Michigan survey ahead; Applied Digital surges; gold dips - what’s moving markets

Introduction & Market Context

Olin Corporation (NYSE:OLN) presented its second quarter 2025 earnings results on July 29, 2025, revealing significant year-over-year profitability declines across all business segments. The chemical and ammunition manufacturer reported a net loss of $2.8 million for the quarter, a stark contrast to the $72.3 million net income recorded in the same period last year.

The company’s stock has been under substantial pressure, trading at $21.26 at market close on July 28, 2025, near the lower end of its 52-week range of $17.66 to $49.60. This represents a decline of over 58% in the past year, reflecting ongoing challenges in Olin’s operating environment.

Quarterly Performance Highlights

Olin reported second quarter 2025 Adjusted EBITDA of $176.1 million, down 37% from $278.1 million in Q2 2024. Total (EPA:TTEF) sales across segments showed mixed results compared to the previous quarter, with sequential improvements in two of three business units.

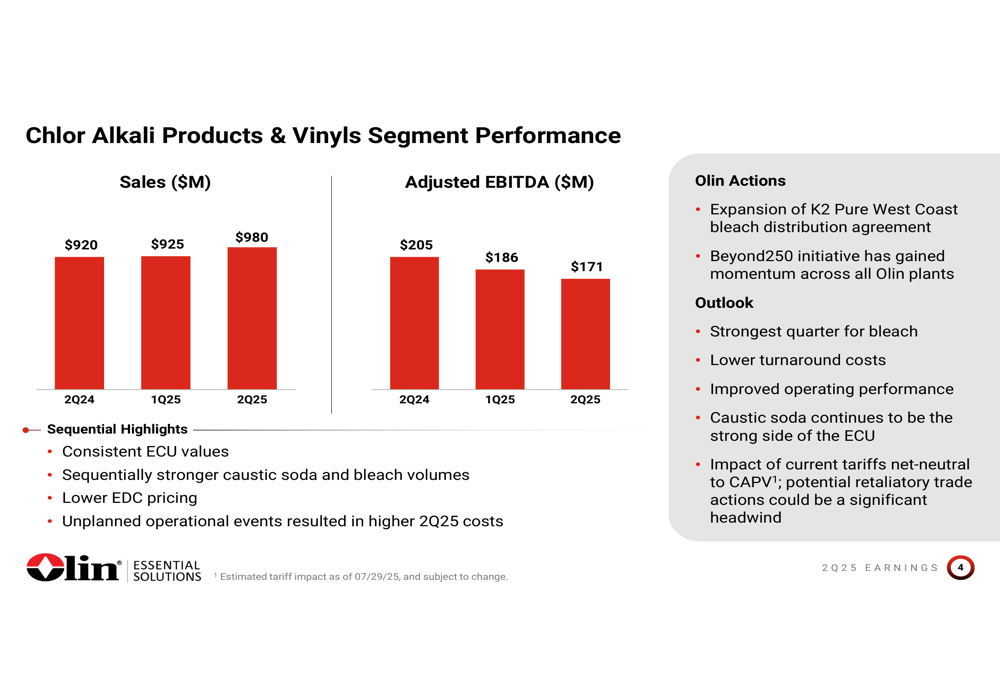

As shown in the following chart of the Chlor Alkali Products & Vinyls (CAPV) segment performance:

The CAPV segment, Olin’s largest business unit, posted sales of $980 million in Q2 2025, up from $925 million in Q1 2025 but with Adjusted EBITDA declining to $171 million from $186 million sequentially. The segment benefited from consistent electrochemical unit (ECU) values and seasonally improved demand for caustic soda and bleach, but faced headwinds from lower ethylene dichloride (EDC) pricing and unplanned operational events that increased costs.

