BofA warns Fed risks policy mistake with early rate cuts

Old National Bancorp (NYSE:NASDAQ:ONB) presented its first-quarter 2025 financial results on April 22, showing modest growth in loans and deposits, strong capital ratios, and continued expansion of tangible book value. The bank reported adjusted earnings per share of $0.45 and maintained a strong capital position as it prepares for the integration of Bremer Financial Corporation.

The market responded positively to the results, with ONB shares jumping 13.23% to $21.74 in premarket trading, suggesting investors were pleased with the bank’s performance and outlook.

Quarterly Performance Highlights

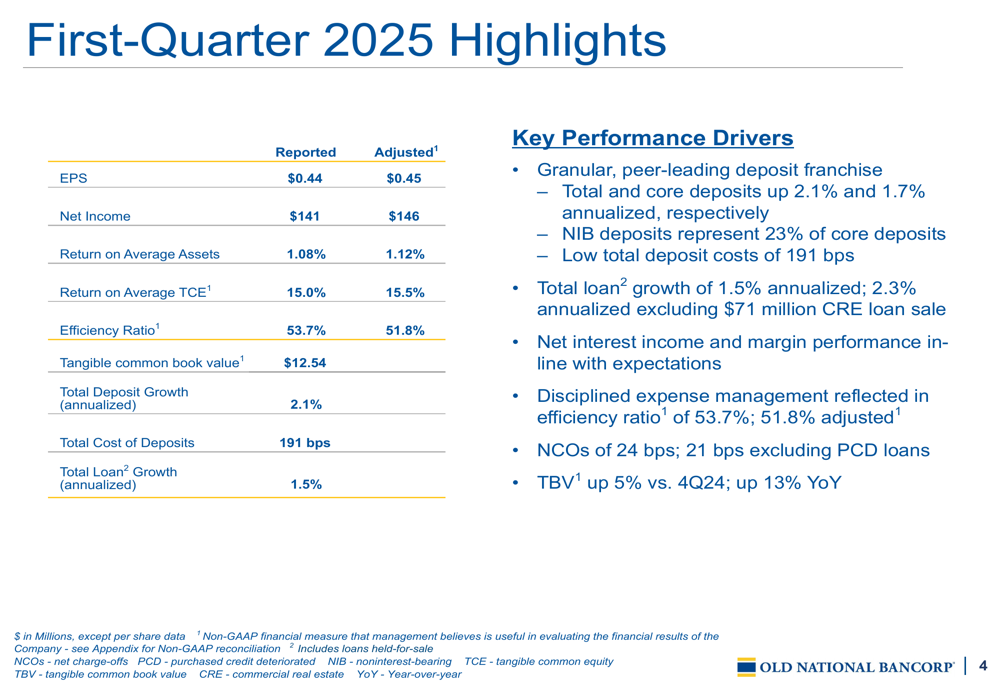

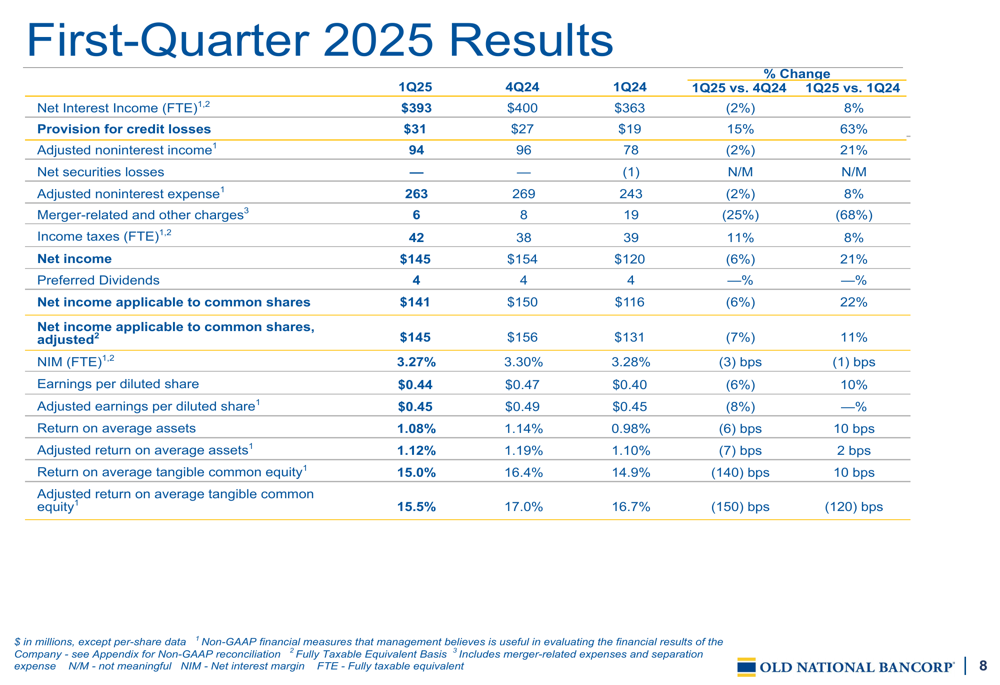

