Bank of America just raised its EUR/USD forecast

Introduction & Market Context

Okta Inc (NASDAQ:OKTA) released its Q1 FY26 financial results on May 27, 2025, showing continued revenue growth and significant margin expansion as the identity security provider maintains its focus on profitability. Despite a challenging after-hours market reaction with shares dropping 11.59%, the company delivered solid financial performance with revenue growing 12% year-over-year.

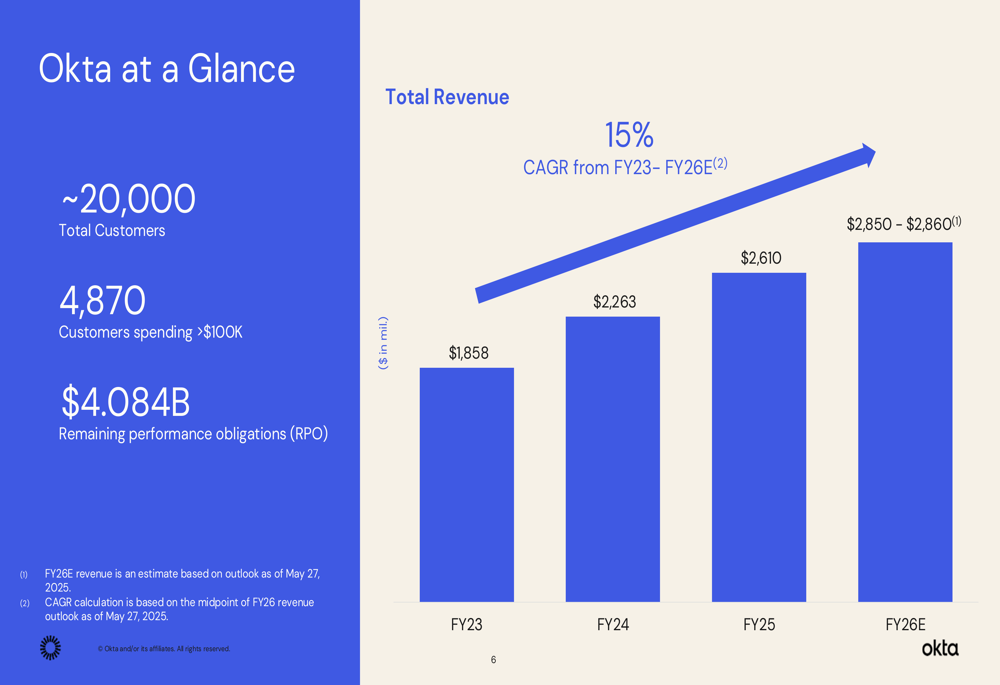

The identity security specialist, which serves approximately 20,000 customers, continues to position itself as a comprehensive solution provider in an estimated $80 billion total addressable market. Okta’s presentation emphasized its dual approach of securing workforce identities with its core platform while addressing customer identity needs through its AuthO offering.

As shown in the following snapshot of Okta’s key metrics:

Quarterly Performance Highlights

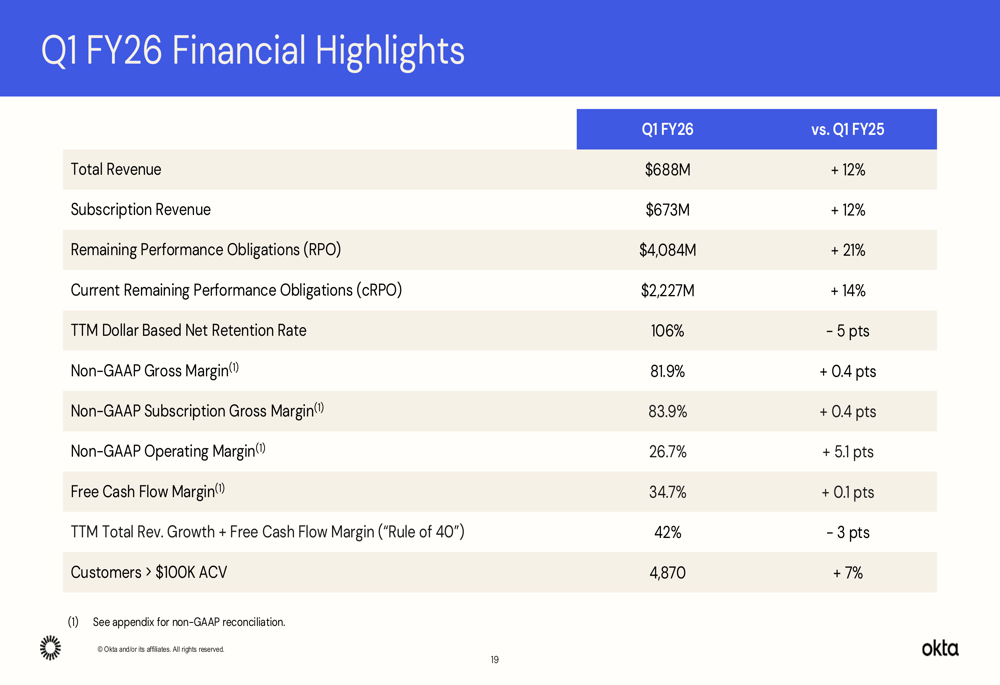

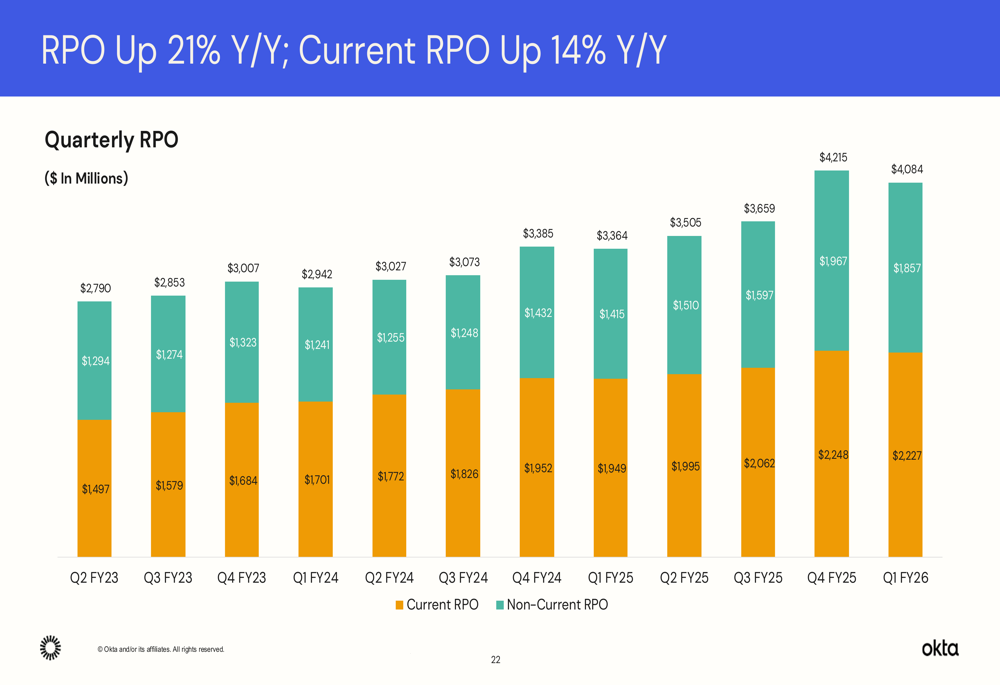

Okta reported Q1 FY26 total revenue of $688 million, representing 12% year-over-year growth, with subscription revenue accounting for $673 million of that total. The company’s remaining performance obligations (RPO) – a key indicator of future revenue – grew 21% year-over-year to $4.08 billion, while current RPO increased 14% to $2.23 billion.

