FTSE 100 today: Index rises, GBP flat; Mitchells & Butlers jumps, Whitbread falls

Introduction & Market Context

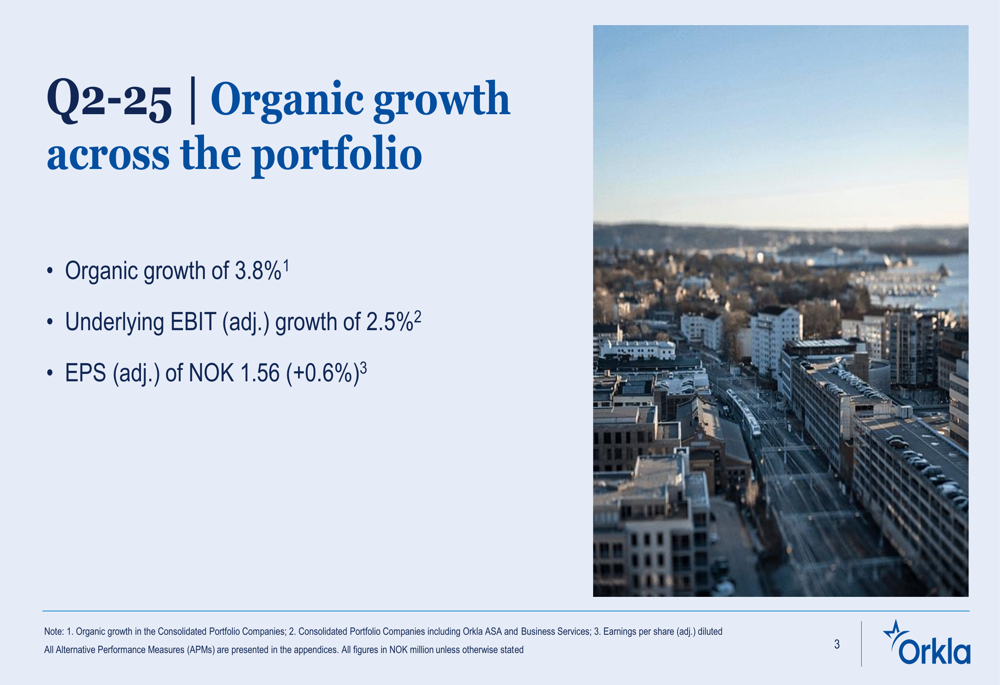

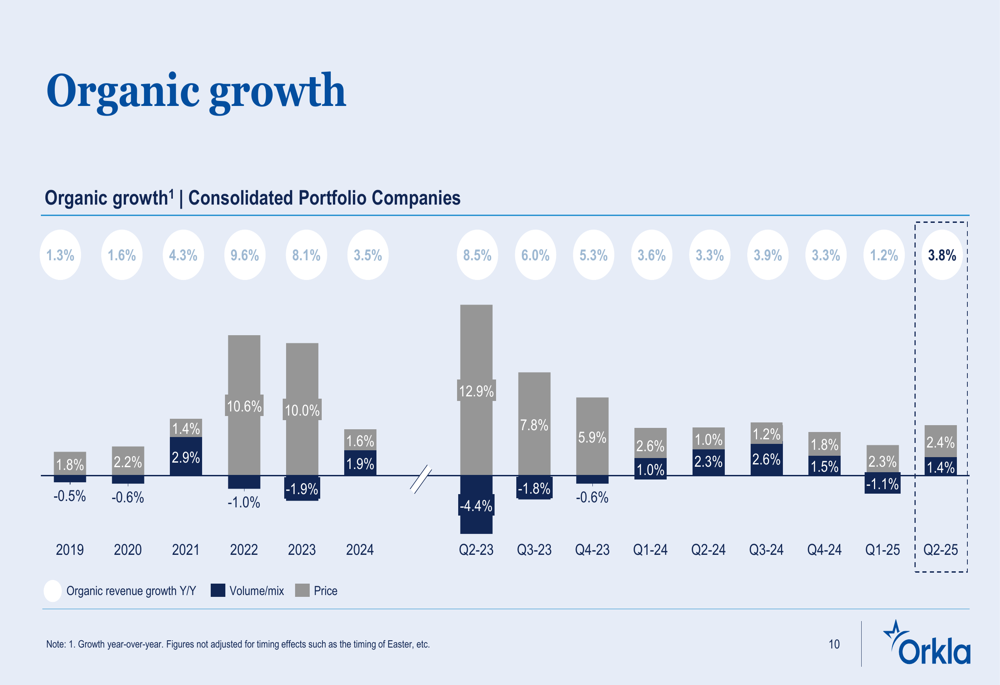

Norwegian consumer goods giant Orkla ASA (OBX:ORK) reported accelerating organic growth in its Q2 2025 results presentation on July 14, showing improved momentum after a slower first quarter. The company, which operates across multiple consumer segments from foods to personal care, posted 3.8% organic growth for Q2, a significant improvement from the 1.2% reported in Q1 2025.

