Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Omnicom Group Inc. (NYSE:OMC) reported its first-quarter 2025 results on April 15, showing organic revenue growth of 3.4% despite a challenging macroeconomic environment. The company’s stock fell 3.01% in aftermarket trading to $74.52, reflecting investor concerns about mixed performance across business segments and regions.

The advertising and marketing giant achieved an adjusted earnings per share of $1.70, exceeding analyst expectations of $1.66, while revenue of $3.69 billion fell slightly short of the anticipated $3.72 billion. The results highlight Omnicom’s ability to navigate market uncertainties while continuing to progress with its planned acquisition of Interpublic Group (IPG).

Quarterly Performance Highlights

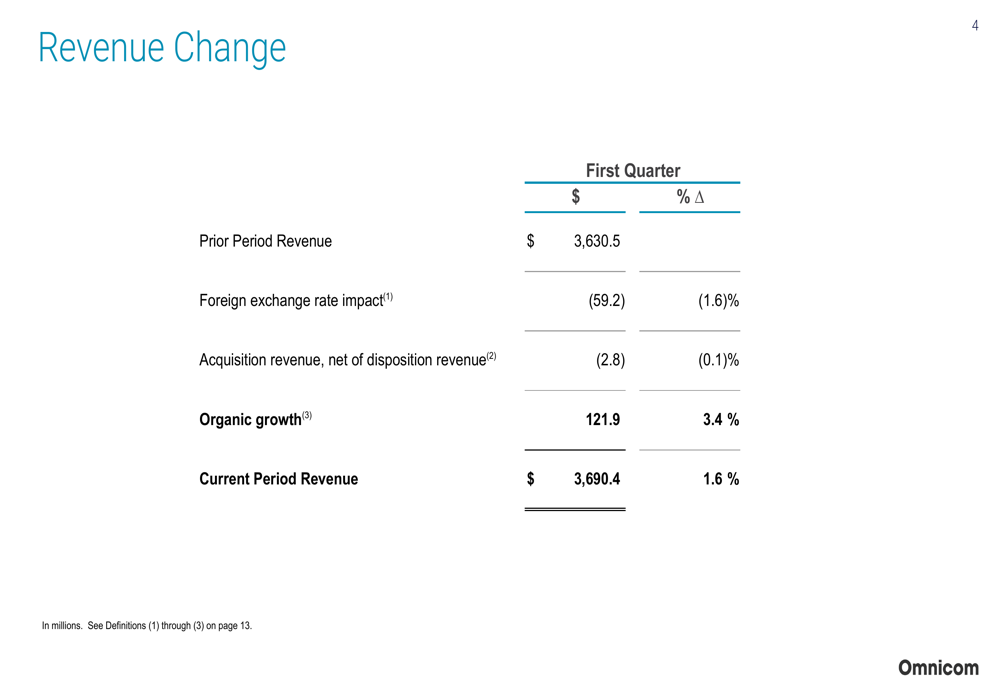

Omnicom’s first-quarter 2025 revenue reached $3,690.4 million, representing a 1.6% increase from $3,630.5 million in the same period of 2024. The company’s organic growth of 3.4% was partially offset by a negative 1.6% foreign exchange impact and a 0.1% decrease from acquisition/disposition activity.

