JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Outfront Media Inc (NYSE:OUT) presented its second quarter 2025 financial results on August 5, showing signs of stabilization after a challenging first quarter. The company’s stock closed at $17.95 on the day of the presentation, up 2.01% from the previous close, indicating positive market reception despite mixed financial results.

The out-of-home advertising company continues to navigate a transitional period, with organizational restructuring and digital transformation efforts aimed at addressing ongoing revenue challenges. Following a disappointing Q1 where the company missed EPS expectations, Q2 results showed modest improvement in key metrics.

Quarterly Performance Highlights

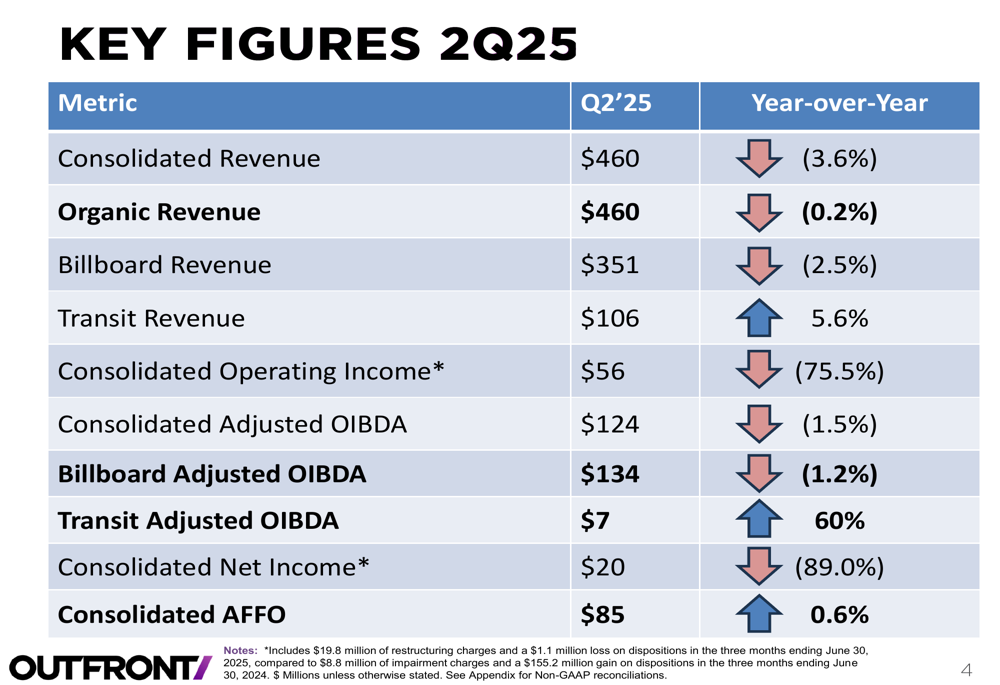

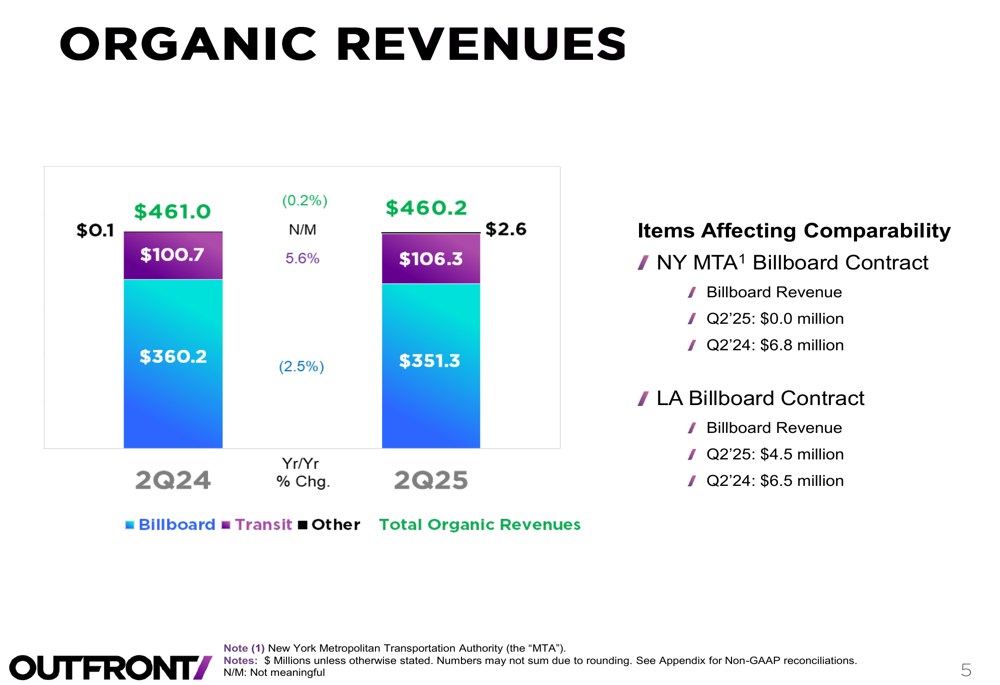

Outfront Media reported consolidated revenue of $460 million for Q2 2025, representing a 3.6% year-over-year decline. However, on an organic basis, revenue was nearly flat at $460.2 million, down just 0.2% compared to the same period last year.

