Senate Republicans to challenge auto safety mandates in January - WSJ

Introduction & Market Context

OMRON Corporation presented its first-half fiscal year 2025 financial results on November 7, 2025, revealing a mixed performance with increased revenue but declining profits. The presentation came as the company's stock faced significant pressure, dropping 9.34% in after-hours trading following a substantial earnings per share miss.

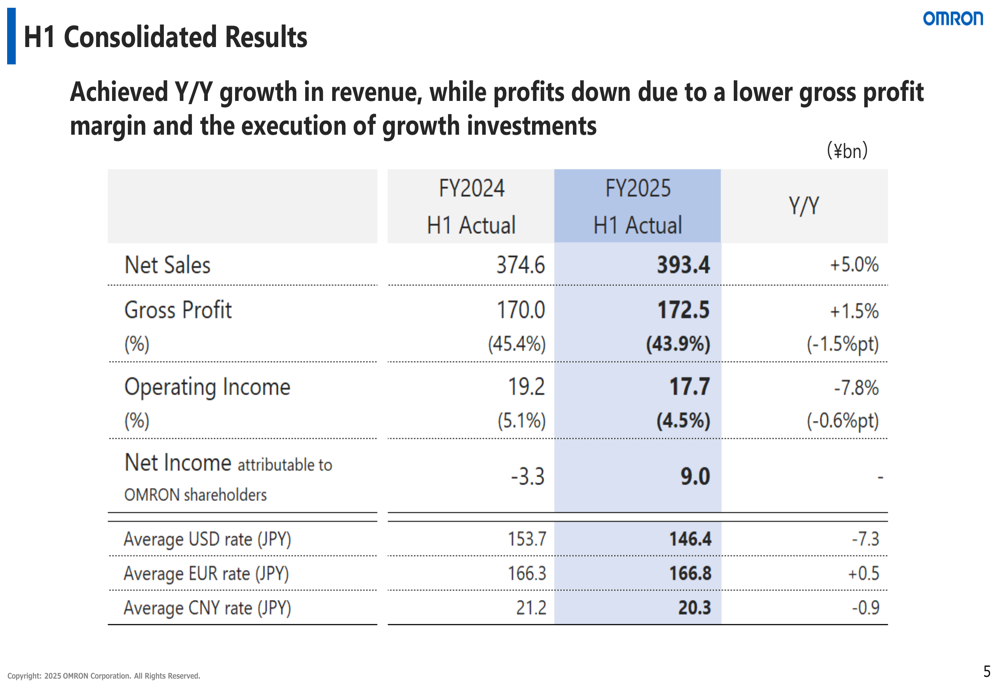

The Japanese electronics manufacturer reported consolidated revenue growth of 5.0% year-over-year to ¥393.4 billion for the first half of FY2025, while operating income decreased by 7.8% to ¥17.7 billion. This performance reflects broader challenges in the global manufacturing sector, including tariff impacts and shifting investment patterns in key industries.

As shown in the following consolidated results summary:

Quarterly Performance Highlights

OMRON's performance varied significantly across its business segments, with Industrial Automation Business (IAB) emerging as the standout performer while Healthcare Business (HCB) faced substantial headwinds.

The segment breakdown reveals that IAB achieved 8.2% revenue growth and 8.5% operating profit growth, driven by strong demand from the semiconductor and secondary battery industries. Meanwhile, HCB experienced an 8.0% revenue decline and a steep 33.8% drop in operating profit, though the company noted that Q2 showed improvement after a weak Q1.

The following segment analysis illustrates these contrasting performances:

The Data Solutions Business (DSB) demonstrated the strongest percentage growth at 20.0% for revenue and 125.1% for operating profit, albeit from a smaller base. Device & Module Solutions Business (DMB) also performed well with 10.8% revenue growth.