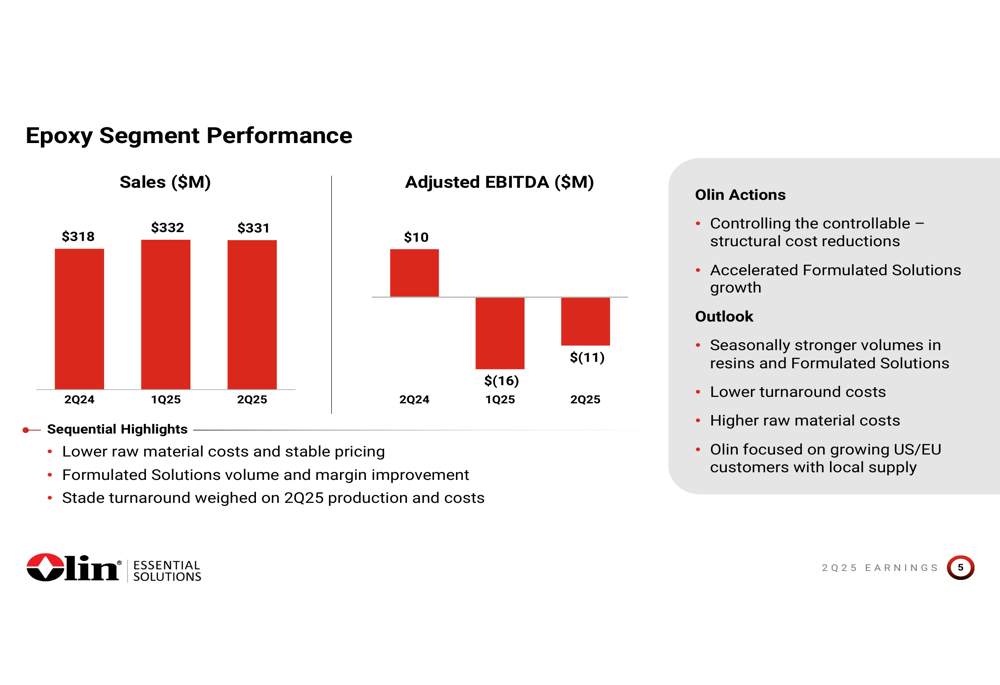

The Epoxy segment showed signs of stabilization as illustrated in this performance chart:

Epoxy sales remained relatively flat at $331 million compared to $332 million in the previous quarter, while Adjusted EBITDA improved to a loss of $11 million from a $16 million loss in Q1 2025. This improvement was driven by lower raw material costs, stable pricing, and better performance in Formulated Solutions. However, a planned turnaround at the Stade facility weighed on production and costs.

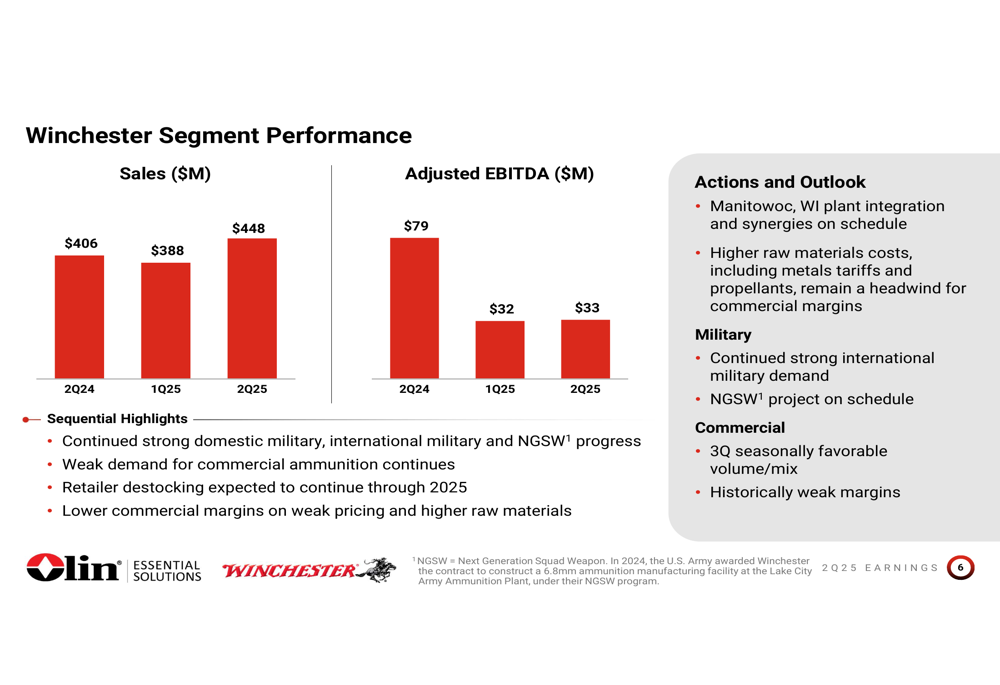

Winchester ammunition segment results revealed contrasting trends between military and commercial markets:

Winchester delivered the strongest sequential sales growth, increasing to $448 million from $388 million in Q1 2025, with Adjusted EBITDA slightly improving to $33 million from $32 million. The segment continues to benefit from strong domestic and international military demand, but faces persistent weakness in commercial ammunition markets. Retailer destocking is expected to continue through 2025, while commercial margins remain under pressure from weak pricing and higher raw material costs, including metals affected by tariffs.

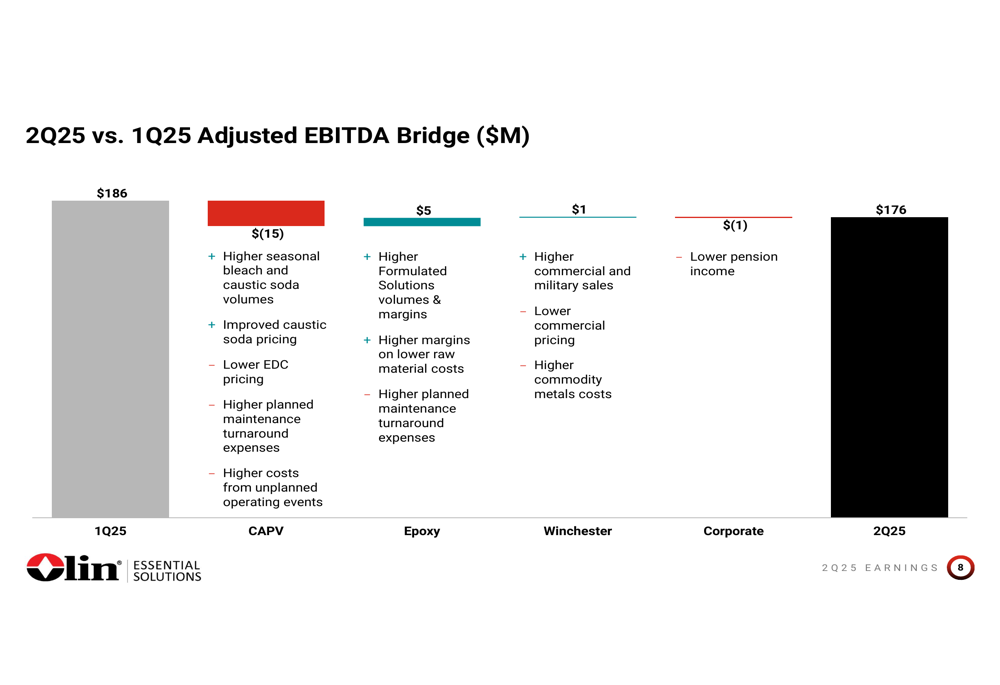

The following bridge chart illustrates the factors affecting Olin’s quarter-over-quarter EBITDA performance:

Strategic Initiatives

In response to ongoing market challenges, Olin has accelerated its "Beyond250" cost reduction initiative, which targets over $250 million in structural cost savings by 2028. The company aims to achieve $70-90 million in annualized run-rate savings by year-end 2025.

As the CEO explained during the presentation, the program focuses on global operational excellence through enterprise benchmarking, asset rightsizing, elimination of remnant costs, and reduction of purchased services and contract labor. Freeport, Texas has been designated as the initial transformation site.