Old National reported first-quarter 2025 net income of $141 million, or $0.44 per share on a GAAP basis, with adjusted earnings of $146 million, or $0.45 per share. The bank achieved a return on average tangible common equity (ROATCE) of 15.0% on a reported basis and 15.5% on an adjusted basis.

As shown in the following comprehensive summary of first-quarter results:

The bank maintained an efficiency ratio of 53.7% (51.8% adjusted), demonstrating continued operational discipline. This represents a slight improvement from the previous quarter, reflecting the bank’s ongoing focus on expense management.

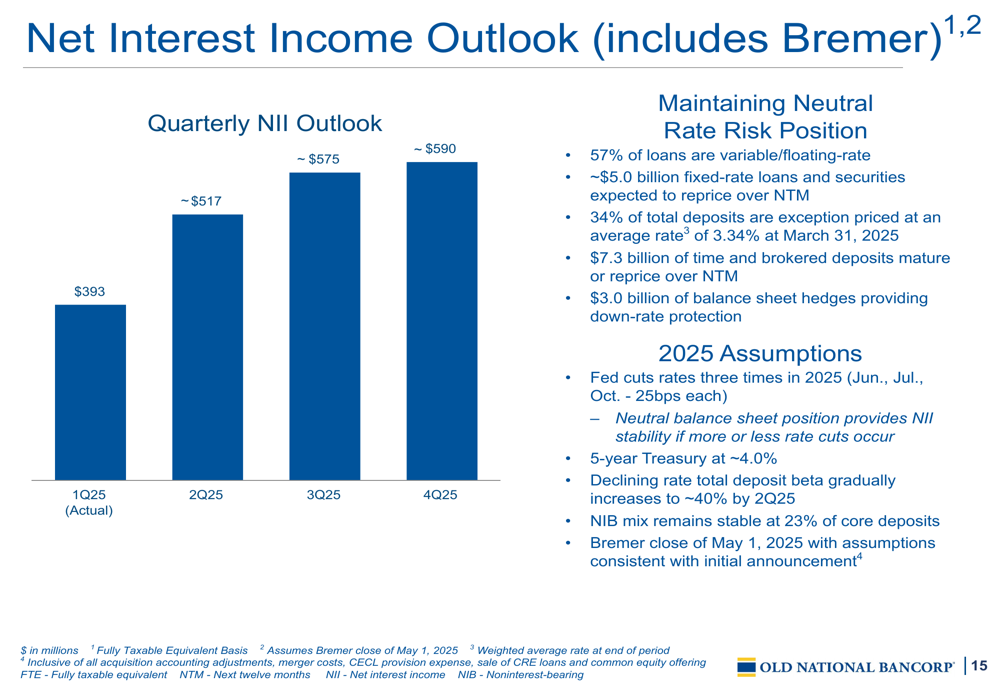

Net interest income on a fully taxable equivalent (FTE) basis was $393 million for the quarter, while the net interest margin stood at 3.27%. The bank’s provision for credit losses was $31 million, reflecting a conservative approach to credit management in the current economic environment.