Detailed Financial Analysis

Despite the revenue increase, OMRON's operating income declined due to multiple factors, including lower gross profit margins and increased investments. The gross profit margin decreased from 45.4% to 43.9% year-over-year, reflecting challenges in maintaining pricing power amid changing market conditions.

The following waterfall chart breaks down the factors contributing to the operating income decline:

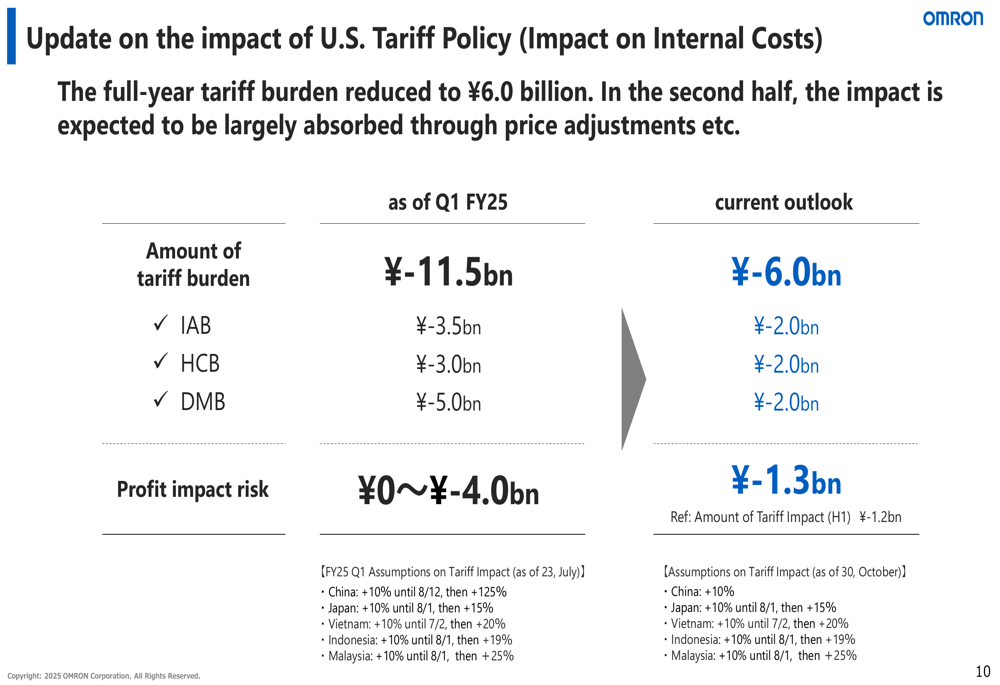

A key factor affecting profitability was the impact of U.S. tariff policies, though OMRON has revised its expected tariff burden downward from the initial estimate. The company now expects a full-year tariff impact of ¥6.0 billion, reduced from the initial ¥11.5 billion forecast, with plans to largely absorb the second-half impact through price adjustments.

As shown in the tariff impact analysis:

This reduction in expected tariff burden provides some relief, though the earnings article suggests that cost management challenges extend beyond tariff impacts, as evidenced by the significant EPS miss of $11.34 versus the forecast of $39.08.

