Street Calls of the Week

Introduction & Market Context

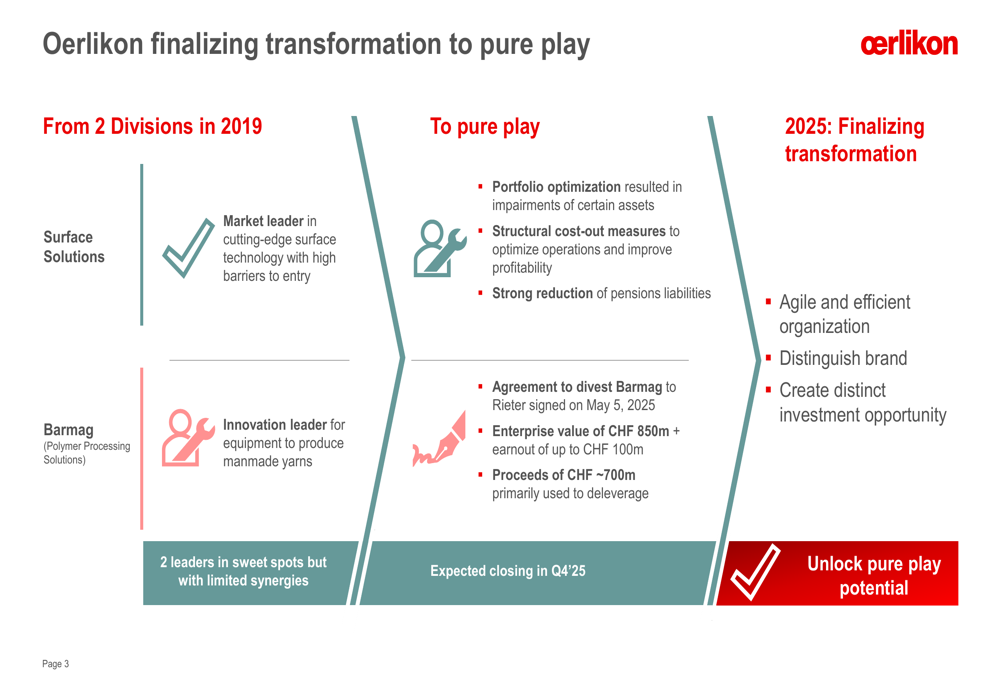

Oerlikon presented its half-year 2025 financial results on August 5, 2025, highlighting its ongoing transformation into a pure play surface solutions company while navigating challenging market conditions. The Swiss industrial group is finalizing a strategic shift that began with the company operating two distinct divisions - Surface Solutions and Barmag (Polymer Processing Solutions) - and is now moving toward a more focused business model.

The presentation comes amid a difficult business environment characterized by weak customer purchasing behavior and Euro area PMIs in contraction territory, with the exception of the aviation sector, which continues to show positive momentum.

Strategic Transformation

A central focus of Oerlikon’s presentation was its transformation journey to become a pure play surface solutions provider. The company has signed an agreement to divest its Barmag division to Rieter for an enterprise value of CHF 850 million, with a potential earnout of up to CHF 100 million. The transaction, announced on May 5, 2025, is expected to close in Q4 2025, with proceeds of approximately CHF 700 million primarily earmarked for deleveraging.

The Surface Solutions division is described as a market leader in cutting-edge surface technology with high barriers to entry, while Barmag is positioned as an innovation leader for equipment to produce manmade yarns. The company noted that while both divisions are strong in their respective markets, they offered limited synergies, driving the decision to separate them.

The transformation process has included portfolio optimization resulting in asset impairments, structural cost-cutting measures, and a significant reduction of pension liabilities. Management emphasized that the end goal is to "unlock pure play potential" through an agile and efficient organization, a distinguished brand, and a distinct investment opportunity.

