CME glitch; U.S. dollar on pace for weekly fall; Tokyo CPI - what’s moving markets

Introduction & Market Context

Orthofix Medical Inc. (NASDAQ:OFIX) released its third-quarter 2025 financial results on November 4, showing continued revenue growth across all business segments despite ongoing profitability challenges. The medical device company's stock traded at $16.69 in pre-market, up 3.92% from the previous close of $16.06, after initially dropping 4.7% following the earnings announcement.

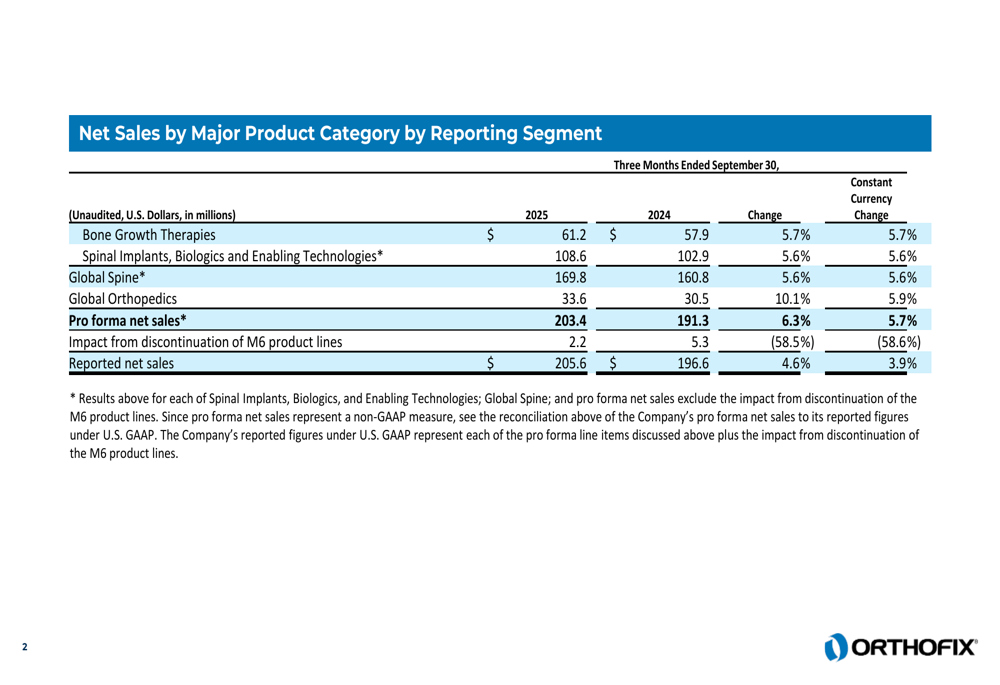

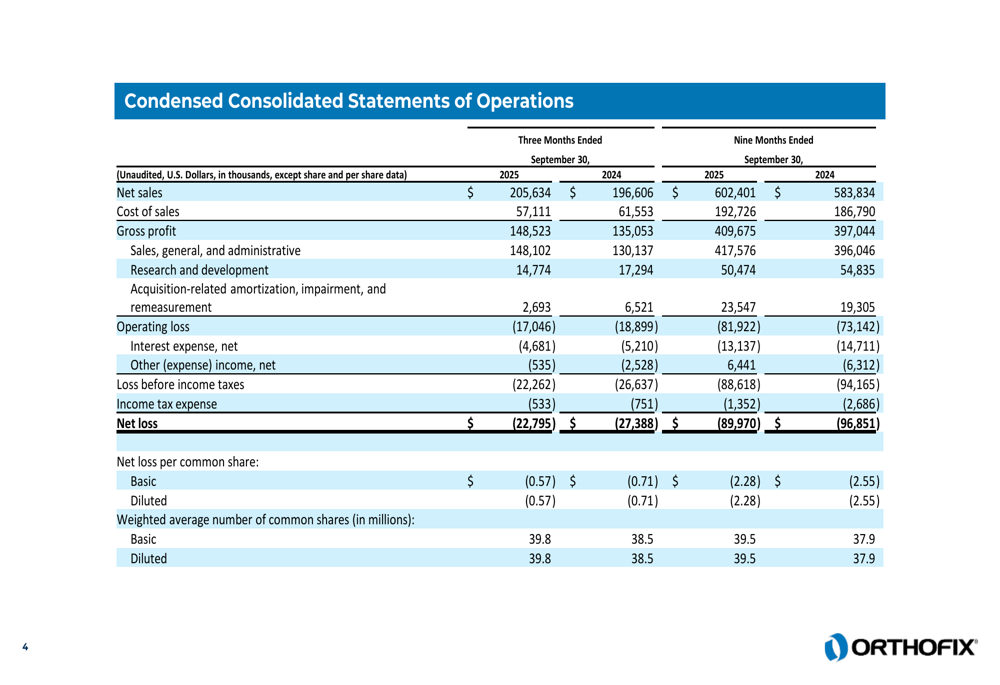

The company reported pro forma net sales of $203.4 million, representing a 6.3% increase year-over-year and exceeding analyst expectations of $200.26 million. However, Orthofix posted a net loss of $22.8 million, translating to earnings per share of -$0.57, which significantly missed the forecasted -$0.33.

Quarterly Performance Highlights

Orthofix's revenue growth was consistent across all major product categories, with particularly strong performance in Global Orthopedics, which increased by 10.1% compared to the same period last year.

As shown in the following breakdown of net sales by major product category:

The company's Global Spine segment, which includes Bone Growth Therapies and Spinal Implants, Biologics and Enabling Technologies, grew by 5.6% to $169.8 million. This growth reflects the company's strategic focus on its core product lines, excluding the impact of the discontinued M6 product lines.

CEO Massimo Calafiore noted in the earnings call, "We are well-positioned for our next phase of profitable growth," highlighting the sustained momentum in Orthofix's spine, bone growth therapies, and orthopedics businesses.

Detailed Financial Analysis

Despite the net loss, Orthofix showed improvement in several key financial metrics. The consolidated statements of operations reveal the company's progress in narrowing losses while growing revenue:

