SoFi CEO enters prepaid forward contract on 1.5 million shares

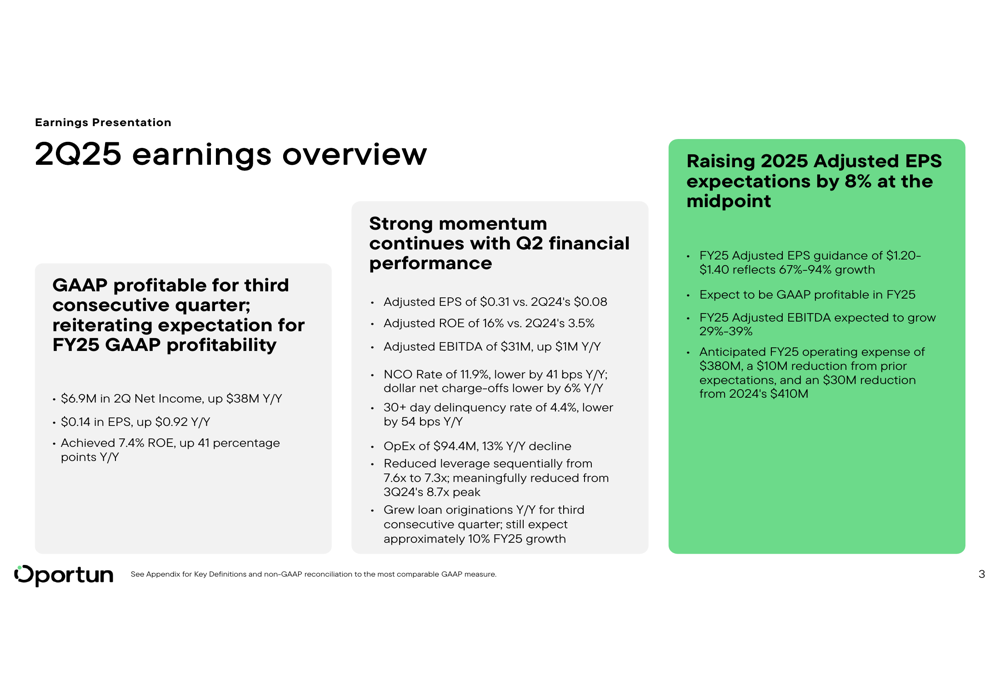

Oportun Financial Corp (NASDAQ:OPRT) presented its second quarter 2025 earnings results on August 6, highlighting its third consecutive quarter of GAAP profitability despite a slight year-over-year revenue decline. The company’s strategic focus on credit quality improvements and operational efficiency continues to drive stronger financial performance, with significant improvements in key profitability metrics.

Quarterly Performance Highlights

Oportun reported GAAP net income of $6.9 million for Q2 2025, representing a substantial $38 million improvement year-over-year. This translated to earnings per share of $0.14, up $0.92 from the same period last year. The company achieved a return on equity of 7.4%, marking a 41 percentage point improvement compared to Q2 2024.

On an adjusted basis, the company reported EPS of $0.31 (versus $0.08 in Q2 2024) and an adjusted ROE of 16% (versus 3.5% in Q2 2024). Adjusted EBITDA came in at $31 million, up $1 million year-over-year.

