S&P 500 cuts losses as Nvidia climbs ahead of results

Introduction & Market Context

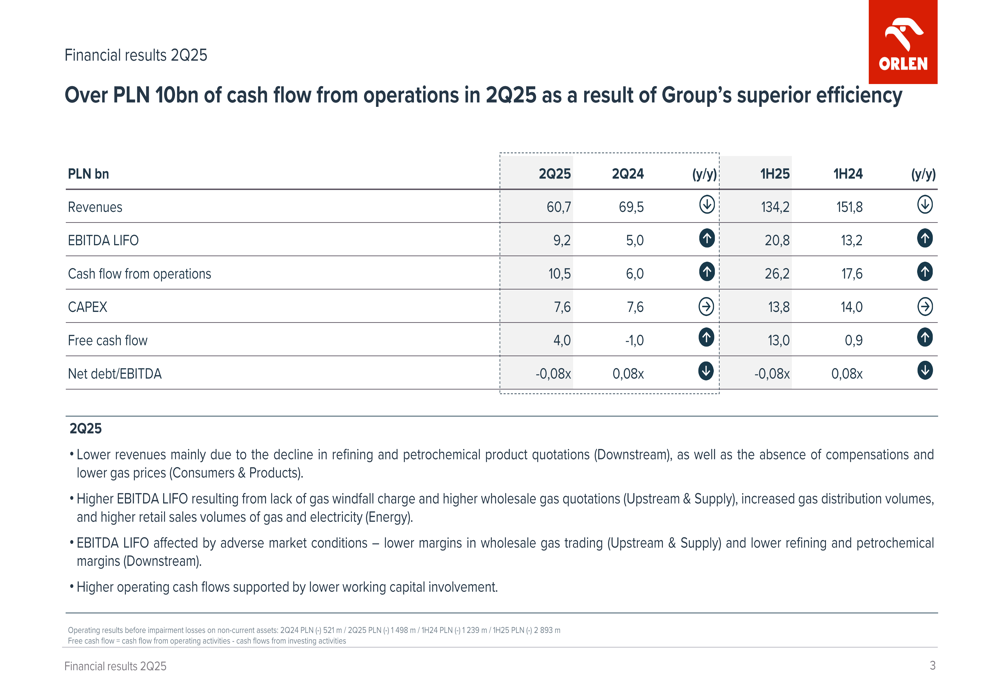

ORLEN Group presented its second quarter 2025 financial results on August 21, 2025, revealing a significant improvement in profitability despite challenging market conditions. The Polish energy giant reported an 85% year-over-year increase in EBITDA LIFO to 9.2 billion PLN, even as revenues declined to 60.7 billion PLN.

