Fubotv earnings beat by $0.10, revenue topped estimates

Organon & Co (NYSE:OGN) shares jumped over 6% in premarket trading after the company’s Q2 2025 earnings presentation revealed raised revenue guidance and continued progress on debt reduction, despite ongoing challenges from loss of exclusivity (LOE) and pricing pressures.

Quarterly Performance Highlights

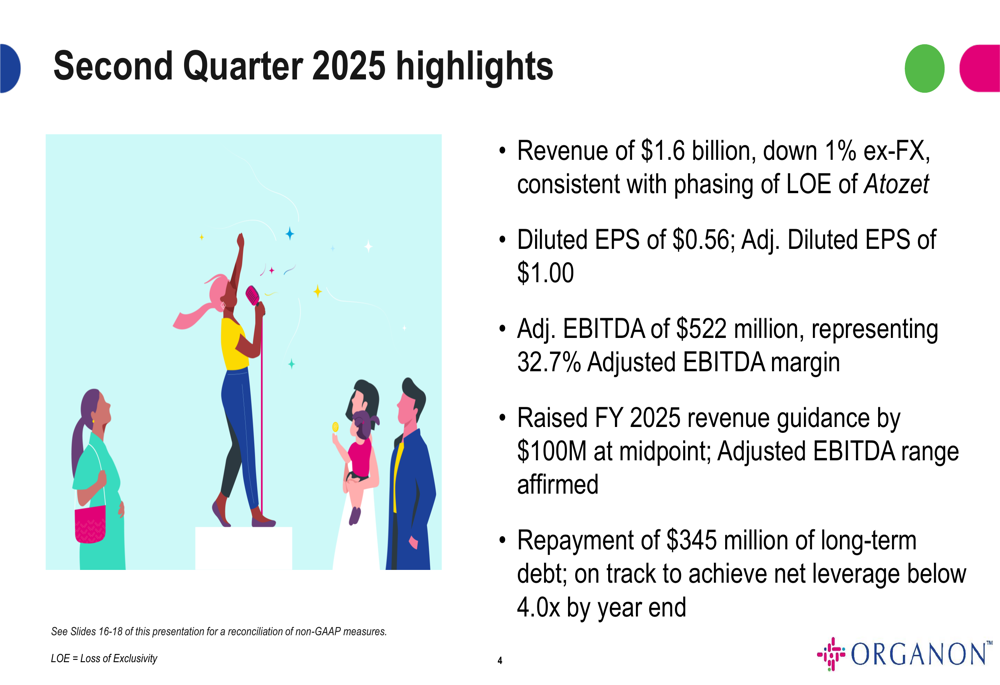

Organon reported Q2 2025 revenue of $1.6 billion, down 1% excluding foreign exchange effects, which the company attributed largely to the loss of exclusivity for Atozet. Diluted earnings per share came in at $0.56 on a GAAP basis, while adjusted diluted EPS reached $1.00. The company achieved an adjusted EBITDA of $522 million, representing a 32.7% margin, an improvement from 31.9% in the same quarter last year.

As shown in the following summary of Q2 highlights, the company made significant progress on debt reduction while raising its full-year revenue guidance:

This performance marks a notable improvement from Q1 2025, when Organon reported a 4% revenue decline and saw its stock plummet 24.25% following the announcement. The company’s Q2 results suggest stabilization and improved outlook, reflected in the positive premarket trading reaction.