Quarterly Performance Highlights

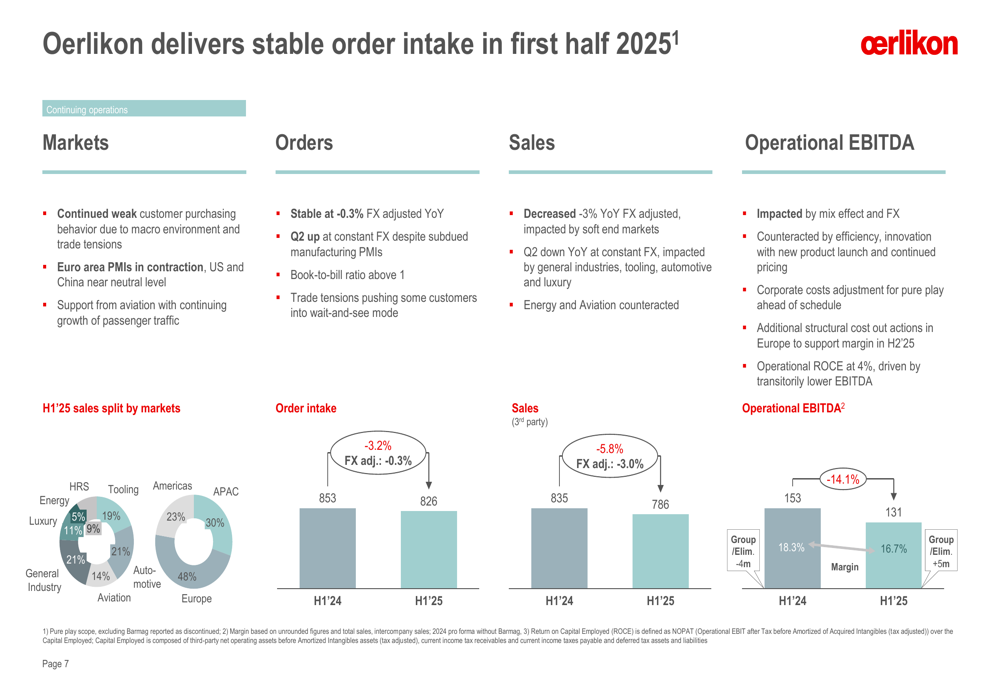

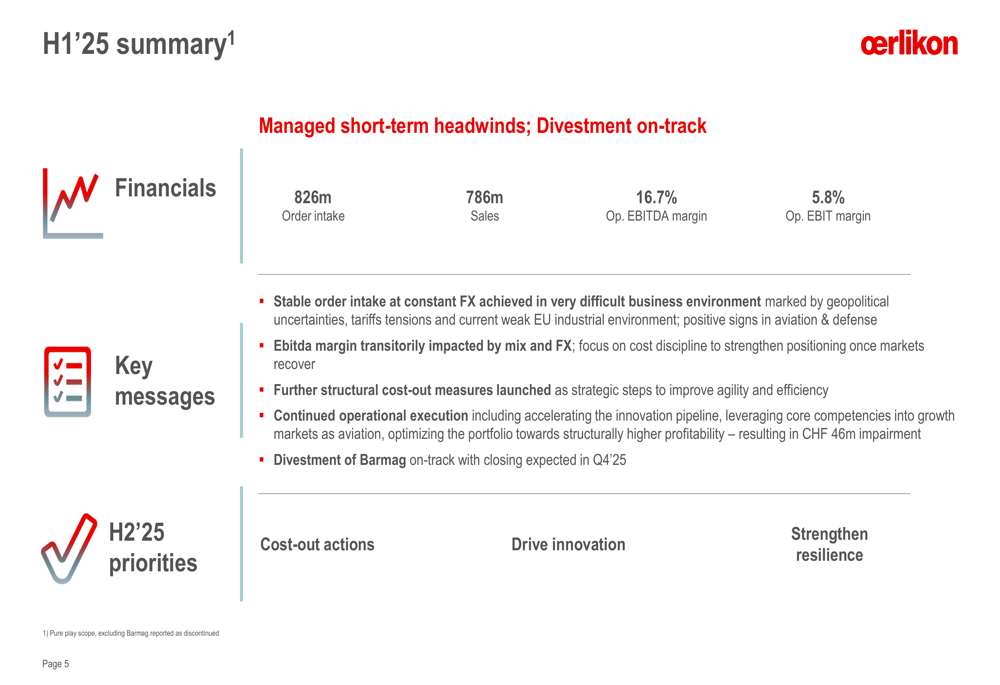

Oerlikon delivered stable order intake in the first half of 2025 despite market headwinds. The company reported order intake of CHF 826 million, representing a slight decline of 0.3% year-over-year on an FX-adjusted basis. Sales decreased by 3% year-over-year on an FX-adjusted basis to CHF 786 million, while operational EBITDA margin contracted to 16.7% from 18.3% in the same period last year.

As shown in the following chart detailing the company’s financial performance:

The operational EBITDA declined by 14.1% to CHF 131 million, impacted by an unfavorable mix effect and foreign exchange headwinds, though partially offset by efficiency measures and corporate cost adjustments. The company maintained a book-to-bill ratio above 1, suggesting potential future growth.

Meanwhile, Barmag, now classified as a discontinued operation pending its divestment, showed improved sales performance with a 9.1% increase on an FX-adjusted basis to CHF 352 million. Its order intake, while down 14.4% year-over-year, showed sequential improvement.

