Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

Omda AS (OMDA) presented its Q1 2025 financial results on May 14, 2025, revealing strong performance across key metrics. The Nordic healthcare software provider saw its stock rise 8.66% following the announcement, building on what has already been a strong year for the company. Omda’s shares closed at 43.9 before the presentation, having already appreciated significantly from their 52-week low of 26.2.

The company described Q1 2025 as "a defining quarter," highlighting its established position as a Nordic leader in specialized healthcare software while demonstrating improved financial performance. The results reflect Omda’s continued focus on building recurring revenue streams and expanding its presence beyond the Nordic region.

Quarterly Performance Highlights

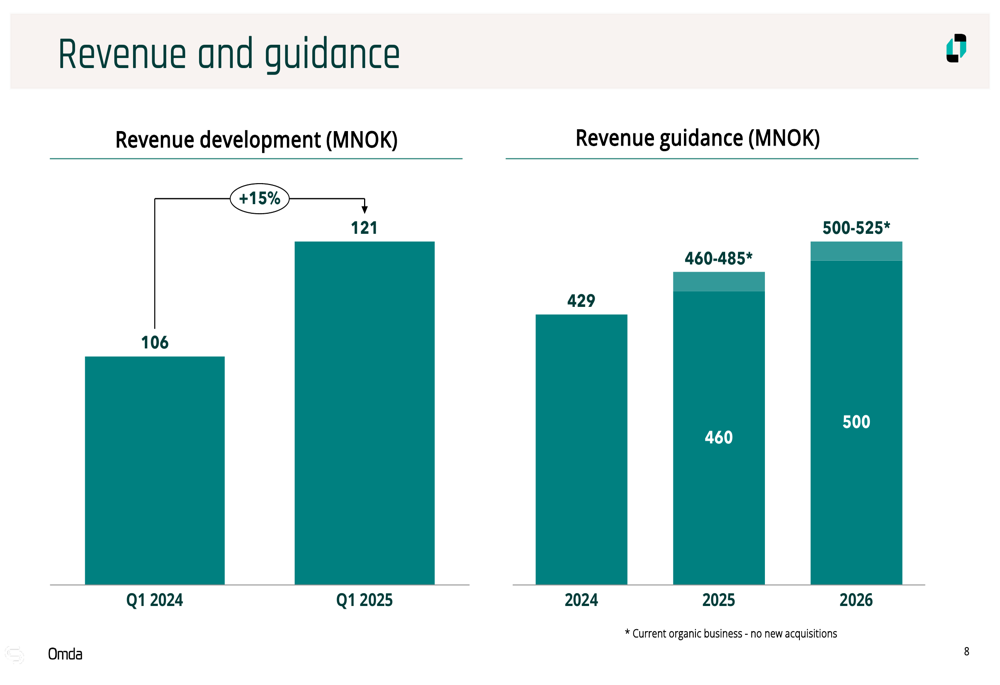

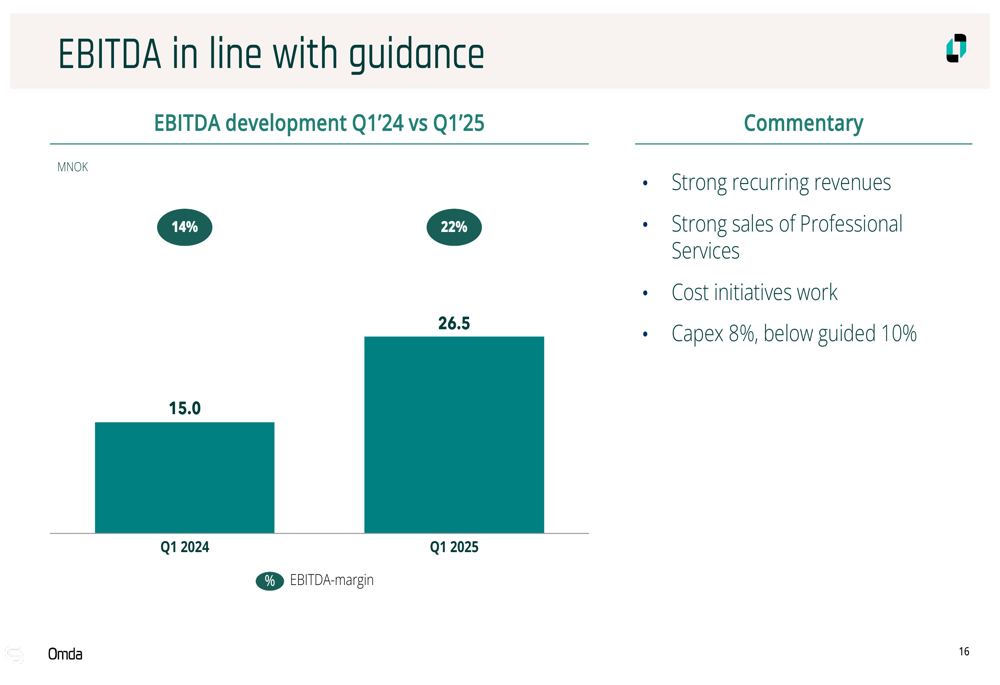

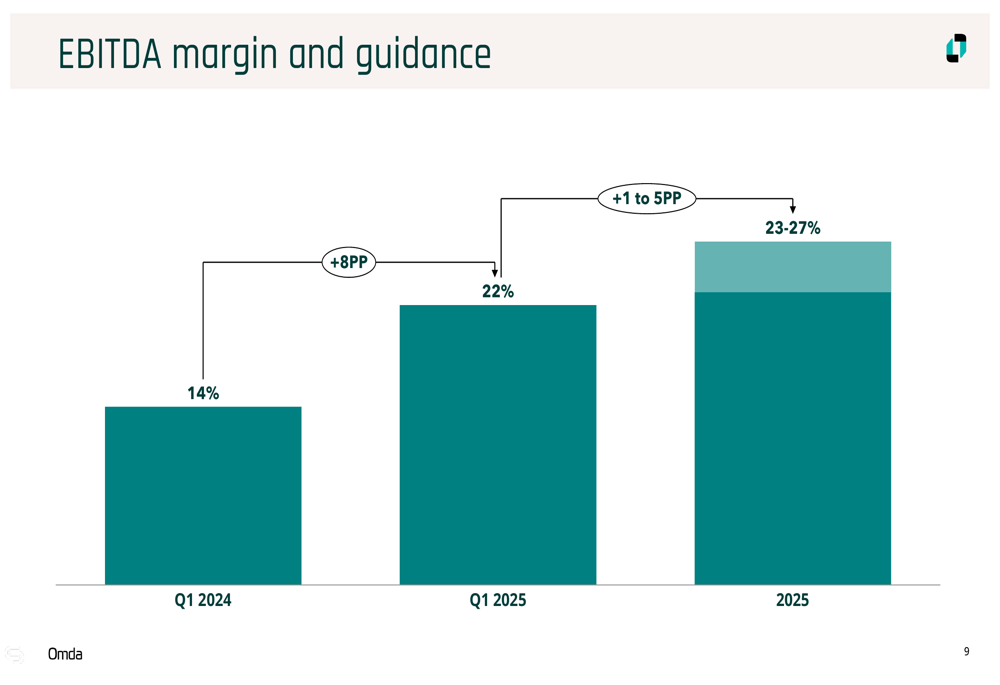

Omda reported Q1 2025 revenue of 121 MNOK, representing 15% growth compared to the same period last year. This acceleration from the 6% growth reported in Q4 2024 signals strengthening business momentum. More impressively, the company’s EBITDA margin expanded to 22%, an 8 percentage point improvement from 14% in Q1 2024.

