Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

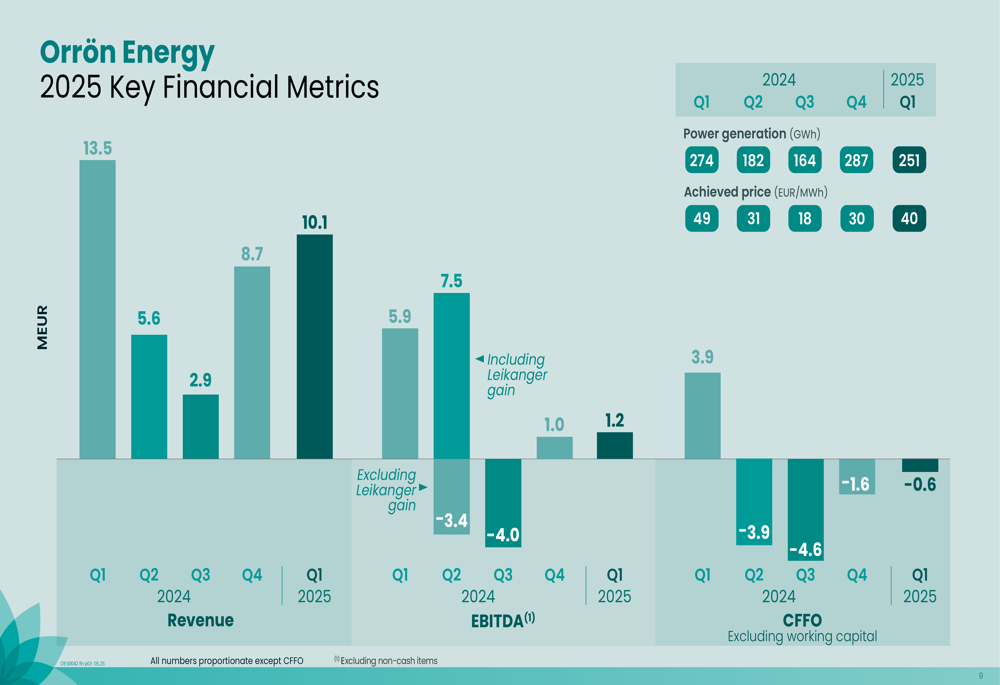

Orrön Energy AB (STO:ORRON) presented its first quarter 2025 results on May 6, showing a return to positive EBITDA after two consecutive negative quarters in the second half of 2024. Despite this improvement, investors appeared cautious, with the stock falling 5.81% to 4.41 SEK following the presentation, continuing to trade near its 52-week low of 3.87 SEK.

The renewable energy company reported power generation of 251 GWh for the quarter, generating revenue of 10.1 MEUR and EBITDA of 1.2 MEUR. While these results represent an improvement from the latter half of 2024, they remain significantly below the company’s performance in Q1 2024, when it achieved EBITDA of 7.5 MEUR.

Quarterly Performance Highlights

Orrön Energy’s Q1 2025 performance showed mixed results when compared to previous periods. The company achieved an average price of 40 EUR/MWh, higher than the 18-31 EUR/MWh range seen in Q2-Q4 2024, but still below the 49 EUR/MWh achieved in Q1 2024.

As shown in the following chart of key financial metrics across recent quarters, the company has experienced significant volatility in its financial performance:

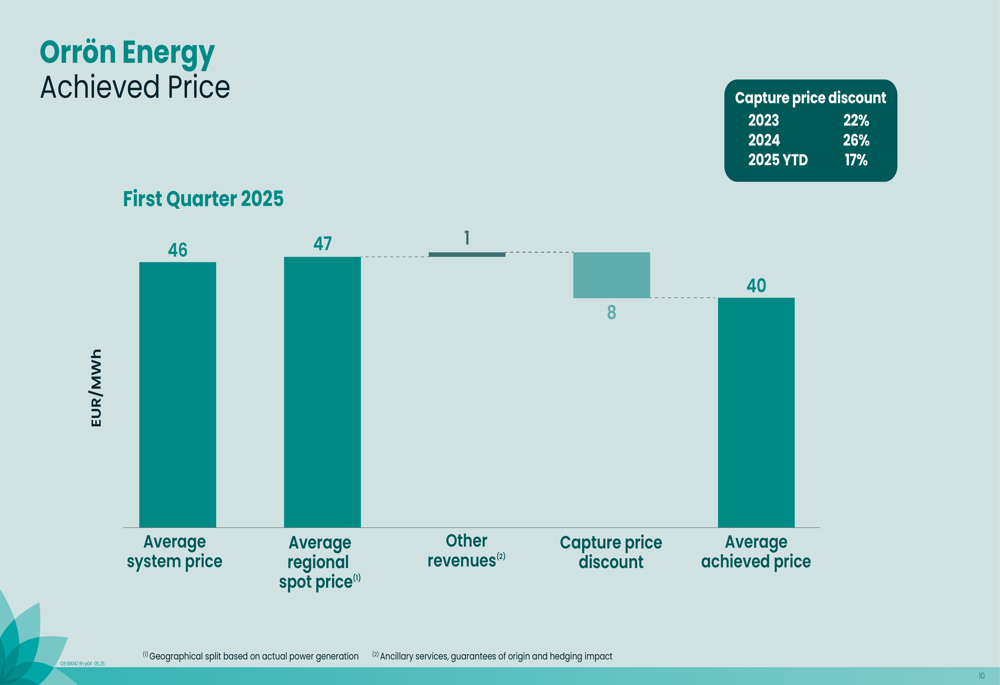

The company highlighted that it has improved its capture price discount to 17% in 2025 year-to-date, compared to 26% in 2024, indicating better revenue optimization. This improvement is partly attributed to the implementation of price-dependent bidding across 67% of the portfolio.

The breakdown of achieved price components provides insight into the company’s revenue structure:

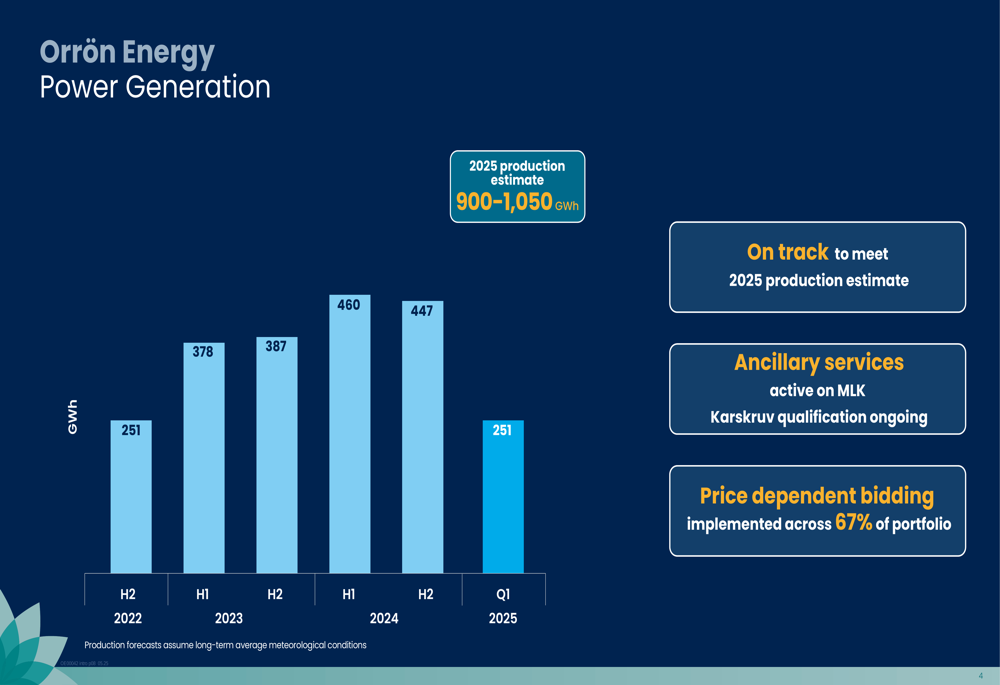

Orrön Energy confirmed it is on track to meet its 2025 production estimate of 900-1,050 GWh, with Q1 contributing 251 GWh toward this target. The company’s historical power generation shows a steady increase over recent years:

Project Pipeline & Growth Strategy

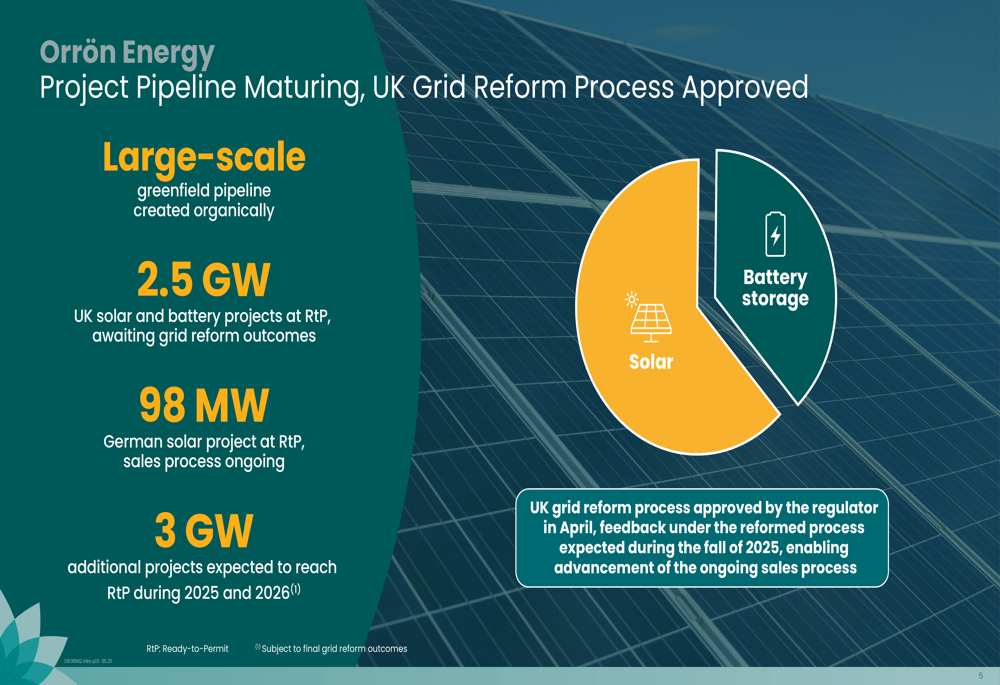

A significant focus of the presentation was Orrön Energy’s expanding project pipeline, particularly its greenfield developments across multiple markets. The company highlighted its 98 MW Agri-PV project in Germany, which has reached Ready-to-Permit status with a sales process currently underway. Commercial operations for this project are targeted for 2028.

The company’s project pipeline is illustrated in the following slide:

In the UK, Orrön Energy has 2.5 GW of solar and battery projects at Ready-to-Permit stage, awaiting the outcome of the UK grid reform process. The company noted that the reform was approved by the regulator in April, with feedback under the reformed process expected in the fall of 2025, which will enable advancement of the ongoing sales process.

Additionally, the company expects 3 GW of projects to reach Ready-to-Permit status during 2025 and 2026, further expanding its development portfolio.