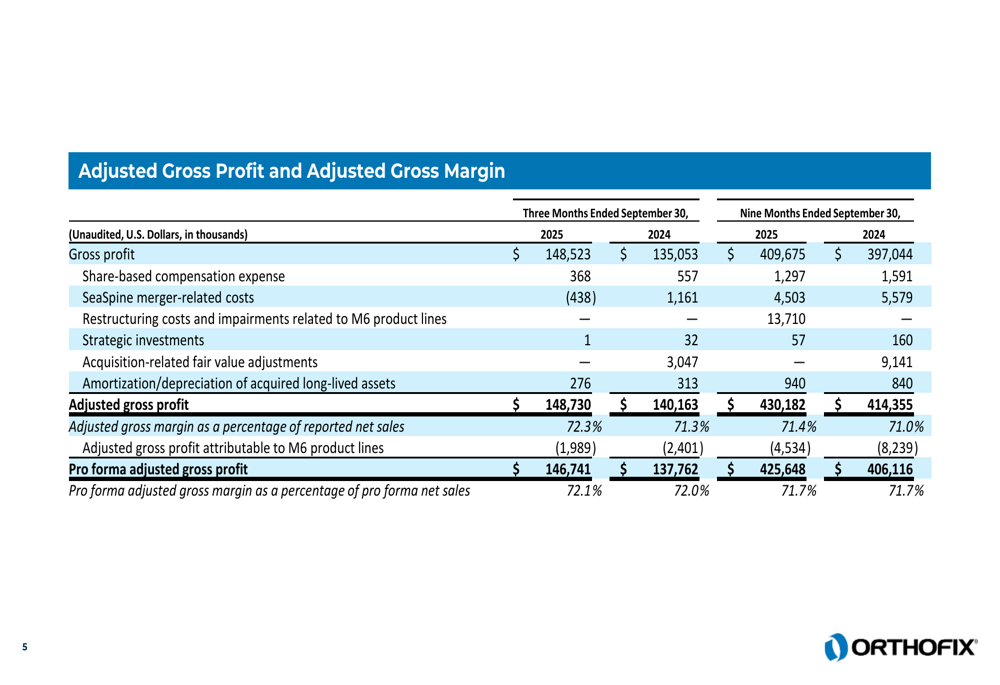

The company's adjusted gross margin improved to 72.3% in Q3 2025, up from 71.3% in the same period last year. On a pro forma basis, which excludes the impact of discontinued M6 product lines, the adjusted gross margin was 72.1%, representing an 80 basis point increase from the previous year.

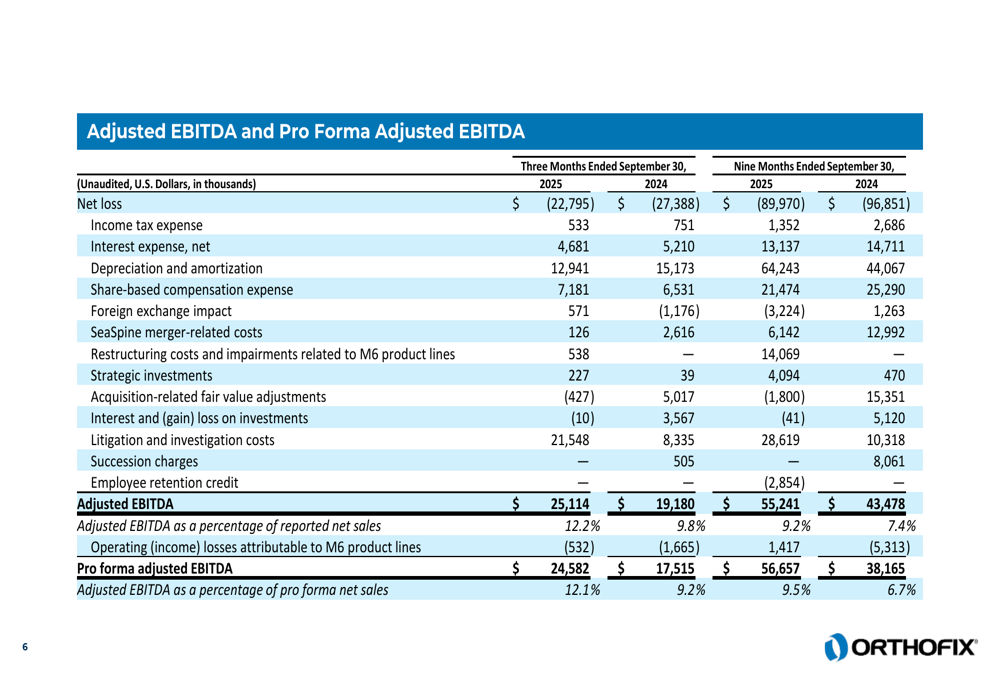

A significant bright spot in Orthofix's financial performance was the improvement in adjusted EBITDA, which increased to $25.1 million or 12.2% of reported net sales, compared to $19.2 million or 9.8% in Q3 2024. This marks the seventh consecutive quarter of EBITDA margin expansion, according to the company.