Balance Sheet and Capital Position

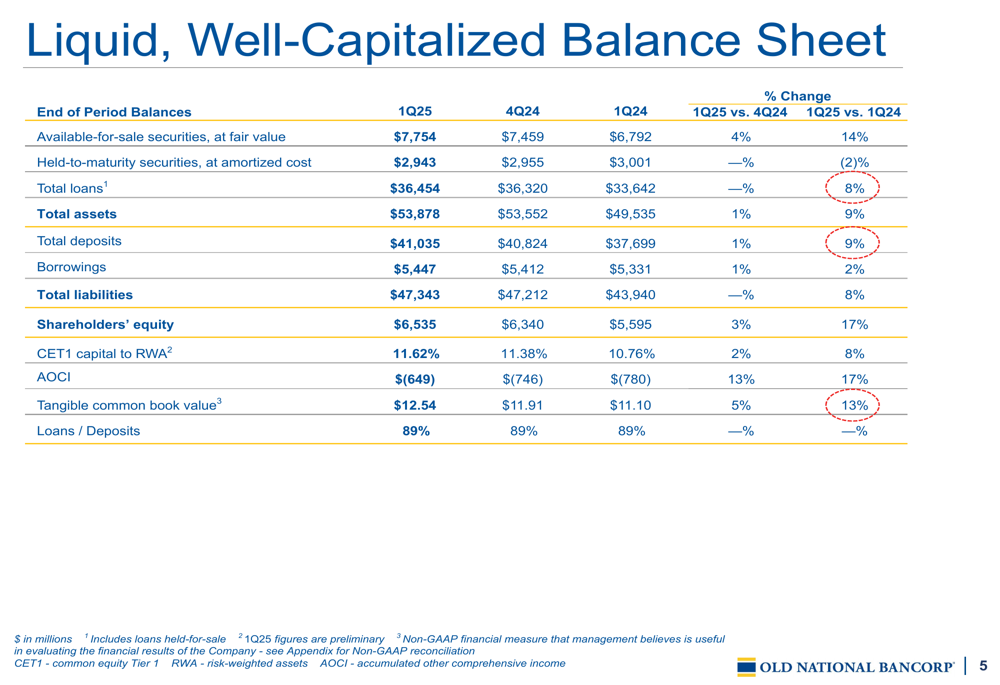

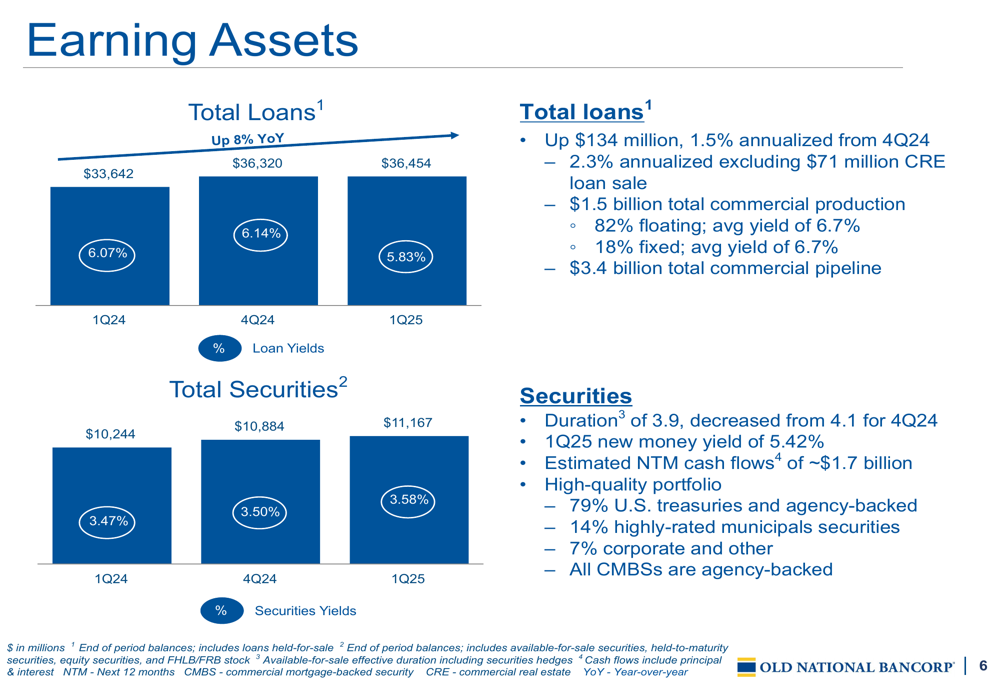

Old National’s balance sheet showed solid year-over-year growth, with total assets reaching $53.9 billion, up 9% from Q1 2024 and 1% from the previous quarter. The bank’s loan portfolio expanded to $36.5 billion, representing annualized growth of 1.5% from Q4 2024 and 8% year-over-year.

