Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

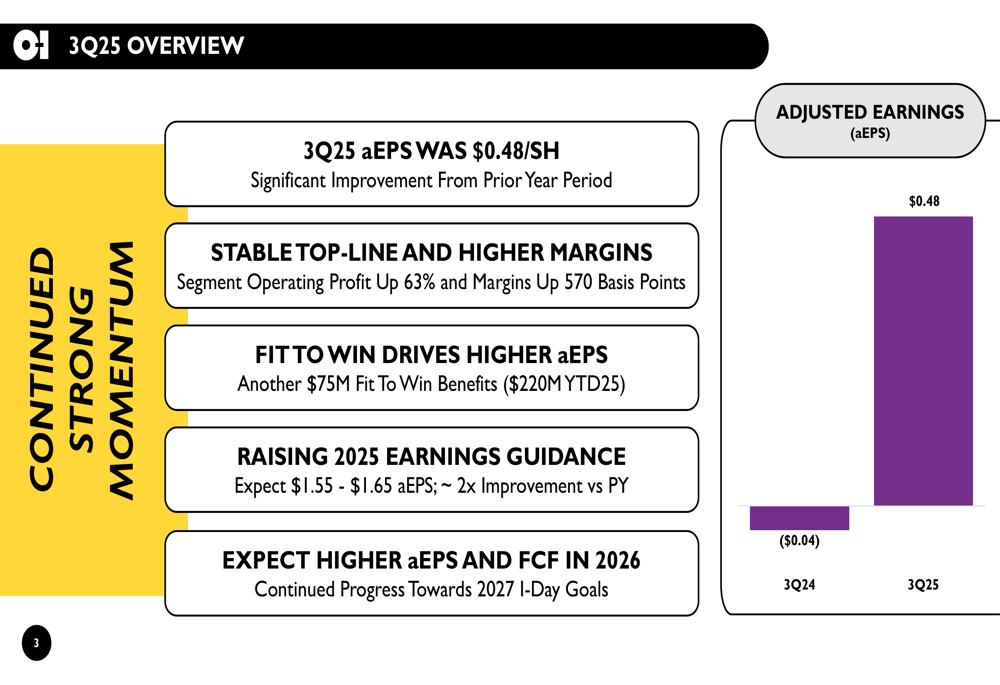

O-I Glass Inc (NYSE:OI) presented its third quarter 2025 earnings results on November 5, revealing a dramatic improvement in profitability despite stable revenue. The glass packaging manufacturer reported adjusted earnings per share of $0.48, significantly outperforming the -$0.04 recorded in the same period last year and exceeding analyst expectations of $0.42. The strong results triggered a notable market response, with shares surging 11.78% to close at $13.19, after climbing as high as $13.05 in premarket trading.

The company's performance comes amid evolving glass demand trends, which management categorized as both cyclical (short-term) and structural (long-term) in nature. Despite these market dynamics, O-I Glass has maintained stable revenue while substantially improving margins through its cost-cutting initiatives.

