60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

NRC Group ASA (OB:NRC), a leading Nordic railway infrastructure contractor, presented its second quarter 2025 results on August 14, showing a significant financial turnaround. The company has successfully reversed last year's substantial losses, reporting positive EBIT figures and improved performance across its Nordic operations.

The presentation, delivered by CEO Anders Gustafsson and CFO Åsgeir Nord, highlighted the company's return to profitability amid challenging market conditions in the infrastructure sector. NRC Group's shares closed at NOK 7.13 on August 13, 2025, showing significant recovery from its 52-week low of NOK 2.98.

Quarterly Performance Highlights

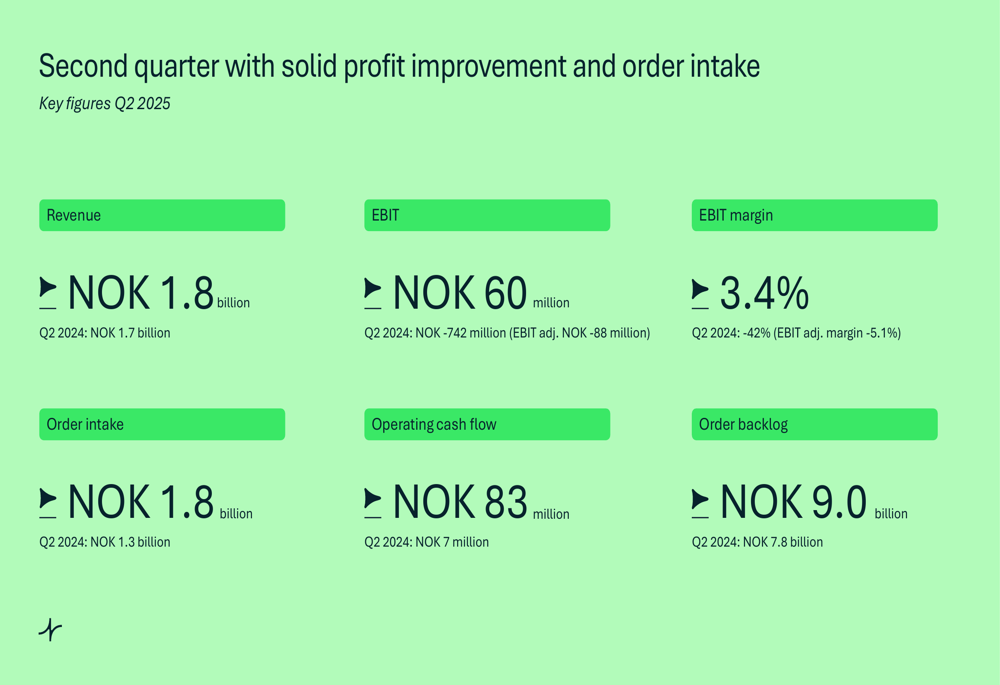

NRC Group reported second quarter revenue of NOK 1.8 billion, a slight increase from NOK 1.7 billion in the same period last year. The most dramatic improvement came in EBIT, which reached NOK 60 million compared to a substantial loss of NOK 742 million in Q2 2024, resulting in an EBIT margin of 3.4%.

The company's order intake grew significantly to NOK 1.8 billion, up from NOK 1.3 billion in Q2 2024, while the order backlog increased to NOK 9.0 billion from NOK 7.8 billion a year earlier. Operating cash flow also showed substantial improvement, reaching NOK 83 million compared to just NOK 7 million in the same quarter last year.

As shown in the following financial highlights chart:

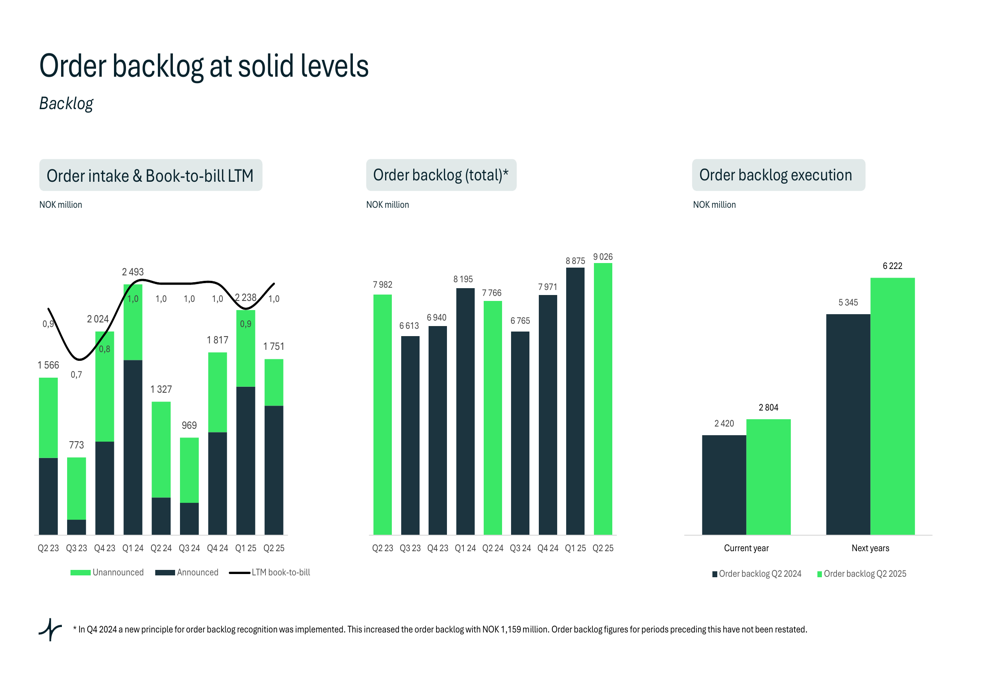

The order backlog analysis reveals a consistent book-to-bill ratio between 0.9 and 1.0 over the last twelve months, indicating a stable relationship between new orders and completed work. The execution timeline for the current backlog shows NOK 2,804 million scheduled for completion in 2025 and NOK 6,222 million for 2026 and beyond, providing solid revenue visibility.

Detailed Financial Analysis

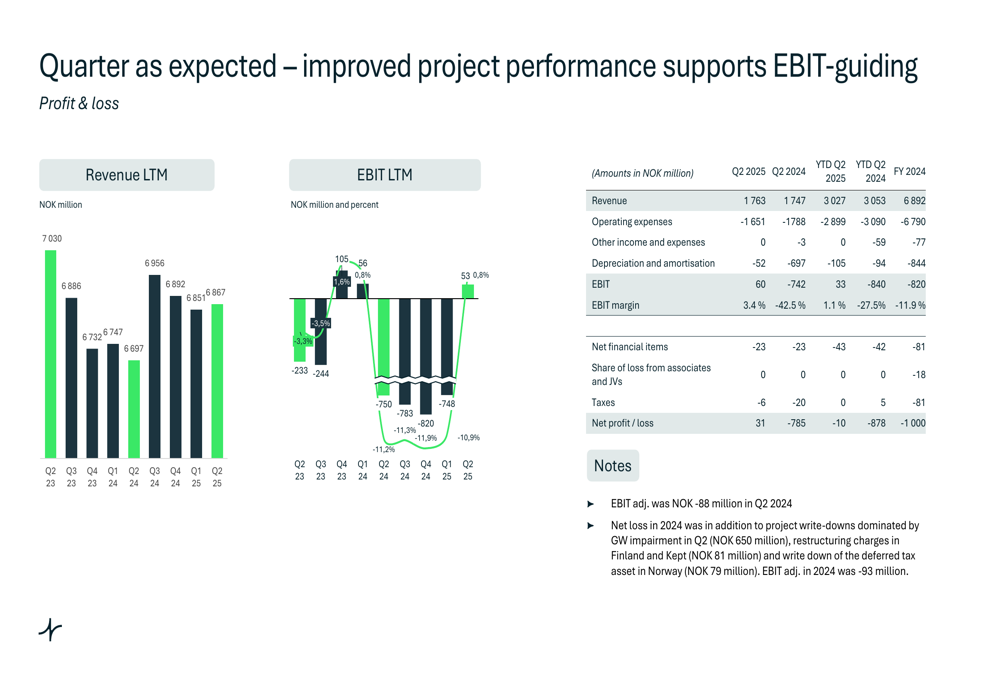

The company's long-term financial performance shows stabilizing revenue with dramatically improving profitability. Revenue on a last-twelve-months basis remained relatively flat at NOK 6,851 million in Q2 2025 compared to NOK 6,886 million in Q2 2023, while EBIT on the same basis improved from negative NOK 233 million to positive NOK 53 million.