As shown in the following chart of quarterly revenue growth and guidance:

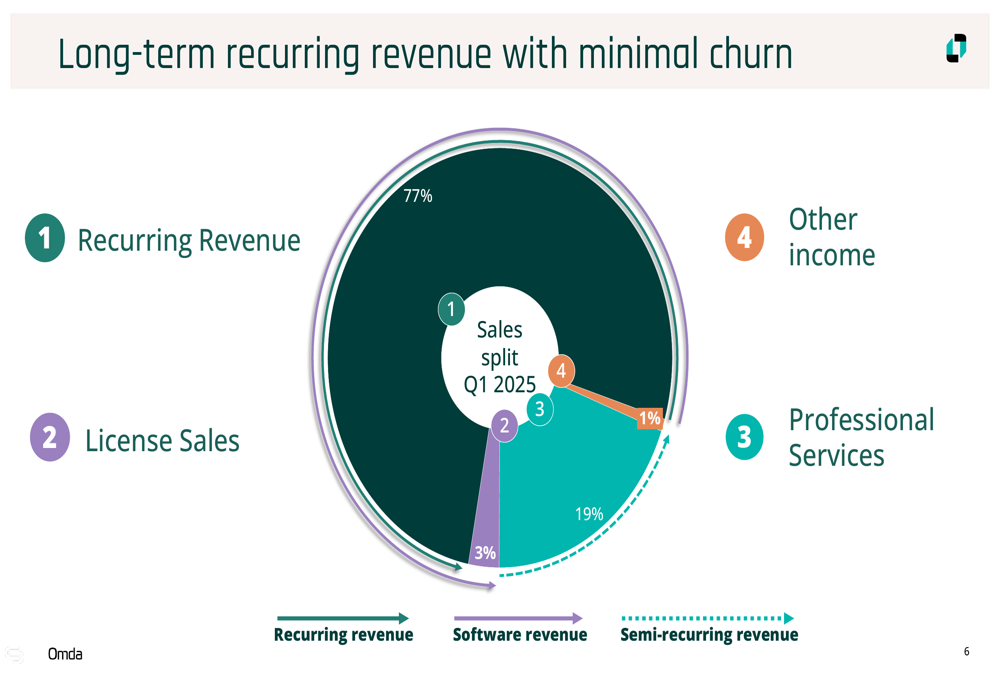

The company’s recurring revenue reached 93 MNOK in Q1 2025, representing an annual recurring revenue (ARR) of 373 MNOK. This recurring revenue now accounts for 77% of Omda’s total revenue, up from 75% reported in the previous quarter, demonstrating the company’s successful execution of its subscription-based business model.

The revenue mix breakdown illustrates the dominance of recurring revenue in Omda’s business model:

Detailed Financial Analysis

Omda’s financial performance shows significant improvement in profitability metrics. The EBITDA margin expansion to 22% represents one of the strongest quarterly performances in the company’s history, as illustrated in this comparison:

The company’s cost management initiatives appear to be yielding results, with recurring revenue of 93 MNOK now nearly covering all operating costs. This provides increased visibility on future profitability. Capital expenditure was reported at 8% of revenue, below the company’s guidance of 10%, indicating efficient capital deployment.