The following comprehensive financial highlights demonstrate Okta’s performance across key metrics:

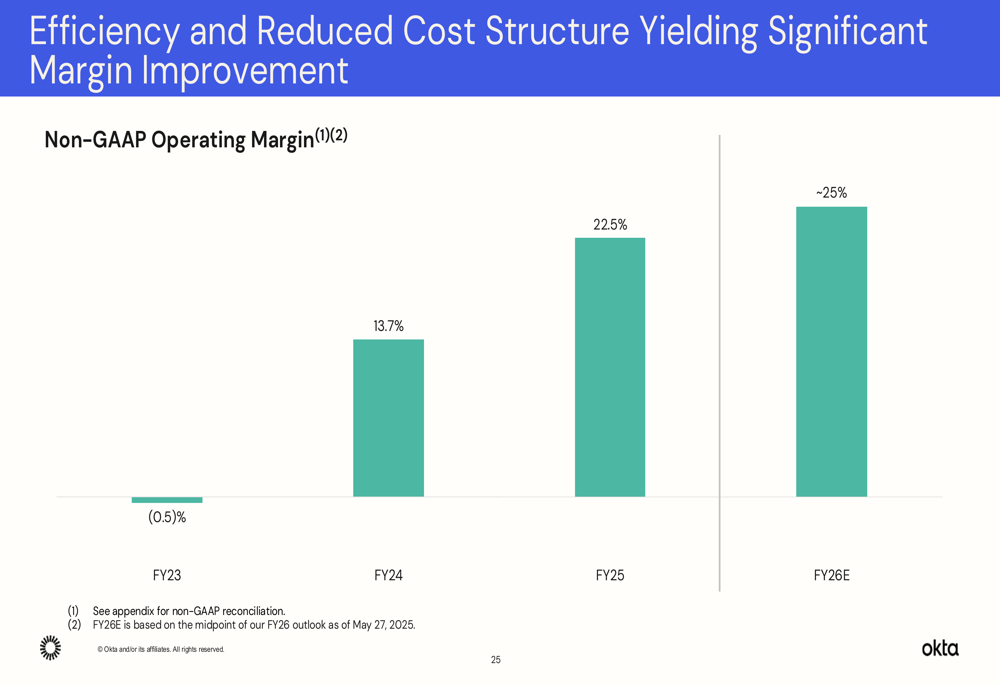

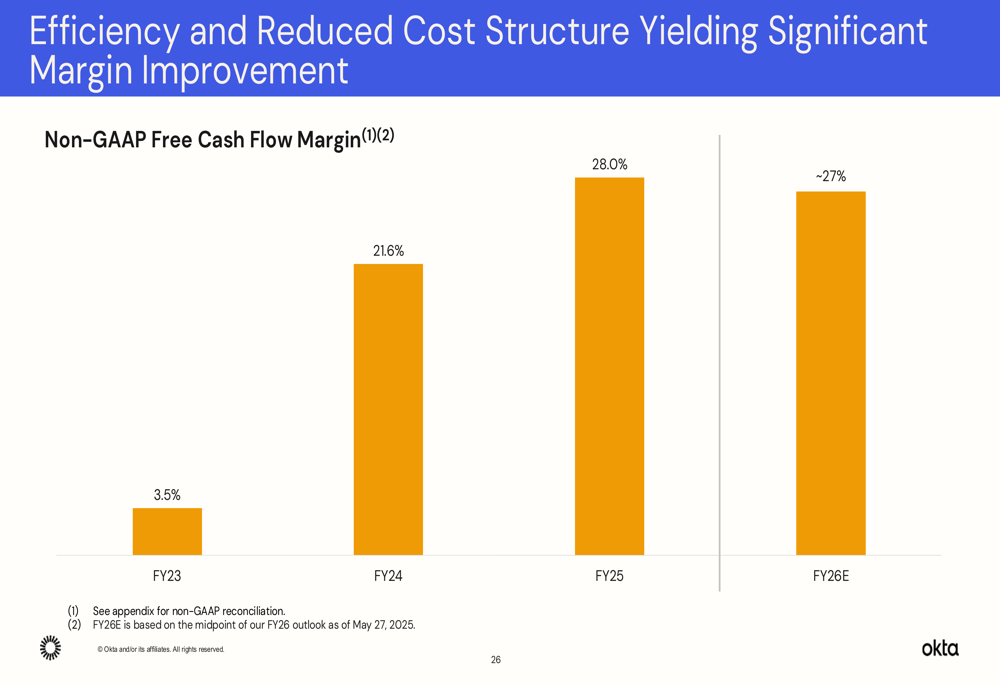

Particularly noteworthy was Okta’s continued margin expansion, with non-GAAP operating margin reaching 26.7%, a 5.1 percentage point improvement compared to the same period last year. Free cash flow margin remained strong at 34.7%, essentially flat year-over-year. The company’s "Rule of 40" metric, which combines total revenue growth and free cash flow margin, stood at a healthy 42%, though this represented a 3-point decline from the previous year.