The quarterly financial performance chart illustrates this turnaround trajectory:

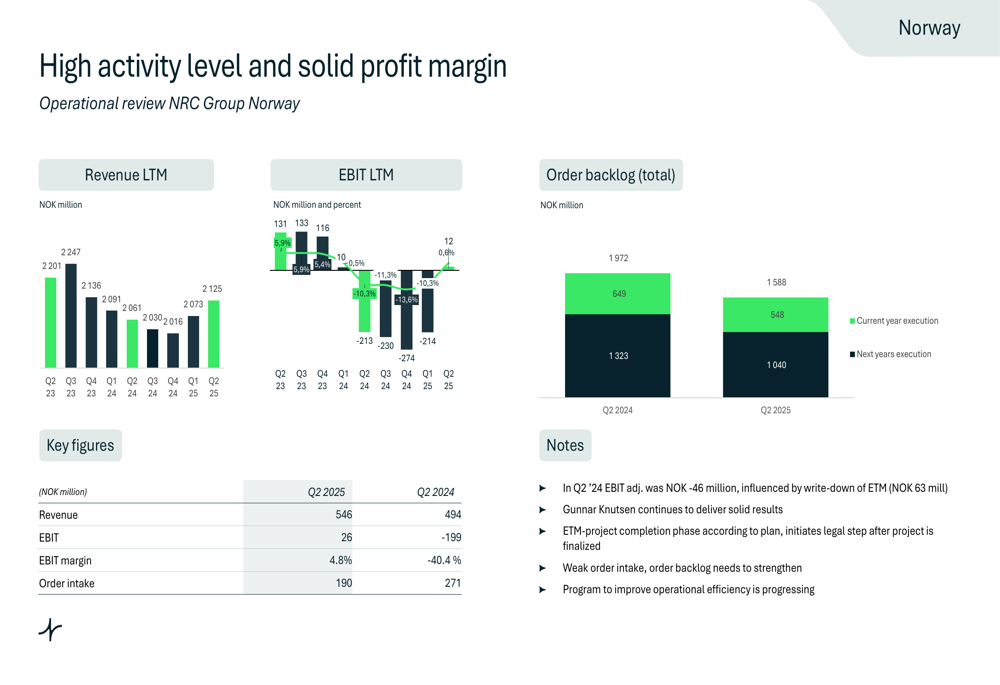

Performance varied across NRC Group's three geographic segments:

Norway operations showed improved profitability with revenue of NOK 546 million (up from NOK 494 million in Q2 2024) and EBIT of NOK 26 million (compared to negative NOK 199 million). The EBIT margin reached 4.8%, a dramatic improvement from -40.4% a year earlier. However, order intake decreased to NOK 190 million from NOK 271 million.

