S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Organon & Co (NYSE:OGN) reported first quarter 2025 results showing revenue of $1.5 billion, down 7% as reported and 4% excluding foreign exchange impacts. The decline was primarily attributed to the loss of exclusivity (LOE) for Atozet, though this was partially offset by strong performance in the Women’s Health segment. Despite the revenue challenges, the company maintained its full-year 2025 guidance.

The results come amid significant market volatility for the stock, which saw a substantial 17.4% decline in premarket trading following the earnings release, with the stock price dropping to $10.68. This reaction contrasts with the generally stable operational performance detailed in the presentation.

Quarterly Performance Highlights

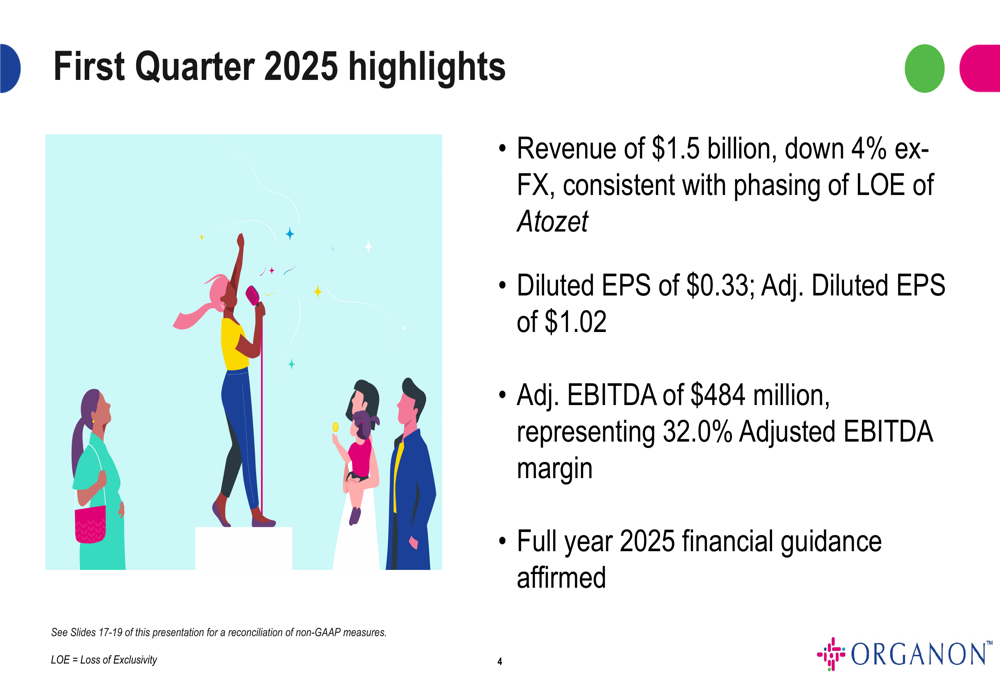

Organon reported Q1 2025 revenue of $1.5 billion, with adjusted diluted EPS of $1.02 and adjusted EBITDA of $484 million, representing a 32.0% margin. These results reflect the anticipated impact of Atozet’s loss of exclusivity while highlighting the company’s ability to maintain strong profitability.

As shown in the following quarterly highlights:

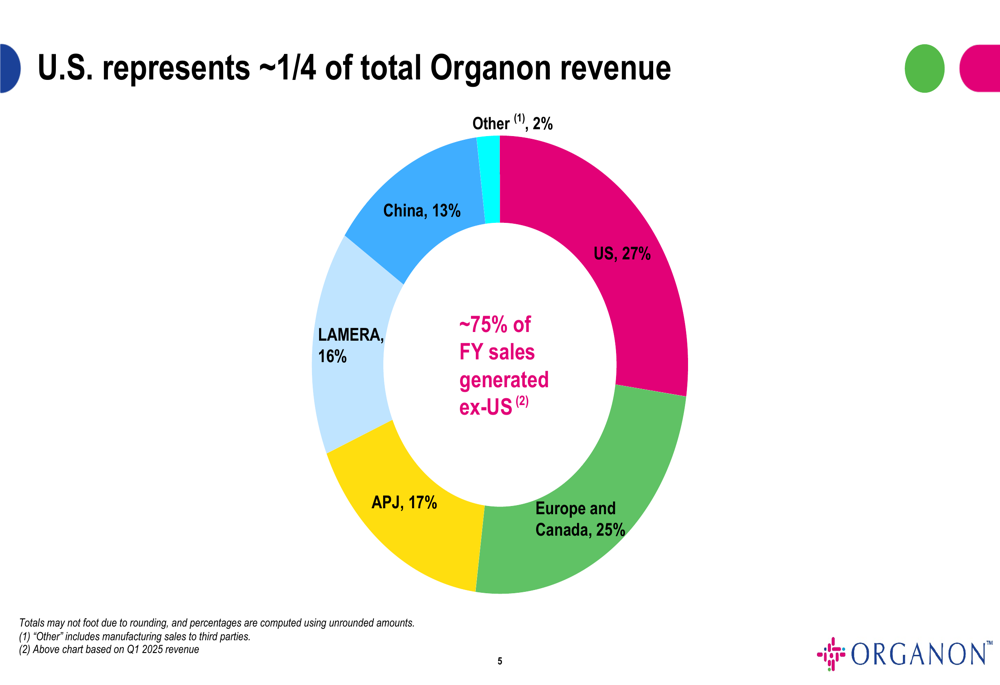

The company’s geographic revenue diversification remains a key strength, with approximately 75% of sales generated outside the United States. This global footprint helps buffer against regional market fluctuations and provides multiple growth avenues.

The following chart illustrates Organon’s geographic revenue distribution:

Women’s Health as Growth Driver

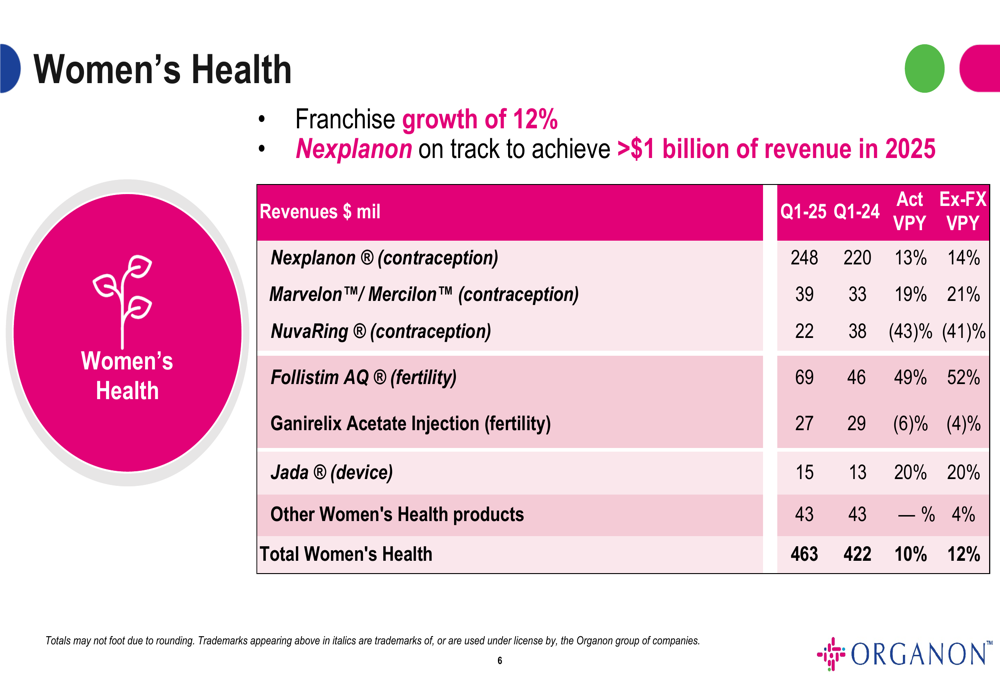

The Women’s Health franchise emerged as the standout performer, growing 12% on an ex-FX basis to $463 million. Nexplanon, the company’s contraceptive implant, led this growth with a 14% increase (ex-FX), putting it on track to exceed $1 billion in revenue for 2025. This performance reinforces Women’s Health as Organon’s primary growth engine.

The detailed performance of the Women’s Health portfolio is illustrated in this breakdown:

Fertility treatments also contributed significantly to the segment’s growth, with Follistim AQ posting a 52% increase (ex-FX). This robust performance in Women’s Health is crucial as the company navigates headwinds in other segments.