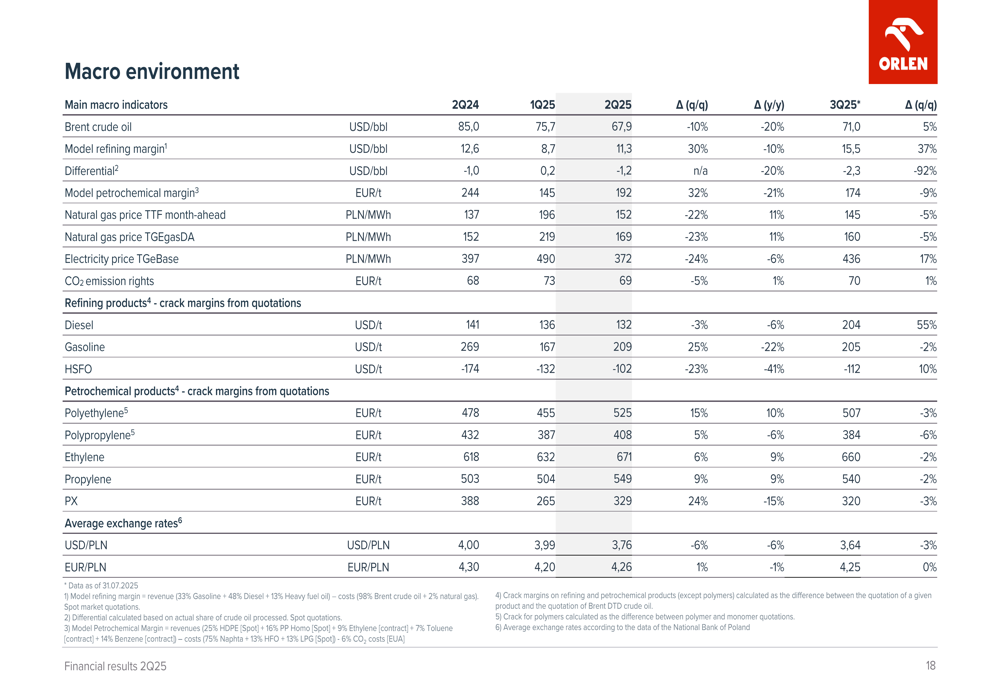

The impressive performance came against a backdrop of lower refining and petrochemical quotations, with Brent crude oil prices dropping 20% year-over-year to $67.9 per barrel. The company also faced headwinds from a 10% decrease in refining margins (to 11.3 USD/bbl) and a 21% decline in petrochemical margins (to 192 EUR/t).

Quarterly Performance Highlights

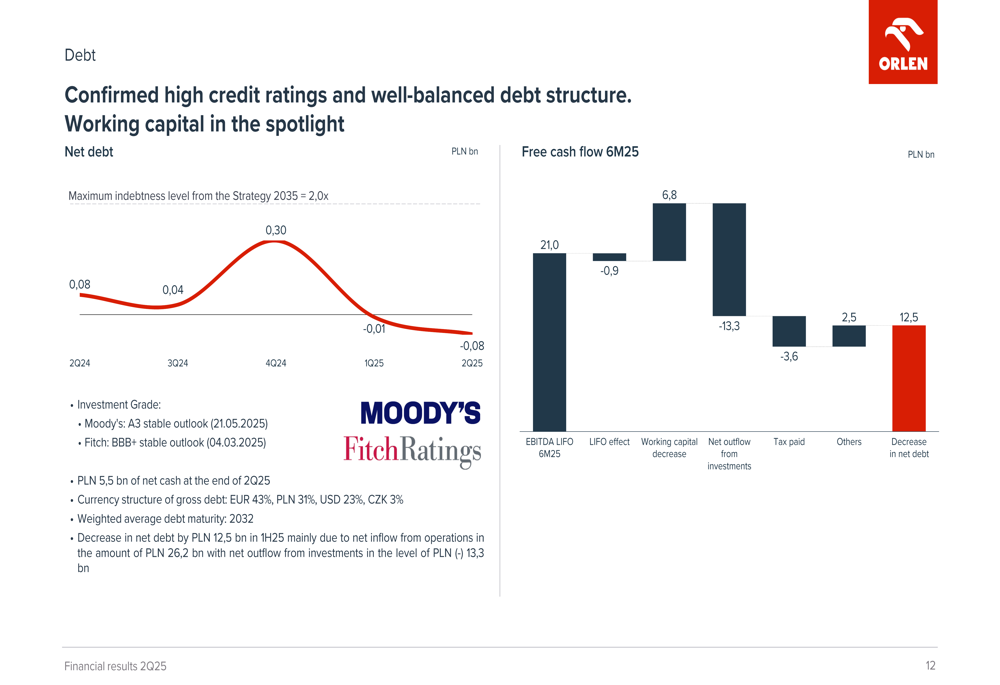

ORLEN’s Q2 2025 results demonstrated the company’s operational resilience and financial strength. Despite the revenue decline, cash flow from operations increased significantly to 10.5 billion PLN, while free cash flow rose to 4.0 billion PLN compared to the same period last year.

The company’s net debt-to-EBITDA ratio improved to -0.08x, indicating ORLEN has transitioned to a net cash position. This financial transformation reflects the company’s strong cash generation capabilities and disciplined capital allocation.