Detailed Financial Analysis

The company’s H1 2025 summary highlighted several key financial metrics and strategic priorities:

Oerlikon’s operational EBIT margin stood at 5.8% for the first half of 2025. The company’s Return on Capital Employed (ROCE) was calculated at 4.3%, excluding effects from amortized acquired intangibles. The presentation noted impairments related to restructuring of Nitriding activities and some R&D initiatives, as well as impairments of intangible assets mainly related to Eldim.

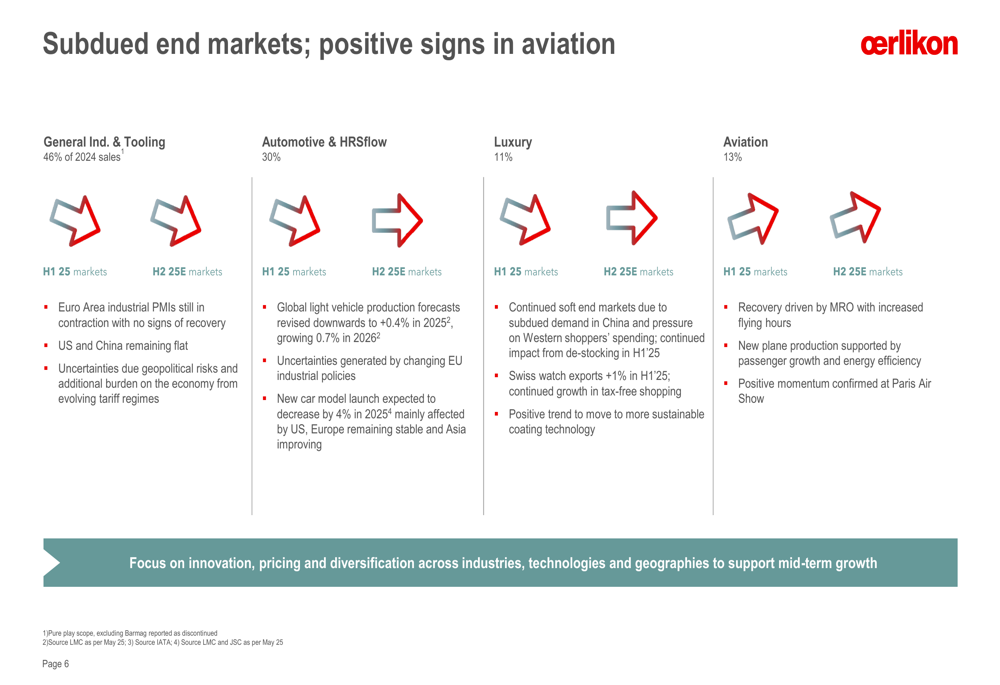

The company’s end markets showed varying performance, with General Industries & Tooling representing the largest segment at 46% of 2024 sales, followed by Automotive & HRSflow at 30%, Aviation at 13%, and Luxury at 11%. While most segments faced headwinds, Aviation stood out with positive momentum driven by increased MRO (Maintenance, Repair, and Overhaul) activity due to higher flying hours and new plane production supported by passenger growth and energy efficiency demands.