Strategic Initiatives

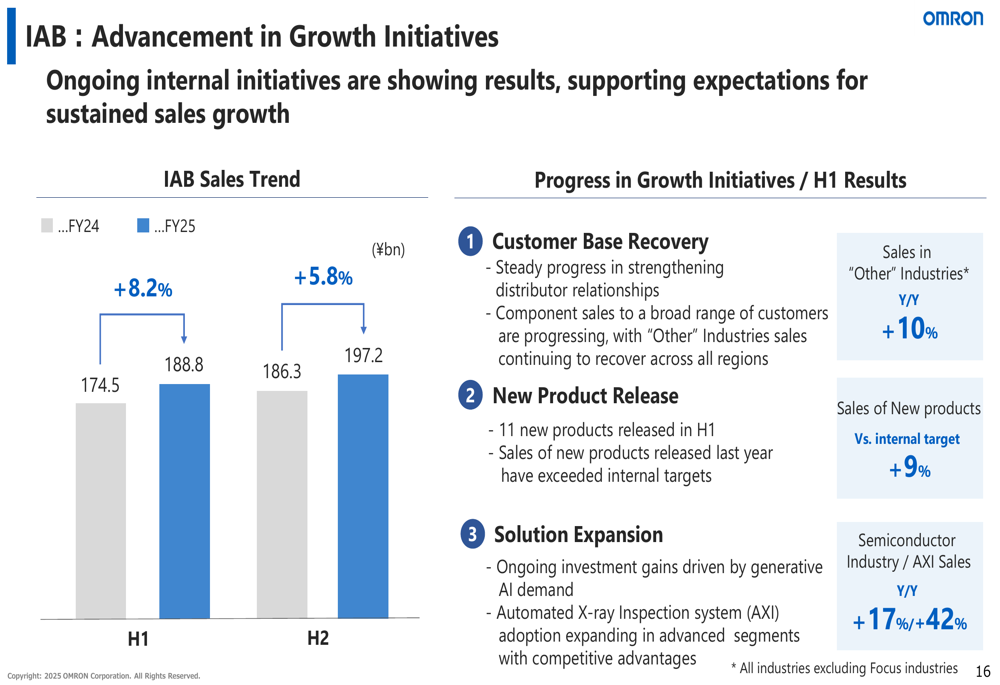

OMRON is making progress on its growth initiatives, particularly in the IAB segment where customer base recovery and new product releases are showing positive results. Sales in "Other" Industries increased by 10% year-over-year, while new product sales exceeded internal targets by 9%.

The semiconductor industry remains a strategic focus, with sales up 17% year-over-year, while Automated X-ray Inspection (AXI) sales grew by an impressive 42%.

The following slide illustrates the advancement in IAB growth initiatives:

The company's operating environment outlook for the second half of FY2025 indicates continued strength in the semiconductor industry, particularly for AI applications, while EV investments in Japan are expected to decline due to tariff impacts. Chinese secondary battery investments have peaked and are slowing, with demand slightly below initial forecasts.