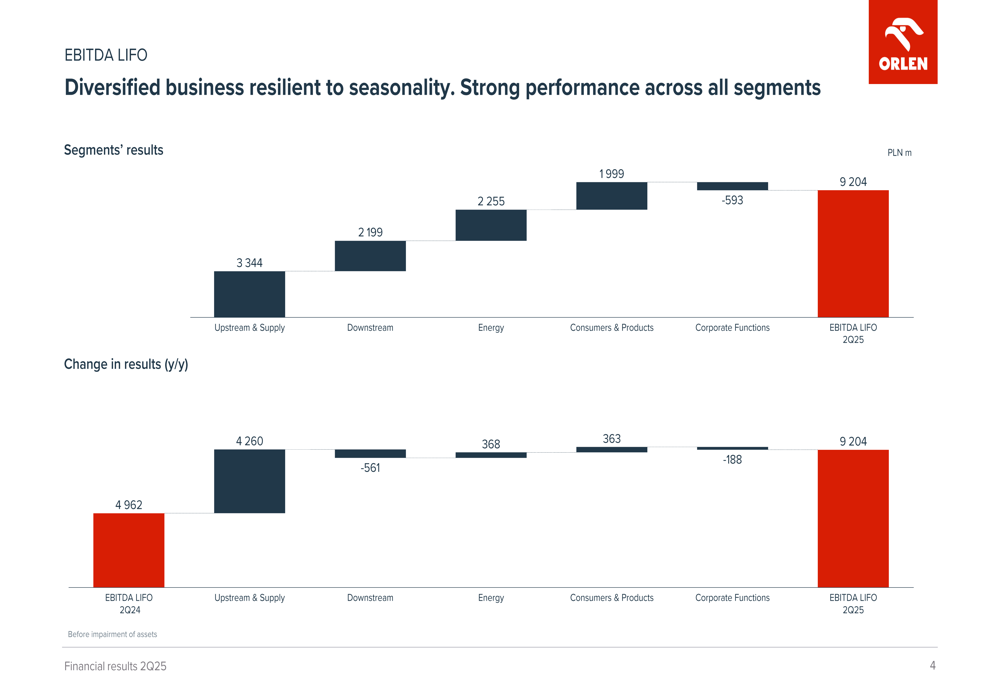

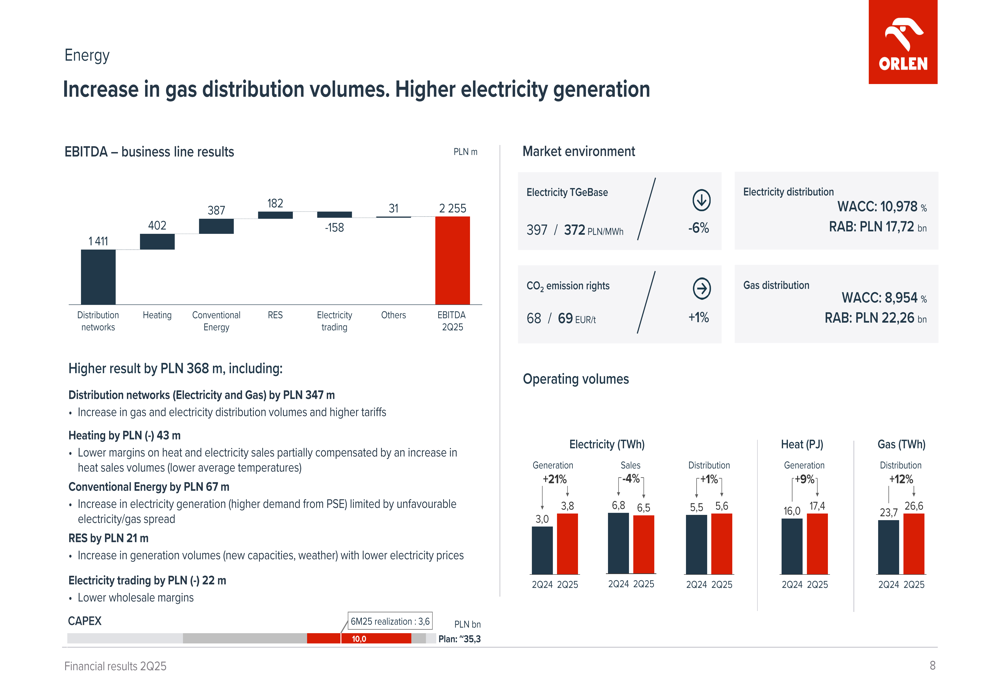

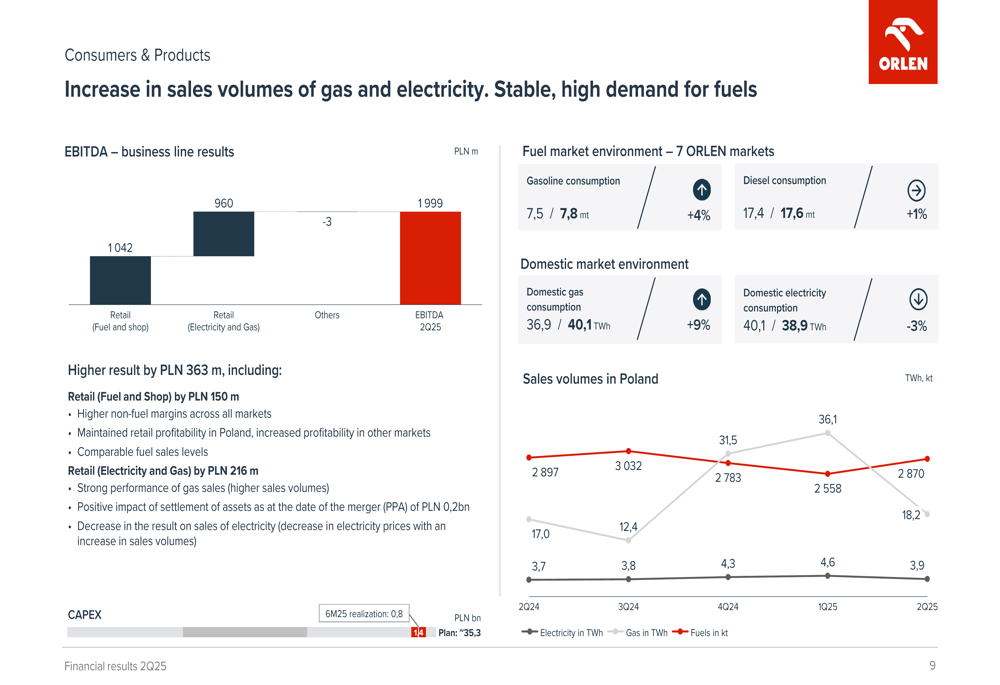

The EBITDA LIFO improvement was driven primarily by two segments: Upstream & Supply, which contributed 3,344 million PLN (up from 1,653 million PLN in Q2 2024), and Consumers & Products, which delivered 1,999 million PLN (a substantial increase from 363 million PLN). The Energy segment also performed well with 2,255 million PLN, while Downstream maintained its contribution at 2,199 million PLN.

