Intel surges more than 8% after chipmaker’s profits top expectations

Introduction & Market Context

Orange Polska (WSE:OPL) presented its second quarter 2025 financial results on July 29, showing steady growth across key metrics despite competitive market pressures. The company’s stock responded positively, rising 1.47% to close at 7.34 PLN, contributing to an impressive 25.06% year-to-date return.

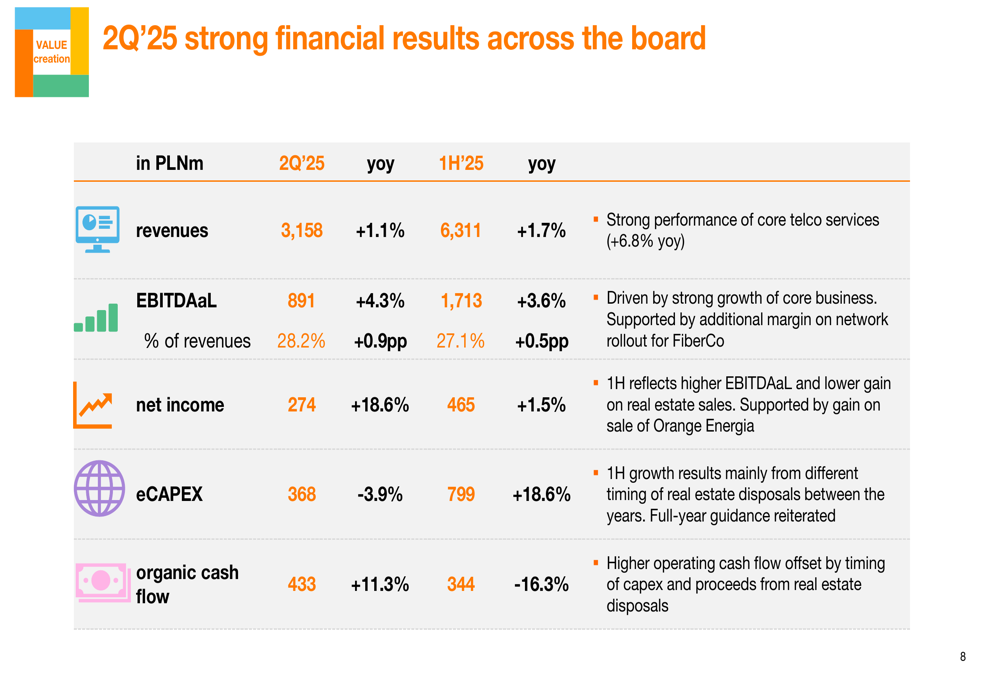

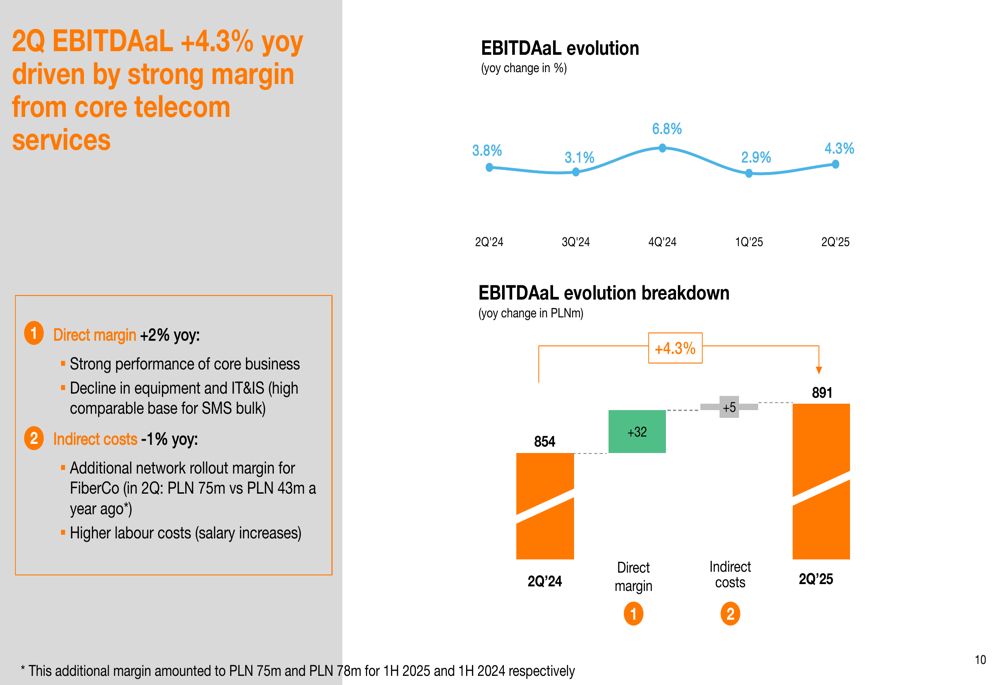

The Polish telecom provider reported a 1.1% year-over-year increase in Q2 revenue, reaching PLN 3,158 million, while EBITDAaL (EBITDA after Leases) grew by 4.3% to PLN 891 million. The results reflect Orange Polska’s successful focus on core telecom services amid challenging market conditions in equipment sales and the B2B segment.

Quarterly Performance Highlights