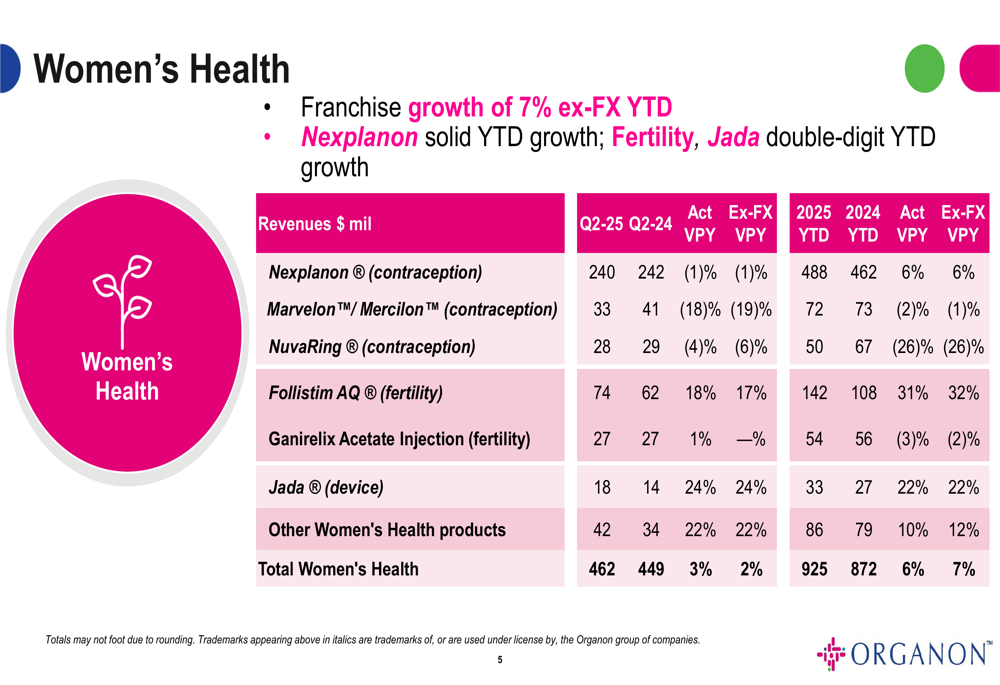

Women’s Health & Growth Products

The Women’s Health franchise continues to be a bright spot for Organon, growing 7% year-to-date on a constant currency basis. Nexplanon, the company’s contraceptive implant, showed solid growth with year-to-date sales of $488 million, up 6% from the same period in 2024. Fertility products and Jada, a device for postpartum hemorrhage, both delivered double-digit growth.

The detailed breakdown of Women’s Health performance demonstrates the strength across multiple products:

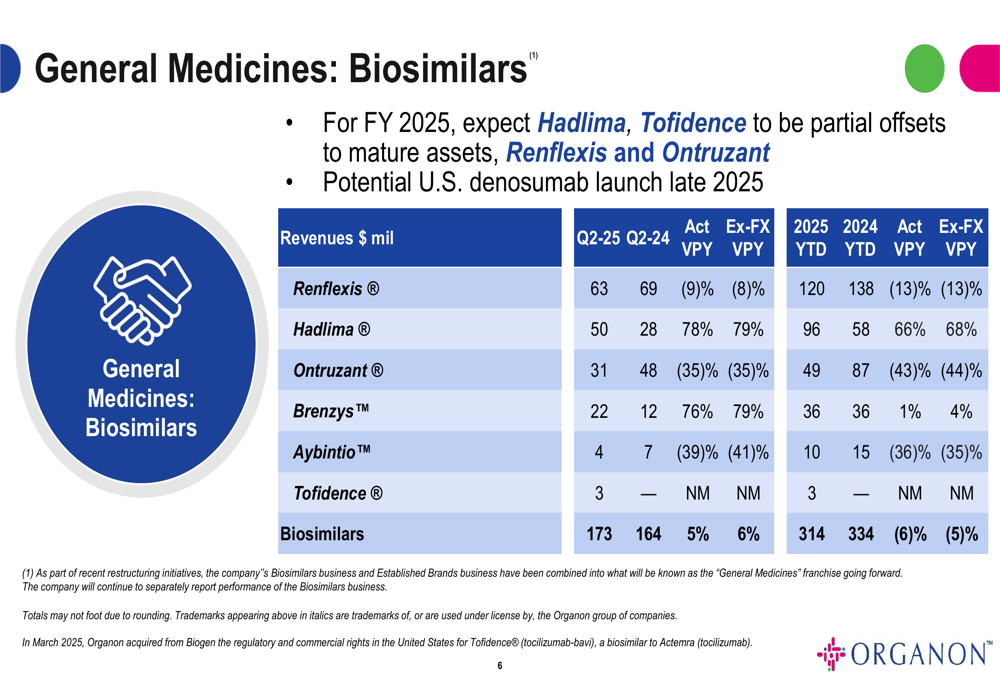

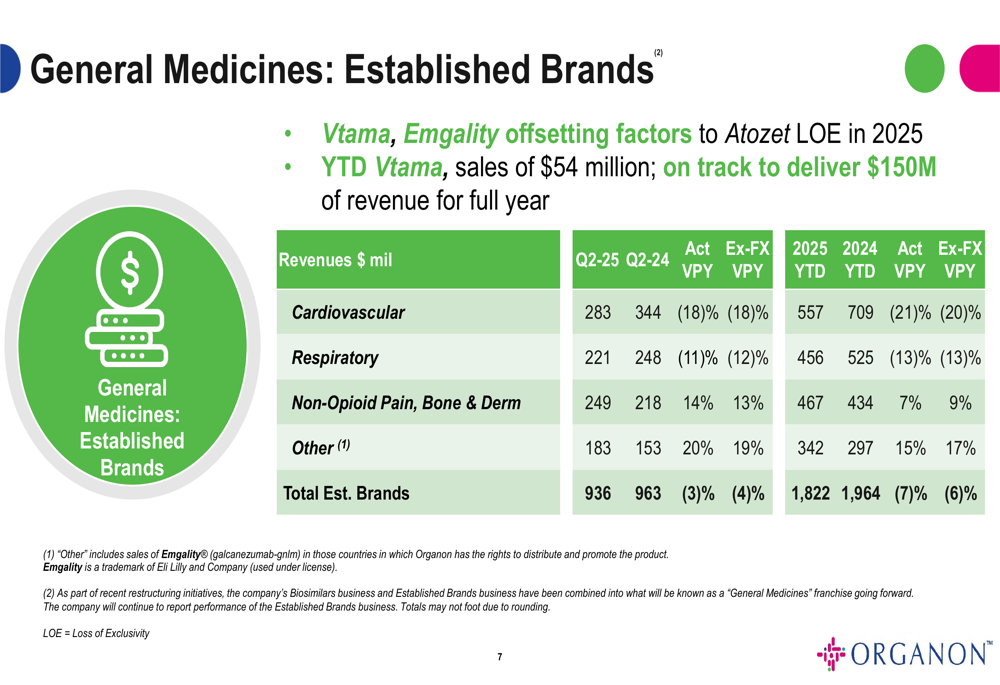

In the General Medicines segment, newer products are helping to offset declines in mature brands. Vtama, a treatment for plaque psoriasis, has generated $54 million in sales year-to-date and is on track to deliver $150 million in revenue for the full year, consistent with the company’s projections from Q1. Similarly, in the biosimilars portfolio, Hadlima showed strong growth of 79% ex-FX in Q2, helping to counterbalance declines in older biosimilars.

The following chart illustrates the performance of Organon’s biosimilars portfolio:

Challenges & Headwinds

Despite the positive developments in growth products, Organon continues to face headwinds from loss of exclusivity and pricing pressures. The company’s established brands segment, which includes cardiovascular and respiratory products, declined 6% year-to-date on a constant currency basis, primarily due to the LOE impact on Atozet.

The following breakdown of established brands performance highlights these challenges:

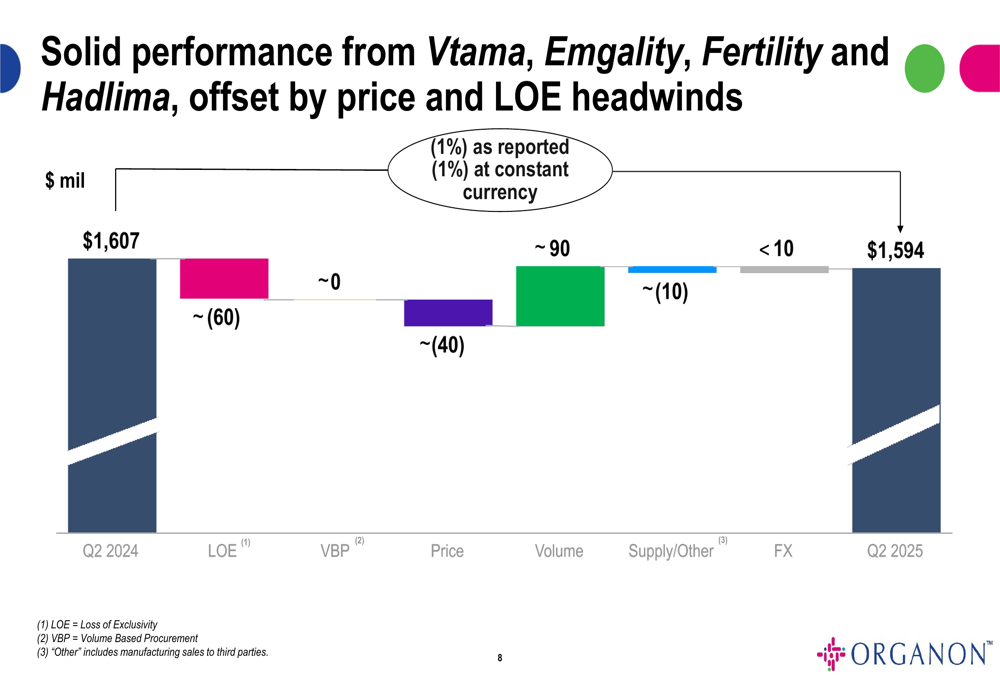

A closer examination of the factors affecting Q2 revenue reveals that while volume growth contributed positively (+$90 million), this was offset by LOE impact (-$60 million) and pricing pressures (-$40 million):

Financial Position & Debt Reduction

Organon made significant progress on debt reduction in Q2, repaying $345 million of long-term debt. The company maintains it is on track to achieve its target of reducing net leverage below 4.0x by year-end, down from approximately 4.3x at the end of June 2025.