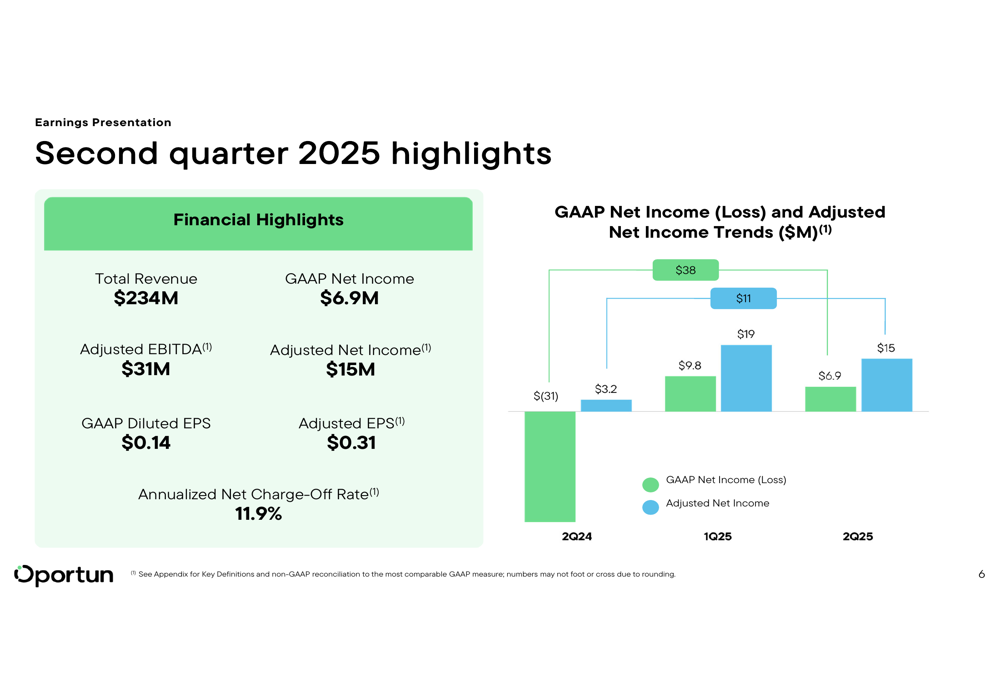

As shown in the following comprehensive overview of the quarter’s performance:

Total (EPA:TTEF) revenue for the quarter was $234 million, down $16 million year-over-year, primarily due to the $10 million impact from the credit card portfolio sale. However, net revenue increased significantly to $105 million, up $45 million year-over-year, as reduced fair value marks and net charge-offs more than offset the total revenue decline and higher interest expense.

The following chart illustrates the company’s GAAP Net Income and Adjusted Net Income trends:

Notably, Oportun’s Q2 revenue of $234 million fell slightly below its guidance range of $237-$242 million, while the company met its targets for the annualized net charge-off rate (11.9%) and adjusted EBITDA ($31 million, within the $29-$34 million guidance range).

