How are energy investors positioned?

Introduction & Market Context

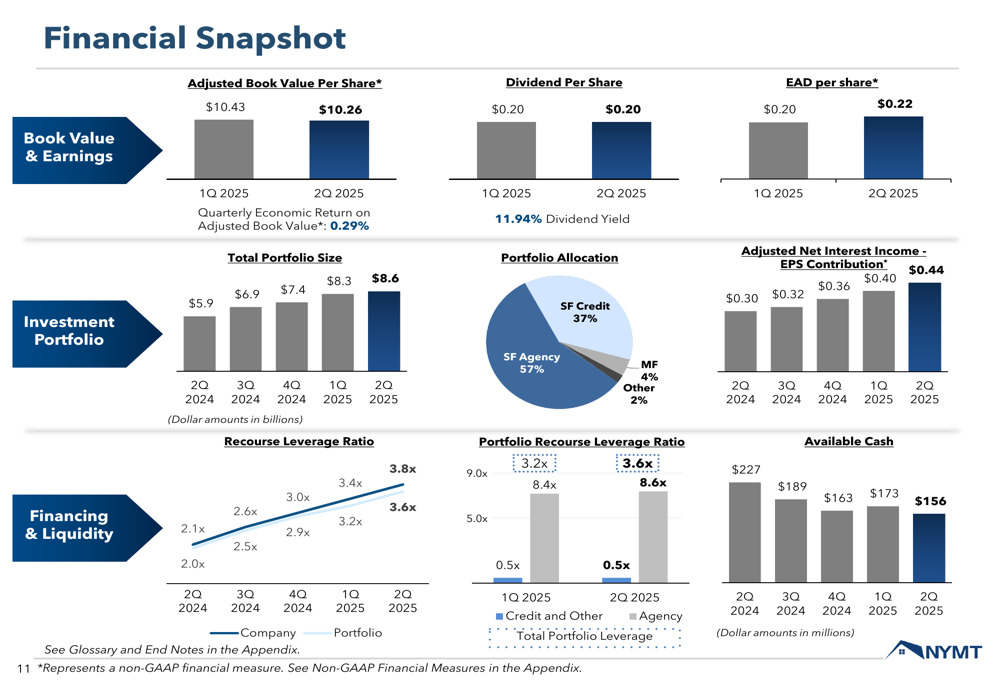

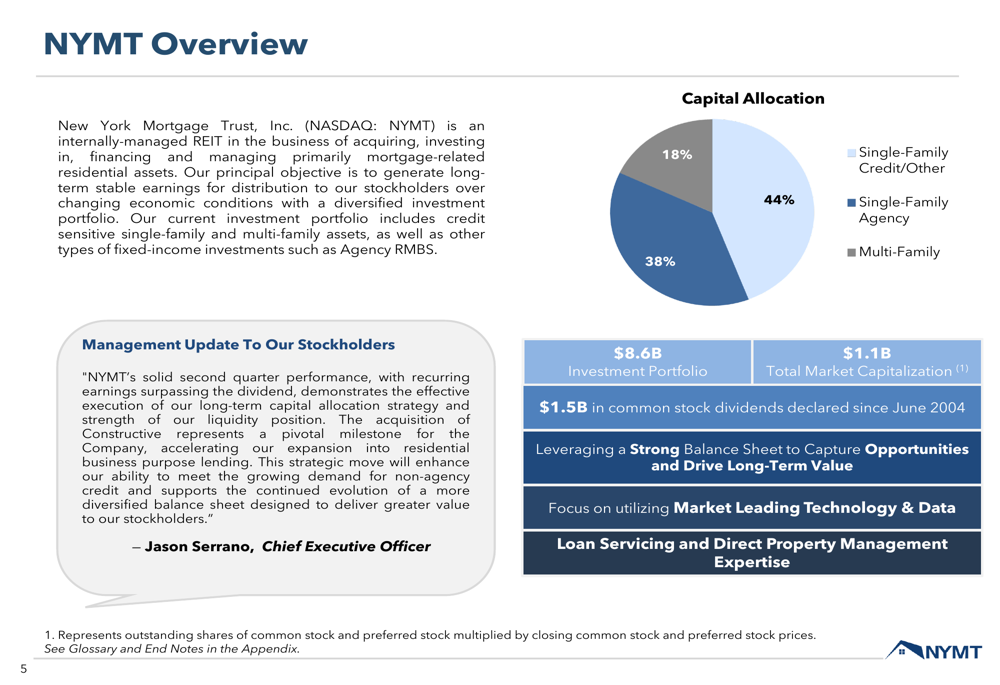

New York Mortgage Trust, Inc. (NASDAQ:NYMT) released its second quarter 2025 financial results presentation, highlighting continued growth in earnings available for distribution (EAD) despite pressure on book values. The internally-managed REIT, which focuses on mortgage-related residential assets, reported a 10% quarter-over-quarter increase in EAD per share to $0.22, while expanding its investment portfolio to $8.6 billion.

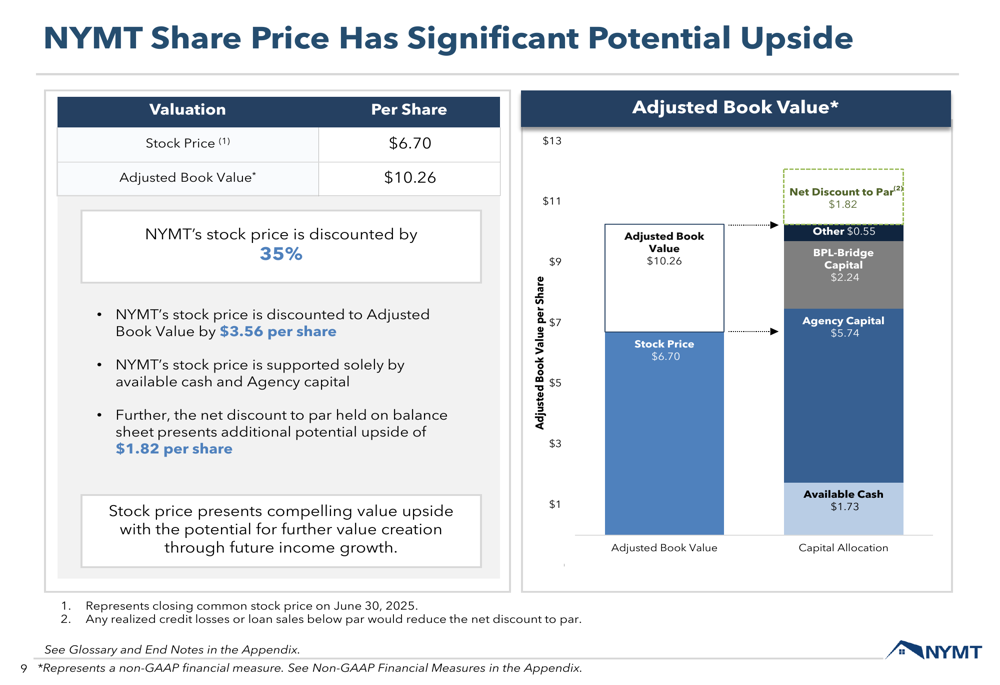

The company’s stock closed at $6.82 on July 30, 2025, trading at a significant discount to its adjusted book value of $10.26 per share. This 35% discount represents potential upside of $3.56 per share according to management’s analysis, as the company continues to execute on its strategy of deploying capital into Agency RMBS and business purpose loans.

Quarterly Performance Highlights

NYMT reported a GAAP loss per share of $(0.04) for Q2 2025, while EAD per share reached $0.22, up from $0.20 in the previous quarter. The company’s book value per share declined 2.77% quarter-over-quarter to $9.11, while adjusted book value per share fell 1.63% to $10.26. Despite these pressures, the company maintained its quarterly dividend of $0.20 per share, representing an annualized yield of 11.94%.