Segment Analysis

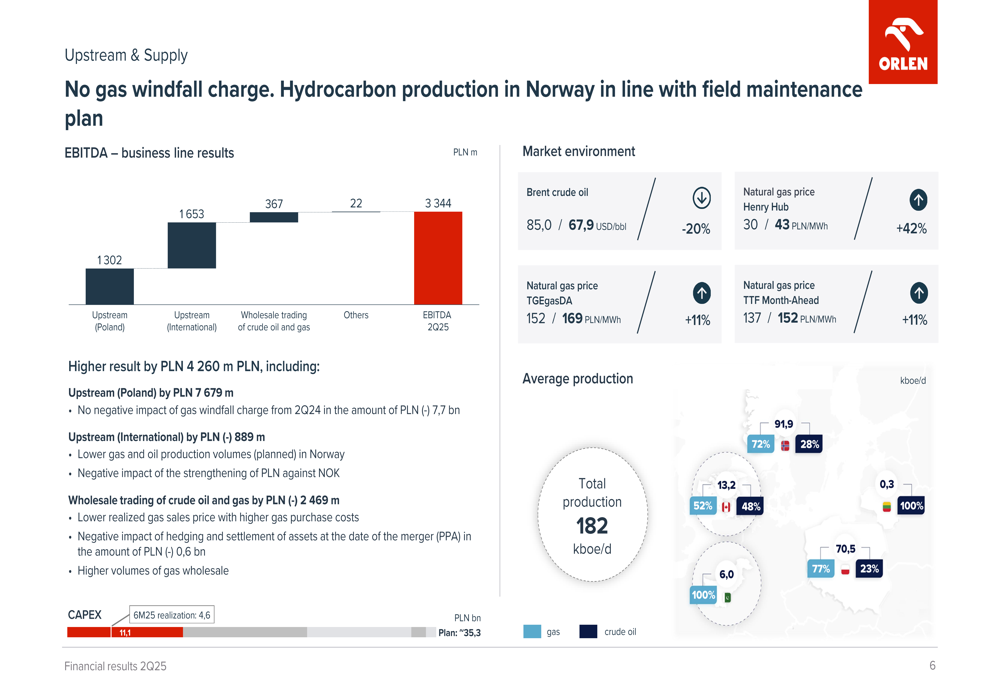

The Upstream & Supply segment’s performance was particularly strong, with results improving by 4,260 million PLN year-over-year. This improvement came despite a 16% decline in crude oil production and an 11% decrease in natural gas production. A key factor was the absence of the gas windfall charge that had negatively impacted the previous year’s results.

