Index falls as earnings results weigh; pound above $1.33, Bodycote soars

Introduction & Market Context

Otovo AS (OB:OTOVO), a solar and battery marketplace operating across 10 European countries, presented its Q1 2025 results on May 6, showing signs of recovery after several challenging quarters. The company’s stock closed at 1.91 NOK on May 5, and saw a 12.35% increase ahead of the presentation, signaling positive market expectations.

The European solar market appears to be rebounding after a synchronized decline noted in previous quarters, with Otovo highlighting improved consumer outlook driven by better payback times and rising energy costs. The company operates in a strategic position at the intersection of renewable energy adoption and home electrification, with operations spanning Germany, Poland, Italy, France, Austria, Portugal, Spain, Switzerland, Sweden, and Norway.

Quarterly Performance Highlights

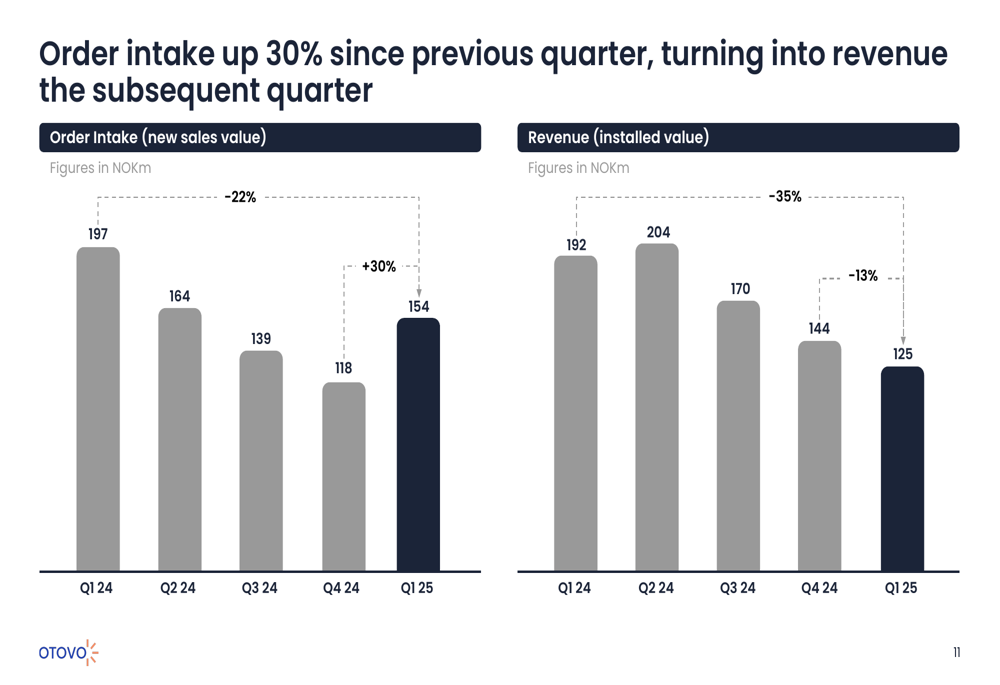

Otovo reported a significant turnaround in order intake, which increased by 30% compared to Q4 2024, reaching NOK 154 million. This growth comes after several quarters of decline, including a 35% drop in Q3 2024. The company’s backlog also grew substantially to NOK 195 million, representing a 27% increase from the previous quarter.

As shown in the following chart of quarterly order intake and revenue trends:

Despite the positive momentum in new orders, revenue decreased by 13% compared to Q4 2024, totaling NOK 125 million. Gross profit also saw a slight decline of 8% to NOK 31 million. However, gross margin improved by 2 percentage points to 25%, indicating better profitability per project.

Net sold projects showed strong recovery with a 34% increase in Q1 2025, reaching 1,410 projects, while installations decreased by 15% to 1,017. This divergence suggests a potential pipeline for future revenue as the backlog converts to installations.

Strategic Initiatives

Otovo’s strategy centers around three key pillars: cost reduction, monetization through portfolio sales, and sales growth. The company has implemented significant cost cuts, prioritized certain geographies, and restructured operations to achieve cost reductions of NOK 200-250 million.