Orange Polska delivered strong financial performance in Q2 2025, with notable improvements across all key metrics. Revenue increased by 1.1% year-over-year to PLN 3,158 million, while EBITDAaL rose 4.3% to PLN 891 million, representing 28.2% of revenues (a 0.9 percentage point improvement). Net income showed the strongest growth at 18.6%, reaching PLN 274 million.

As shown in the following financial results overview:

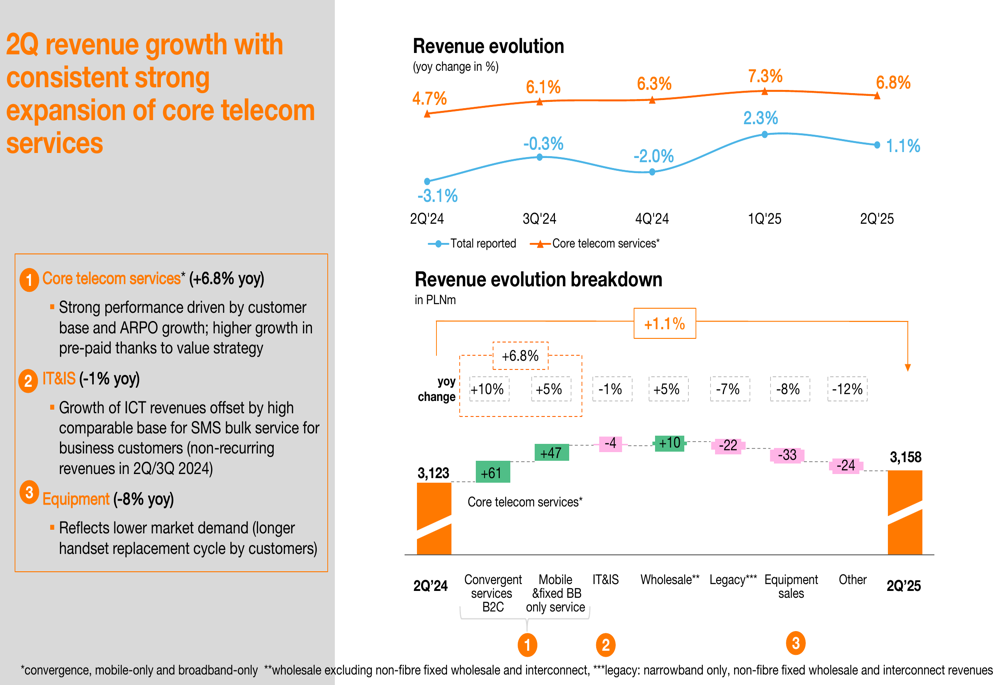

The company’s core telecom services demonstrated particularly strong performance, with revenue growth of 6.8% year-over-year. This growth was driven by both customer base expansion and ARPO (Average Revenue Per Offer) increases. The company also benefited from its value strategy in the pre-paid segment.

This positive revenue trend is clearly visible in the quarterly progression:

However, equipment sales declined by 8% year-over-year, reflecting lower market demand as customers extend their handset replacement cycles. IT and Integration Services revenue also decreased slightly (-1% YoY) due to a high comparable base for SMS bulk service for business customers in 2024.

