Five things to watch in markets in the week ahead

Introduction & Market Context

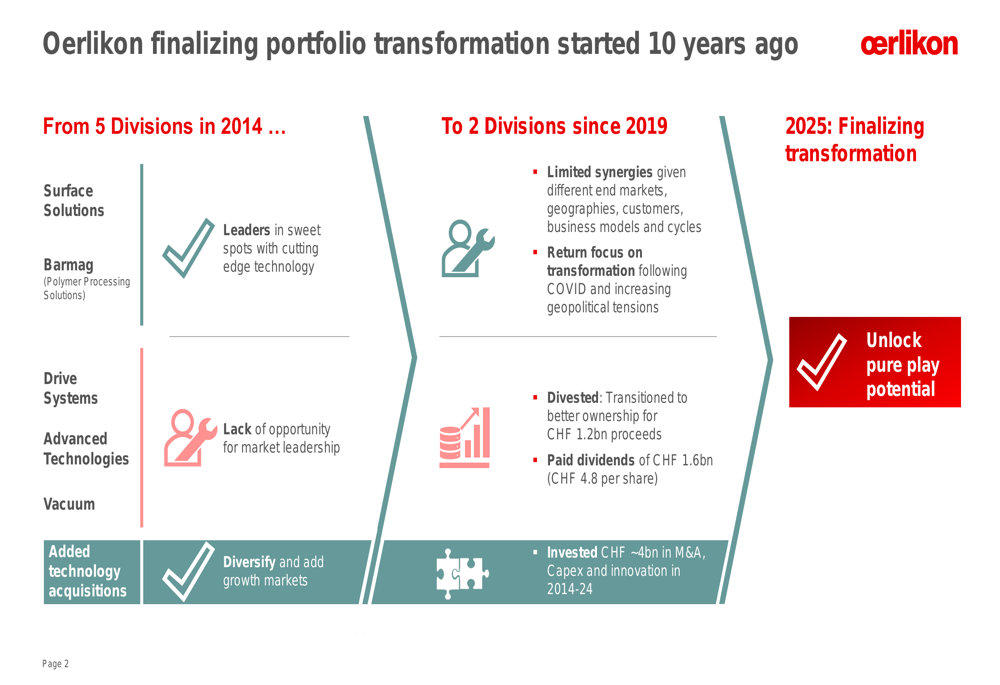

Oerlikon (SWX:OERL) unveiled plans to divest its Barmag division to Rieter for an enterprise value of CHF 850 million, potentially rising to CHF 950 million including earn-outs, according to a presentation released on May 6, 2025. The transaction marks the culmination of a decade-long portfolio transformation strategy, as the Swiss industrial group refocuses on becoming a pure-play leader in surface technology solutions.

The divestment represents a significant milestone in Oerlikon’s strategic evolution from a diversified industrial conglomerate with five divisions in 2014 to a specialized surface technology company. The company has invested approximately CHF 4 billion in M&A, capital expenditures, and innovation over the past decade while returning CHF 1.6 billion to shareholders through dividends.

As shown in the following portfolio transformation timeline:

Strategic Initiatives

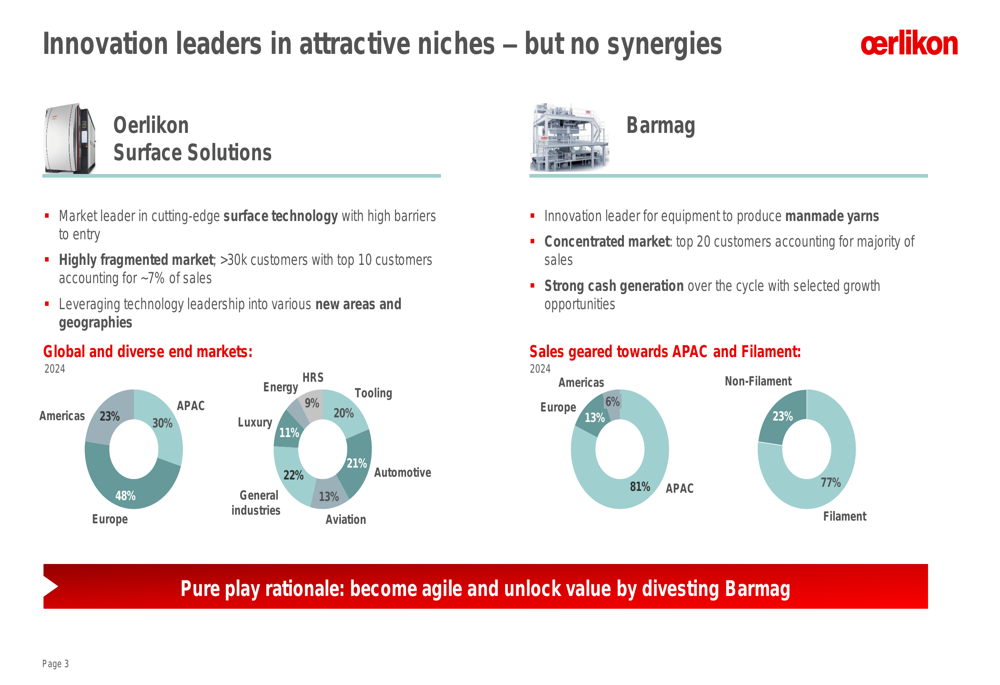

The strategic rationale for divesting Barmag centers on the limited synergies between Oerlikon’s two remaining divisions. The presentation highlighted fundamental differences in their market approaches, customer bases, and geographic focus. While Oerlikon Surface Solutions operates in a highly fragmented market with over 30,000 customers spread across Europe (48%), Asia-Pacific (30%), and the Americas (23%), Barmag is concentrated in Asia-Pacific (81%) with a customer base dominated by its top 20 clients.

The company illustrated these contrasting business models in the following comparison:

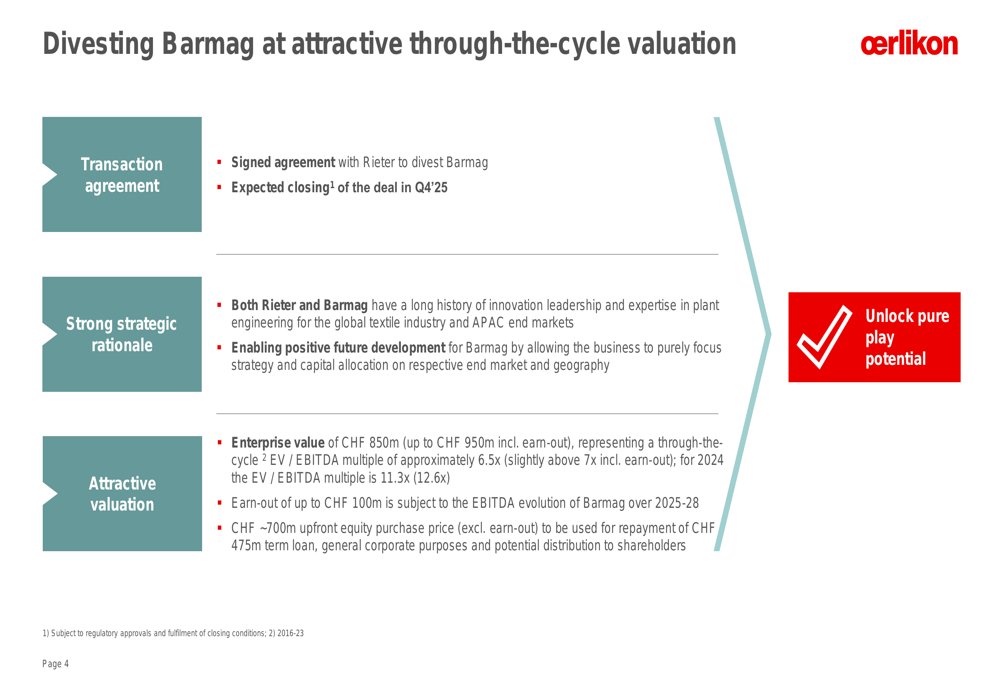

The transaction with Rieter is expected to close in Q4 2025, with Oerlikon citing strong strategic rationale for both companies. Rieter and Barmag share a history of innovation in the textile industry, and the acquisition is positioned to enable positive future development for Barmag through focused strategy and capital allocation.

The divestment terms include an attractive valuation with detailed financial parameters:

The CHF 700 million upfront equity purchase price (excluding earn-out) will be allocated to repay a CHF 475 million term loan, fund general corporate purposes, and potentially distribute capital to shareholders. The earn-out of up to CHF 100 million is contingent on Barmag’s EBITDA performance between 2025 and 2028.

Detailed Financial Analysis

The transaction values Barmag at a through-the-cycle EV/EBITDA multiple of approximately 6.5x (slightly above 7x including earn-out). Based on 2024 figures, the multiple stands at 11.3x (12.6x including earn-out), reflecting current market conditions.