Credit Quality Improvements

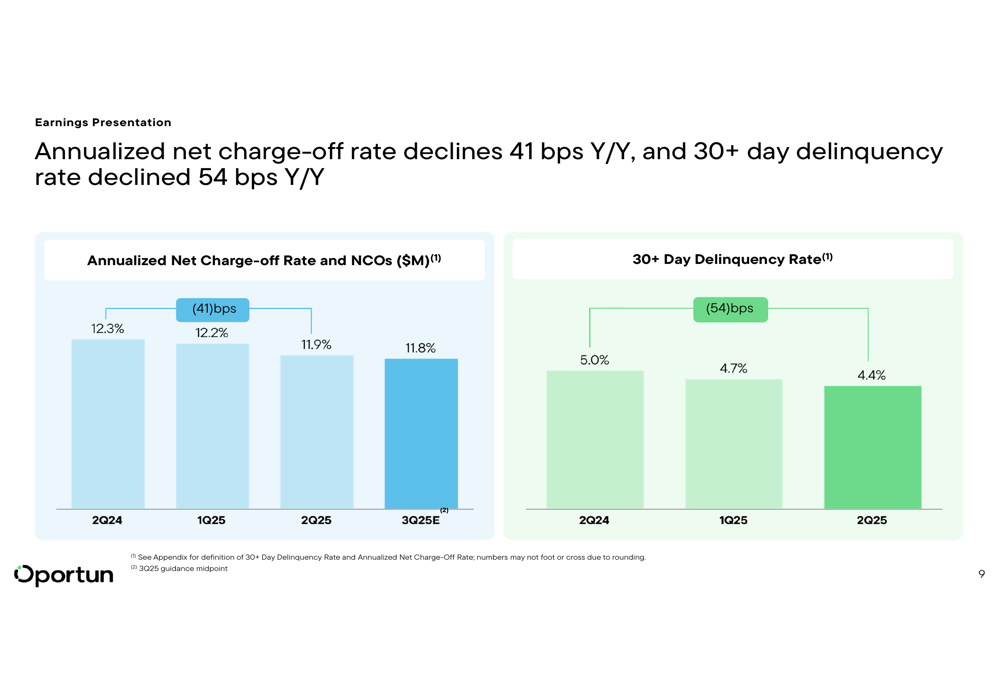

A key driver of Oportun’s improved profitability has been the consistent enhancement in credit quality metrics. The company reported an annualized net charge-off rate of 11.9% for Q2 2025, representing a 41 basis point improvement year-over-year. Similarly, the 30+ day delinquency rate improved to 4.4%, down 54 basis points from Q2 2024.

The following chart demonstrates the declining trend in both net charge-off rates and delinquency rates:

Oportun’s credit improvement strategy has been particularly effective as the company’s "back book" (loans originated before July 2022 credit tightening) has decreased to just 2% of the portfolio as of Q2 2025, down from 61% at year-end 2022. This transition has significantly improved overall portfolio performance, as the front book’s annualized net charge-off rate of 11.6% is substantially better than the back book’s 18.0%.

The company’s disciplined credit stance is reflected in its member stability metrics, with 100% of applicants having verified income (median gross income of approximately $50,000), 94% of borrowers receiving loans in U.S. bank accounts, average employment stability of 5.1 years with the same employer, and average residential stability of 5.3 years at the same residence.

Strategic Initiatives

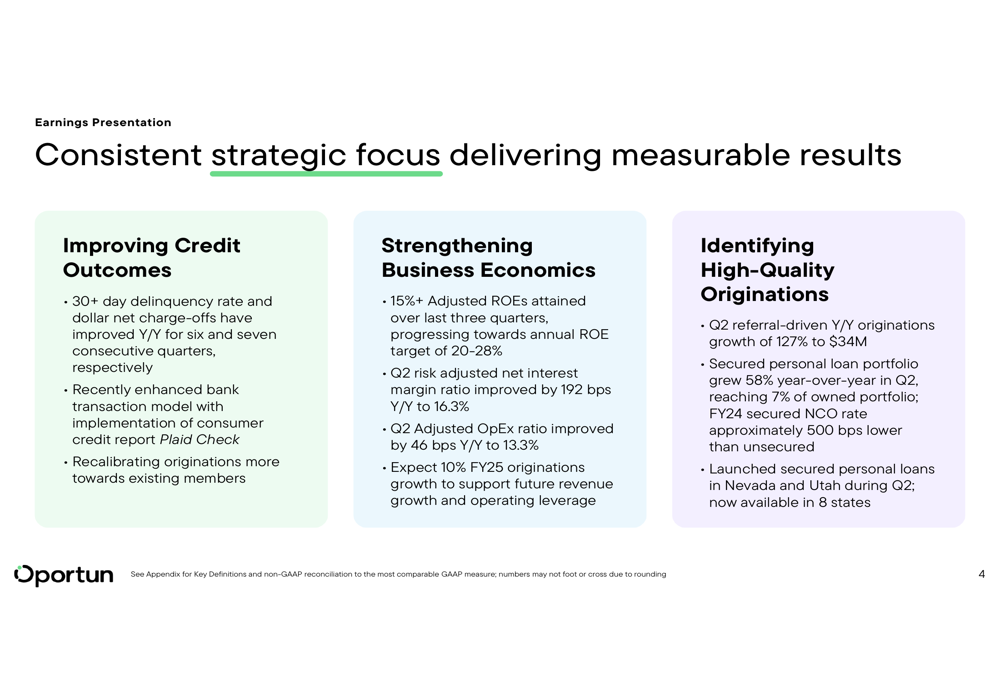

Oportun’s strategic focus on high-quality originations and operational efficiency continues to yield positive results. The company has achieved six and seven consecutive year-over-year improvements in credit outcomes, while strengthening business economics with 15%+ adjusted ROEs.

