Can anything shut down the Gold rally?

Introduction & Market Context

Offerpad Solutions Inc (NYSE:OPAD) released its second quarter 2025 results on August 4, showing signs of improving profitability metrics despite flat revenue growth. The real estate technology company continues its strategic transition toward a diversified "Real Estate as a Service" model in a challenging housing market characterized by high mortgage rates and affordability concerns.

The company’s stock closed at $1.22 on the day of the announcement but jumped 9.84% to $1.34 in aftermarket trading, suggesting investor optimism about the improving profitability trends despite ongoing challenges.

Quarterly Performance Highlights

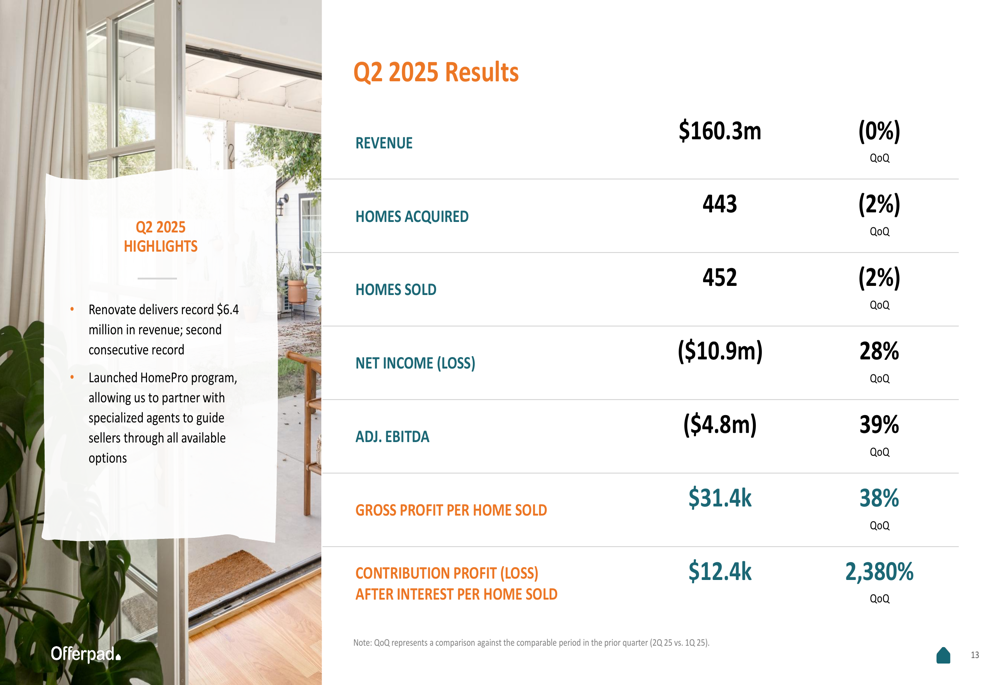

Offerpad reported Q2 2025 revenue of $160.3 million, essentially flat compared to the previous quarter. While this represents a significant decrease from the $251.1 million reported in Q2 2024, the company showed notable improvements in profitability metrics.

The company’s net loss improved to $10.9 million, a 28% improvement quarter-over-quarter, while Adjusted EBITDA loss narrowed to $4.8 million, representing a 39% sequential improvement. Gross profit per home sold increased to $31.4k, up 38% from the previous quarter.

As shown in the following results summary from the company’s presentation:

Perhaps most impressive was the dramatic improvement in contribution profit after interest per home sold, which reached $12.4k, representing a 2,380% increase from the previous quarter. This suggests Offerpad’s focus on operational efficiency and unit economics is beginning to yield results.

The company sold 452 homes during the quarter, a slight 2% decrease from Q1, while acquiring 443 new properties, also down 2% sequentially.

Strategic Initiatives

Offerpad continues to evolve its business model beyond traditional iBuying toward a more diversified "Real Estate as a Service" approach. The company’s presentation highlighted its expanding product ecosystem, which includes Cash Offers, Direct+ (listing services), Renovate (renovation services), and HomePro (agent partnerships).

