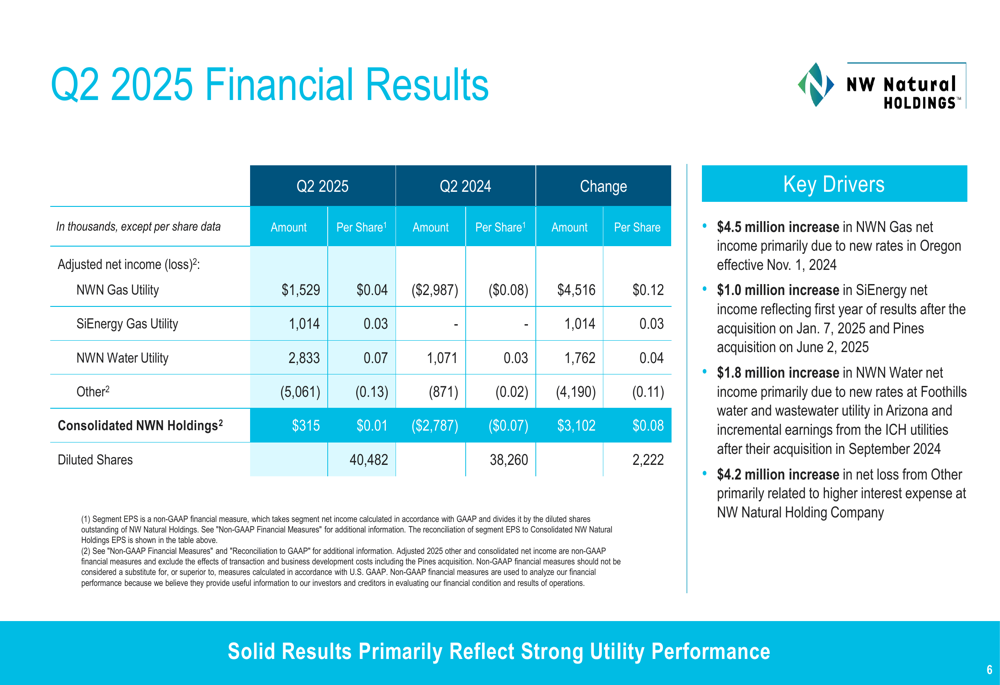

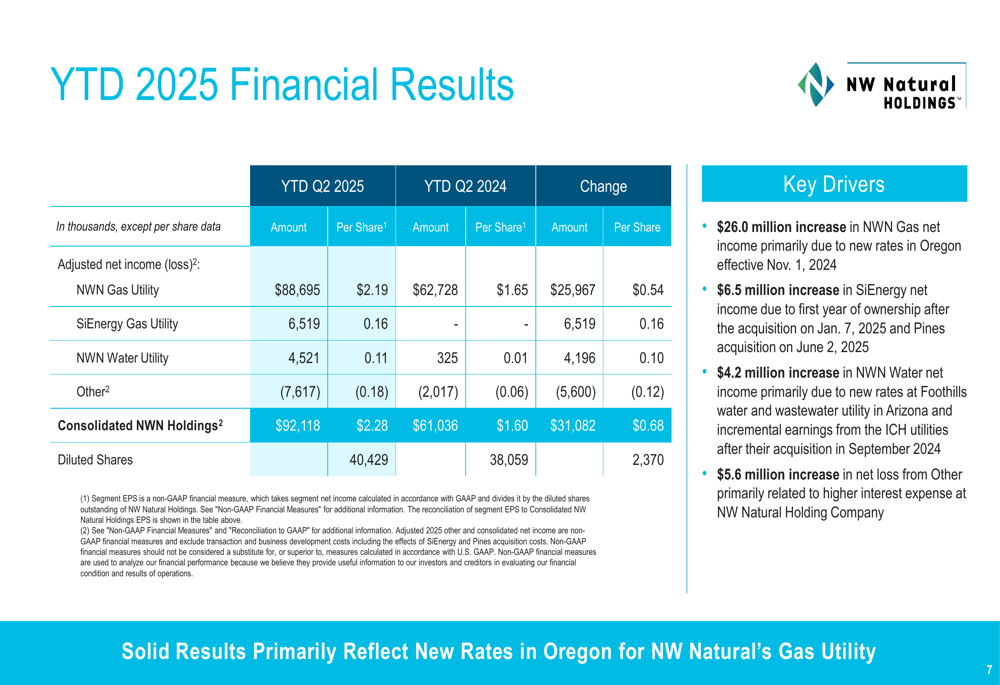

Northwest Natural reported significant financial improvements across its business segments for the second quarter of 2025. The company’s adjusted net income reached $315,000 for Q2, with year-to-date adjusted net income of $92.1 million.

"We delivered strong results in the second quarter, with substantial increases in both our gas and water utility operations," noted Justin B. Palfreyman, President & CEO, according to the presentation materials.

The company’s customer base expanded considerably, adding over 92,000 gas and water utility connections, representing a growth rate of 10.6%. Organic customer growth remained solid at 1.9% for the first half of 2025, demonstrating continued demand for the company’s services.