The results come as Orkla continues to implement its portfolio restructuring strategy, divesting non-core assets while focusing on strengthening its core business segments. This strategic approach appears to be yielding results, with the stock having delivered a 44% return over the past year according to previous financial reports.

Quarterly Performance Highlights

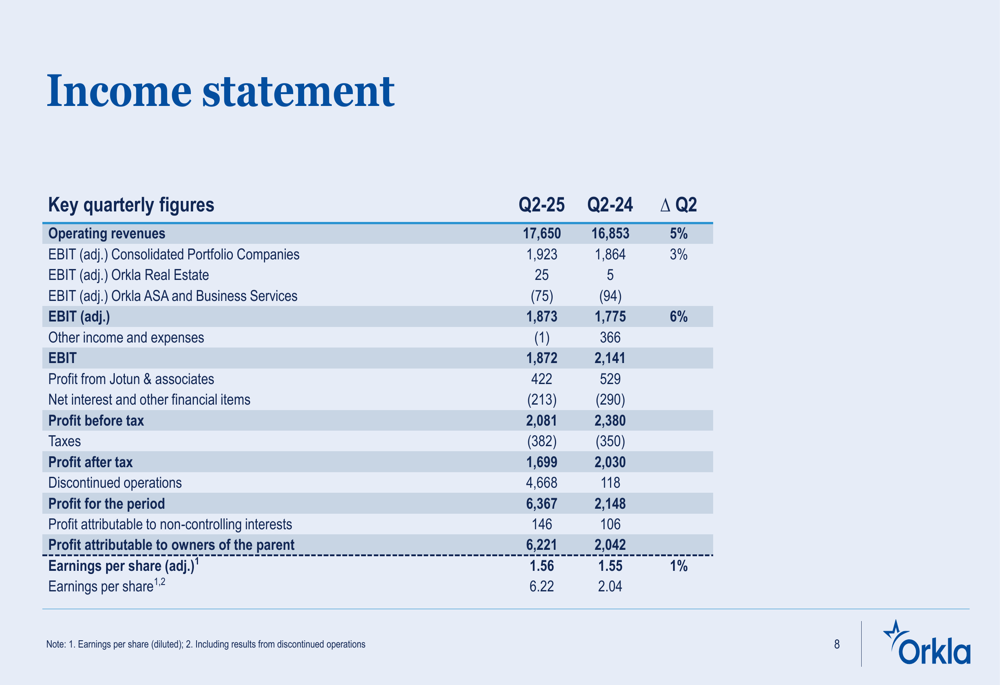

Orkla reported Q2 2025 operating revenues of NOK 17,650 million, representing a 5% increase compared to NOK 16,853 million in Q2 2024. Underlying EBIT (adjusted) grew by 2.5%, while adjusted earnings per share reached NOK 1.56, a modest 0.6% increase year-over-year.