Forward-Looking Statements

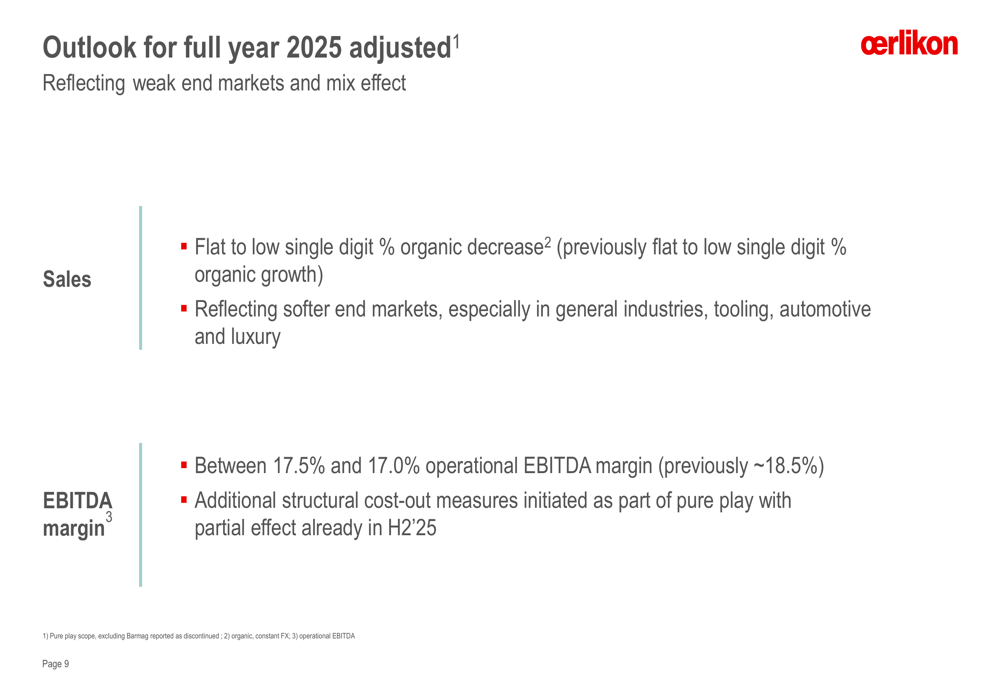

In response to the challenging market conditions, Oerlikon adjusted its full-year 2025 outlook downward:

The company now expects flat to low single-digit percentage organic sales decrease for the full year, revised from its previous guidance of flat to low single-digit percentage organic growth. This adjustment reflects softer end markets, particularly in general industries, tooling, automotive, and luxury segments.

Similarly, the operational EBITDA margin forecast was lowered to between 17.0% and 17.5%, down from the previous target of approximately 18.5%. To address these challenges, Oerlikon has initiated additional structural cost-cutting measures as part of its pure play strategy, with partial effects expected to materialize in the second half of 2025.

Strategic Initiatives

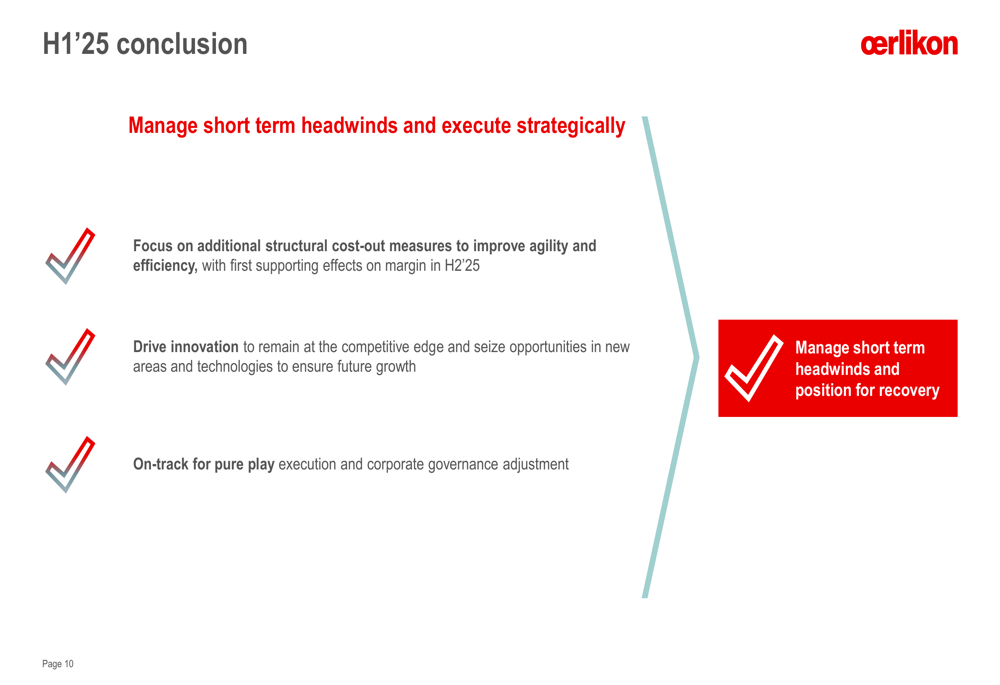

Oerlikon outlined three key priorities for the second half of 2025:

The company is focusing on implementing additional structural cost-cutting measures to improve agility and efficiency, driving innovation to maintain competitive advantage and seize opportunities in new areas and technologies, and executing its pure play strategy with corresponding corporate governance adjustments.

Management emphasized the need to "manage short-term headwinds and position for recovery," highlighting the importance of diversification across industries, technologies, and geographies to support mid-term growth. The company also stressed its continued operational execution, including accelerating the innovation pipeline.

Conclusion

Oerlikon’s H1 2025 presentation portrays a company in transition, both strategically through its transformation to a pure play surface solutions provider and operationally as it navigates challenging market conditions. While the company faces headwinds in most of its end markets, it is taking proactive measures through cost optimization and innovation focus to strengthen its resilience.

The Barmag divestment represents a significant milestone in Oerlikon’s strategic evolution, with the transaction on track for completion by the end of 2025. Despite the downward revision to its full-year outlook, the company maintains a forward-looking stance, emphasizing its positioning for eventual market recovery while implementing measures to address current challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.