The following balance sheet summary highlights the bank’s strong capital and liquidity position:

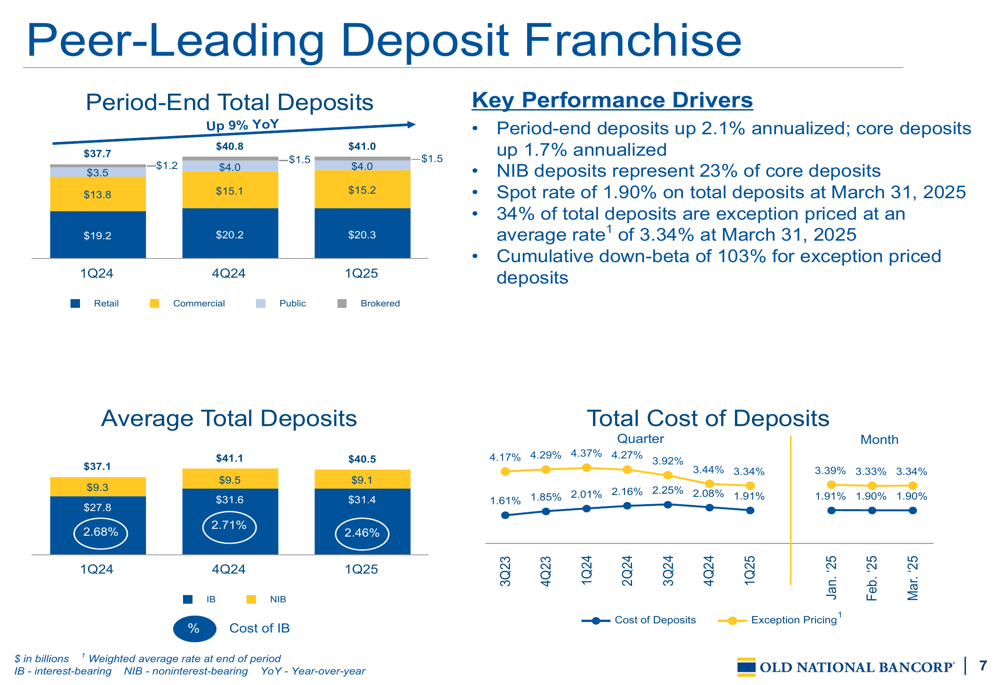

Total (EPA:TTEF) deposits grew to $41.0 billion, up 9% year-over-year and representing annualized growth of 2.1% from the previous quarter. The bank maintained a loan-to-deposit ratio of 89%, indicating a well-balanced funding structure.