As shown in the following key highlights slide, the company’s performance metrics indicate stable growth despite challenging market conditions:

The company’s profit for the period showed a dramatic increase to NOK 6,367 million compared to NOK 2,148 million in the same period last year, though this was significantly impacted by one-off items. When examining the detailed income statement, we can see the comprehensive breakdown of financial performance:

Orkla’s EBIT margin has shown steady improvement over recent quarters, reaching 10.3% on a rolling 12-month basis by Q2 2025. This represents a continued recovery from the 9.0% seen in Q1 2023, suggesting that the company’s operational efficiency initiatives are bearing fruit.

The following chart illustrates Orkla’s organic growth trend, showing how the current 3.8% growth compares to historical performance:

Segment Performance Analysis

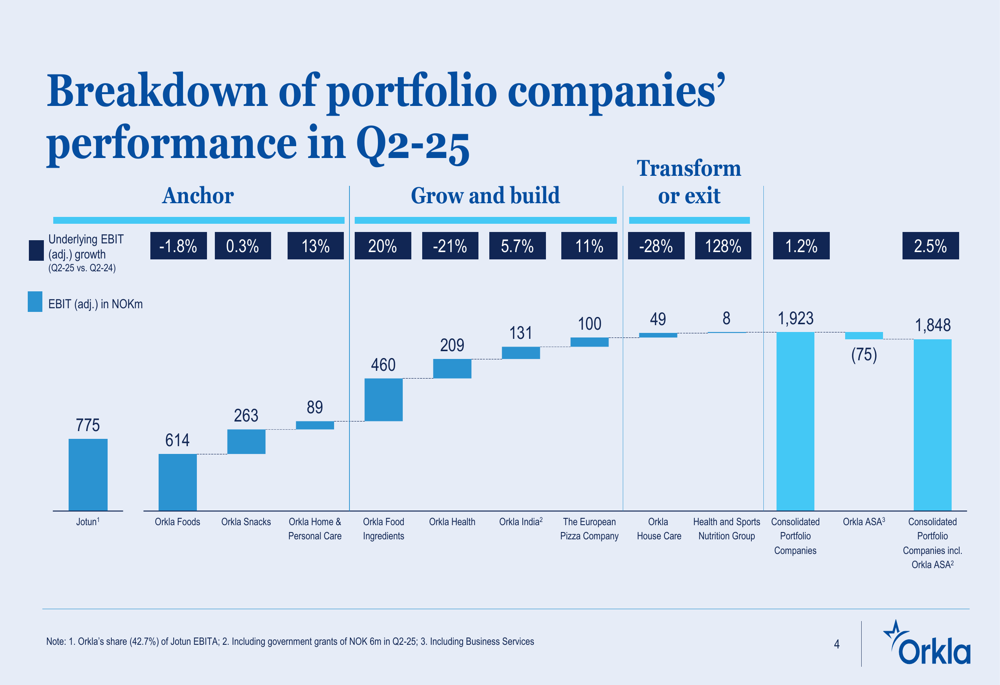

Orkla’s portfolio companies showed mixed performance in Q2 2025, with significant variations across segments. The company categorizes its businesses into "Anchor," "Grow and Build," and "Transform or Exit" segments, with each showing different growth trajectories.

The following breakdown illustrates the performance of each portfolio company:

Among the standout performers, Orkla Home & Personal Care delivered impressive EBIT growth of 20%, driven by volume increases and effective revenue management. The segment achieved a strong ROCE of 23.6% and cash conversion of 113%, demonstrating excellent operational efficiency.

Orkla Snacks also performed well with 13% EBIT growth, successfully mitigating the impact of high cocoa costs throughout its value chain. The segment received notable recognition by being named to the TIME100 Most Influential Companies list, and plans to launch its BUBS brand in the US market in Q3.

Conversely, Orkla Food Ingredients faced challenges with a 21% decline in EBIT, despite showing organic growth. Jotun, in which Orkla holds a 42.7% stake, saw a slight EBIT decline of 1.8% but maintained a strong ROCE of 32.2%.