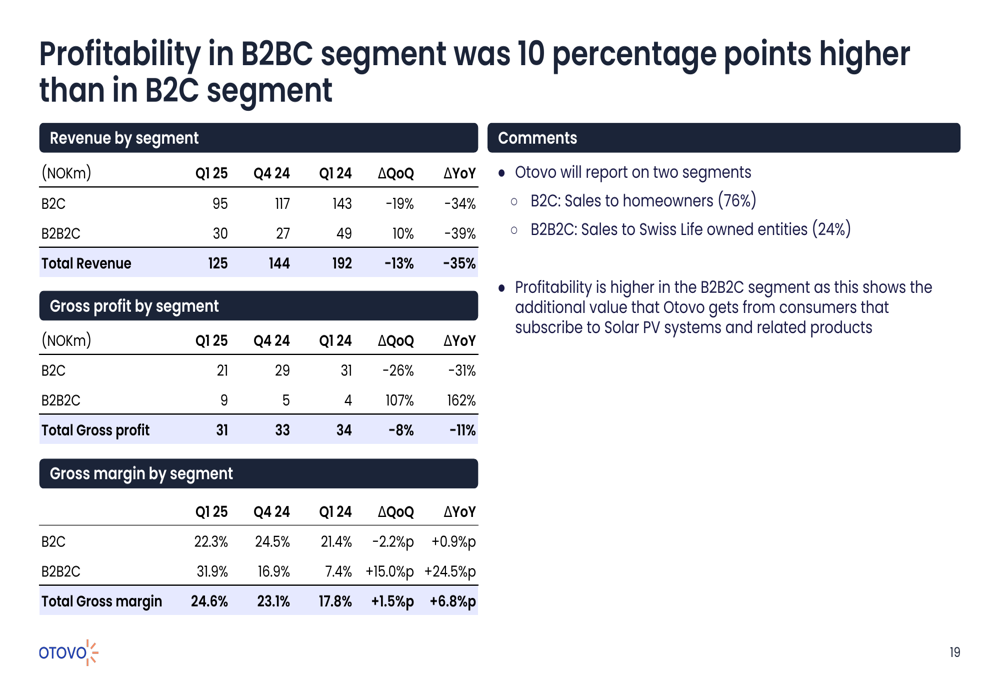

The company’s business model now clearly distinguishes between two segments: direct-to-consumer (B2C), which accounted for 76% of Q1 revenue with a 23% gross margin, and the leasing portfolio owner (B2B2C) segment, which showed higher profitability with a gross margin of 32% for the Rest of Europe portfolio.

The following chart illustrates the profitability comparison between these segments:

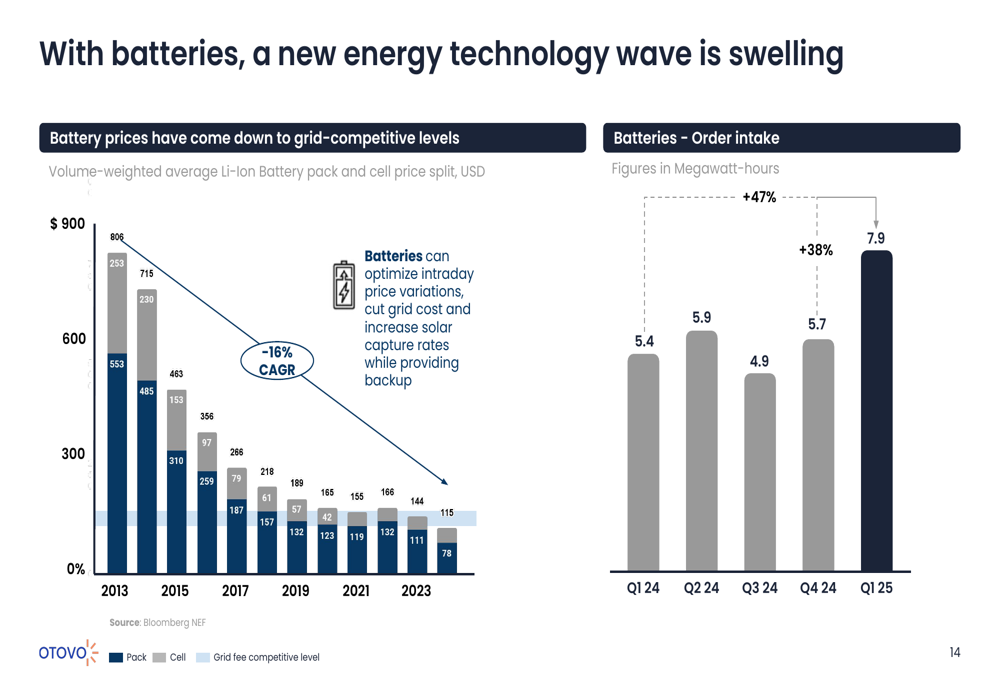

A significant strategic focus is the growing battery market, which Otovo believes represents the next wave in energy technology adoption. Battery order intake increased to 7.9 MW in Q1 2025, up from 5.7 MW in Q4 2024, representing a substantial growth opportunity as battery prices continue to decline at a CAGR of -16%.