The bank’s earning assets showed modest growth, with total loans increasing to $36.5 billion and securities rising to $11.2 billion. Loan yields decreased slightly to 5.83% from 6.07% a year earlier, while securities yields improved to 3.58% from 3.47%.

Old National continues to benefit from a strong deposit franchise, with period-end deposits growing at an annualized rate of 2.1% and core deposits up 1.7% annualized. Non-interest-bearing deposits represent 23% of core deposits, providing a stable, low-cost funding source.

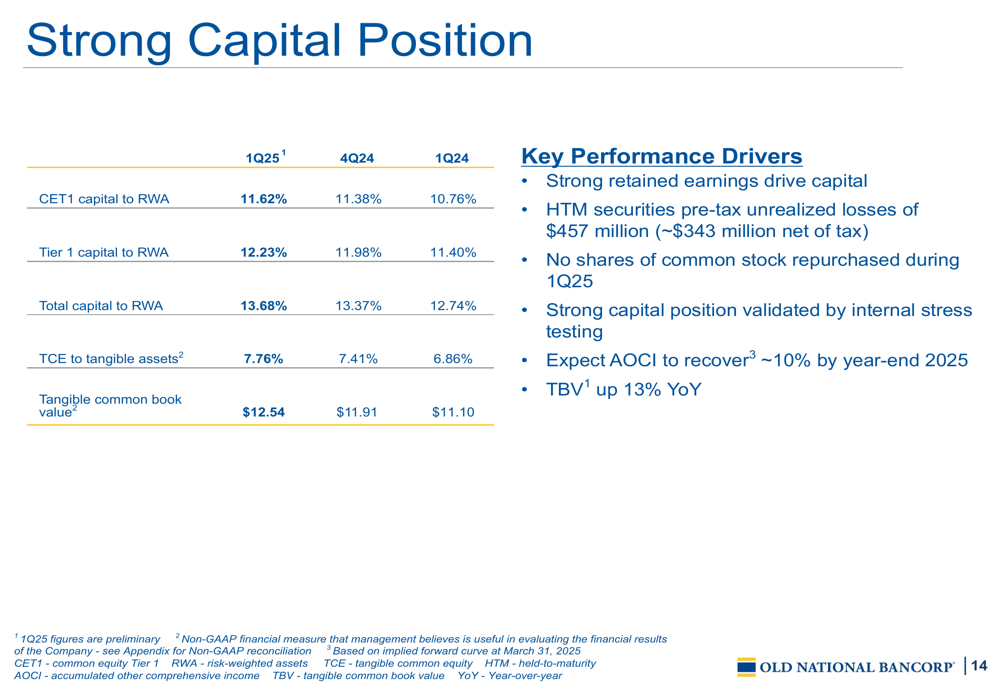

Capital Strength and Tangible Book Value Growth

Old National maintained robust capital ratios, with Common Equity Tier 1 (CET1) capital to risk-weighted assets at 11.62%, well above regulatory requirements. The bank’s tangible common book value per share reached $12.54, representing impressive growth of 5% from the previous quarter and 13% year-over-year.

The following chart illustrates the bank’s strong capital position:

This capital strength provides the bank with flexibility for organic growth, potential share repurchases, and strategic initiatives, including the pending Bremer acquisition.