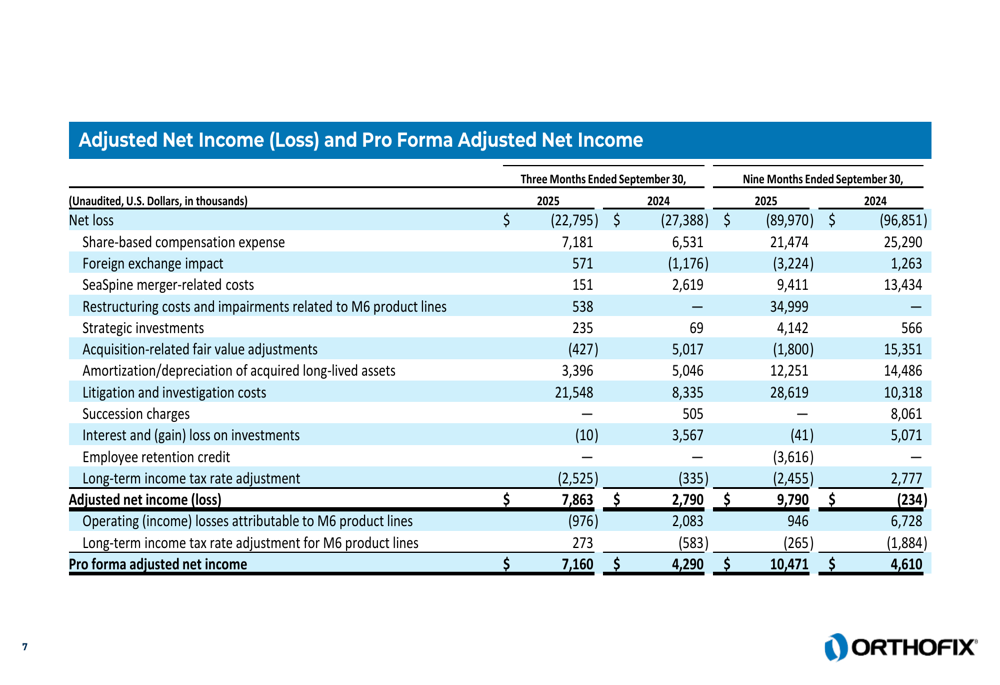

The company also reported adjusted net income of $7.9 million for Q3 2025, a substantial improvement from $2.8 million in Q3 2024, despite the GAAP net loss.

Balance Sheet and Cash Flow

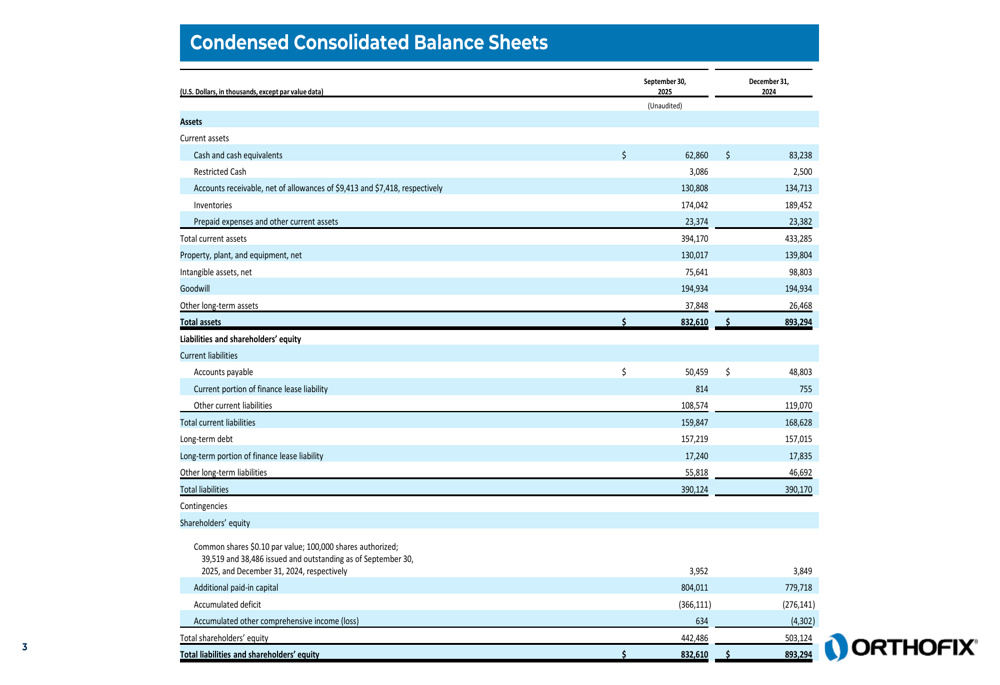

Orthofix's balance sheet shows a cash position of $62.9 million as of September 30, 2025, down from $83.2 million at the end of 2024. The company's total assets decreased to $832.6 million from $893.3 million at the end of last year.