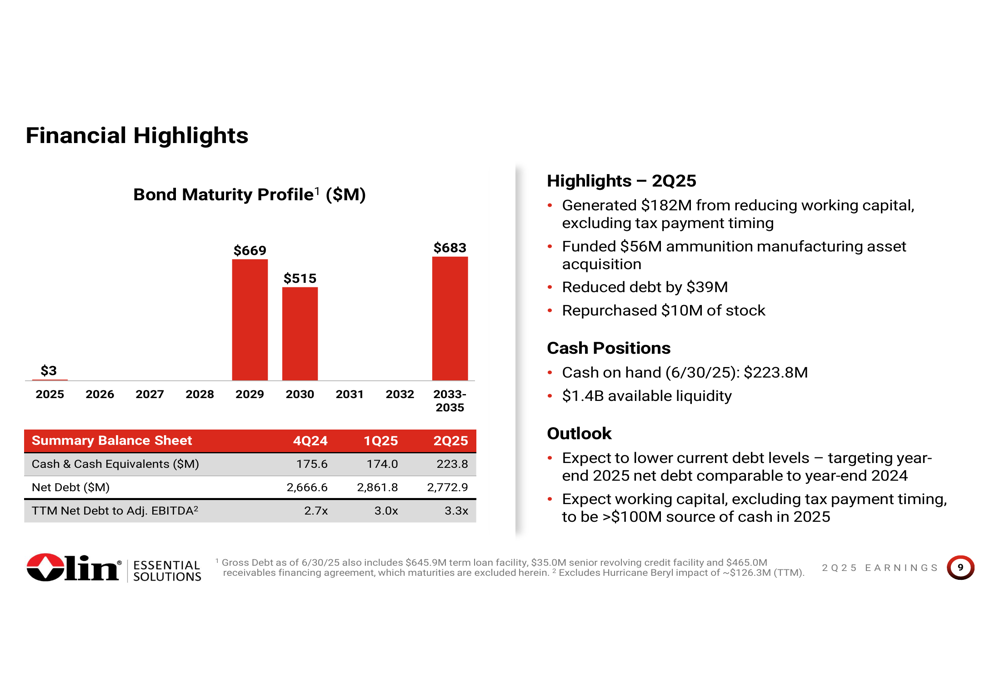

The company’s financial position and debt management strategy are summarized in the following chart:

Olin generated $212 million in operating cash flow during Q2 2025, which funded a $56 million Winchester acquisition, $10 million in share repurchases, and $39 million in debt reduction. The company ended the quarter with $223.8 million in cash and $1.4 billion in available liquidity.

However, Olin’s financial leverage has increased, with trailing twelve-month net debt to Adjusted EBITDA rising to 3.3x from 3.0x in Q1 2025 and 2.7x in Q4 2024. Management indicated they expect to lower current debt levels, targeting year-end 2025 net debt comparable to year-end 2024 levels.