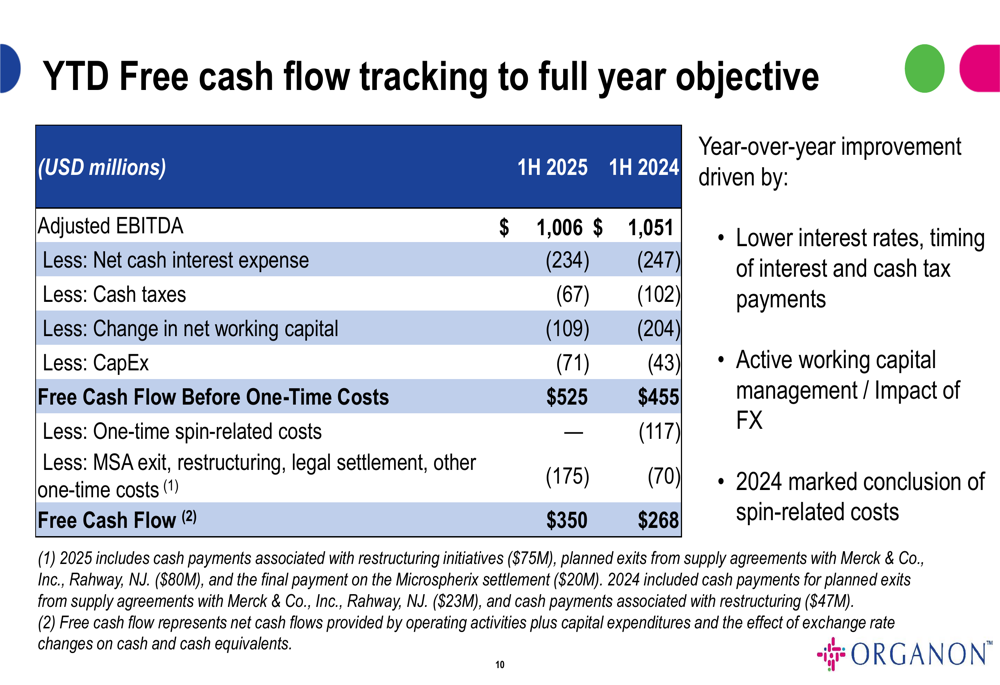

The company’s strong cash generation supported these debt reduction efforts, with free cash flow before one-time costs reaching $525 million in the first half of 2025, a significant improvement from $455 million in the same period of 2024.

The following chart details Organon’s free cash flow performance:

Updated Guidance & Outlook

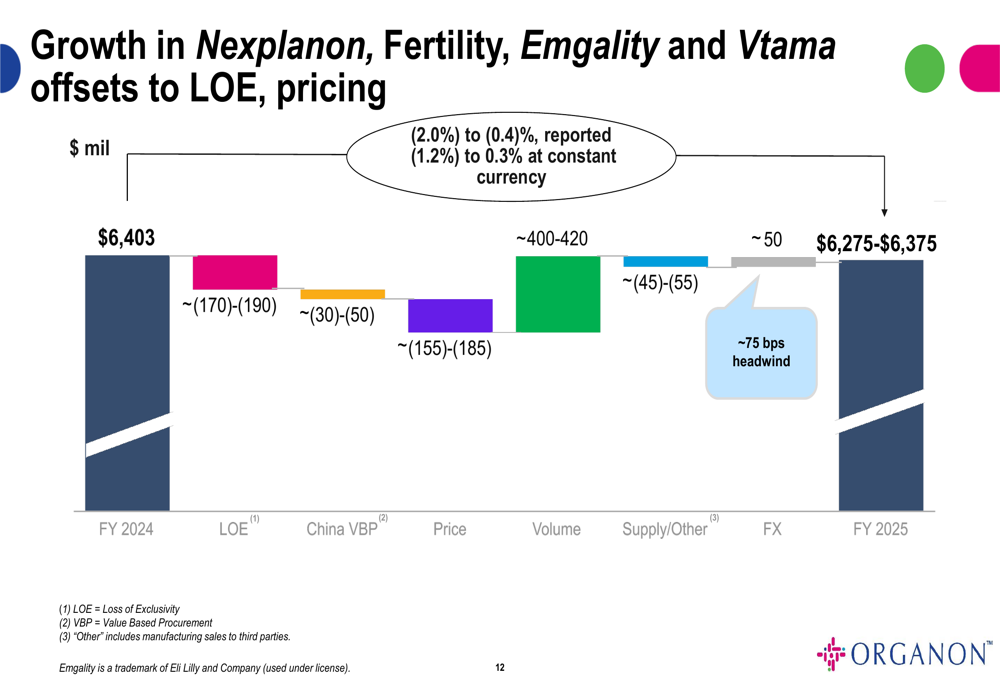

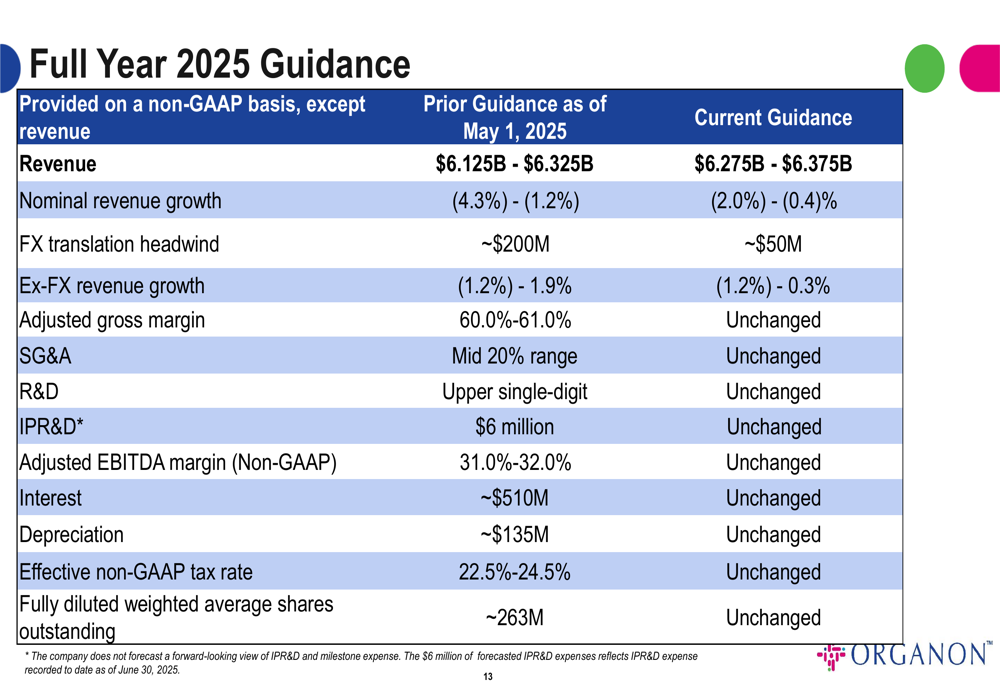

In a significant vote of confidence in its business trajectory, Organon raised its full-year 2025 revenue guidance by $100 million at the midpoint. The updated guidance range is now $6.275 billion to $6.375 billion, compared to the previous range of $6.125 billion to $6.325 billion.

The bridge analysis below illustrates the factors expected to influence full-year revenue performance:

The company maintained its adjusted EBITDA margin guidance of 31.0% to 32.0%, suggesting continued focus on operational efficiency despite revenue challenges. The full updated guidance is detailed below:

This improved outlook stands in contrast to the more cautious stance following Q1 results, when the company maintained flat revenue guidance year-over-year at the midpoint. The raised guidance reflects improved confidence in the company’s ability to offset LOE and pricing challenges with volume growth from its core Women’s Health franchise and newer products like Vtama and Emgality.

Strategic Focus

Organon continues to execute its strategy of building strength in Women’s Health while managing the transition in its established brands and biosimilars portfolios. The potential U.S. launch of denosumab, a biosimilar for bone health, in late 2025 represents another growth opportunity on the horizon.

Geographic diversification remains a key element of Organon’s approach, with strong performance in the U.S. (+9% YTD) and Latin America, Middle East, Russia and Africa regions (+3% YTD ex-FX) helping to offset challenges in Europe and Canada (-11% YTD ex-FX) and Asia Pacific (-7% YTD ex-FX).

With its improved revenue outlook and continued progress on debt reduction, Organon appears to be navigating its challenges more effectively than anticipated earlier in the year, though the company still faces significant headwinds from LOE impacts and pricing pressures in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.