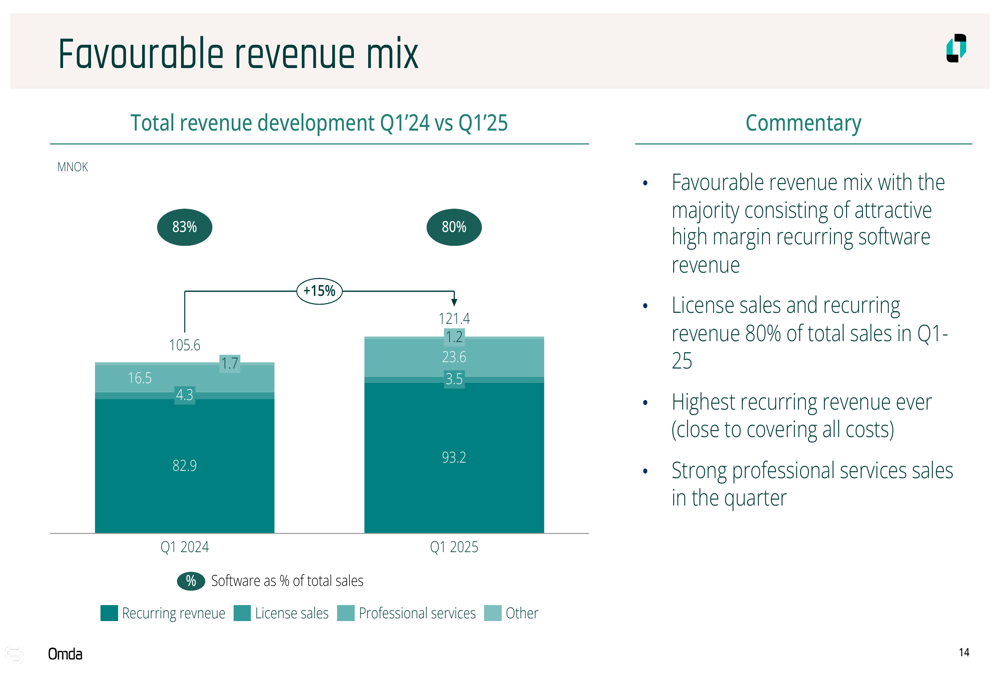

Omda’s revenue mix has evolved favorably, with recurring revenue and license sales together accounting for 80% of total sales in Q1 2025:

Net working capital stood at -5% in Q1 2025, which represents an improvement from Q1 2024 but remains short of the company’s target of -10% or better. The negative working capital reflects Omda’s business model of upfront customer invoicing, which contributes to strong cash flow dynamics.

Strategic Initiatives & Business Diversification

Omda continues to diversify its business across multiple healthcare software segments and geographies. The company closed two acquisitions in Q1 2025 (aweria and dermicus), reinforcing its M&A strategy as a growth driver.

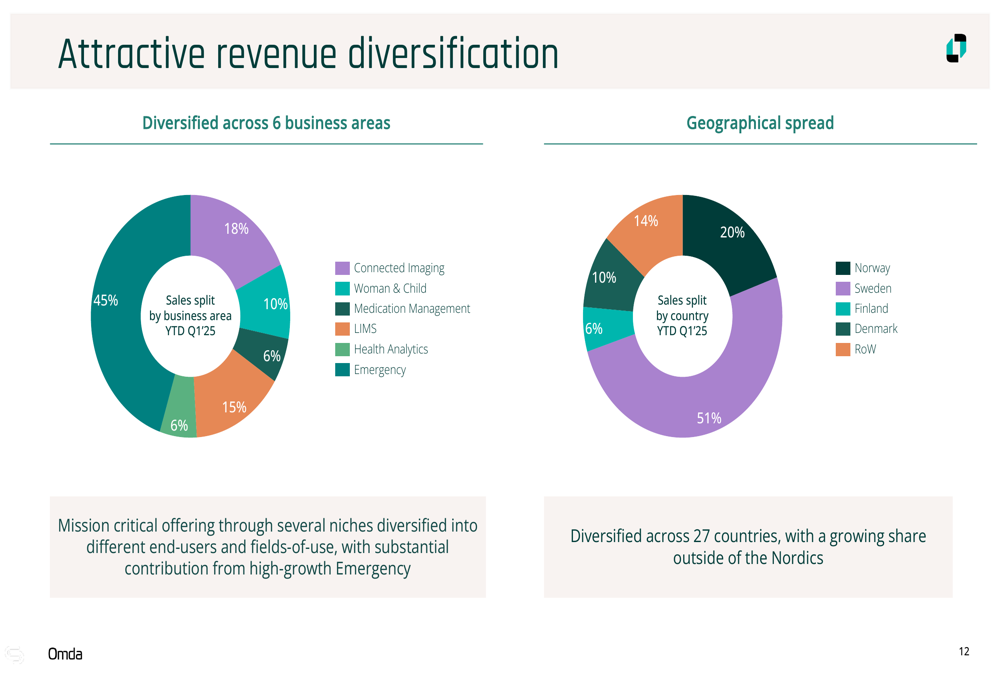

The company’s revenue is well-diversified across business areas and geographies, reducing dependency on any single market:

This diversification provides Omda with multiple growth avenues and helps mitigate market-specific risks. The company now operates in 27 countries, with 51% of revenue coming from outside the Nordic region, highlighting its successful international expansion.