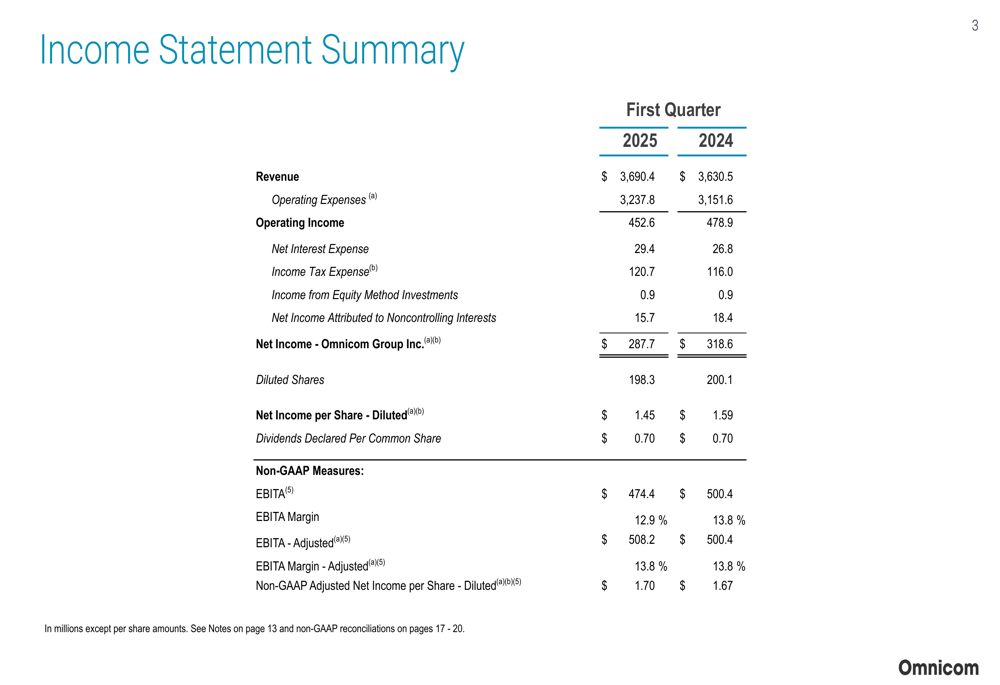

As shown in the following income statement summary, Omnicom’s reported operating income decreased to $452.6 million from $478.9 million in Q1 2024, while net income attributable to Omnicom Group declined to $287.7 million from $318.6 million:

However, the company emphasized its non-GAAP metrics, which exclude acquisition-related costs. Adjusted EBITA increased by 1.6% to $508.2 million, and adjusted diluted earnings per share rose 1.8% to $1.70. These adjustments primarily reflect costs associated with the pending IPG acquisition.

The following chart breaks down the components contributing to Omnicom’s revenue change from Q1 2024 to Q1 2025:

Revenue by Discipline and Region

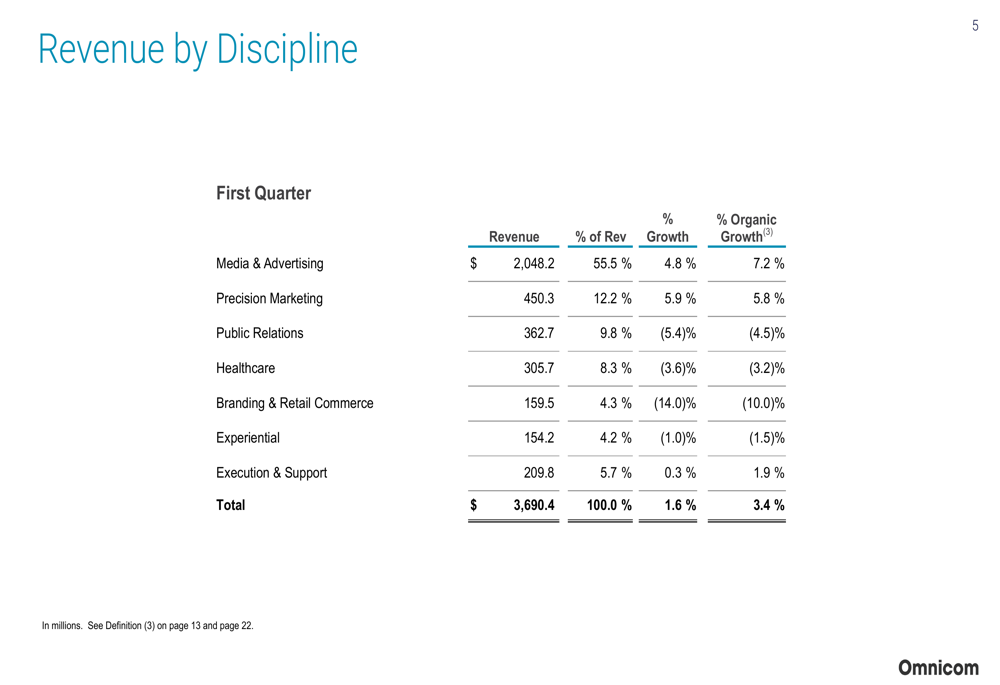

Omnicom’s performance varied significantly across its business disciplines. Media & Advertising, which accounts for 55.5% of total revenue, led growth with 7.2% organic expansion. Precision Marketing also performed strongly with 5.8% organic growth. However, these gains were partially offset by declines in Public Relations (-4.5%), Healthcare (-3.2%), and particularly Branding & Retail Commerce (-10.0%).

The following breakdown illustrates the performance of each discipline in Q1 2025:

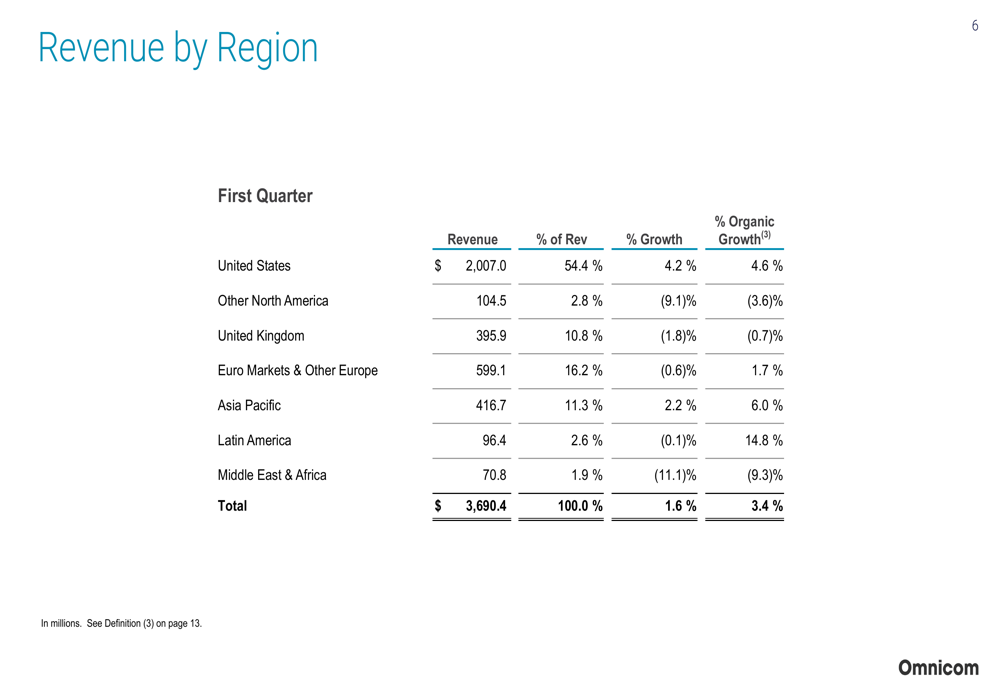

From a geographic perspective, the United States remained Omnicom’s strongest market with 4.6% organic growth, representing 54.4% of total revenue. Latin America showed impressive 14.8% organic growth, while Asia Pacific grew by 6.0%. Performance was weaker in the United Kingdom (TADAWUL:4280) (-0.7%), Other North America (-3.6%), and Middle East & Africa (-9.3%).

The regional revenue breakdown provides insight into Omnicom’s global performance:

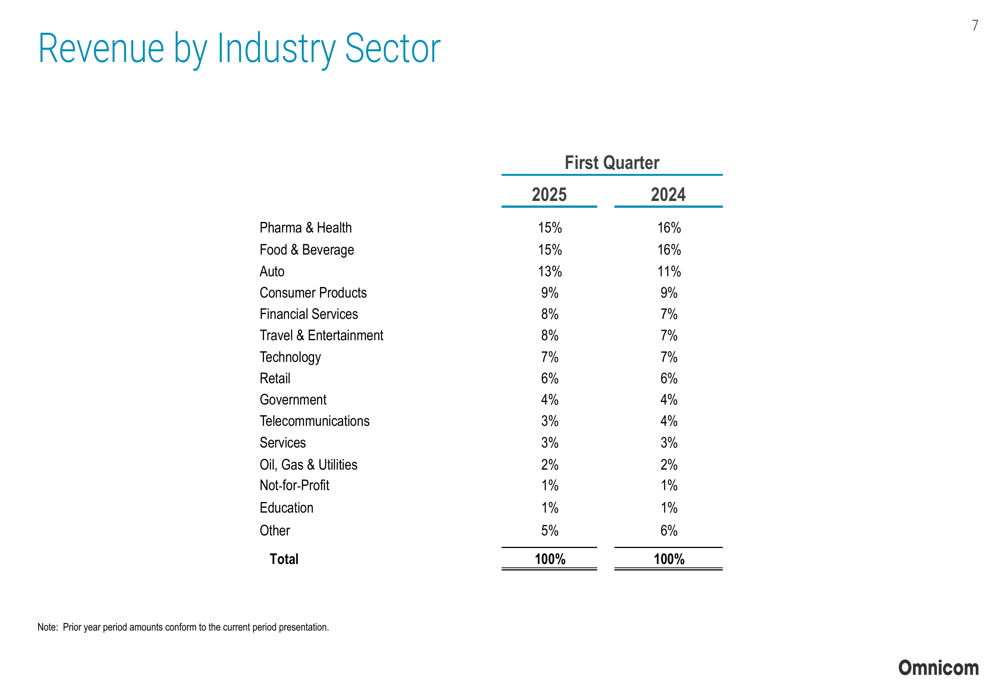

Omnicom’s client industry mix showed some shifts compared to the previous year. The Auto sector increased its share from 11% to 13%, while Pharma & Health and Food & Beverage each decreased by one percentage point to 15%. Financial Services and Travel & Entertainment both increased from 7% to 8% of the revenue mix.