The company’s product ecosystem is designed with interconnected services that create multiple revenue streams:

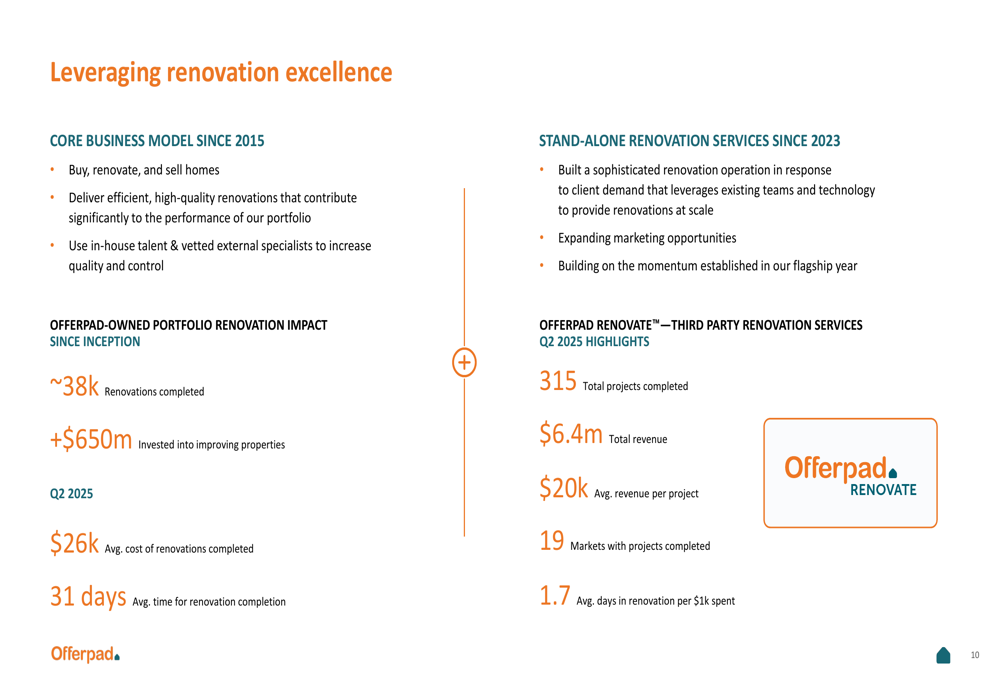

A notable bright spot in Q2 was Offerpad’s renovation business, which delivered record revenue of $6.4 million, marking the second consecutive record quarter for this segment. The company completed 315 renovation projects with an average revenue of $20k per project across 19 markets.

The renovation business leverages Offerpad’s existing expertise, as illustrated in the presentation:

Offerpad also announced the launch of its HomePro program, which aims to expand its partner ecosystem through broker partnerships, agent referrals, and homebuilder services. This initiative aligns with the company’s goal of increasing market penetration while maintaining a capital-efficient approach.