Strategic Initiatives & Portfolio Restructuring

Orkla continues to execute on its strategic restructuring plan, reporting progress on several key initiatives in the first half of 2025. These include the sale of its Hydro Power portfolio and Pierre Robert Group, as well as filing a Draft Red Herring Prospectus with SEBI for Orkla India, suggesting a potential IPO or market listing.

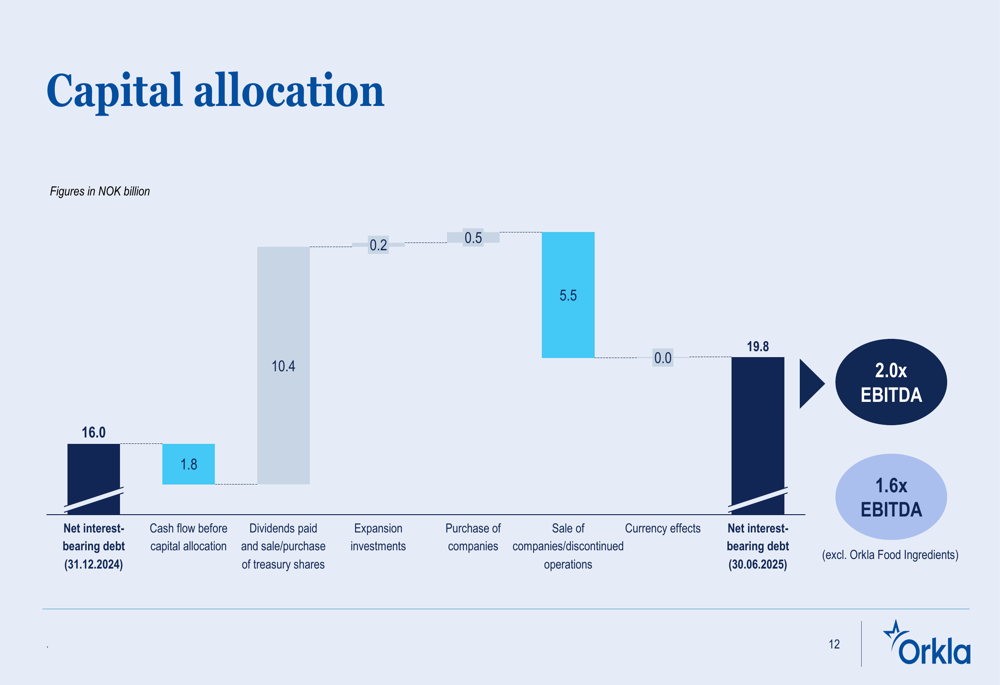

The company’s capital allocation strategy is clearly illustrated in the following chart, showing how Orkla has managed its debt position while balancing investments, divestments, and shareholder returns:

Orkla’s strategic approach is guided by three core commitments, as outlined in their presentation:

The company’s focus on driving organic value while reducing portfolio complexity appears to be yielding results, with improved organic growth in Q2 despite varied segment performance. The continued execution of value-adding structural transactions, such as the divestments mentioned above, demonstrates Orkla’s commitment to optimizing its business portfolio.

Forward-Looking Statements

Looking ahead, Orkla has maintained its financial targets for 2023-2026, aiming for 8-10% CAGR in underlying EBIT growth, an EBIT margin of 10.5-11% by 2026, and a Return on Capital Employed (ROCE) of 13% by 2026.

The company faces both opportunities and challenges across its portfolio. Jotun maintains a positive outlook despite increased global economic uncertainty, while Orkla Snacks is positioned for potential growth with its planned US market entry. However, segments like Orkla Health face headwinds, with volume/mix declines in most geographies and categories.

Orkla’s cash flow from operations showed some weakness, declining to NOK 2.4 billion for YTD-25 compared to NOK 2.8 billion in YTD-24. This aligns with trends seen in Q1 and suggests that while revenue growth has accelerated, cash generation remains a challenge that management will need to address.

The company’s next quarterly results are scheduled for October 29, 2025, which will provide further insight into whether the accelerating organic growth trend continues and how effectively Orkla is executing its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.