Forward-Looking Statements

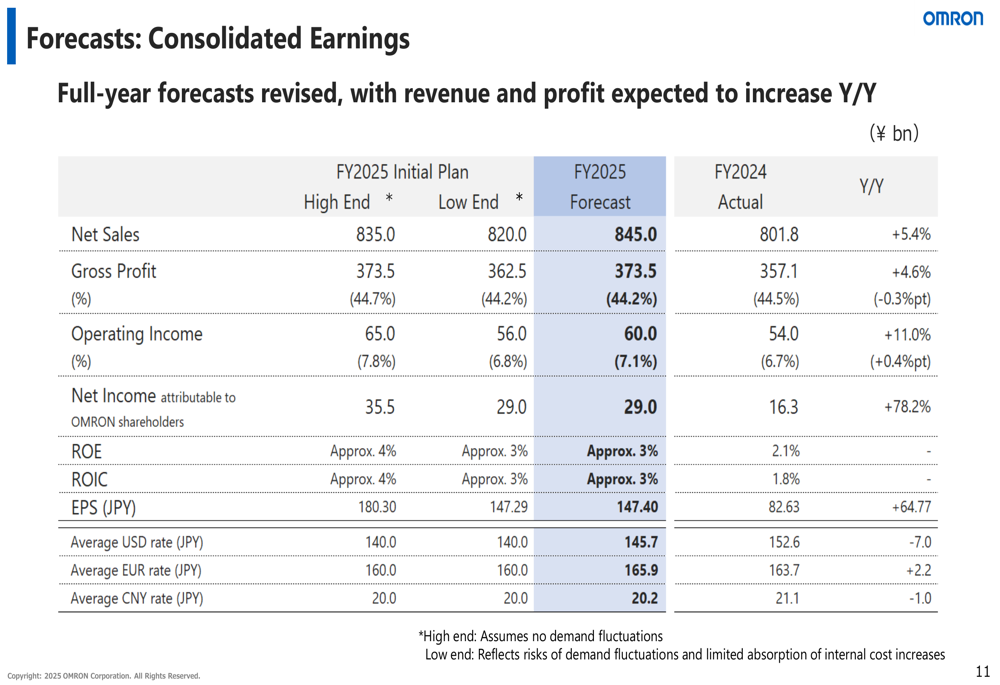

Despite the challenges in the first half, OMRON has revised its full-year forecasts with expectations of higher revenue and profit. The company now projects net sales of ¥845.0 billion (+5.4% Y/Y) and operating income of ¥60.0 billion (+11.0% Y/Y) for FY2025.

The consolidated earnings forecast is detailed below:

OMRON maintained its initial full-year dividend guidance of ¥104 per share, with the interim dividend fixed at ¥52, signaling confidence in its second-half performance despite the first-half challenges.

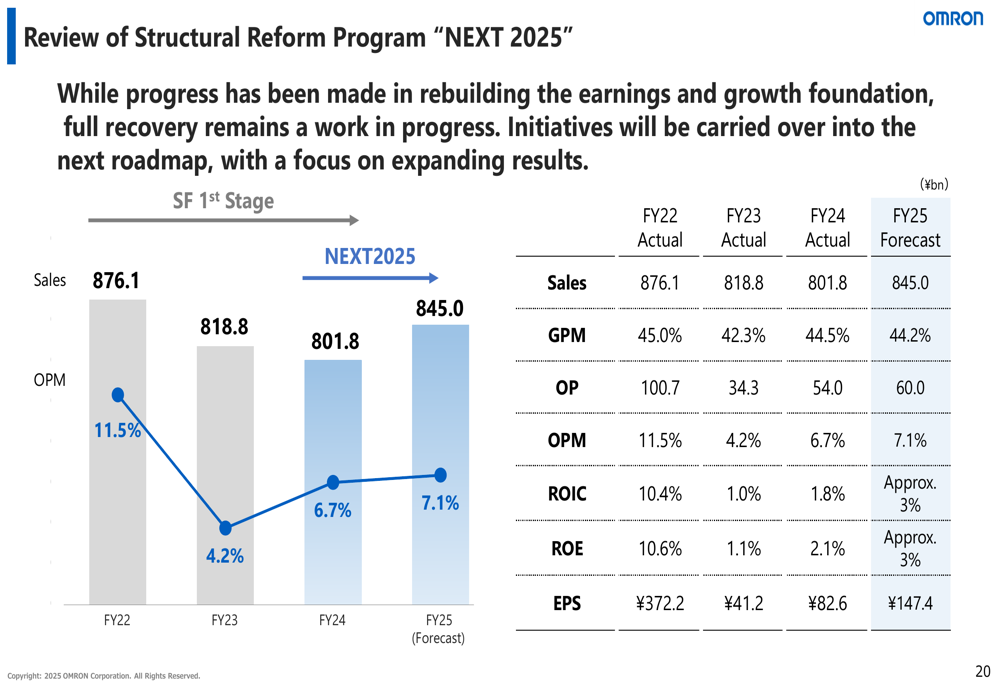

The company is also continuing its structural reform program "NEXT 2025," though progress has been slower than initially planned. While OMRON projects improvement in key metrics like ROIC and ROE to approximately 3% in FY2025, these figures remain below the FY2022 levels of 10.4% and 10.6%, respectively.

As shown in the review of the structural reform program:

While OMRON's presentation focuses on positive developments and strategic initiatives, the market reaction following the earnings release suggests investors remain concerned about the company's ability to translate revenue growth into stronger bottom-line results. The significant gap between actual and forecasted EPS indicates challenges that may require more aggressive cost management and operational efficiency improvements in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.