Forward-Looking Statements

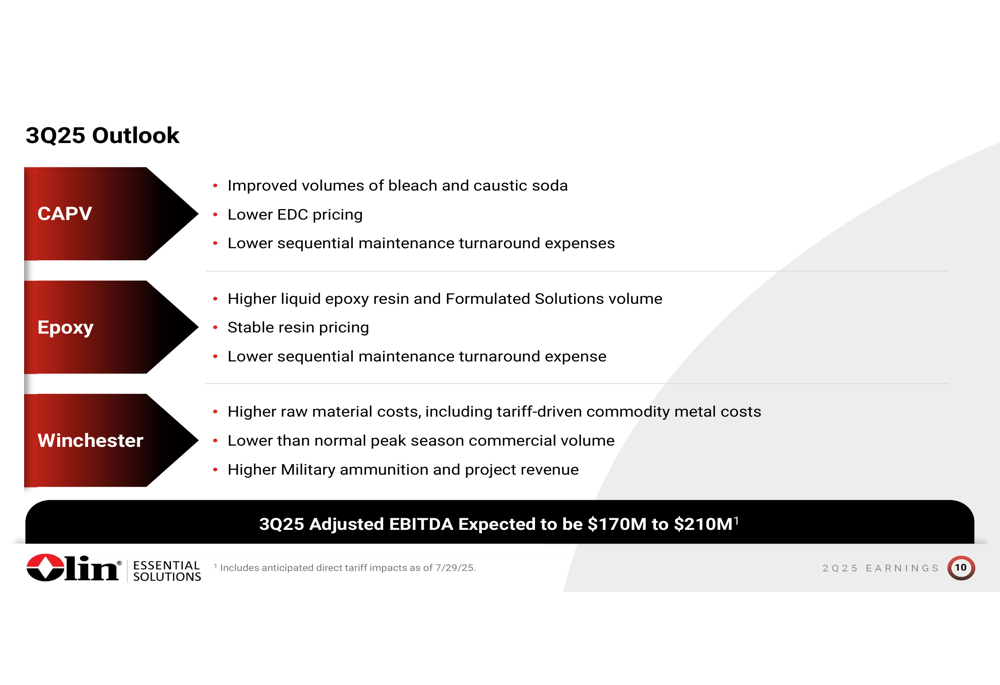

Olin provided the following outlook for the third quarter of 2025:

For Q3 2025, Olin expects Adjusted EBITDA between $170 million and $210 million. The CAPV segment anticipates improved volumes of bleach and caustic soda, lower EDC pricing, and reduced maintenance turnaround expenses. The Epoxy segment expects higher liquid epoxy resin and Formulated Solutions volume, stable resin pricing, and lower maintenance turnaround expenses.

The Winchester segment faces continued challenges from higher raw material costs, including tariff-driven commodity metal prices, and lower than normal peak season commercial volume, though this will be partially offset by higher military ammunition and project revenue.

For the full year 2025, Olin projects capital spending of $200-220 million, above 2024 levels, with depreciation and amortization of approximately $525 million. The company expects working capital, excluding tax payment timing, to be a source of more than $100 million in cash for 2025.

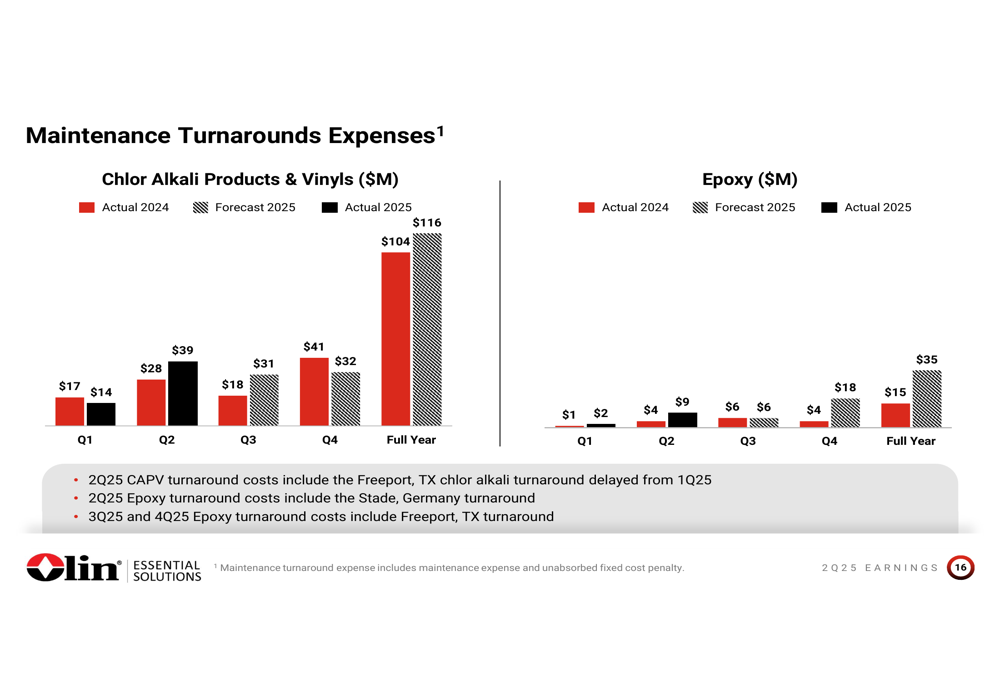

The maintenance turnaround expenses, which significantly impacted Q2 results, are expected to decrease in the second half of the year as shown in this chart:

Despite the challenging environment, Olin’s management remains focused on cash generation, debt reduction, and structural cost improvements as they navigate through what appears to be a prolonged period of market weakness across their key business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.