Strategic Initiatives

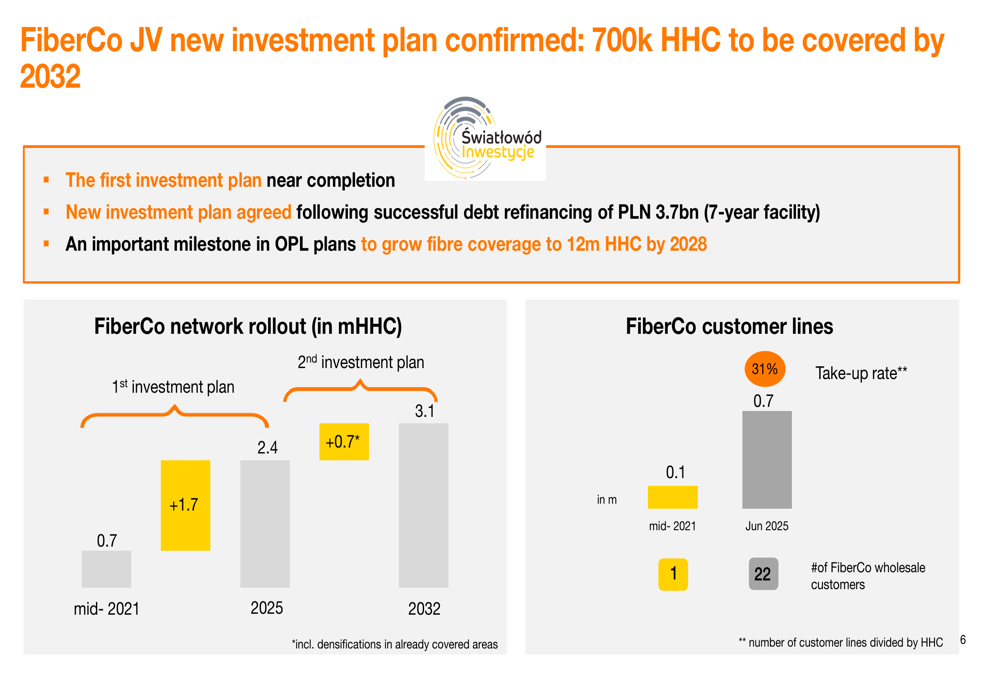

Orange Polska’s presentation highlighted several strategic initiatives aimed at strengthening its market position and supporting long-term growth. A key development is the new investment plan for FiberCo JV, which confirms an additional 700,000 households to be covered by 2032. This expansion follows successful debt refinancing of PLN 3.7 billion through a seven-year facility.

The FiberCo network rollout represents an important component of Orange Polska’s ambitious plan to grow fibre coverage to 12 million households by 2028:

Another strategic move highlighted in the presentation was the sale of Orange Energia, which confirms the company’s focus on its core telecommunications business. This divestment contributed positively to the bottom line with an estimated gain of PLN 71 million in the first half of 2025.

The company continues to invest in its mobile network, with ongoing 5G rollout in both core and RAN (Radio Access Network) renewal. These investments are reflected in the capital expenditure breakdown, with mobile network investments accounting for PLN 197 million in 1H 2025.