Navigating LOE Challenges

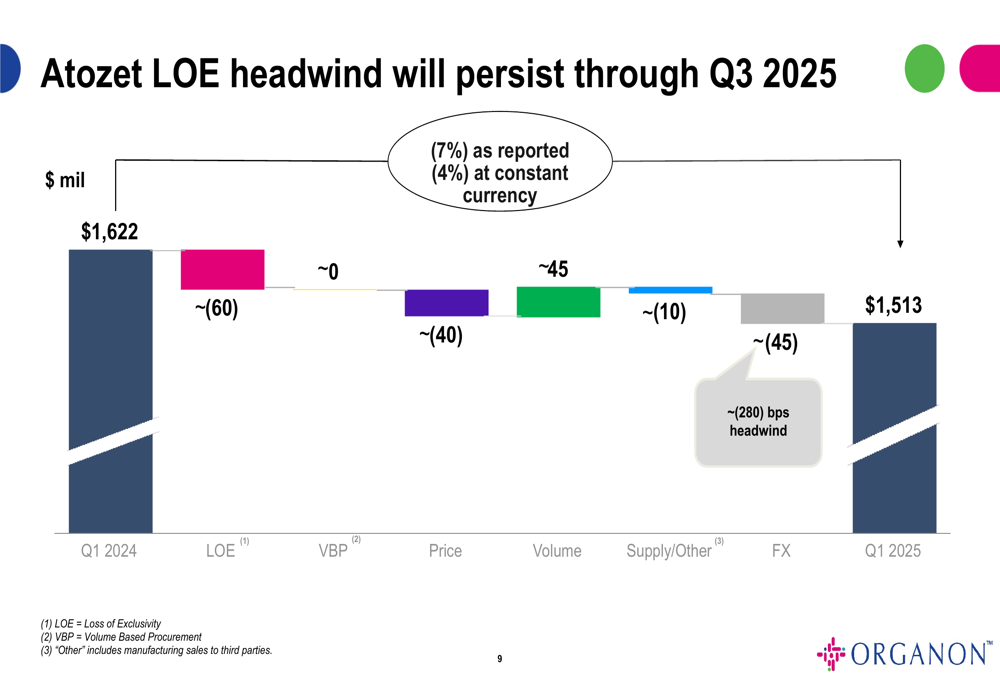

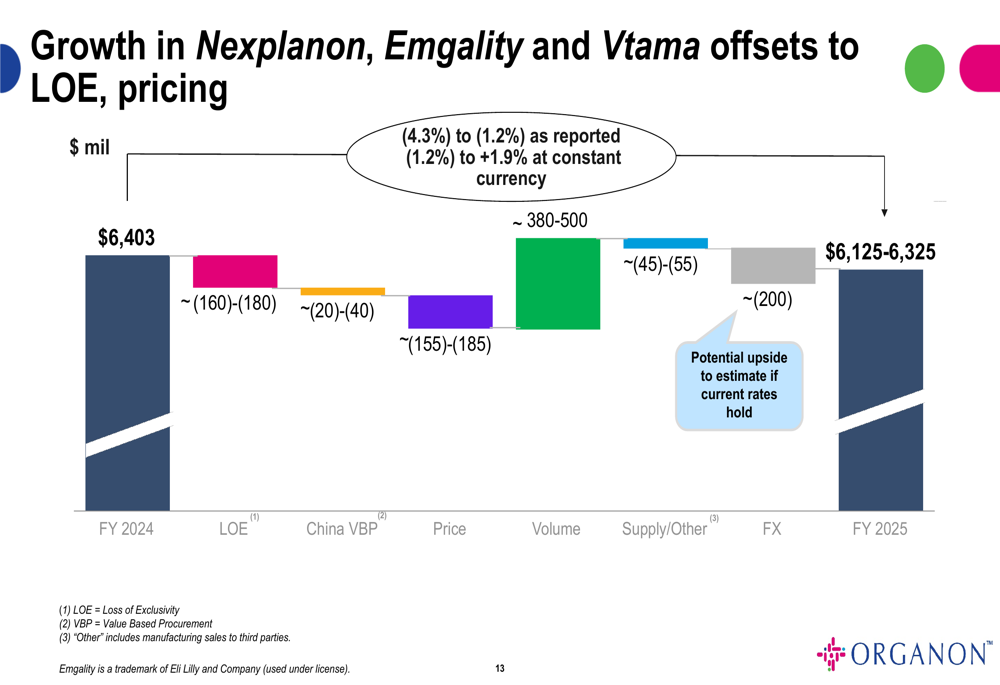

The loss of exclusivity for Atozet, a cholesterol medication, created a significant revenue headwind in Q1 2025. The company quantified this impact at approximately $60 million for the quarter, with additional pressure from pricing and foreign exchange effects.