As shown in the following comprehensive overview of key results:

The financial breakdown reveals that NWN Gas Utility contributed $1,529,000 to adjusted net income, while SiEnergy Gas Utility added $1,014,000 and NWN Water Utility provided $2,833,000. These positive contributions were partially offset by a $5,061,000 loss in the "Other" category, primarily due to higher interest expenses.

The detailed quarterly financial results demonstrate the drivers behind the company’s performance:

Year-to-date financial results further illustrate the company’s growth trajectory, with consolidated adjusted net income of $92.1 million:

Strategic Initiatives & Acquisitions

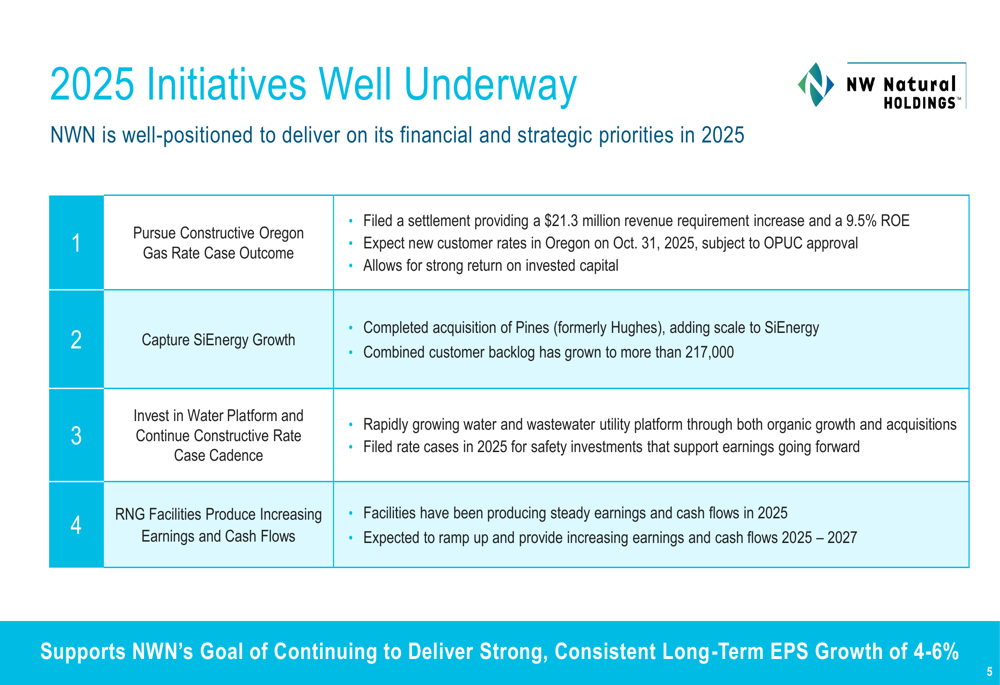

Northwest Natural’s presentation emphasized four key strategic initiatives for 2025, all of which are progressing according to plan. The company reached a settlement in its Oregon general rate case for $21.3 million in revenue, with new rates expected to take effect on October 31, 2025. This regulatory outcome provides a foundation for stable returns in its core market.

The acquisition of Pines gas utility (formerly Hughes) has been completed, expanding the company’s footprint in Texas. SiEnergy’s backlog now exceeds 217,000 potential connections, providing visibility into future growth. The water utility platform continues to grow rapidly through acquisitions, with multiple rate cases filed to support returns on these investments.

The company’s strategic initiatives are illustrated in the following slide:

Financial Position & Outlook

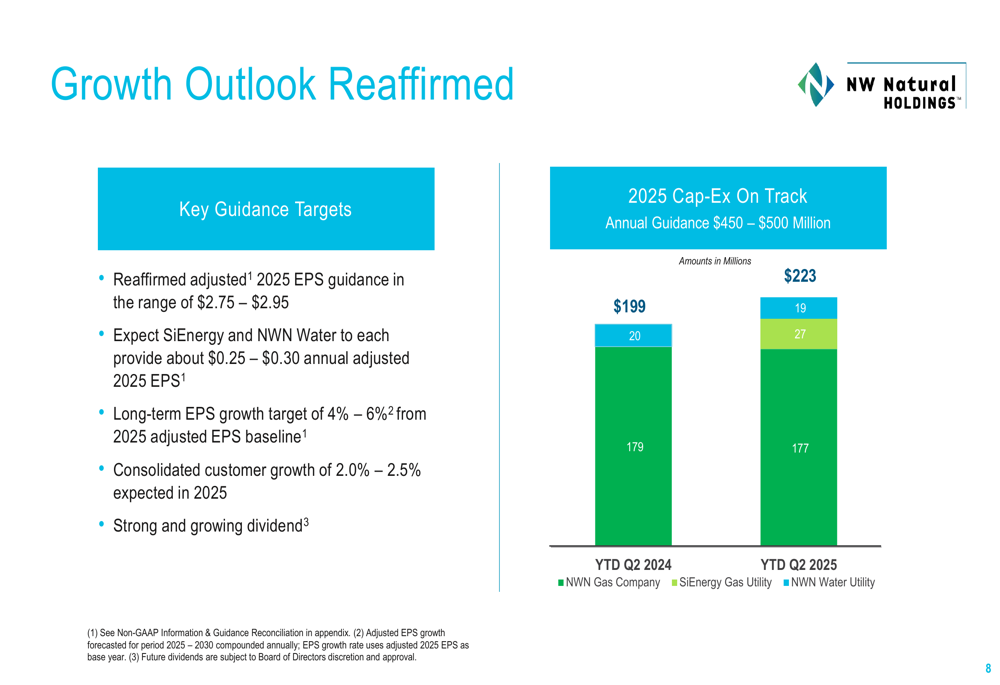

Northwest Natural reaffirmed its 2025 adjusted EPS guidance of $2.75 to $2.95, along with its long-term EPS growth target of 4% to 6% from the 2025 adjusted EPS baseline. Management expects SiEnergy and NWN Water to each contribute $0.25 to $0.30 to annual adjusted 2025 EPS, highlighting the growing importance of these business segments.

Capital expenditures remain on track with annual guidance of $450 to $500 million. Year-to-date capital expenditures reached $223 million, compared to $199 million in the same period last year, reflecting continued investment in infrastructure and growth initiatives.

The company’s growth outlook and capital expenditure progress is detailed in the following slide:

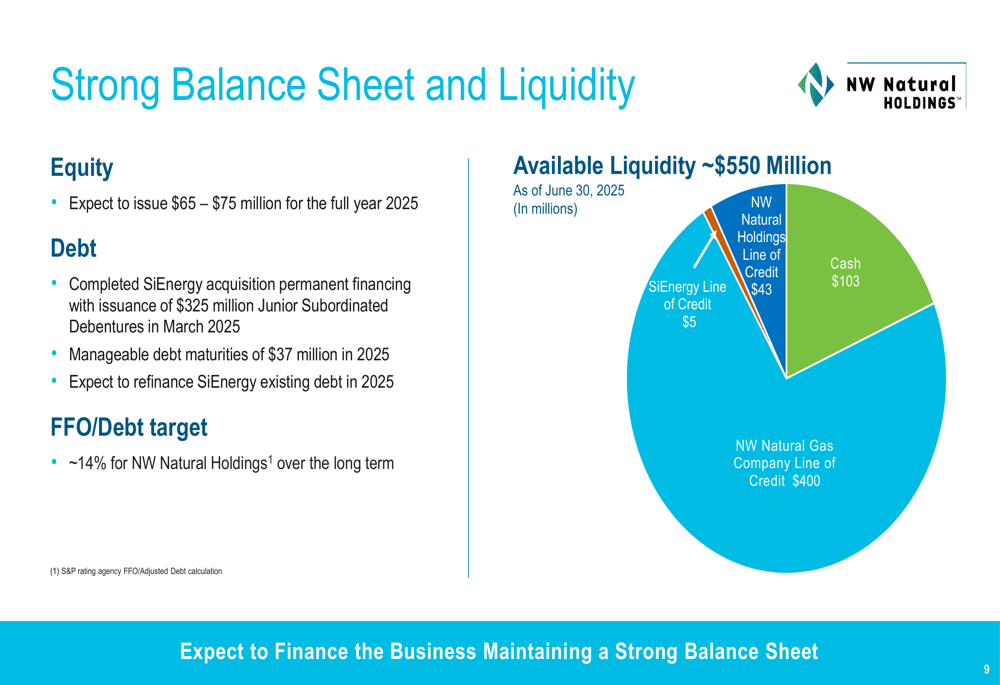

Northwest Natural maintains a strong balance sheet with approximately $550 million in available liquidity, including $103 million in cash. The company expects to issue $65 to $75 million in equity for the full year 2025 and has manageable debt maturities of $37 million in 2025. In March 2025, the company completed SiEnergy acquisition financing with $325 million in Junior Subordinated Debentures.

The company’s balance sheet strength and liquidity position are illustrated in this slide:

Forward-Looking Statements

Looking ahead, Northwest Natural expects consolidated customer growth of 2.0% to 2.5%, supported by both organic growth and acquisitions. The company’s renewable natural gas (RNG) facilities are producing earnings that are expected to increase from 2025 to 2027, adding another growth driver to the portfolio.

Management is targeting a funds from operations (FFO) to debt ratio of approximately 14% for Northwest Natural Holdings over the long term, which supports the company’s investment-grade credit rating. The company also emphasized its commitment to maintaining a strong and growing dividend, which has been a hallmark of its shareholder return strategy.

"Our 2025 initiatives are well underway and support our goal of consistent long-term EPS growth of 4-6%," stated Ray Kaszuba, SVP & CFO, according to the presentation.

The leadership team presenting these results includes:

While Northwest Natural’s presentation paints a positive picture of growth and strategic execution, investors should note that higher interest expenses continue to pressure results in the "Other" segment. Additionally, the successful integration of recent acquisitions and timely implementation of rate case outcomes will be critical factors in achieving the company’s guidance for the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.