Detailed Financial Analysis

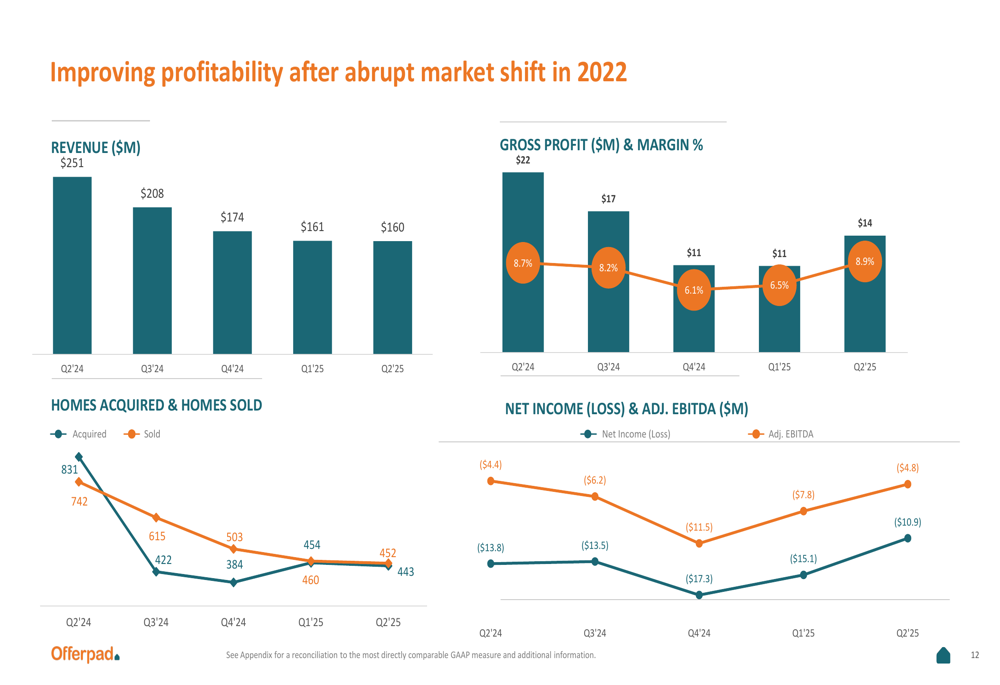

The company’s financial performance shows a clear trend of improving profitability metrics despite revenue challenges. The presentation highlighted five consecutive quarters of data, revealing how Offerpad has navigated the market shift since 2022:

Gross profit margin improved to 8.9% in Q2 2025, up from 6.5% in the previous quarter and returning to levels similar to mid-2024. This improvement suggests the company is becoming more efficient in its core operations and pricing strategy.

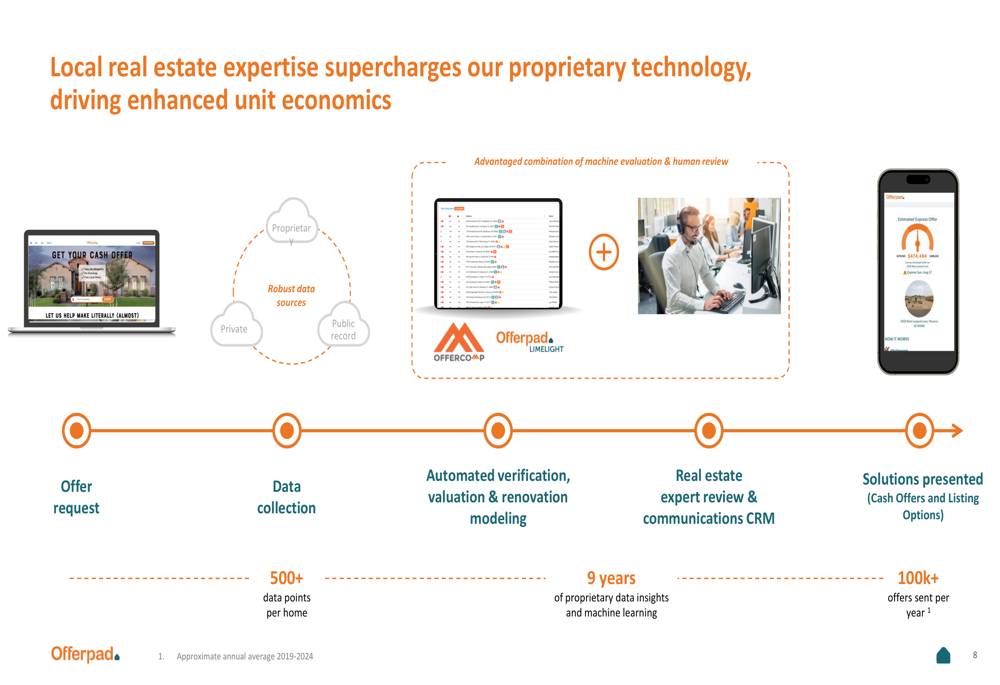

Offerpad’s technology-driven approach to real estate transactions is central to its unit economics. The company leverages data analytics and machine learning to improve valuation accuracy and operational efficiency:

According to the presentation, Offerpad collects over 500 data points per home and has accumulated nine years of proprietary data insights. This data-driven approach helps the company make more accurate offers and renovation estimates, potentially contributing to the improved gross profit per home.