As shown in the following financial snapshot, NYMT has demonstrated consistent growth in its total portfolio size and adjusted interest income contribution:

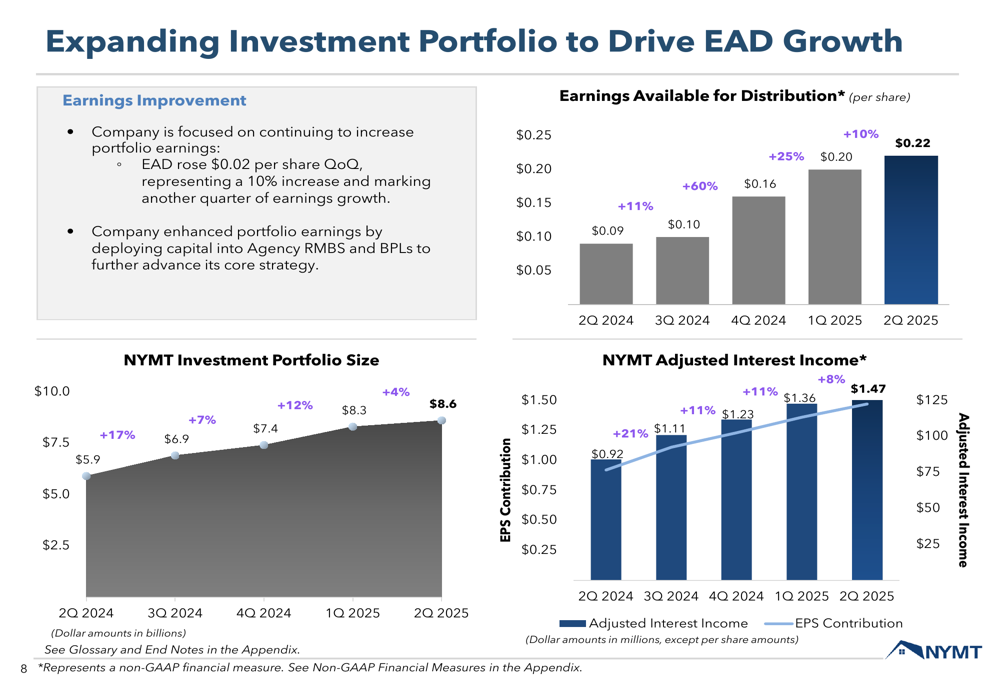

The company’s investment portfolio increased by $339 million (4%) during the quarter to reach $8.6 billion. Total (EPA:TTEF) adjusted interest income rose to $132.5 million, an 8% increase from the previous quarter. Management highlighted that the company’s focus on deploying capital into Agency RMBS and business purpose loans (BPLs) has enhanced portfolio earnings.

The following chart illustrates how NYMT’s expanding investment portfolio has driven EAD growth over the past year:

Strategic Initiatives

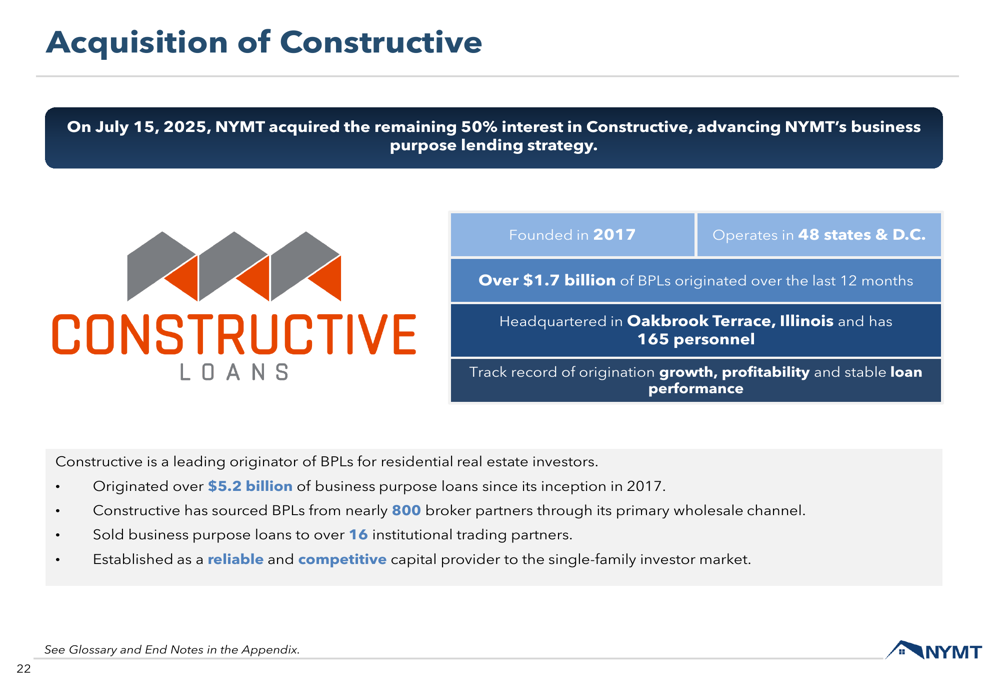

A significant development during the quarter was NYMT’s acquisition of the remaining 50% ownership stake in Constructive Loans, LLC, a business purpose loan originator. Founded in 2017, Constructive operates in 48 states and has originated over $1.7 billion of BPLs over the last 12 months.

The following image provides an overview of Constructive’s operations and scale:

CEO Jason Serrano highlighted the strategic importance of this acquisition, noting that it strengthens NYMT’s origination capabilities and provides a direct pipeline for investment opportunities. The acquisition aligns with the company’s focus on business purpose loans, which now represent a significant portion of its single-family credit portfolio.

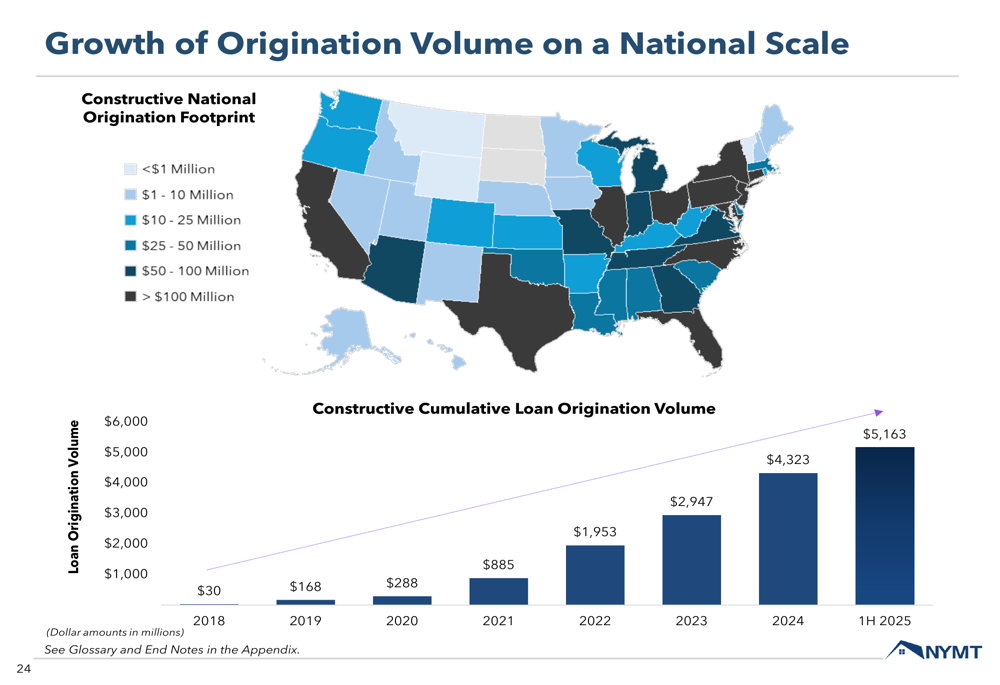

Constructive has demonstrated impressive growth in origination volume, expanding from $30 million in 2018 to over $5.1 billion in the first half of 2025:

Detailed Financial Analysis

NYMT’s capital allocation strategy continues to emphasize a balanced approach, with 44% allocated to Single-Family Credit/Other, 18% to Single-Family Agency, and 38% to Multi-Family investments. The company holds a diversified portfolio of assets across these segments:

The company’s investment activities during Q2 2025 included the acquisition of $798 million of new single-family investments, comprised of $504 million of Agency RMBS with a 5.29% average coupon and $280 million of Residential Loans (99% BPL). NYMT also reported repurchasing 231,200 shares of common stock at an average price of $6.50 per share.