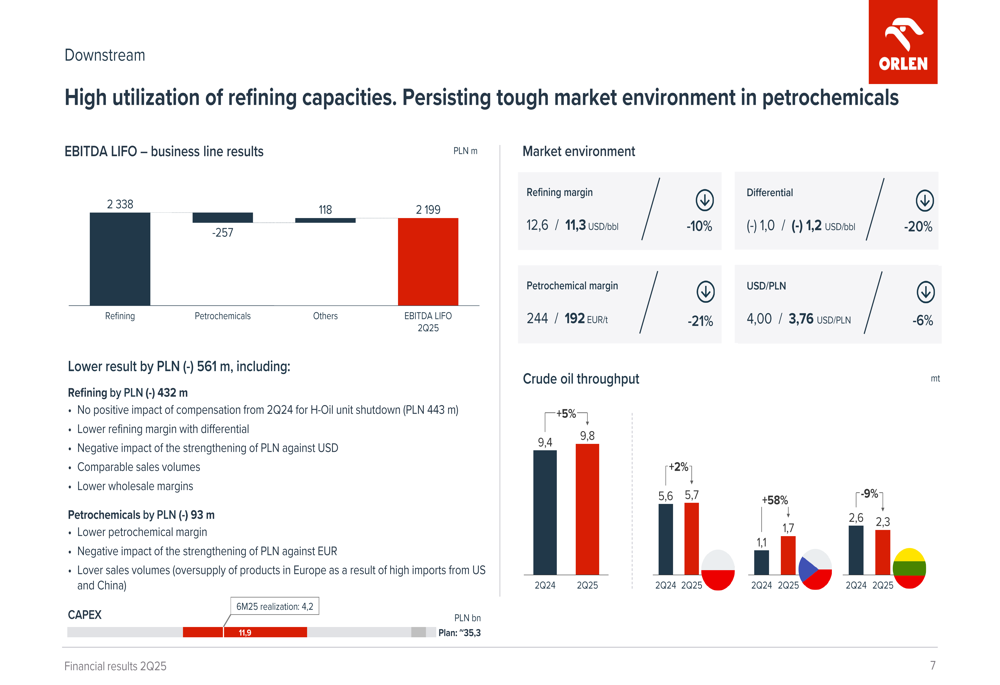

In contrast, the Downstream segment faced challenges, with results declining by 561 million PLN compared to Q2 2024. This was primarily due to lower refining and petrochemical margins, despite a 5% increase in crude oil throughput to 9.4 million tons.

The Energy segment delivered improved results, up by 368 million PLN year-over-year, despite a 6% decrease in electricity prices. The segment benefited from a 42% increase in renewable energy generation and a 27% rise in overall electricity generation.

The Consumers & Products segment showed remarkable growth, with results increasing by 363 million PLN. This improvement came despite relatively stable retail fuel sales volumes, suggesting enhanced margins and operational efficiencies.

Financial Position & CAPEX

ORLEN reported a strong financial position at the end of Q2 2025, with 5.5 billion PLN of net cash. The company’s solid financial standing is further validated by confirmed high credit ratings from Moody’s (A3 stable outlook) and Fitch (BBB+ stable outlook).