As illustrated in the following strategic overview:

Particularly noteworthy is the company’s focus on secured personal loans, which grew 58% year-over-year in Q2, reaching 7% of the owned portfolio. These secured loans have demonstrated significantly better performance, with an NCO rate approximately 500 basis points lower than unsecured loans.

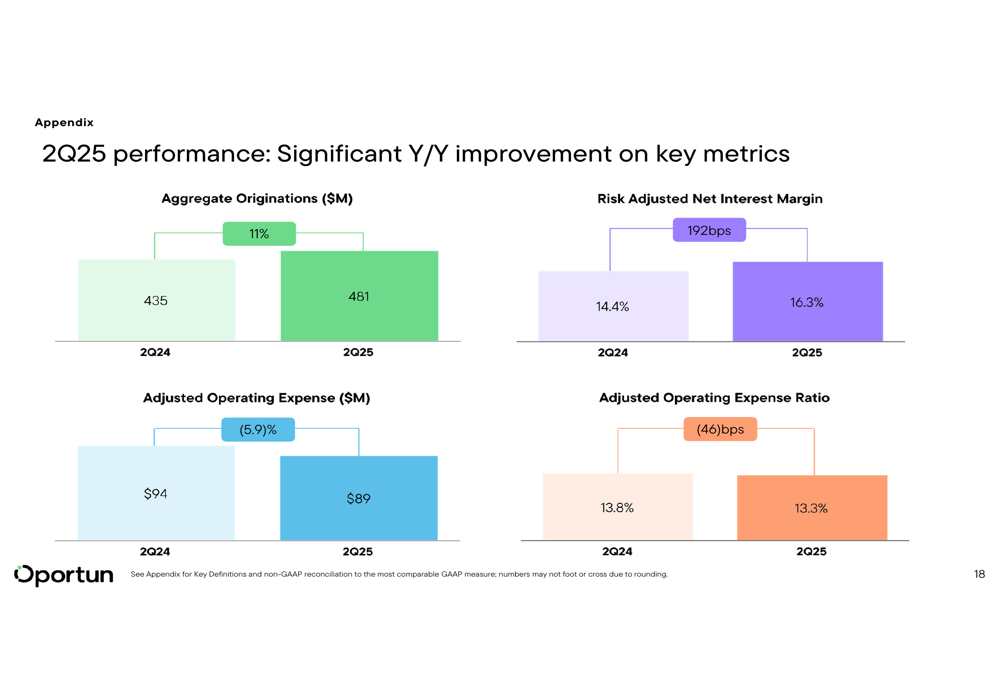

Additionally, referral-driven originations grew 127% year-over-year to $34 million, highlighting the effectiveness of Oportun’s targeted acquisition strategy. Overall aggregate originations increased by 11% year-over-year to $481 million.

The company’s year-over-year improvements across key metrics are clearly demonstrated in the following chart:

Oportun has also made significant progress in strengthening its balance sheet, reducing leverage from 7.6x to 7.3x quarter-over-quarter while repaying $55 million of debt during Q2. The company maintains strong liquidity with $1,201 million in available sources and 86% fixed-rate debt.