Quarterly Performance Highlights

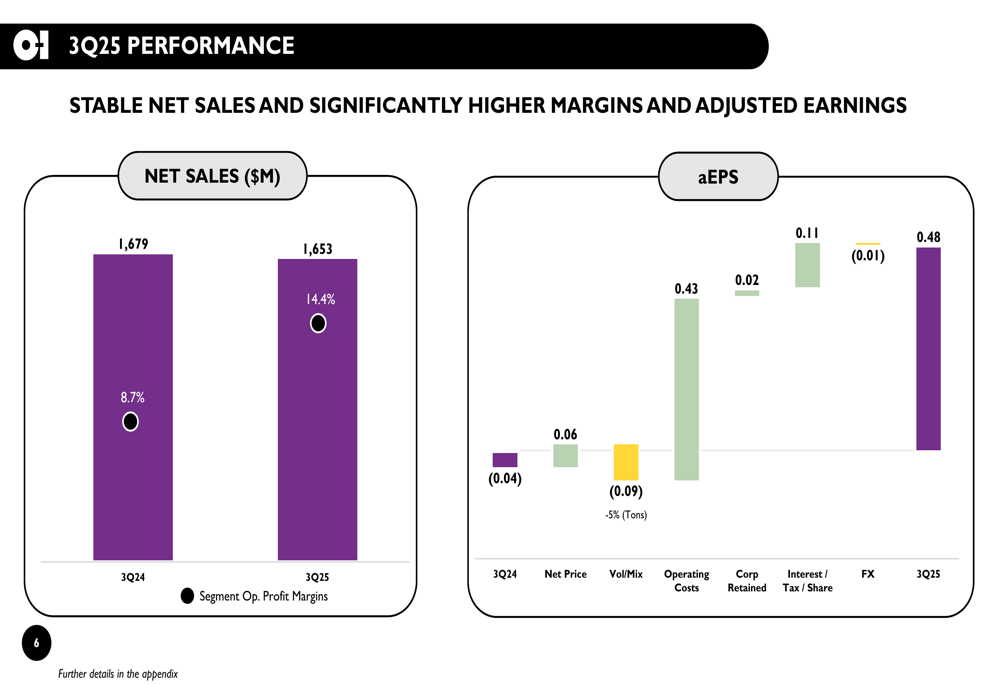

O-I Glass delivered stable net sales of $1.65 billion in Q3 2025, compared to $1.68 billion in the same quarter last year. The real story, however, was the company's dramatic improvement in profitability metrics. Segment operating profit margins increased to 14.4% from 8.7% in Q3 2024, representing a 570 basis point improvement.

As shown in the following performance overview chart, adjusted EPS increased dramatically from -$0.04 in Q3 2024 to $0.48 in Q3 2025:

This twelve-fold improvement in adjusted EPS was achieved despite relatively flat sales, highlighting the company's successful focus on operational efficiency and cost management. The quarter's performance was primarily driven by improved pricing, substantial cost reductions, and favorable interest and tax impacts, partially offset by slightly negative volume/mix effects.

A detailed breakdown of the EPS bridge shows the primary contributors to this improvement:

Fit to Win Program Success

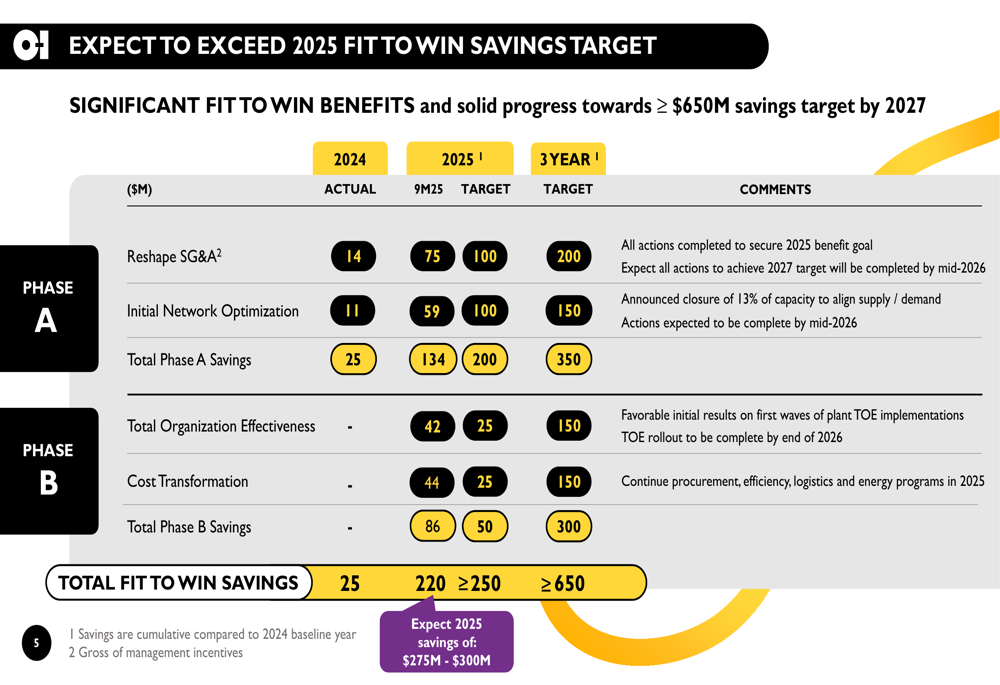

The cornerstone of O-I Glass's improved performance has been its "Fit to Win" cost-saving initiative, which delivered another $75 million in benefits during the third quarter, bringing year-to-date savings to $220 million. The company now expects to exceed its 2025 target of $250 million in savings.

As illustrated in the following chart, O-I Glass has made substantial progress across multiple cost-saving categories:

The program focuses on four key areas: reshaping SG&A expenses, network optimization, organizational effectiveness, and cost transformation. With $220 million already achieved in the first nine months of 2025, the company is well on track to meet or exceed its three-year target of at least $650 million in savings by 2027.

CEO Gordon Hardie emphasized during the earnings call that the company is "only focused on volume that delivers economic profit," highlighting the strategic shift toward higher-margin business rather than pursuing volume growth at the expense of profitability.