The following waterfall chart visualizes how various factors affected Q1 revenue:

To offset these challenges, Organon is leveraging growth from newer products. The company highlighted that Emgality and Vtama are expected to partially counterbalance Atozet’s LOE impact throughout 2025. Vtama, a dermatology treatment, generated $24 million in Q1 sales and is projected to deliver $150 million for the full year.

The company’s strategy for managing these offsets is detailed in this projection:

Financial Position

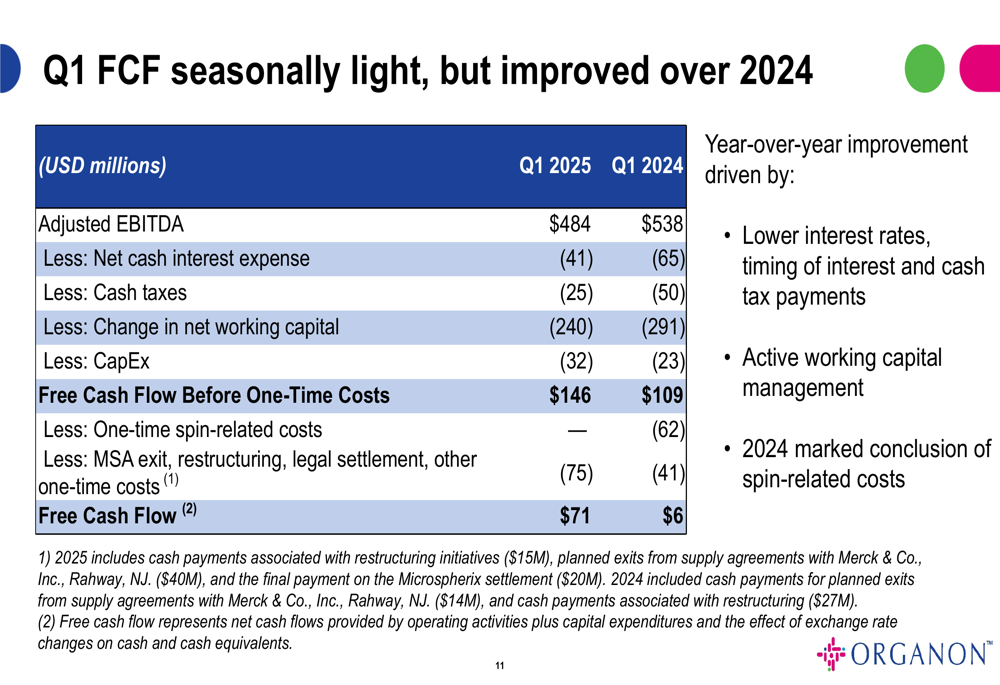

Despite revenue challenges, Organon demonstrated improved financial efficiency in Q1. Free cash flow increased substantially to $71 million, compared to just $6 million in Q1 2024. This improvement came despite seasonally light cash generation, reflecting better working capital management and reduced one-time costs.

The following breakdown shows the components of this free cash flow improvement:

The company’s leverage position remains elevated, with a net leverage ratio of approximately 4.3x as of March 31, 2025. Net debt increased slightly to $8,409 million, primarily due to unfavorable foreign exchange impacts and a decrease in cash balance.