Customer Base Growth

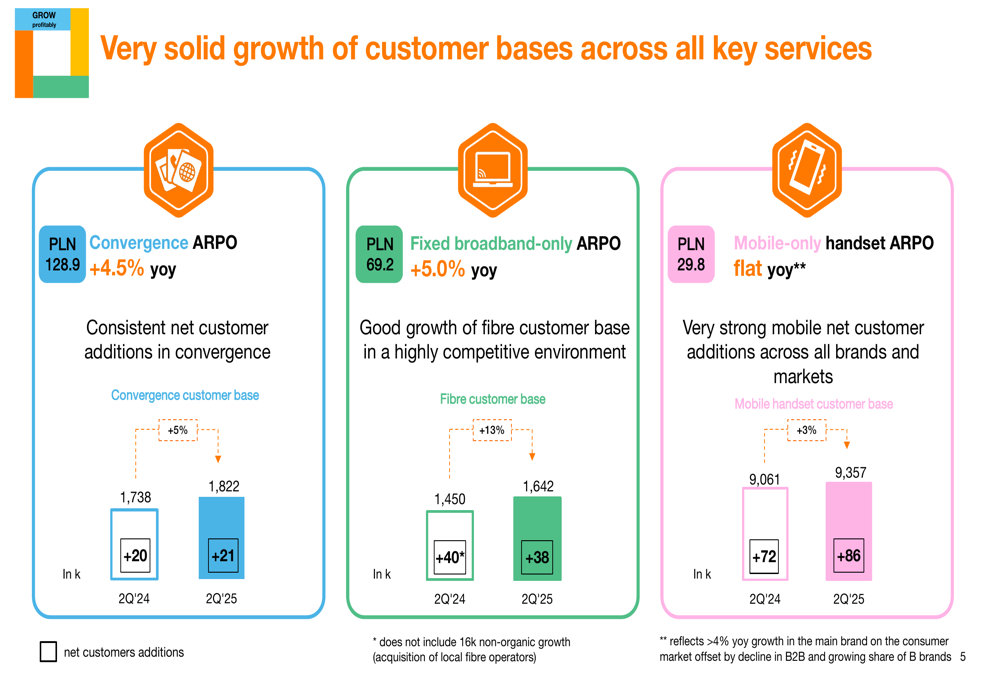

Orange Polska reported customer growth across all key service categories, demonstrating its ability to attract and retain subscribers in a competitive market environment. The convergence customer base grew to 1,822,000, adding 21,000 customers in Q2 and 84,000 year-over-year. The fixed broadband-only segment expanded to 1,642,000 customers, including 16,000 non-organic growth, while mobile-only handset subscribers increased to 9,357,000.

The following chart illustrates this consistent growth across all service categories:

ARPO metrics also showed positive trends, with convergence ARPO increasing by 4.5% year-over-year to PLN 128.9 and fixed broadband-only ARPO rising by 5.0% to PLN 69.2. Mobile-only handset ARPO remained flat at PLN 29.8, but this masked underlying strength in the main brand, which grew by more than 4% in the consumer market, offset by declines in B2B and a growing share of budget brands.

Detailed Financial Analysis

The company’s EBITDAaL growth of 4.3% in Q2 2025 was driven by strong margin performance in core telecom services. Direct margin increased by 2% year-over-year, while indirect costs decreased by 1%, benefiting from additional network rollout margin for FiberCo (PLN 75 million in Q2 2025 versus PLN 43 million a year ago), partially offset by higher labor costs due to salary increases.

The EBITDAaL evolution shows consistent growth over five consecutive quarters:

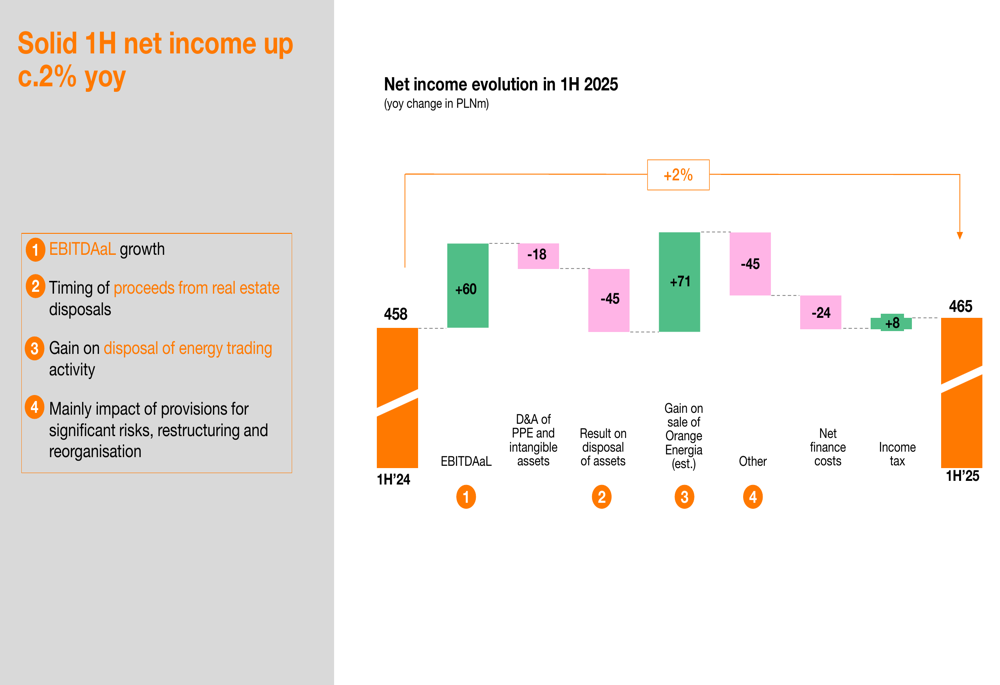

Net income for the first half of 2025 reached PLN 465 million, representing a 1.5% increase year-over-year. This modest growth reflects the positive impact of EBITDAaL growth and the gain from the Orange Energia sale, offset by higher depreciation and amortization expenses, lower gains from asset disposals, and increased net finance costs.