As shown in the following data on battery technology trends:

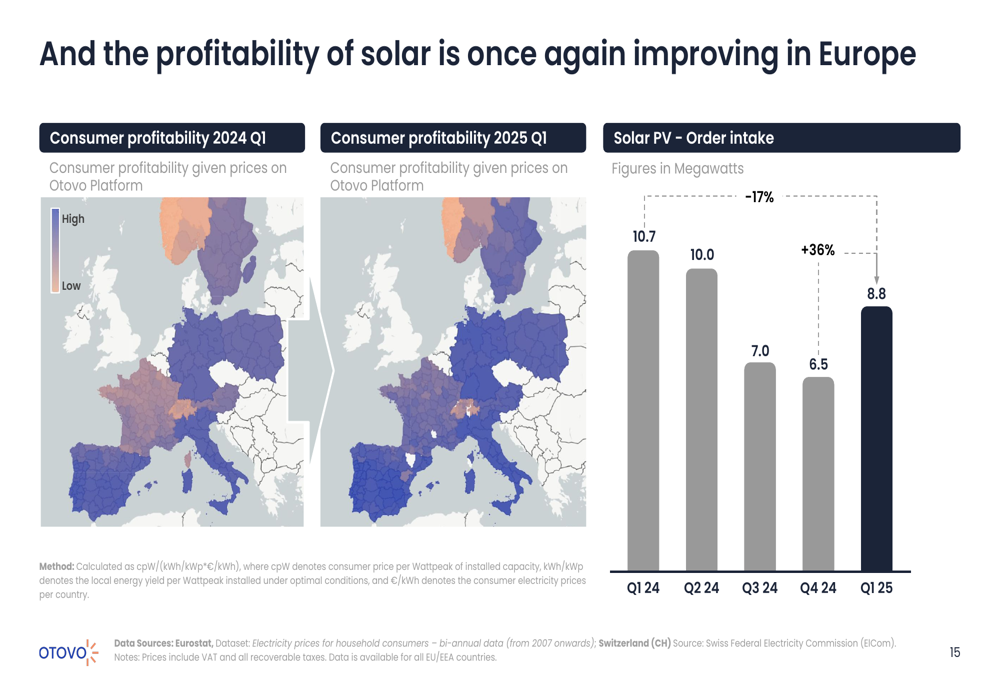

Similarly, solar PV order intake has rebounded to 8.8 MW in Q1 2025 from 6.5 MW in Q4 2024, as profitability of solar installations improves across Europe:

Detailed Financial Analysis

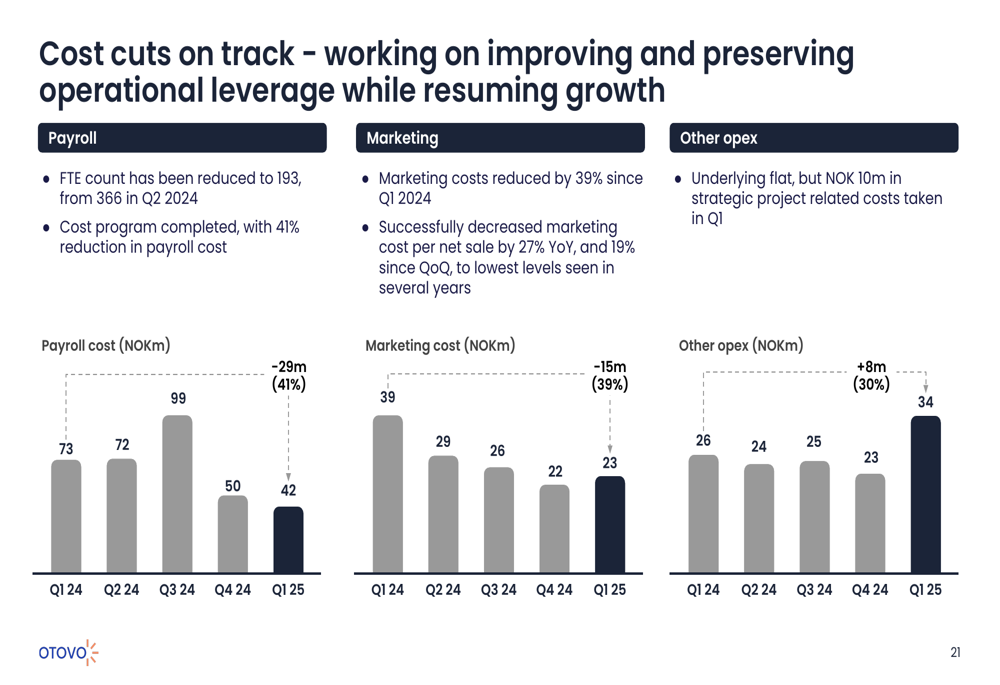

Otovo’s financial position reflects both the ongoing transformation and early signs of recovery. The company has successfully reduced its cost structure, with significant cuts in marketing and payroll expenses compared to the previous year.