Detailed Financial Analysis

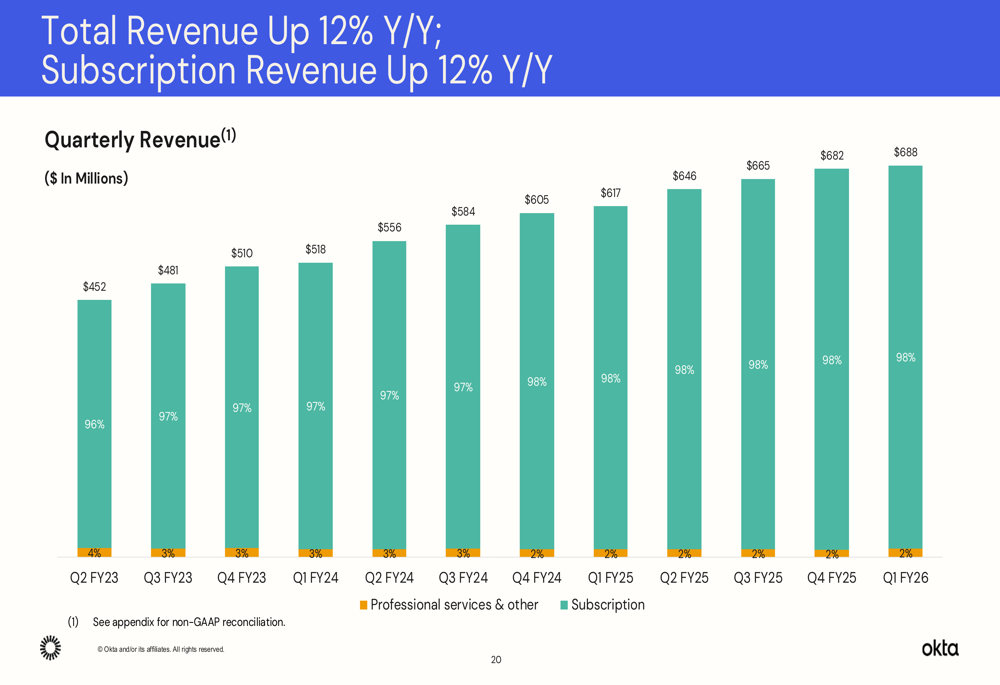

Okta’s quarterly revenue has shown consistent growth over the past three years, though the rate of growth has moderated. As illustrated in the following chart, the company has maintained steady revenue increases while subscription revenue continues to represent 98% of total revenue:

The company’s RPO growth of 21% year-over-year outpaced revenue growth, suggesting healthy future revenue potential. This metric serves as a leading indicator for subscription revenue, as explained in the presentation:

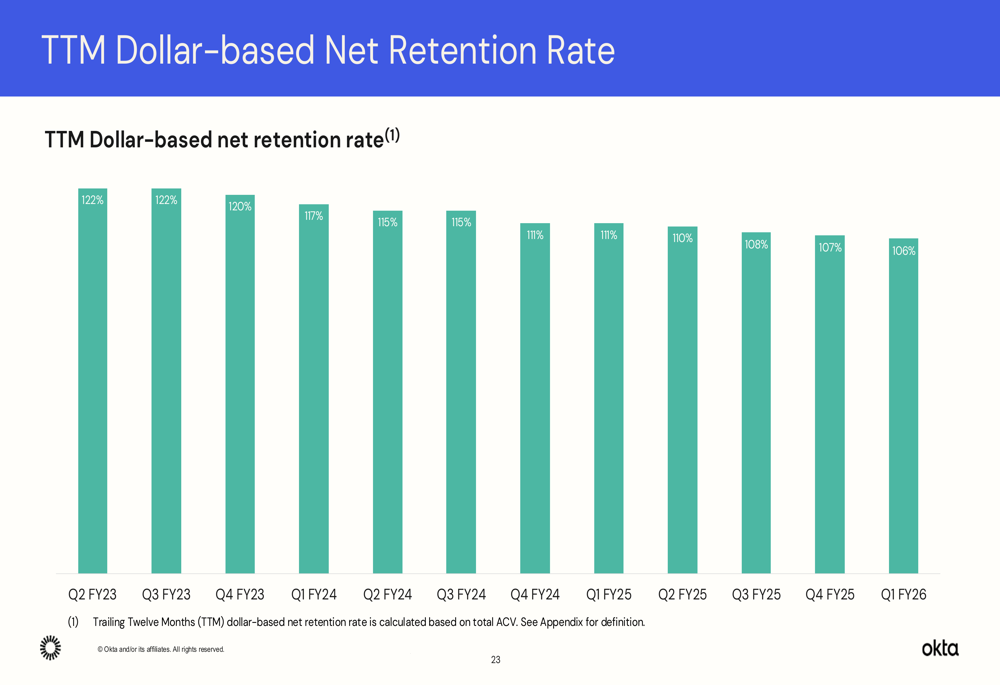

However, Okta’s dollar-based net retention rate has been steadily declining, dropping from 122% in Q2 FY23 to 106% in Q1 FY26. This metric, which measures expansion within existing customers, suggests moderating growth from the existing customer base:

On the profitability front, Okta has made significant strides, transforming from negative operating margins in FY23 to substantial profitability today. The company’s focus on efficiency and cost structure optimization has yielded impressive results:

Similarly, free cash flow margin has improved dramatically from 3.5% in FY23 to 34.7% in Q1 FY26:

Competitive Industry Position

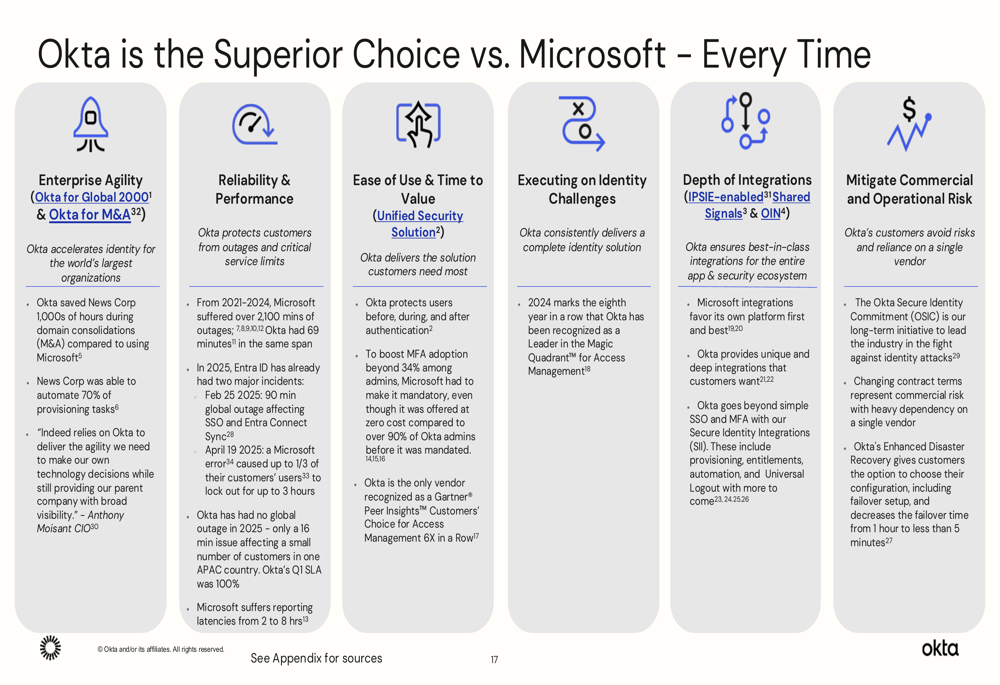

Okta continues to position itself as a superior alternative to Microsoft (NASDAQ:MSFT) in the identity security space. The presentation highlighted several areas where Okta claims advantages, including enterprise agility, reliability, ease of use, and depth of integrations:

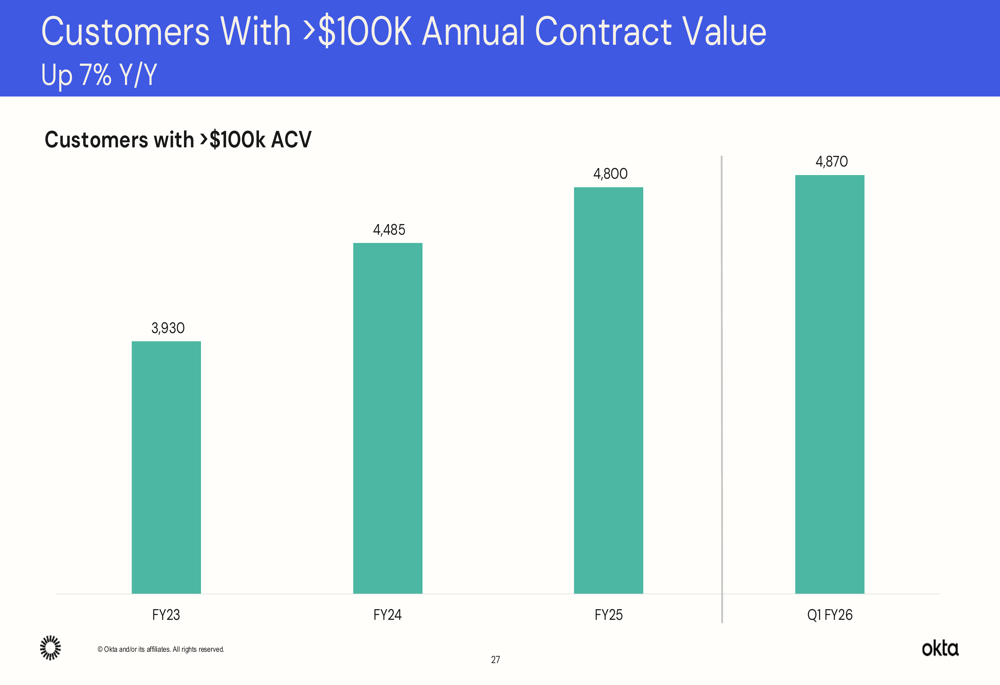

The company’s customer base continues to grow, particularly among larger enterprises. Okta reported 4,870 customers with annual contract values exceeding $100,000, representing 7% year-over-year growth:

Forward-Looking Statements

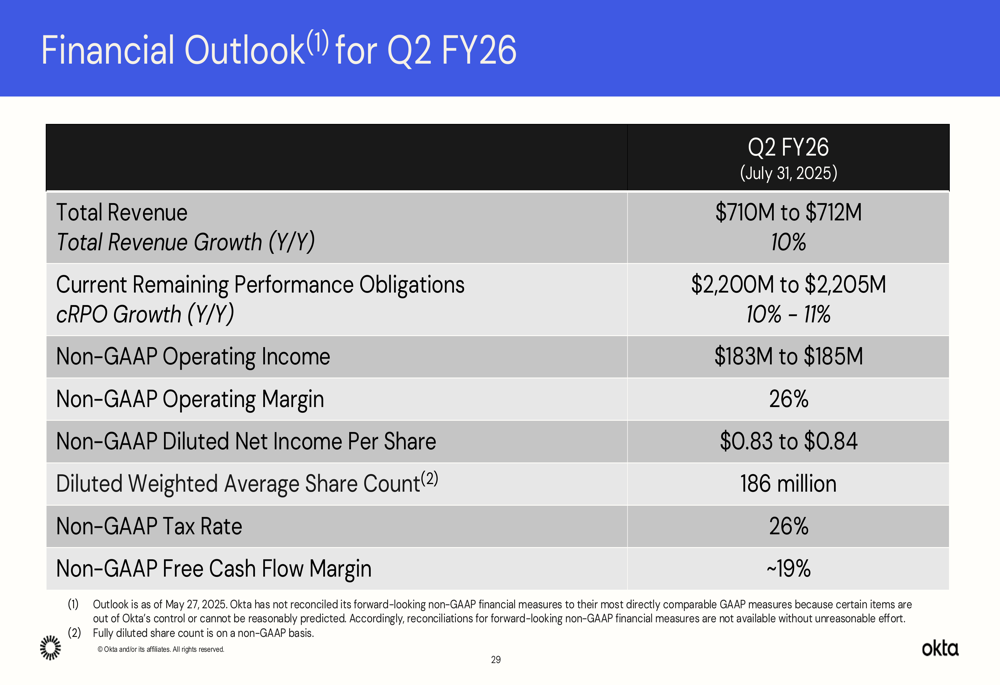

For Q2 FY26, Okta expects revenue between $710 million and $712 million, representing 10% year-over-year growth. The company forecasts current RPO growth of 10-11% and anticipates maintaining its strong operating margin at 26%:

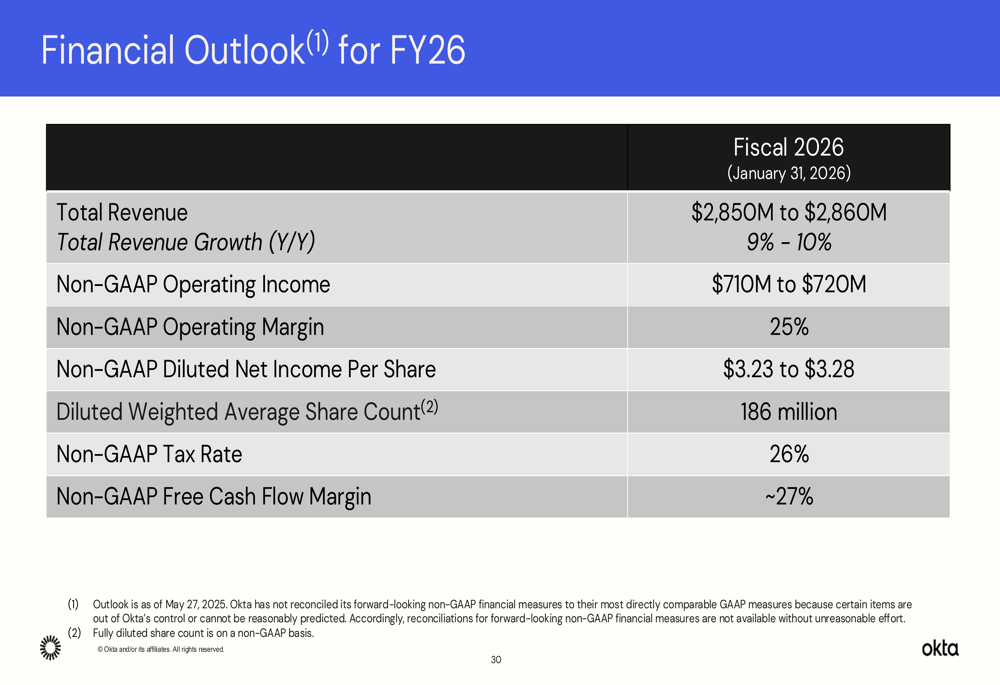

Looking at the full fiscal year 2026, Okta projects revenue of $2.85 billion to $2.86 billion, representing 9-10% growth. The company expects to maintain a 25% operating margin and approximately 27% free cash flow margin:

These projections align with Okta’s strategic priorities for FY26, which include elevating industry security standards through its Okta Secure Identity Commitment (OSIC), winning IT and security teams with the Okta platform, and capturing developer mindshare with AuthO.

The company emphasized multiple growth vectors, including platform innovation, expansion within large enterprises, leveraging its partner ecosystem, and international growth. With a strong balance sheet and improving profitability metrics, Okta appears well-positioned to continue its evolution as a leader in the identity security market, though investors will be watching closely to see if the company can maintain its growth trajectory in an increasingly competitive landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.