Management analysis suggests significant potential upside in NYMT’s share price, as illustrated in the following chart:

Forward-Looking Statements

Looking ahead, NYMT management believes that current market conditions, characterized by low housing inventory and systemic underinvestment in U.S. housing, are supportive for home prices and rents. This environment creates opportunities for the company’s business purpose loan strategies, which focus on providing financing for real estate investors.

The company completed several financing transactions subsequent to quarter-end, including the issuance of $90 million of 9.875% senior unsecured notes due 2030 and a $370 million rated securitization with a 5.70% effective cost. These transactions enhance NYMT’s liquidity position and support future growth.

NYMT’s recourse leverage ratio increased to 3.8x at quarter-end, up from 3.2x in the previous quarter, reflecting the company’s more aggressive capital deployment strategy. The company reported excess liquidity capacity of $416 million, consisting of $156 million in cash and $260 million in available financing.

Competitive Industry Position

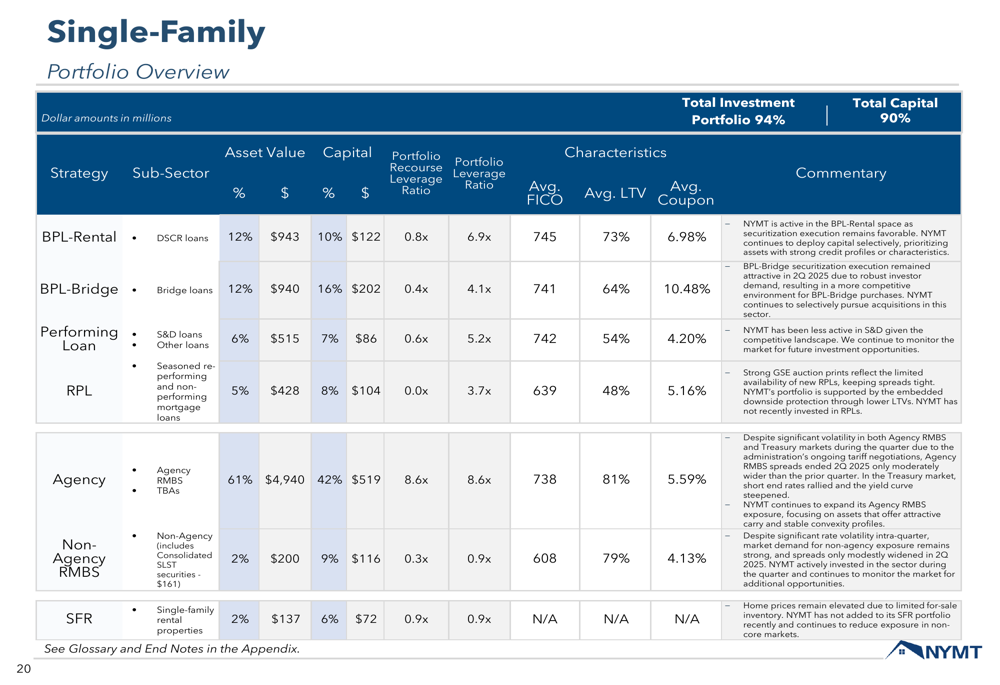

NYMT’s single-family portfolio strategy focuses on several key areas, as outlined in this overview:

The company’s acquisition of Constructive strengthens its competitive position in the business purpose loan market, providing vertical integration from origination through securitization. This integration allows NYMT to capture additional value in the investment chain while maintaining control over credit quality.

The second quarter results demonstrate NYMT’s continued progress in executing its strategic plan, with growing earnings despite book value pressure. While the stock continues to trade at a significant discount to adjusted book value, management believes this gap represents an opportunity for investors as the company continues to focus on generating long-term stable earnings through its diversified investment approach.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.