Financial Analysis & Outlook

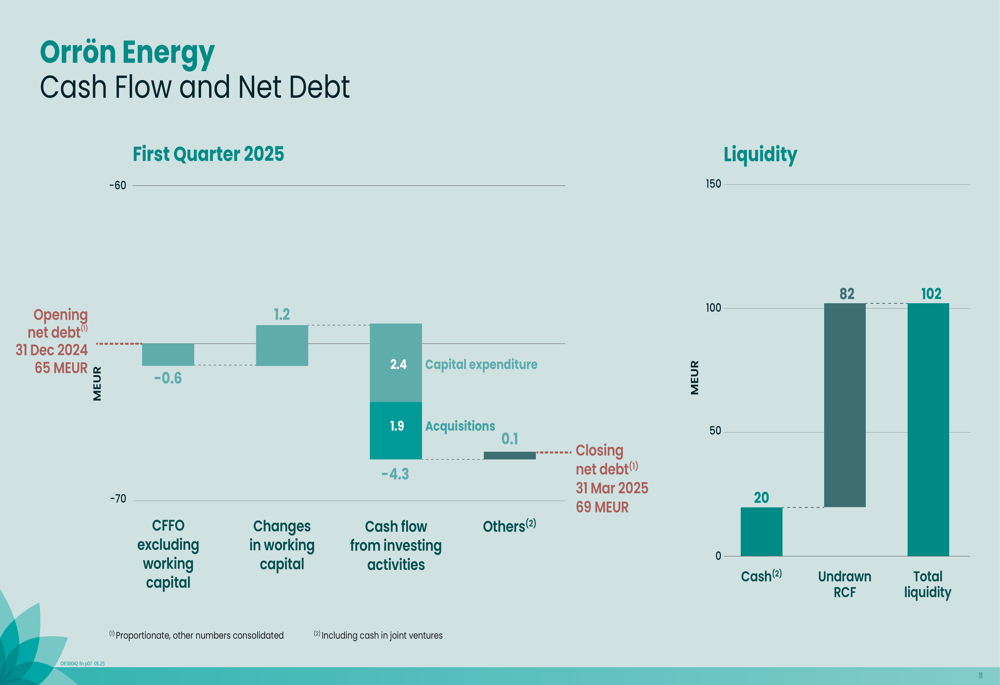

Orrön Energy reported net debt of 69 MEUR at the end of Q1 2025, a slight increase from 65 MEUR at the end of 2024. The company maintains a strong liquidity position with 100 MEUR of headroom, consisting of 20 MEUR in cash and 82 MEUR in undrawn revolving credit facilities.

The cash flow and net debt position is detailed in the following chart:

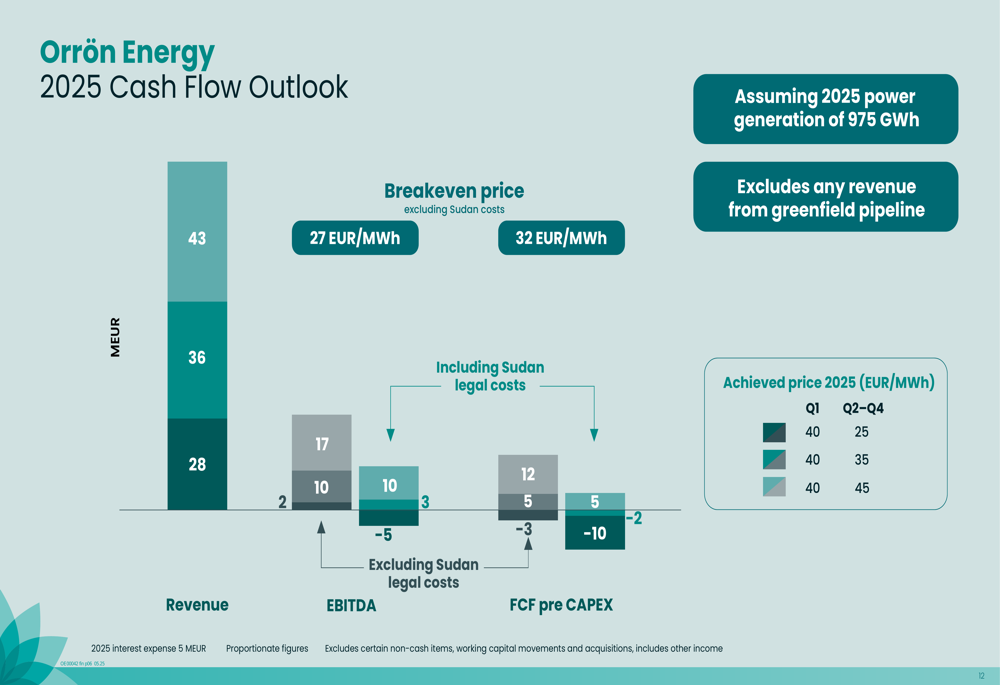

For the full year 2025, Orrön Energy provided a cash flow outlook based on various price scenarios. The company indicated a breakeven price of 27 EUR/MWh excluding Sudan legal costs, and 32 EUR/MWh including these costs. The Q1 achieved price of 40 EUR/MWh is above these breakeven levels, though the company projects varying prices for the remainder of the year.

