Joby Aviation closes $591 million stock offering with full underwriter option

Ormat Technologies Inc (NYSE:ORA) reported mixed first-quarter results with record quarterly EBITDA driven by explosive growth in its energy storage business, according to the company’s Q1 2025 earnings presentation. The renewable energy company’s stock traded up 1.45% at $72.31 following the May 8 presentation.

Quarterly Performance Highlights

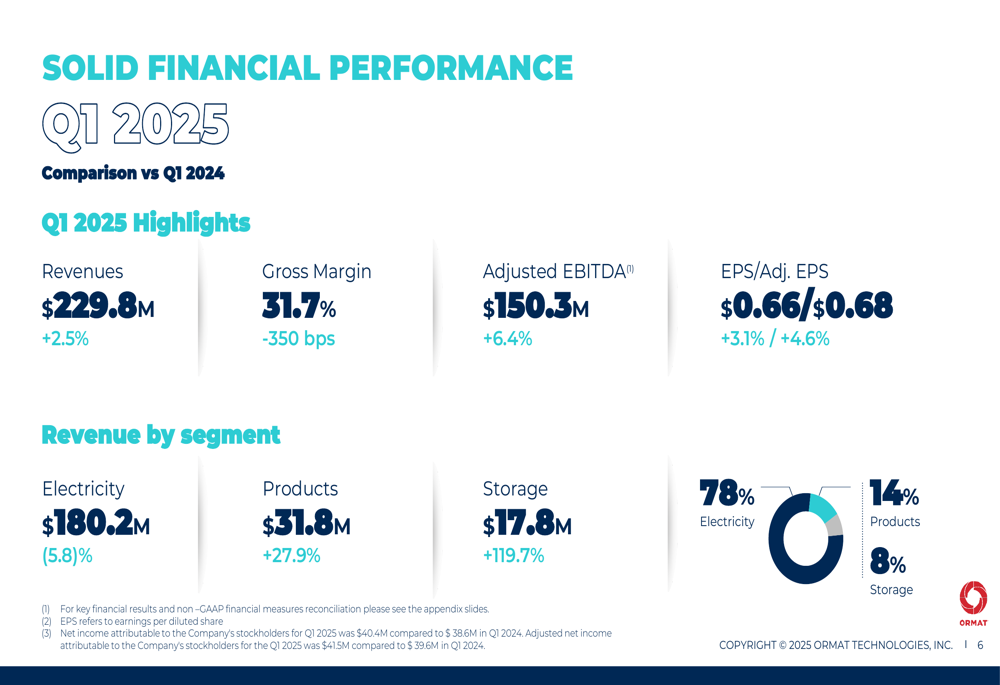

Ormat delivered solid financial results for Q1 2025, with total revenues increasing by 2.5% to $229.8 million compared to the same period last year. The company reported adjusted EBITDA of $150.3 million, representing a 6.4% year-over-year increase, while earnings per share rose 3.1% to $0.66.

"Strong financial results were driven by improved performance of the Storage and Product segments, which offset curtailments in the Electricity segment," the company noted in its presentation.

The company’s performance varied significantly across its three business segments. While the Electricity segment saw a 5.8% revenue decline to $180.2 million, the Products segment grew 27.9% to $31.8 million, and the Storage segment surged by 119.7% to $17.8 million.

As shown in the following revenue breakdown by segment:

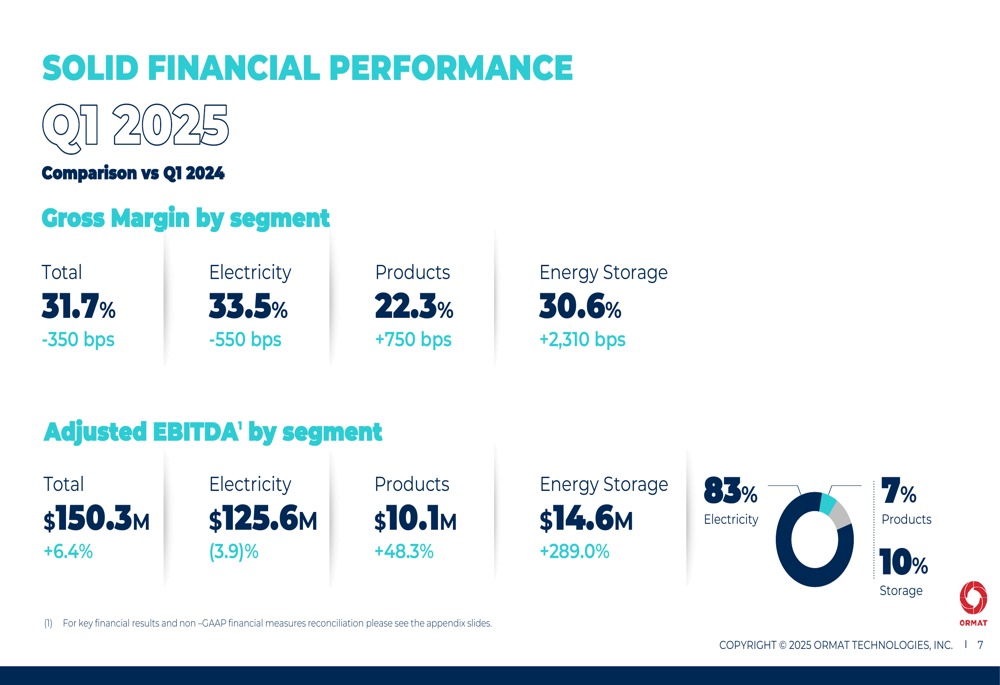

Gross margins showed similar divergence, with the overall gross margin declining 350 basis points to 31.7%. The Electricity segment’s margin fell 550 basis points to 33.5%, while Products improved by 750 basis points to 22.3%. Most notably, the Energy Storage segment’s gross margin jumped by an impressive 2,310 basis points to 30.6%.

The segment-specific adjusted EBITDA performance further illustrates these trends:

Strategic Initiatives

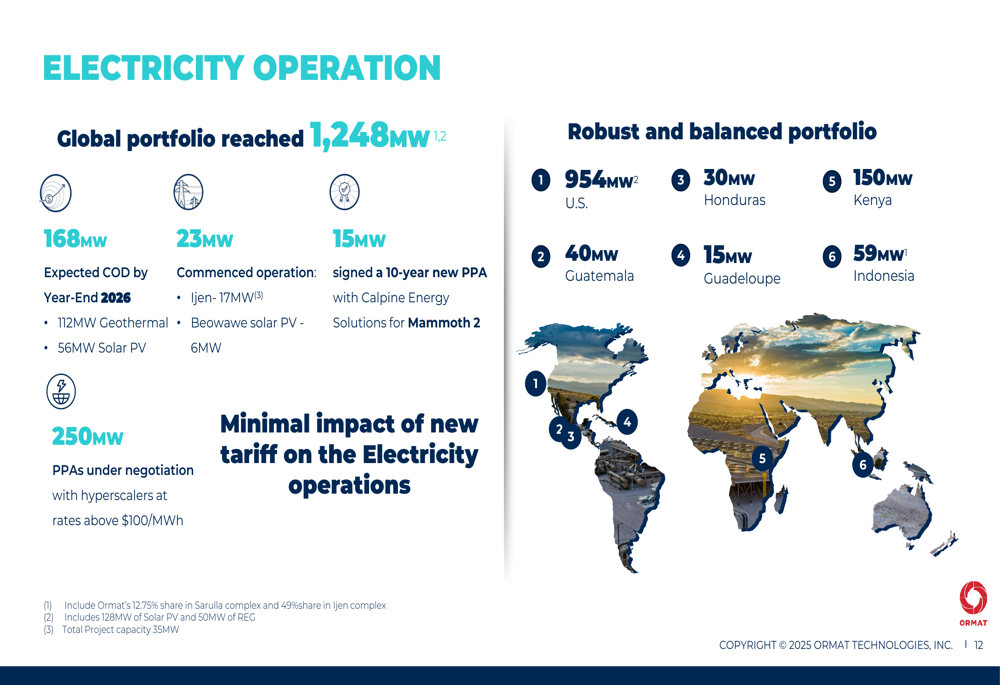

Ormat continued to expand its operational footprint, adding 23MW of capacity during the quarter. The company also announced the acquisition of the 20MW Blue Mountain geothermal power plant from Cyrq Energy for $88 million, with closing expected by the end of June 2025.

"We signed an agreement to acquire 20MW Blue Mountain geothermal power plant from Cyrq Energy for $88M. The power plant has a PPA with NV Energy until 2029," the company stated. Ormat plans to add 3.5MW to the plant by 2027 and potentially develop a 13MW solar facility at the site, subject to PPA approval.