Forward-Looking Guidance

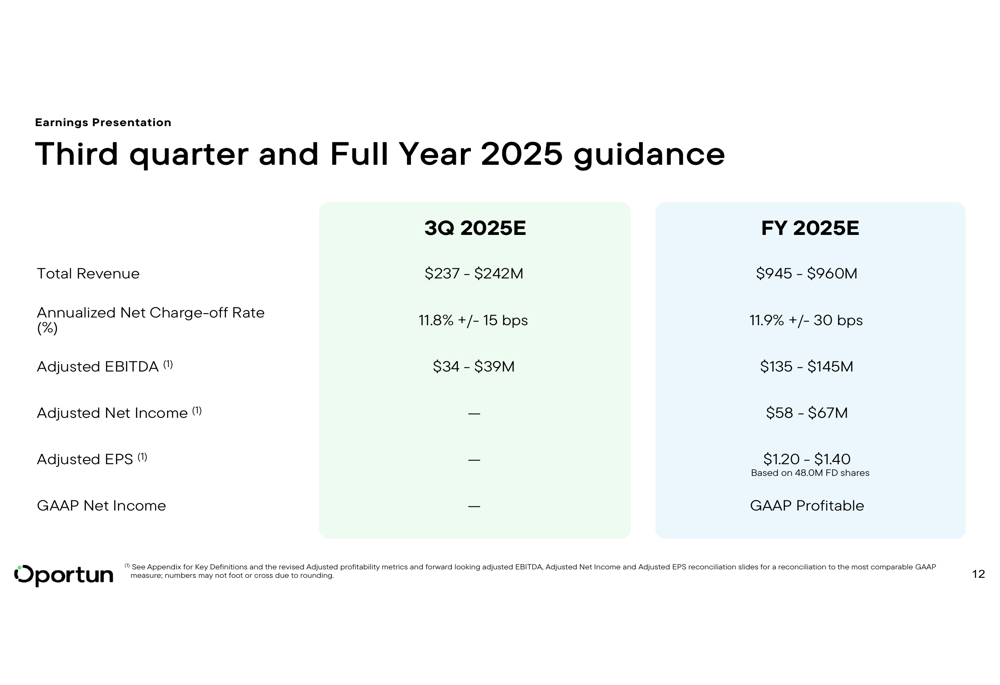

Based on its strong performance in the first half of 2025, Oportun has provided guidance for both Q3 and the full year 2025. For Q3 2025, the company expects total revenue of $237-$242 million, an annualized net charge-off rate of 11.8% (±15 bps), and adjusted EBITDA of $34-$39 million.

For the full year 2025, Oportun raised its adjusted EPS guidance to $1.20-$1.40, representing 67-94% growth. The company expects total revenue of $945-$960 million, an annualized net charge-off rate of 11.9% (±30 bps), and adjusted EBITDA of $135-$145 million. Importantly, Oportun reaffirmed its expectation to achieve GAAP profitability for the full year.

The detailed guidance is presented in the following chart:

This guidance represents a significant improvement from the previous quarter. In Q1 2025, Oportun reported earnings per share of $0.40, substantially exceeding the forecast of $0.05, with revenue of $235.9 million against an anticipated $228.66 million. The company’s stock has shown strong performance, with returns of 99.68% over the past six months and 68.96% over the last year, according to previous reports.