Financial Position and Capital Allocation

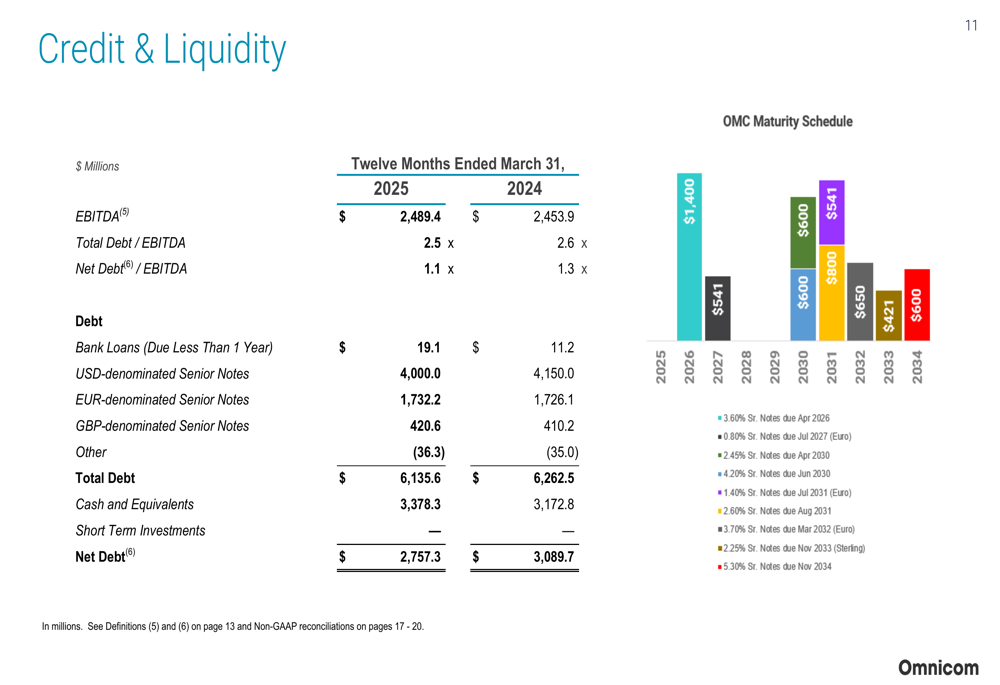

Omnicom maintained a strong financial position with improving debt metrics. The company’s total debt to EBITDA ratio improved to 2.5x from 2.6x a year earlier, while net debt to EBITDA decreased to 1.1x from 1.3x. Cash and equivalents stood at $3,378.3 million as of March 31, 2025.

The following slide illustrates Omnicom’s credit and liquidity position, including its debt maturity schedule:

The company generated $386.5 million in free cash flow during the first quarter, down from $415.1 million in Q1 2024. Omnicom allocated $137.7 million to dividends for common shareholders, $81.0 million to share repurchases, and $29.5 million to capital expenditures.

For the twelve months ended March 31, 2025, Omnicom reported a return on equity of 36.5% and return on invested capital of 19.9%, both metrics declining from the previous year’s 44.3% and 22.3%, respectively.

IPG Acquisition Update

Omnicom provided an update on its proposed acquisition of Interpublic Group, which received overwhelming support from both companies’ shareholders in March, with 93.5% of OMC and 99.6% of IPG votes cast in favor of the transaction.

The company has received regulatory approvals from 5 of the 18 required jurisdictions, including China, Colombia, Brazil, Saudi Arabia, and Egypt. Management remains confident about closing the transaction in the second half of 2025 and achieving the targeted $750 million in cost synergies.

During the earnings call, CEO John Wren addressed concerns about potential client losses due to the merger, stating, "We have not had any client of any significance that we’re in fear of losing because of the transaction." He emphasized that the integration planning is well underway to ensure the company meets its synergy targets.

Forward Outlook

In response to macroeconomic uncertainties, Omnicom expanded its full-year 2025 organic growth guidance range to 2.5-4.5%, lowering the bottom end from the previous 3.0%. The company maintained its adjusted EBITDA margin guidance of 10 basis points improvement over the 15.5% achieved in 2024.

Management highlighted several factors contributing to the cautious outlook, including potential impacts from tariffs, mixed performance in key geographic markets, and declines in public relations and healthcare sectors. However, they expressed confidence in the continued strength of the Media & Advertising and Precision Marketing disciplines.

CEO John Wren emphasized the transformative impact of AI on the company’s operations, stating, "AI is touching every aspect of how our people work." The company has developed OmniAI, an open-source platform leveraging generative AI models for agency-specific use cases, with the goal of having it on the desktop of every client-facing Omnicom employee by the end of the year.

Despite the mixed results and cautious outlook, Omnicom’s management remains confident in the company’s diversified business model and its ability to navigate market uncertainties while progressing toward the completion of the IPG acquisition, which they believe will create significant shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.