The waterfall chart below illustrates the key factors influencing net income evolution:

Capital expenditure (eCapex) for the first half of 2025 increased by 18.6% to PLN 799 million, primarily due to investments in fibre networks for EU-subsidized projects, 5G network rollout, and IT systems transformation. The increase also reflects different timing of proceeds from real estate disposals compared to the previous year.

Forward-Looking Statements

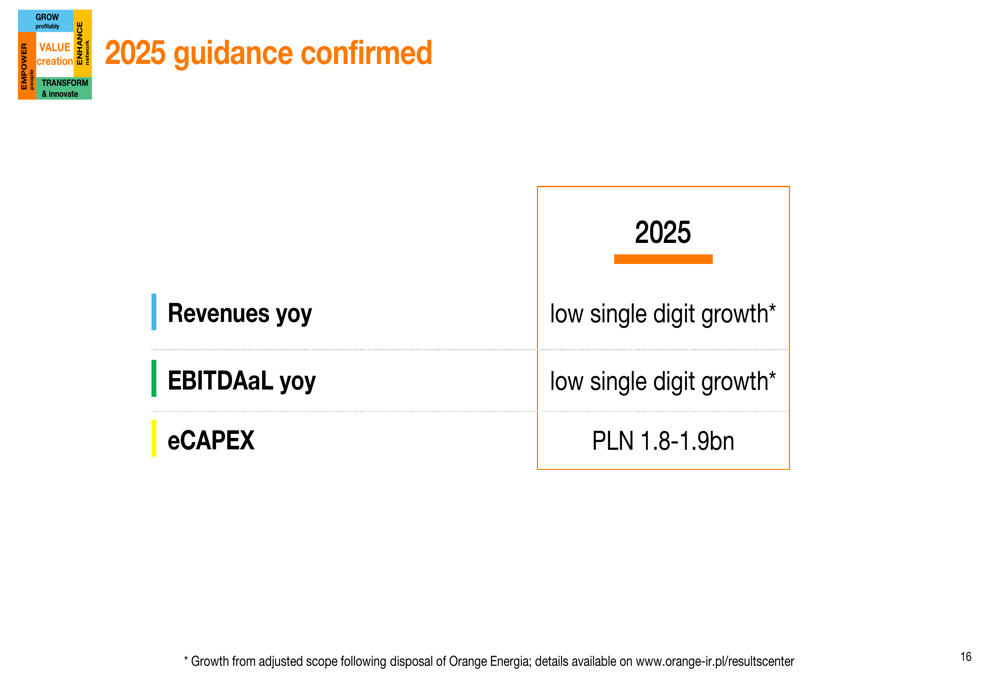

Orange Polska confirmed its full-year guidance for 2025, projecting low single-digit growth for both revenues and EBITDAaL, adjusted for the disposal of Orange Energia. The company expects capital expenditure to remain between PLN 1.8-1.9 billion for the year.

The guidance summary is presented below:

Looking beyond 2025, the company is preparing transformation initiatives for 2026 and beyond, while focusing on the high commercial season in the second half of 2025 and progressive turnaround in the B2B segment.

CEO Liudmila Climoc emphasized the importance of continuous investment in infrastructure, stating, "Our commercial success is underpinned by continuous investment in mobile and fixed infrastructure." This sentiment underscores the company’s commitment to long-term growth through infrastructure development.

Competitive Industry Position

Orange Polska maintains a strong position in the Polish telecommunications market despite intense competition, particularly in the fixed broadband segment. The company’s consistent customer growth across all service categories demonstrates its competitive resilience and the effectiveness of its value proposition.

The FiberCo JV’s network expansion enhances Orange Polska’s competitive position in the fixed broadband market, with 22 wholesale customers already utilizing the infrastructure. The take-up rate for FiberCo customer lines stands at 31%, indicating solid demand for high-speed connectivity services.

While the company faces challenges in the B2B segment and equipment sales, its focus on core telecom services and infrastructure development positions it well for sustainable growth in a competitive landscape. The confirmed guidance for 2025 reflects management’s confidence in navigating these market dynamics successfully.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.