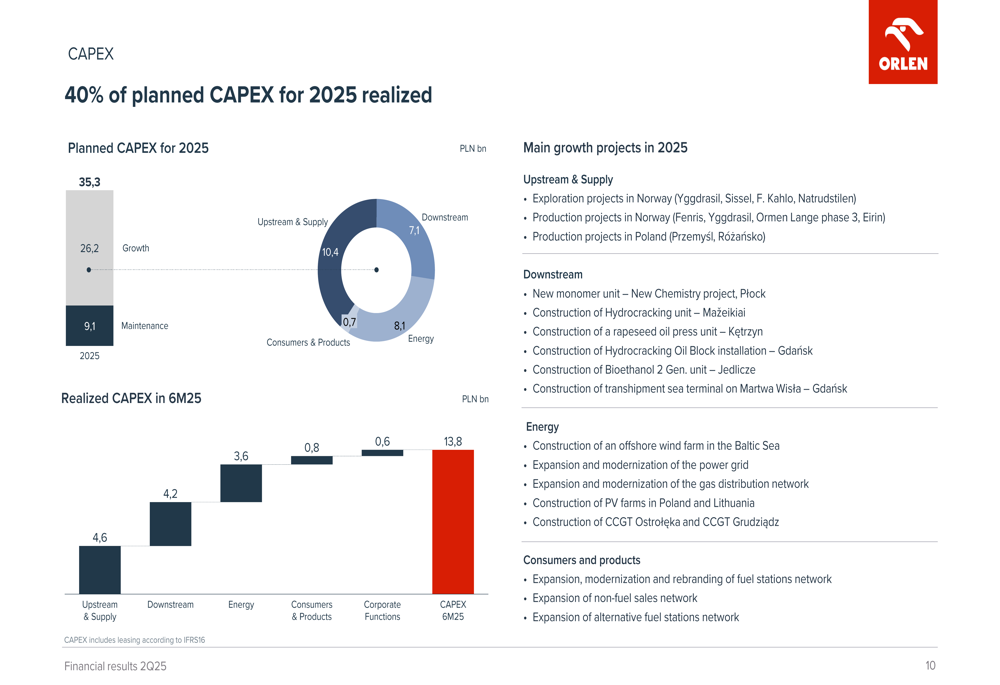

The company has maintained an ambitious capital expenditure program, with 13.8 billion PLN spent in the first half of 2025, representing 40% of the planned 35.3 billion PLN annual CAPEX budget. These investments are strategically allocated across segments to support ORLEN’s long-term growth objectives.

ORLEN has also made significant progress in diversifying its financing sources, completing a USD 1.25 billion bond issuance and a EUR 600 million green Eurobond issuance in the first half of 2025. Additionally, the company secured PLN 3.5 billion in agreements with the European Investment Bank and PLN 1.7 billion in funding for hydrogen projects from the National Power Reform Fund.

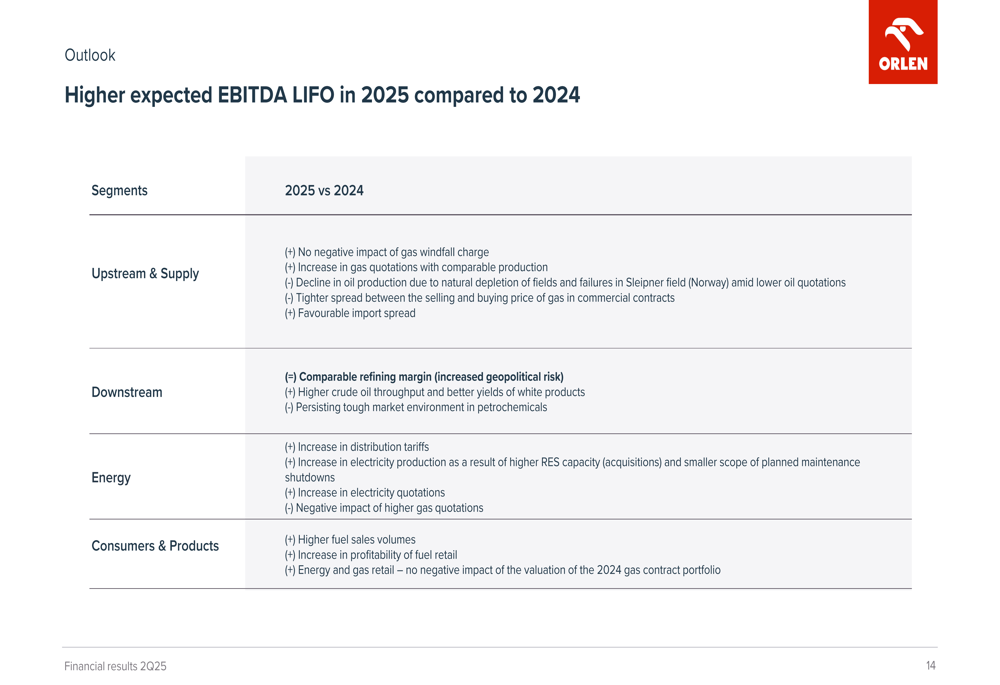

Outlook & Forward-Looking Statements

Looking ahead, ORLEN expects mixed conditions across its business segments for the remainder of 2025. The Upstream & Supply segment is anticipated to benefit from the absence of the gas windfall charge, though this will be partially offset by declining oil production.

The Downstream segment faces a challenging environment, with comparable refining margins but persistent difficulties in petrochemicals. Meanwhile, the Energy segment is expected to benefit from higher regulated revenues and improved availability of generation assets.

The company’s macro outlook suggests some stabilization in key indicators, with Brent crude oil prices projected at $71.0 per barrel for Q3 2025, up from Q2’s $67.9. Model refining margins are expected to improve significantly to $15.5 per barrel, potentially boosting the Downstream segment’s performance in the coming quarter.

Overall, ORLEN’s Q2 2025 results demonstrate the company’s ability to generate strong financial performance despite challenging market conditions. The transition to a net cash position and continued strategic investments position the company well for sustainable growth in an evolving energy landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.