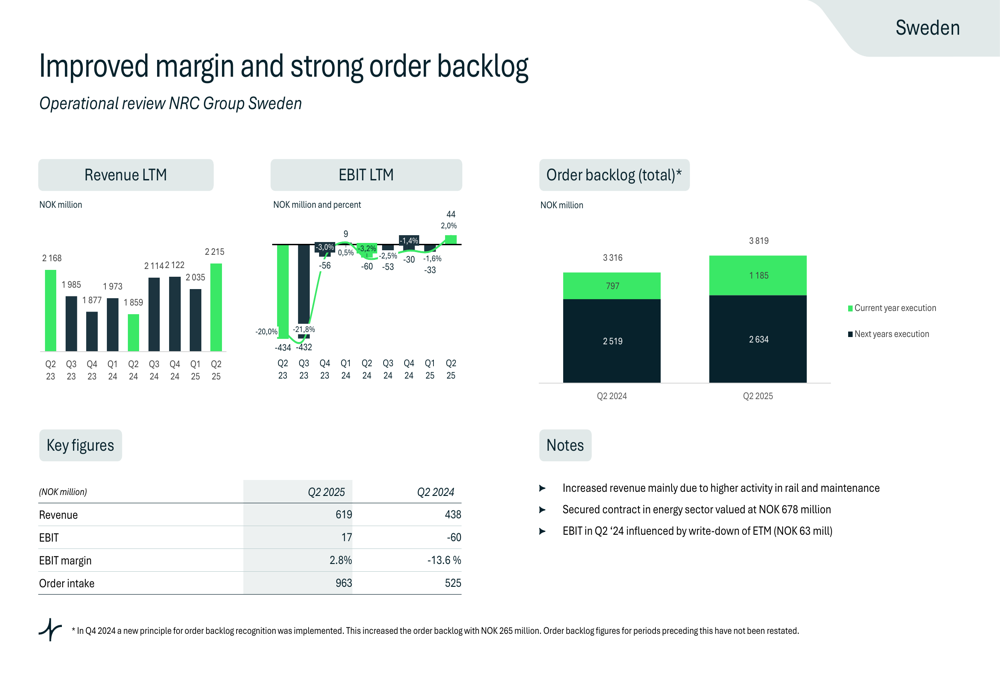

Sweden delivered the strongest growth, with revenue increasing to NOK 619 million from NOK 438 million and EBIT improving to NOK 17 million from negative NOK 60 million. The Swedish operation also secured a significant energy sector contract, contributing to an impressive order intake of NOK 963 million, nearly double the NOK 525 million from Q2 2024.

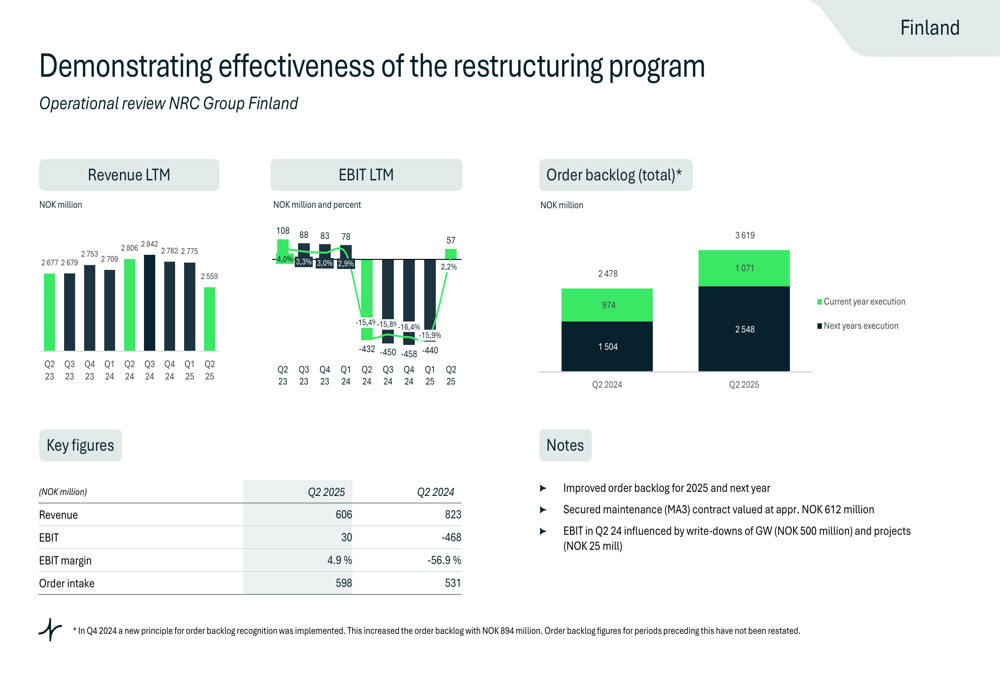

Finland showed mixed results with revenue declining to NOK 606 million from NOK 823 million, but EBIT improving substantially to NOK 30 million from negative NOK 468 million. The EBIT margin reached 4.9%, compared to -56.9% in Q2 2024. Order intake increased modestly to NOK 598 million from NOK 531 million, bolstered by a new maintenance contract.