Segment Performance

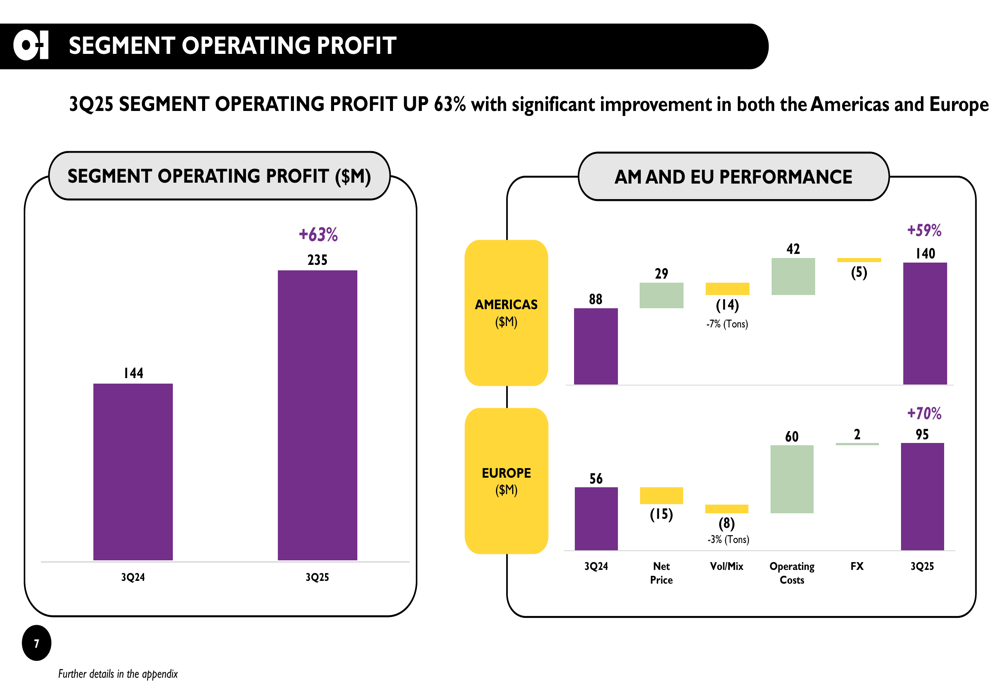

Both of O-I Glass's major geographic segments contributed to the improved performance. The Americas segment operating profit increased from $88 million in Q3 2024 to $140 million in Q3 2025, while Europe's profit grew from $56 million to $95 million during the same period.

The following chart details the segment operating profit improvements and their drivers:

Total segment operating profit increased by 63% year-over-year, from $144 million to $235 million. Both regions benefited from improved pricing and cost reductions, though volume/mix impacts varied by region. The consistent improvement across both major geographic segments demonstrates the broad-based effectiveness of the company's strategic initiatives.