The following chart demonstrates the effectiveness of these cost-cutting measures:

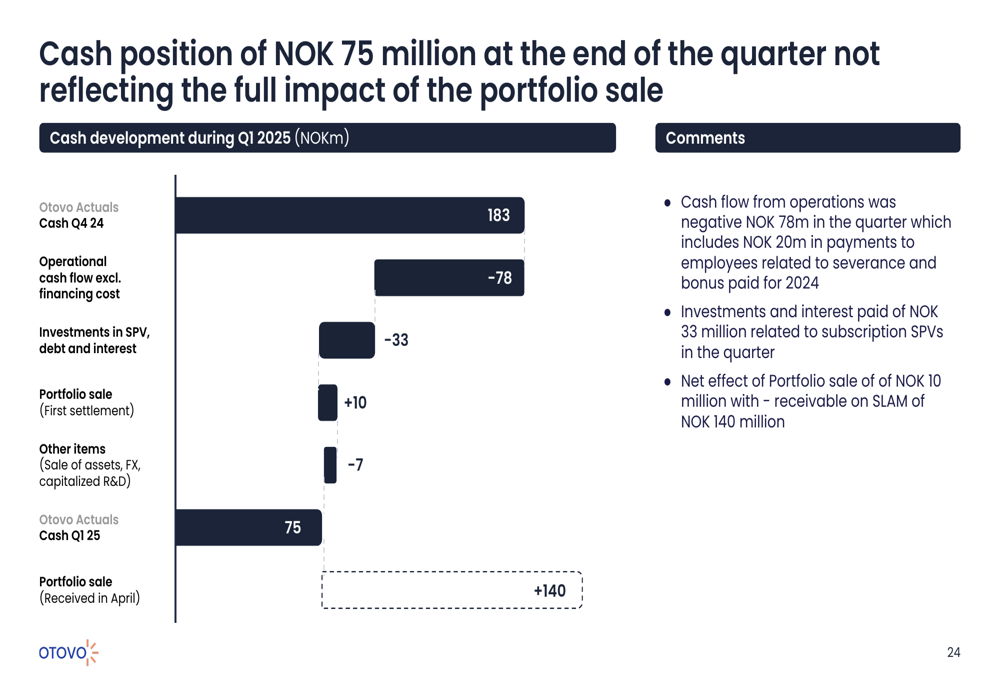

The company reported a cash position of NOK 75 million at the end of Q1, which does not yet fully reflect the impact of the portfolio sale to Swiss Life (SIX:SLHN) Asset Managers. When accounting for all components of the transaction, Otovo indicates it will have over NOK 200 million available.

This waterfall chart shows the components affecting the cash position:

The balance sheet has been reduced following the divestment of the continental subscription portfolio, with Otovo maintaining approximately 11% ownership stake in EDEA Europe, which is now accounted for as an associated company. At quarter end, Otovo had a receivable of approximately NOK 140 million toward EDEA Europe.

One financial challenge noted was adverse currency effects of NOK 24 million in the quarter, though the company emphasized these had no cash effect and were related to financing subsidiaries in EUR.

Forward-Looking Statements

Looking ahead, Otovo’s management expressed confidence in the company’s return to growth trajectory while maintaining its cost discipline. The presentation highlighted several factors expected to drive future performance:

1. Improving consumer outlook triggered by better payback times for solar installations

2. Growing demand for batteries and backup solutions as energy resilience becomes more important

3. Continued profitability improvements, particularly in the B2B2C segment

4. Further optimization of the cost structure while preserving operational leverage

The company’s CEO Andreas Thorsheim and CFO Petter Ulset emphasized that Otovo has positioned itself as a leaner operation capable of scaling without proportional increases in headcount, setting the stage for potential profitability as volumes increase.

The presentation’s quarterly highlights summarize the company’s current position and outlook:

While Otovo faces ongoing challenges in a competitive and evolving European energy market, the Q1 2025 results suggest the company’s strategic reset is beginning to yield positive results, with growth resuming and cost structure improvements taking hold.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.