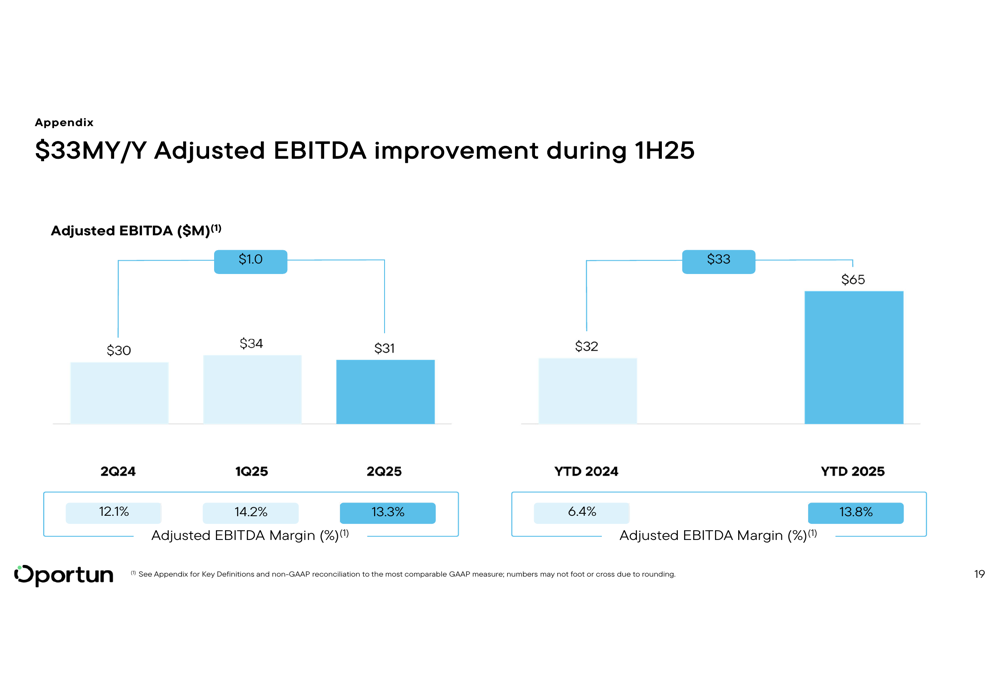

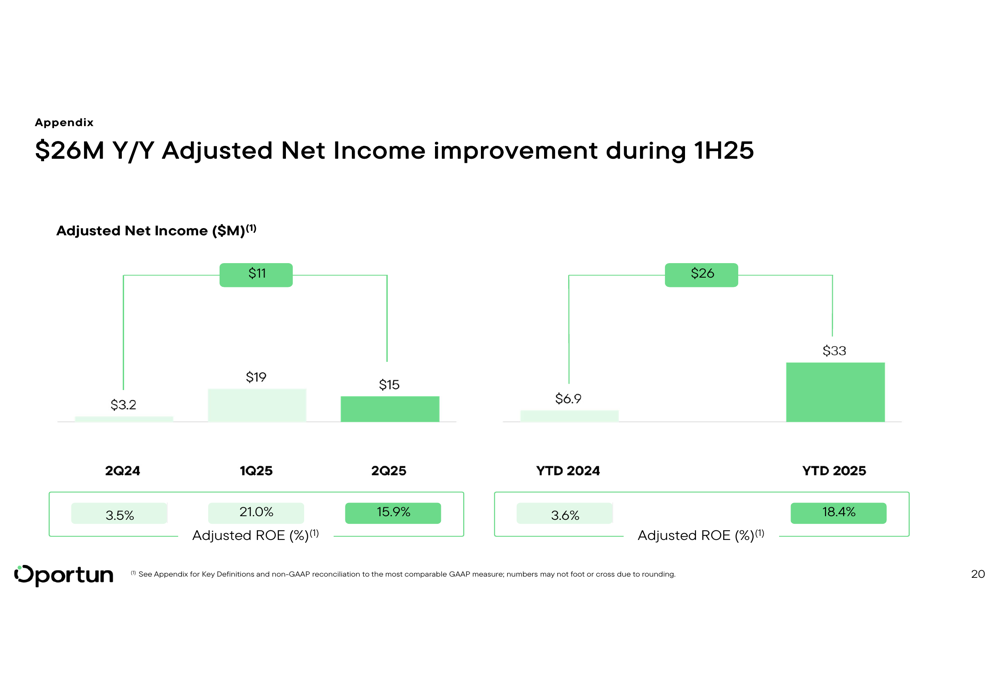

The first half of 2025 has already shown substantial year-over-year improvements, with adjusted EBITDA increasing by $33 million and adjusted net income improving by $26 million compared to the first half of 2024:

Oportun’s continued focus on operational efficiency, credit quality improvements, and strategic originations positions the company well for sustained profitability in the remainder of 2025 and beyond, despite the slight revenue miss in Q2. The company’s transition away from its pre-July 2022 "back book" is nearly complete, which should further stabilize credit performance in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.