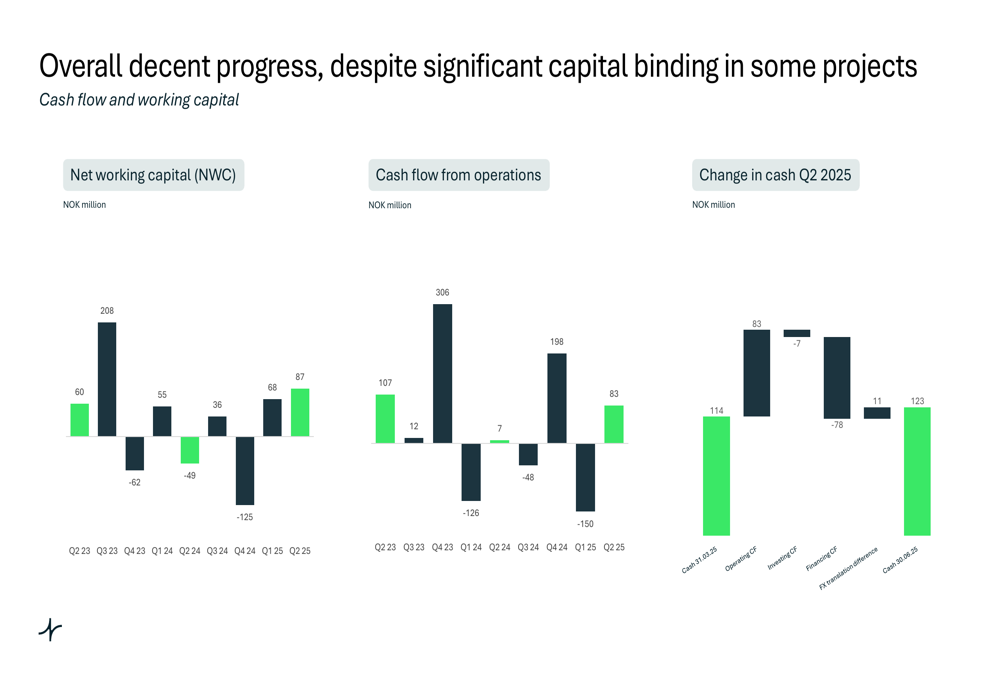

Cash flow and working capital metrics showed significant improvement. Cash flow from operations increased to NOK 198 million on a last-twelve-months basis in Q2 2025, compared to NOK 12 million in Q2 2023. The company ended the quarter with a cash balance of NOK 123 million, after operating cash flow of NOK 83 million and financing cash outflow of NOK 150 million.

Strategic Initiatives

NRC Group highlighted several strategic initiatives driving its turnaround. Cost efficiency programs are progressing as planned, contributing to margin improvements across all regions. The company is also in the completion phase of its ETM (Environmental, Technical, and Maintenance) initiative, which aims to diversify service offerings beyond traditional railway construction.