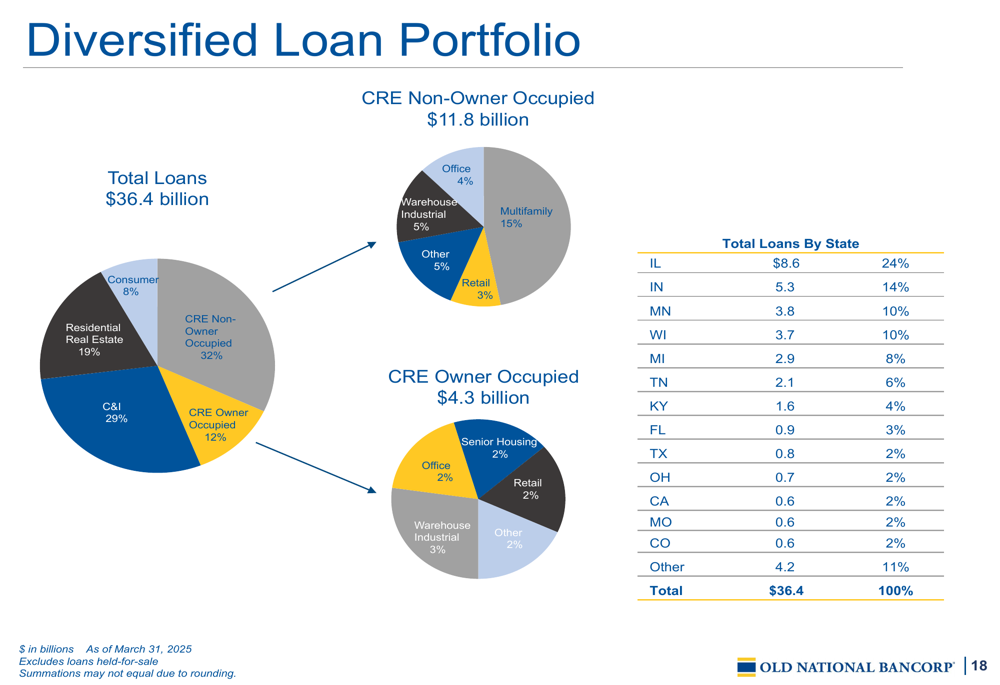

Credit Quality and Loan Portfolio

The bank’s loan portfolio remains well-diversified across geographies and sectors. Total loans stood at $36.4 billion, with commercial real estate (CRE) non-owner occupied representing $11.8 billion and CRE owner-occupied at $4.3 billion. Geographically, Illinois accounts for 24% of the loan portfolio, while Indiana represents 14%.