The company’s global electricity operations now span multiple continents with a total capacity of 1,248MW:

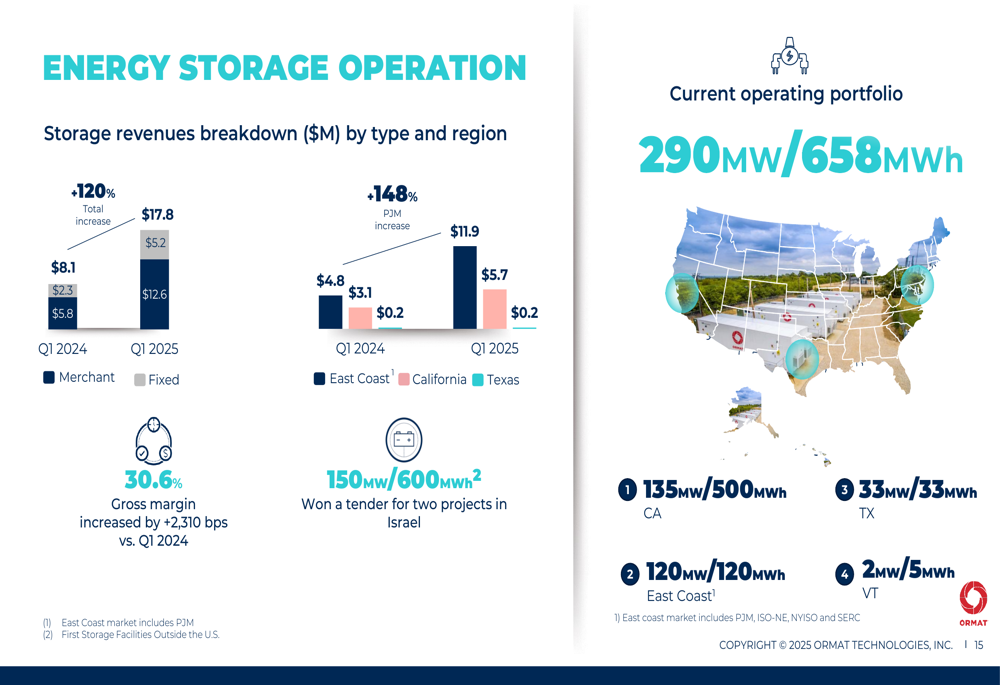

The energy storage business has emerged as a significant growth driver for Ormat. The company currently operates 290MW/658MWh of storage capacity, primarily in California, the East Coast, and Texas. Storage revenues more than doubled year-over-year, with particularly strong growth in PJM markets.

The following chart illustrates the company’s storage operations and revenue growth:

Ormat’s product segment also showed strong momentum, with backlog reaching approximately $314 million, representing a 142% increase compared to Q1 2024. New Zealand accounts for 78% of the current backlog.