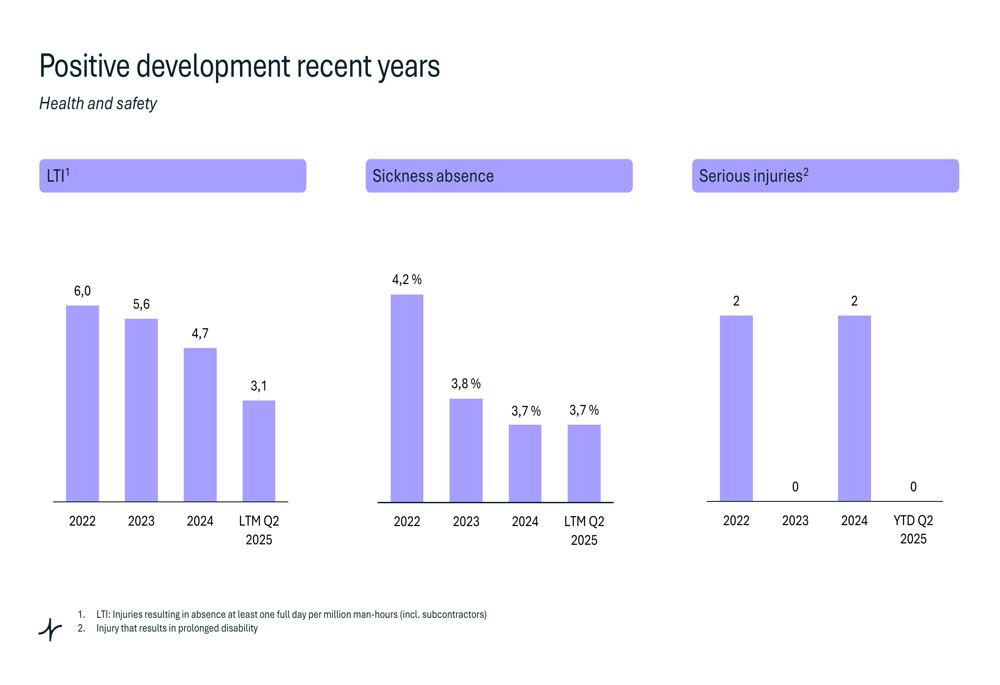

The company's health and safety performance has shown consistent improvement, with Lost Time Injury (LTI) frequency decreasing from 6.0 in 2022 to 3.1 in the last twelve months ending Q2 2025. Sickness absence has also declined from 4.2% to 3.7% over the same period, while serious injuries have been reduced to zero in 2024 and year-to-date 2025.

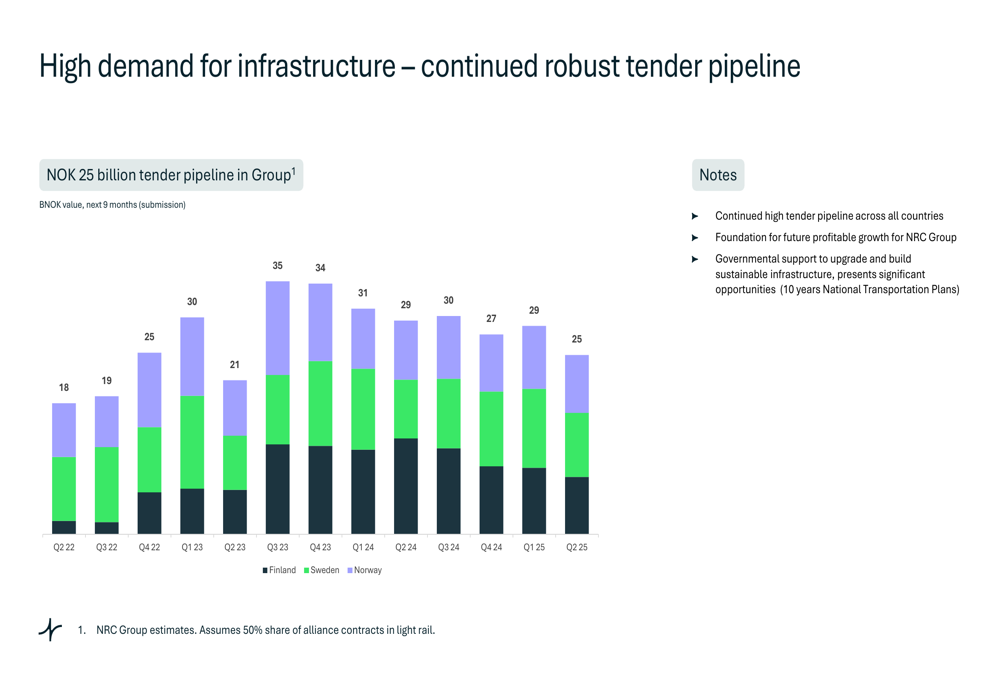

The tender pipeline remains robust at NOK 25 billion across all countries, providing opportunities for continued order intake growth. This strong pipeline is visualized in the following chart:

Forward-Looking Statements

NRC Group provided clear financial targets for the coming years. For 2025, the company expects revenue below NOK 7 billion with an EBIT margin exceeding 2.0%. Looking further ahead, targets include revenue exceeding NOK 7 billion with an EBIT margin above 3.0% in 2026, and revenue exceeding NOK 10 billion with an EBIT margin above 5.0% by 2028.

As illustrated in the company's guidance slide:

CEO Anders Gustafsson expressed confidence in achieving these targets, citing the solid order backlog as a foundation for revenue growth in 2026 and beyond. The company identified securing new contracts in Norway as a key priority, while highlighting promising tender pipelines across all three countries.

NRC Group will announce its third quarter 2025 results on November 4, 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.