Updated Guidance and Future Outlook

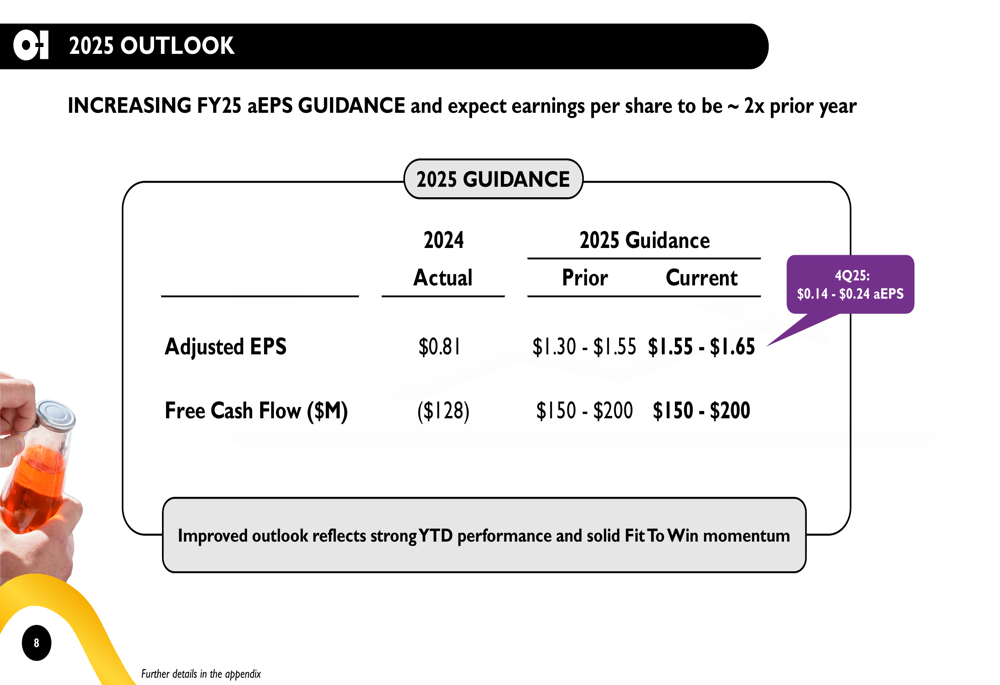

Based on the strong year-to-date performance, O-I Glass has raised its full-year 2025 adjusted EPS guidance to $1.55-$1.65, up from the previous range of $1.30-$1.55. This represents approximately double the adjusted EPS of $0.81 achieved in 2024.

The company's updated outlook is presented in the following chart:

Free cash flow for 2025 is expected to be between $150 million and $200 million, while fourth-quarter adjusted EPS is projected at $0.14-$0.24. The improved outlook reflects both the strong year-to-date performance and continued momentum from the Fit to Win program.

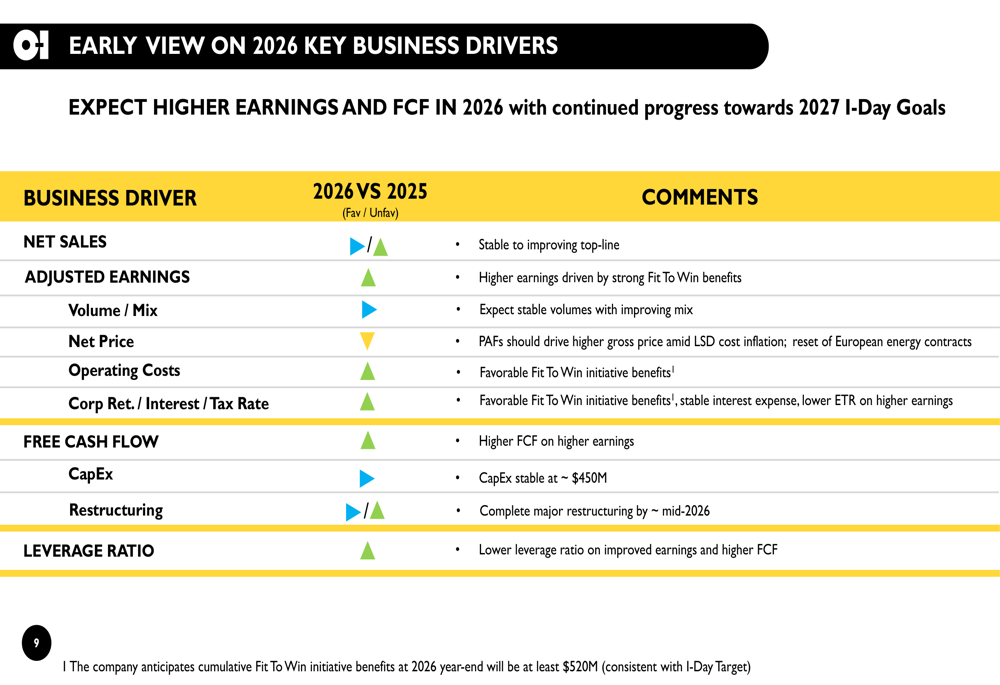

Looking ahead to 2026, O-I Glass provided an early view of key business drivers, indicating expectations for higher earnings and free cash flow:

The company anticipates stable to improving net sales, favorable pricing trends, and continued benefits from the Fit to Win program in 2026. These factors are expected to more than offset potential headwinds from energy contract resets, which management identified as a $150 million challenge during the earnings call.

Conclusion

O-I Glass's third quarter 2025 results demonstrate the effectiveness of its strategic shift toward margin improvement and cost efficiency rather than volume growth. The dramatic improvement in profitability despite stable revenue highlights the success of the Fit to Win program, which continues to exceed expectations.

With raised guidance for 2025 and a positive outlook for 2026, O-I Glass appears well-positioned to continue its earnings growth trajectory. The company's focus on economically profitable volumes, operational efficiency, and strategic cost management has resonated with investors, as evidenced by the strong market response to these results.

The glass manufacturer's performance is particularly notable given the challenging market environment, with soft consumer demand in beer and wine categories. Management's disciplined approach to capacity management and focus on high-margin business segments has enabled the company to thrive despite these headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.