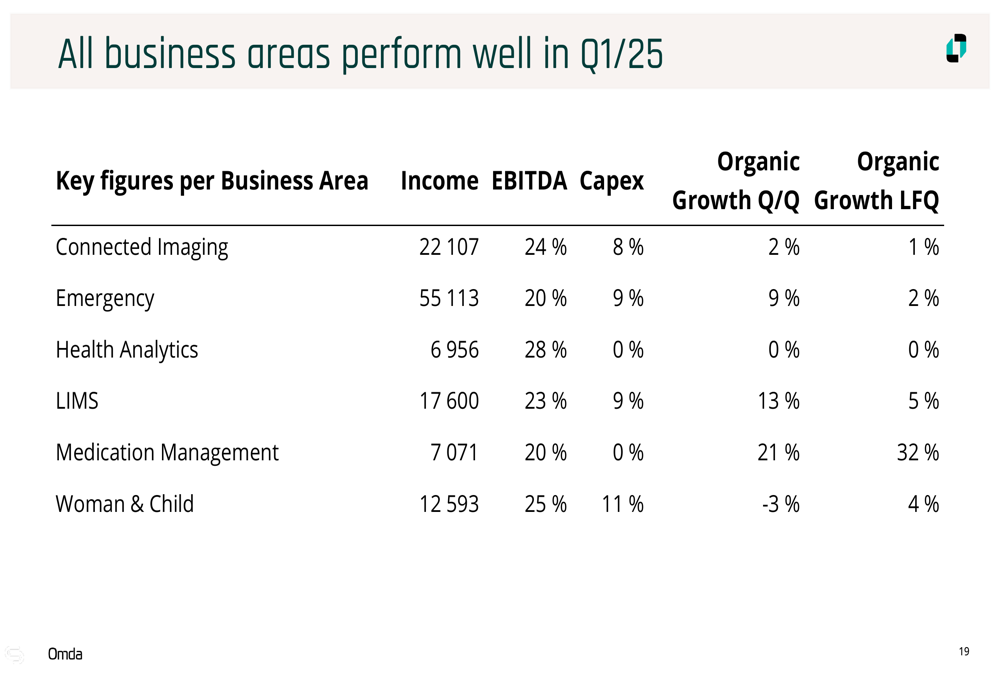

Omda’s business areas show varying performance, with most segments demonstrating healthy EBITDA margins between 20-28%. The detailed breakdown of business area performance provides insight into the company’s operational strengths:

Forward-Looking Statements

Omda maintained its revenue guidance for 2025 at 460-485 MNOK, representing continued growth from 2024’s revenue of approximately 429 MNOK. The company also provided initial guidance for 2026, projecting revenue of 500-525 MNOK. These projections are based on the current organic business and exclude potential new acquisitions.

The company’s revenue and EBITDA margin guidance is illustrated in the following charts:

Omda expects EBITDA margins to continue improving, with 2025 guidance set at 23-27%, representing a 1-5 percentage point improvement from the current Q1 2025 level of 22%. This guidance reflects the company’s confidence in its ability to further enhance operational efficiency while growing revenue.

The company’s long-term strategy continues to focus on organic growth supplemented by strategic acquisitions, with an emphasis on maintaining and expanding its recurring revenue base. Management highlighted that they will continue to explore relevant M&A opportunities while ensuring efficient incorporation of already acquired entities.

With recurring revenue approaching the level needed to cover all operating costs and margins expanding significantly, Omda appears well-positioned to deliver on its financial targets for 2025 and beyond, potentially unlocking additional shareholder value in the process.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.