Forward-Looking Statements

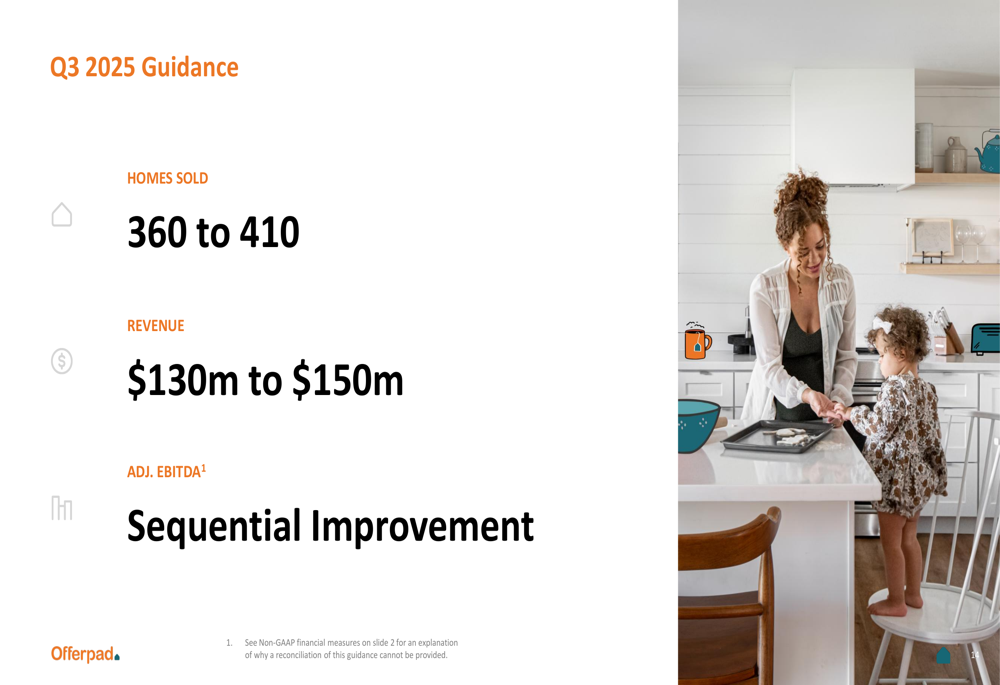

For Q3 2025, Offerpad provided guidance of 360 to 410 homes sold and revenue between $130 million and $150 million. The company also expects sequential improvement in Adjusted EBITDA, continuing the positive trend seen in Q2.

The guidance suggests a potential decrease in transaction volume compared to Q2, but the company’s focus on profitability improvement appears to remain intact.