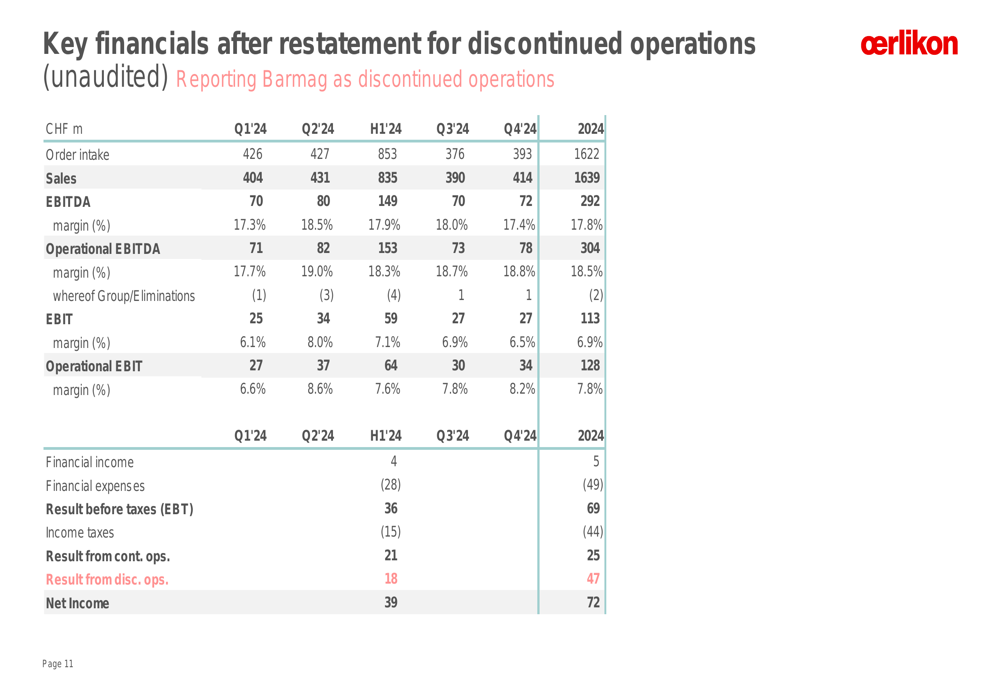

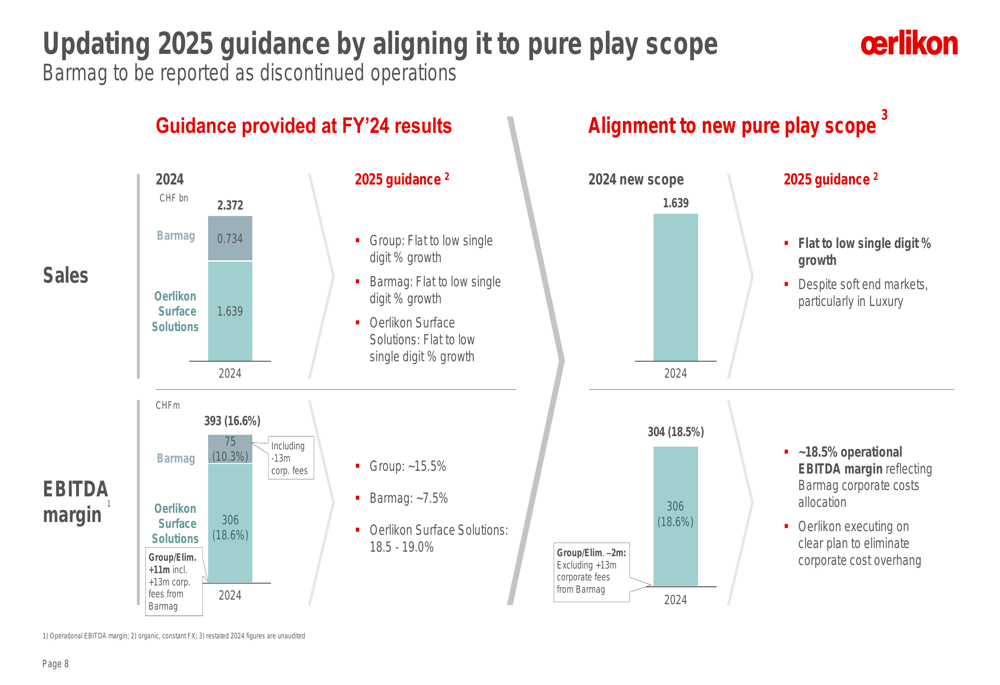

Oerlikon’s financial reporting will be restated to treat Barmag as discontinued operations. For 2024, Oerlikon Surface Solutions generated sales of CHF 1.639 billion with an EBITDA margin of 18.6%, while Barmag contributed CHF 734 million in sales with a 10.3% EBITDA margin.