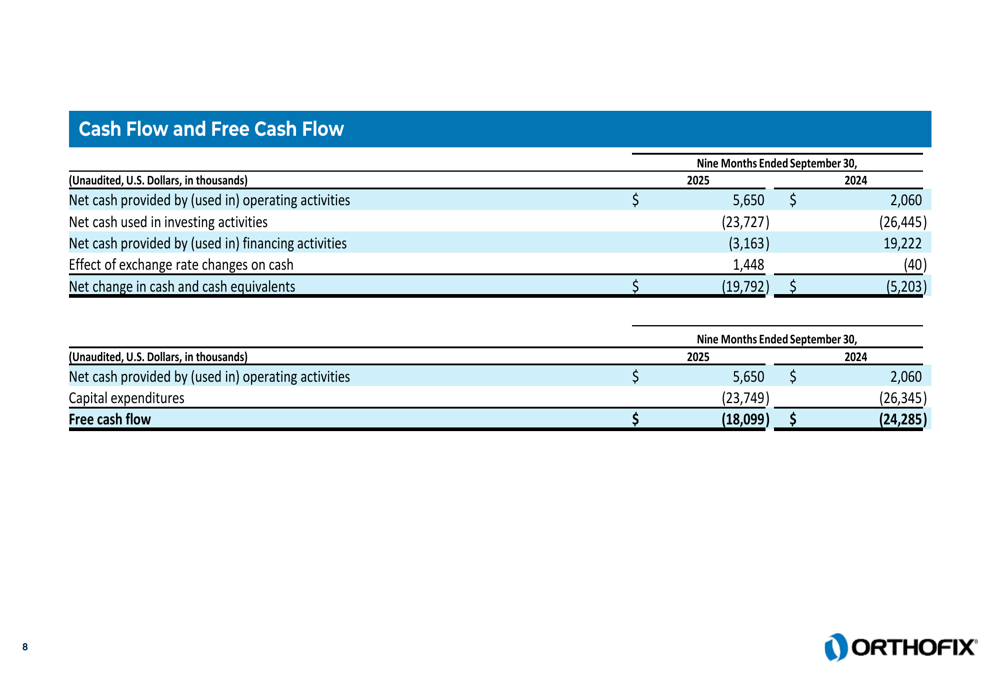

While the company reported negative free cash flow of $18.1 million for the first nine months of 2025, this represents an improvement compared to the negative $24.3 million reported for the same period in 2024. The earnings call mentioned positive free cash flow of $2.5 million for the quarter.

Strategic Initiatives

Orthofix continues to focus on enhancing commercial execution, improving gross margins, and maintaining disciplined capital allocation. The company has been strategically managing its research and development expenses, which decreased to 7.1% of reported net sales in Q3 2025 from 8.8% in Q3 2024.

The company's product portfolio expansion, including the launch of the Virada Spinal Fixation System expected in mid-2026, is anticipated to drive future growth. Orthofix is also emphasizing clinical validation efforts for products like TrueLok Elevate, as mentioned in the earnings call.

Outlook & Guidance

Orthofix has provided full-year net sales guidance of $810-$814 million and adjusted EBITDA guidance of $84-$86 million. The company expects to maintain positive free cash flow in the second half of 2025, as reiterated during the earnings call.

CFO Julie Andrews emphasized the company's commitment to delivering long-term shareholder value through continued operational improvements and strategic growth initiatives.

The company's distributor strategy focuses on consolidation and expansion in targeted geographies, which management believes will support sustainable growth in the coming quarters.

While Orthofix faces challenges in achieving consistent profitability, the improvement in adjusted EBITDA margins and the revenue growth across all segments suggest the company's strategic initiatives are gaining traction. However, investors will likely continue to monitor the gap between adjusted metrics and GAAP results, as well as the company's progress toward sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.