Forward-Looking Statements

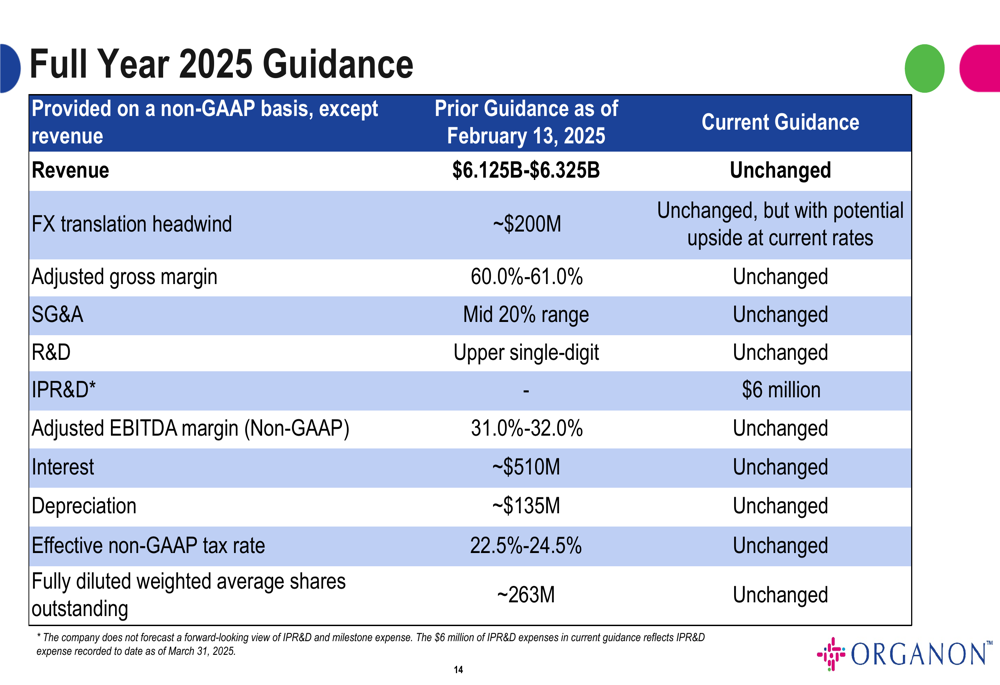

Organon affirmed its full-year 2025 guidance, projecting revenue between $6.125 billion and $6.325 billion. The company expects an adjusted EBITDA margin of 31.0%-32.0%, maintaining its profitability targets despite revenue pressures.

The detailed guidance is presented in this comprehensive overview:

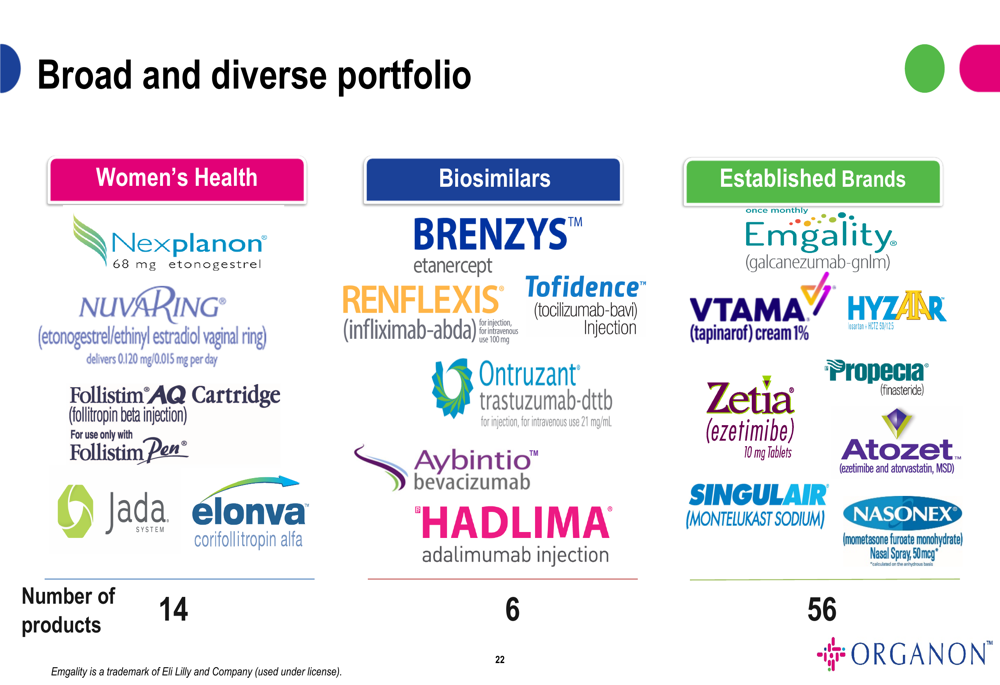

The company’s diverse portfolio provides multiple avenues for growth and stability. Organon’s product lineup includes 14 Women’s Health products, 6 Biosimilars, and 56 Established Brands, creating a broad foundation that helps mitigate individual product risks.

This extensive portfolio is illustrated in the following breakdown:

Strategic Initiatives

Looking ahead, Organon is pursuing several strategic initiatives to drive growth. In the Biosimilars segment, the company is preparing for a potential U.S. denosumab launch in late 2025, which could provide a new revenue stream. The continued expansion of Vtama represents the company’s push into dermatology, diversifying beyond its core therapeutic areas.

The Women’s Health franchise remains the strategic priority, with Nexplanon’s growth trajectory serving as the cornerstone of Organon’s near-term outlook. The company’s geographic diversification strategy also continues, with particular focus on maintaining strength in emerging markets despite currency headwinds.

As Organon navigates the challenges of 2025, its ability to execute on these strategic initiatives while managing the Atozet LOE impact will be crucial for delivering on its financial guidance and rebuilding investor confidence amid recent stock volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.