Forward-Looking Statements

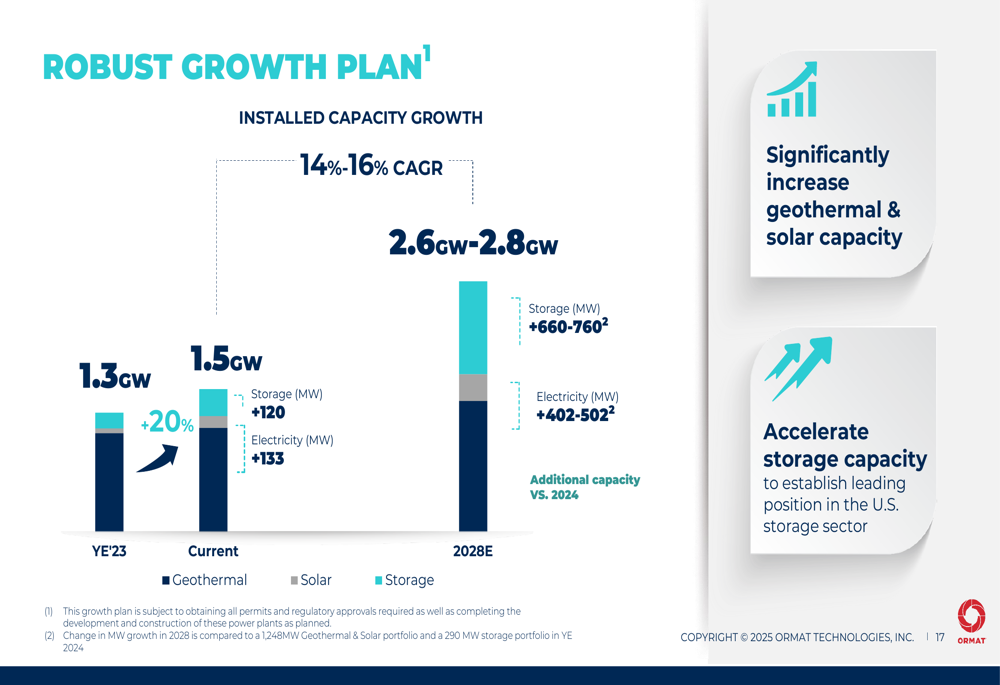

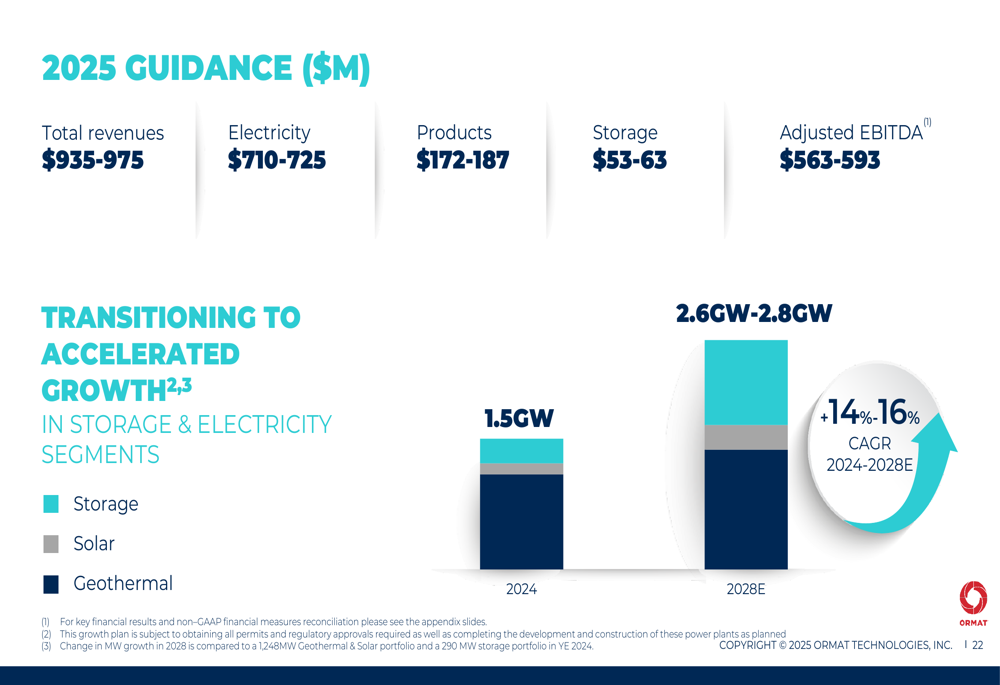

Ormat outlined an ambitious growth trajectory, targeting 14-16% compound annual growth rate (CAGR) from 2024 to 2028, which would expand its total capacity to 2.6-2.8GW by 2028.

The company’s growth plan is visualized in the following chart:

For the full year 2025, Ormat provided the following financial guidance:

The company has a robust development pipeline to support this growth, with 116MW of geothermal projects under development across eight projects globally. Additionally, Ormat is developing 385MW/1,300MWh of energy storage projects across six locations, including two high-voltage projects in Israel totaling 150MW/600MWh.

"We have secured safe harbor for all geothermal projects in the US until 2028 and for all storage projects until 2026 and in some cases beyond," the company emphasized, highlighting the benefits of the Inflation Reduction Act (IRA).

The IRA continues to provide significant financial benefits, with $17.6 million in income attributable to the sale of tax benefits in Q1 2025 and $13.9 million in ITC (NSE:ITC) benefits recorded under income tax. For the full year 2025, Ormat expects approximately $160 million in cash proceeds from tax benefits.

Competitive Industry Position

Ormat is strategically positioning itself to capitalize on growing demand for renewable energy, particularly in the rapidly expanding energy storage market. The company has an impressive storage pipeline of approximately 3.2GW/12.0GWh in the United States, with projects spread across California (1,132MW), the East Coast (595MW), WECC (580MW), Texas (480MW), and other regions (445MW).

The company noted it is negotiating power purchase agreements (PPAs) for 250MW at rates exceeding $100/MWh, primarily with hyperscalers, indicating strong demand and favorable pricing for its renewable energy.

Regarding recent regulatory changes, Ormat stated: "Limited short-term exposure to recent Reciprocal Import Tariffs in all segments. May have long-term slowdown in the U.S. storage development."

From a financial perspective, Ormat maintains a solid capital position with total liquidity of $690.6 million to support its accelerated growth plans. The company’s net debt to adjusted EBITDA ratio stands at 4.2x, with a weighted average interest rate on its debt portfolio of 4.79%.

As the renewable energy sector continues to expand, Ormat appears well-positioned to leverage its diversified business model across electricity generation, products, and energy storage to drive long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.