The company’s post-divestment financial profile shows solid performance metrics as illustrated in this financial summary:

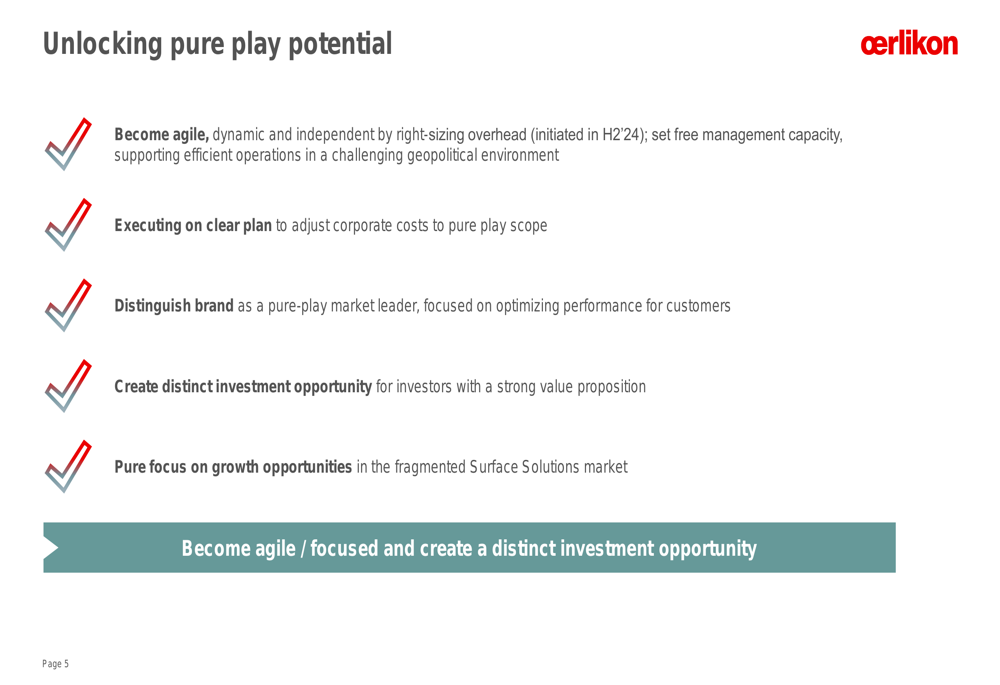

Oerlikon emphasized that becoming a pure-play company will enable it to become more agile and dynamic by right-sizing overhead costs, which the company has already initiated in the second half of 2024. Management outlined a clear plan to adjust corporate costs to align with the new, more focused business scope.

The following slide details how Oerlikon plans to unlock value through its pure-play strategy:

Competitive Industry Position

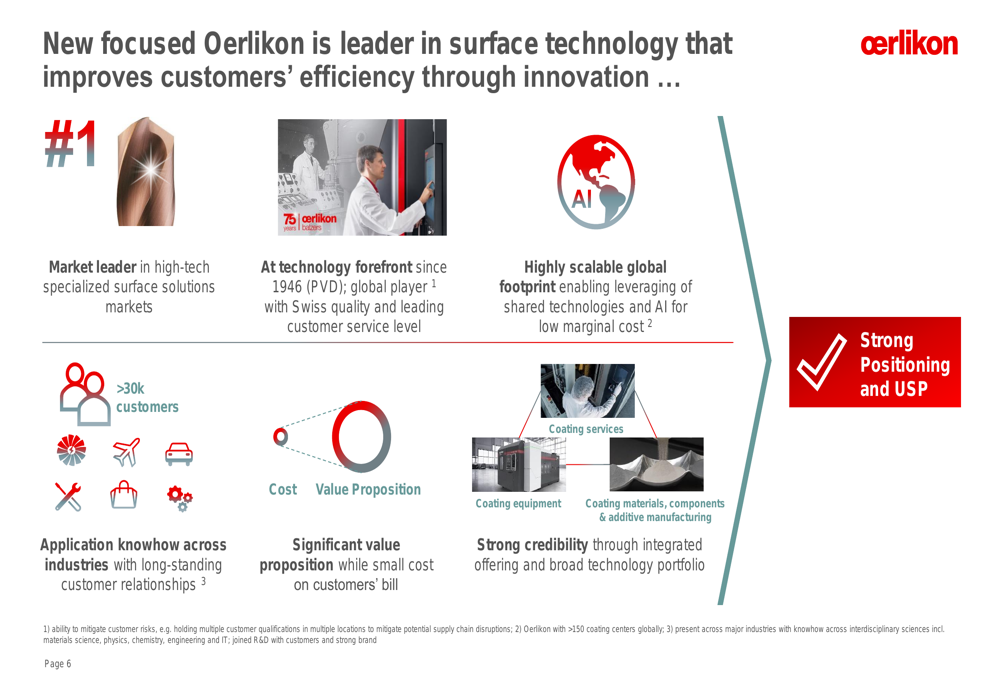

Following the divestment, Oerlikon will position itself as the market leader in high-tech specialized surface solutions. The company traces its technology leadership back to 1946 with the development of Physical Vapor Deposition (PVD) technology and emphasizes its global footprint combined with Swiss quality standards and customer service excellence.

The presentation highlighted several competitive advantages, including a scalable global infrastructure that leverages shared technologies and artificial intelligence to achieve low marginal costs. The company also emphasized its cross-industry application expertise, long-standing customer relationships, and strong value proposition despite representing a small portion of customers’ overall costs.

As shown in this competitive positioning overview:

Forward-Looking Statements

For 2025, Oerlikon provided guidance aligned with its new pure-play scope, projecting flat to low single-digit percentage growth and an operational EBITDA margin of approximately 18.5%. This margin reflects the allocation of Barmag corporate costs, with management executing a plan to eliminate corporate cost overhang.

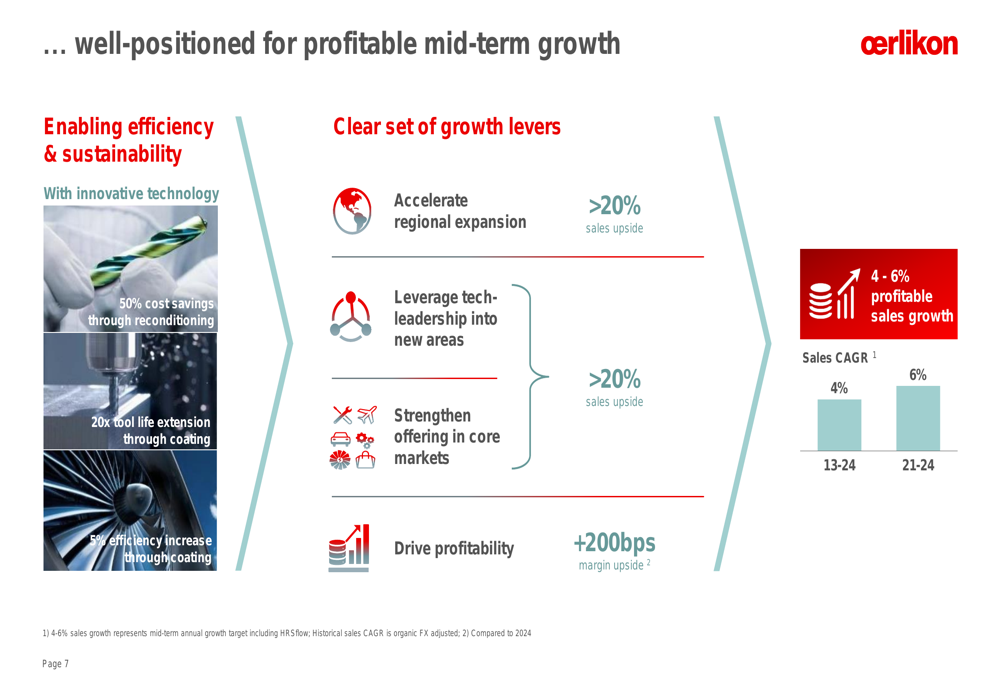

The company’s medium-term growth strategy focuses on four key levers: accelerating regional expansion (>20% sales upside potential), leveraging technology leadership into new areas (>20% sales upside), strengthening offerings in core markets (>20% sales upside), and driving profitability improvements (+200 basis points margin upside).

The following slide illustrates Oerlikon’s growth strategy:

The company’s 2025 guidance, reflecting the new pure-play structure, is detailed in this financial outlook:

Oerlikon’s transformation into a focused surface technology leader represents the final step in a decade-long portfolio restructuring. With the divestment of Barmag, the company aims to create a distinct investment opportunity for shareholders while concentrating its resources on growth opportunities in the fragmented surface solutions market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.