The 2025 cash flow outlook is illustrated in this waterfall chart:

The company appears to be managing its expenses in line with guidance, with Q1 operating expenses of 5 MEUR against full-year guidance of 17 MEUR, G&A expenses of 2 MEUR against guidance of 9 MEUR, and capital expenditure of 2 MEUR against guidance of 12 MEUR.

Forward-Looking Statements

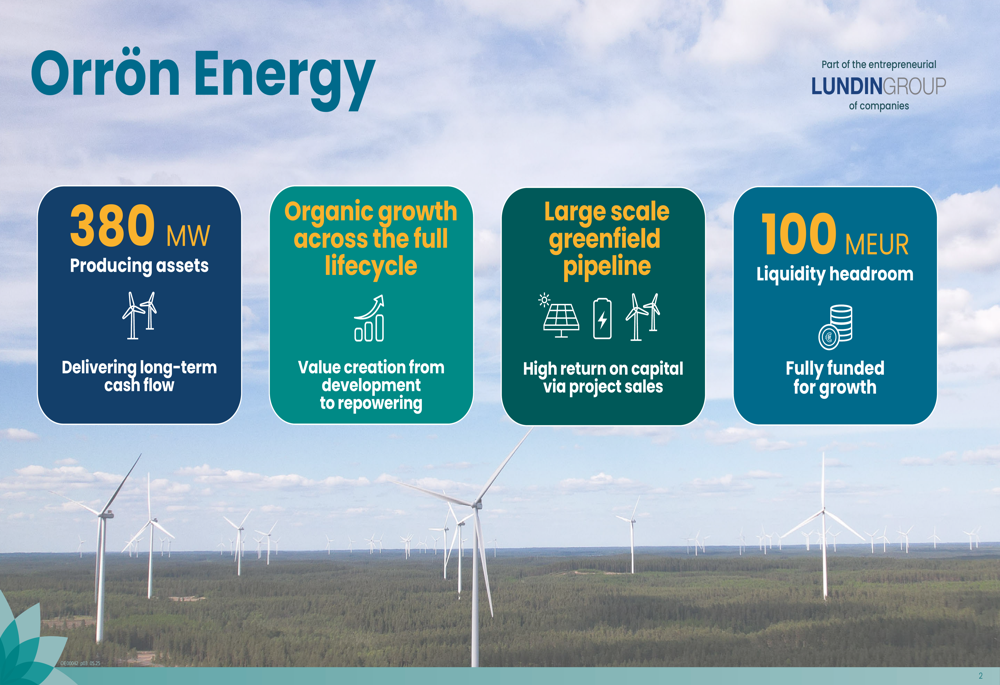

Orrön Energy emphasized its strategy of creating value through the energy transition, focusing on long-term cash flow from operating wind farms and greenfield project sales. The company highlighted its financial resilience with over 100 MEUR in liquidity headroom and organic growth platforms delivering across five countries.

As shown in the company’s strategic overview:

Despite the positive messaging, investors appear concerned about the company’s ability to deliver consistent financial performance in a challenging energy market environment. The ongoing legal costs related to Sudan (2 MEUR in Q1 against full-year guidance of 7 MEUR) continue to impact the company’s profitability.

While Orrön Energy has returned to positive EBITDA territory in Q1 2025, the significant gap compared to its Q1 2024 performance suggests ongoing challenges in the renewable energy market. The company’s focus on project development and sales may provide future value, but investors appear to be taking a cautious approach as they await more concrete evidence of sustainable financial improvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.