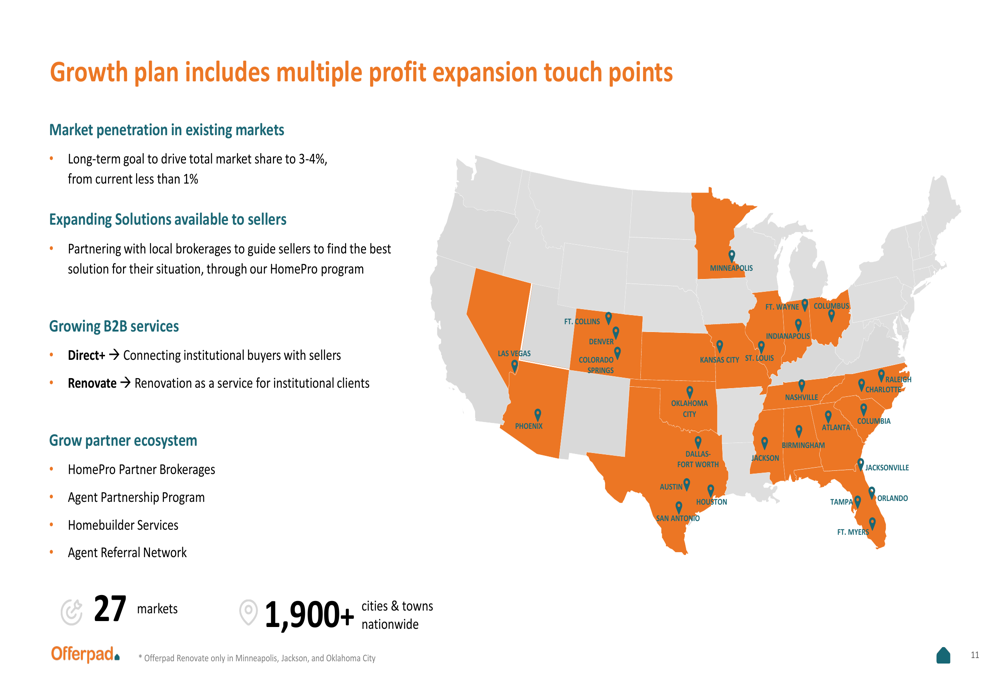

Longer-term, Offerpad aims to increase its market share from less than 1% currently to 3-4% in its existing markets. The company’s growth plan includes deeper market penetration, expanding solutions for sellers, growing B2B services, and expanding its partner ecosystem.

The real estate market opportunity remains substantial, with Offerpad estimating a $1.9 trillion total market that is still 99% non-digital. Within that, the company identifies its current addressable market ("Buy Box") at $1.1 trillion, suggesting significant room for growth if it can successfully execute its strategy.

Competitive Industry Position

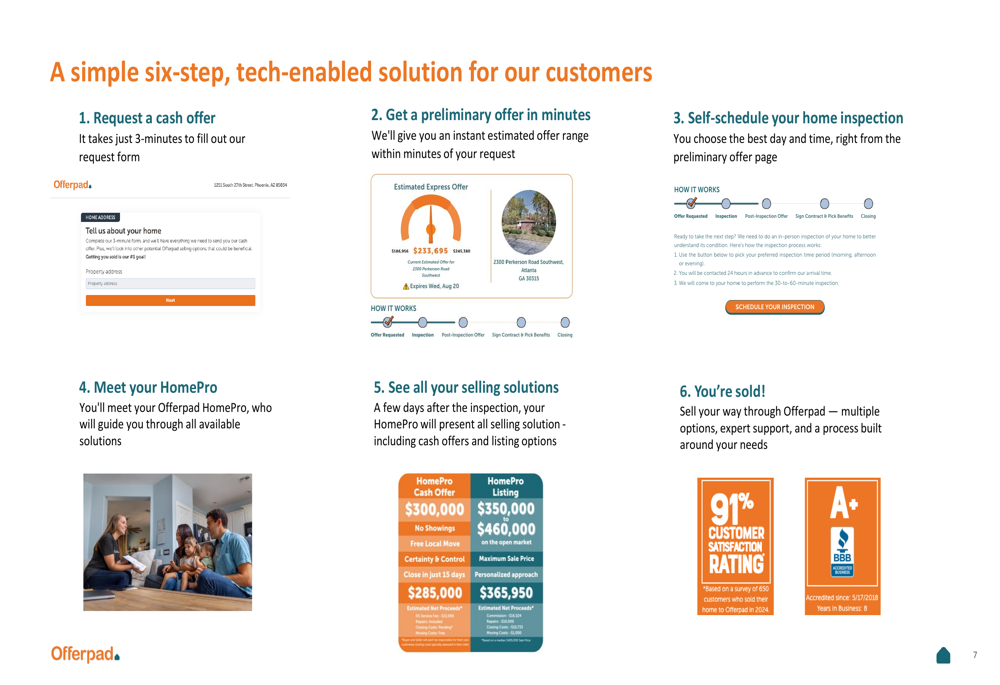

Offerpad positions itself as a technology-enabled real estate platform that offers multiple solutions to homeowners. The company’s customer journey emphasizes convenience and flexibility:

With a 91% customer satisfaction rating and an A+ BBB rating, Offerpad appears to be delivering on its customer experience promises. The company’s platform allows customers to request cash offers in just three minutes and receive preliminary offers almost instantly, addressing the friction points in traditional real estate transactions.

As the real estate market continues to face challenges from high interest rates and affordability concerns, Offerpad’s multi-solution approach may provide more flexibility than pure-play iBuyers. The company’s strategic shift toward service-oriented, asset-light business lines could help it navigate market volatility while building toward long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.