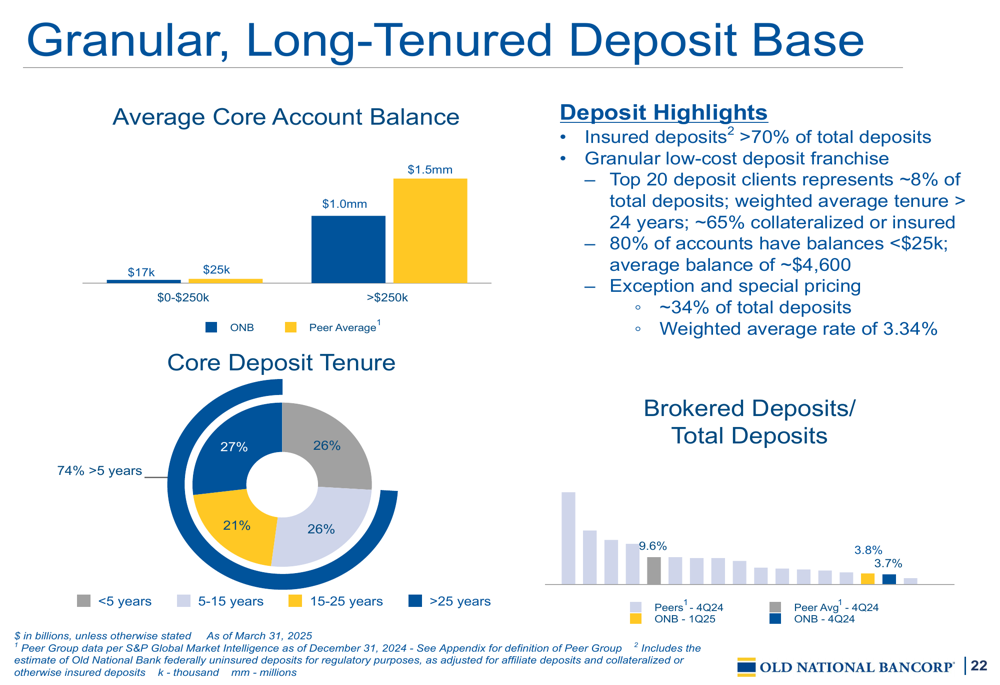

The bank maintains a granular, long-tenured deposit base, with insured deposits representing more than 70% of total deposits. The top 20 deposit clients account for approximately 8% of total deposits, with a weighted average tenure of more than 24 years, highlighting the stability of the bank’s funding sources.

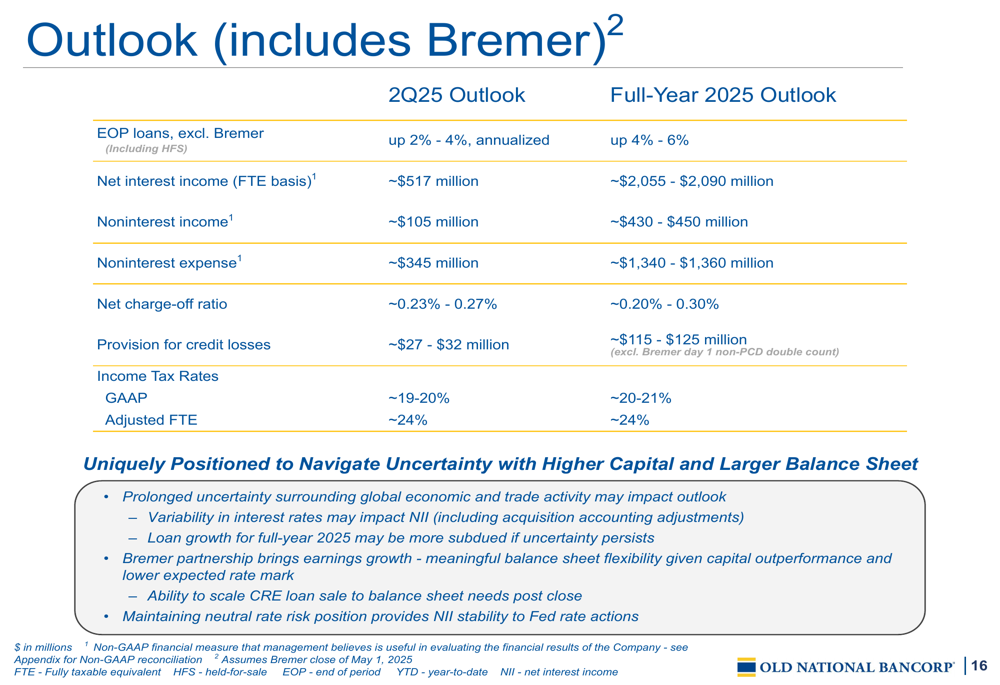

Outlook and Guidance

Old National provided guidance for the second quarter and full-year 2025, including the impact of the Bremer acquisition. The bank expects modest growth in loans and net interest income, with continued focus on fee income and expense management.

For net interest income specifically, the bank projects a gradual increase throughout 2025, benefiting from the Bremer acquisition and a neutral rate risk position. The guidance assumes continued rate cuts by the Federal Reserve, with the bank well-positioned to navigate the changing interest rate environment.

In conclusion, Old National Bancorp’s first-quarter 2025 results demonstrate the bank’s ability to generate solid returns while maintaining strong capital ratios and growing tangible book value. With the pending Bremer acquisition, the bank is positioned for continued growth and enhanced market presence, particularly in the Midwest region. The positive market reaction suggests investors are confident in the bank’s strategy and execution capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.