As shown in the following comprehensive overview of key financial metrics:

The company’s consolidated adjusted OIBDA (Operating Income Before Depreciation and Amortization) reached $124 million, down 1.5% year-over-year, while consolidated AFFO (Adjusted Funds From Operations) showed a slight improvement of 0.6%, reaching $85 million.

Net income saw a significant decline of 89.0% to $20 million, largely due to restructuring charges and losses on dispositions. Operating income dropped 75.5% to $56 million, reflecting these one-time charges as the company repositions itself strategically.

Segment Analysis: Billboard vs Transit

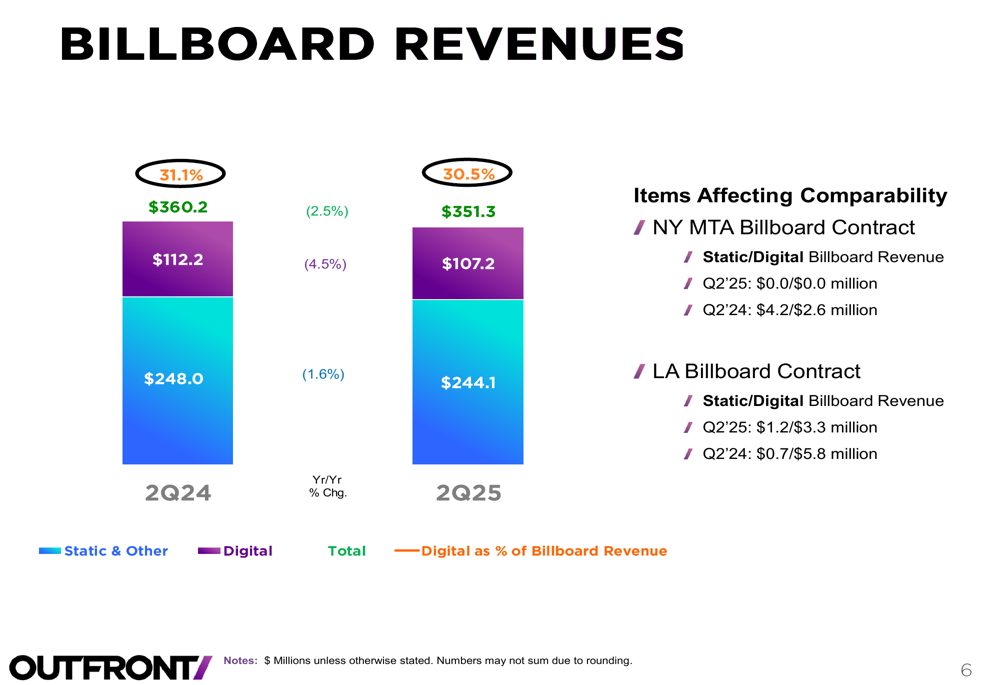

The company’s performance showed a clear divergence between its billboard and transit segments. Billboard revenue, which constitutes the majority of Outfront’s business, declined 2.5% year-over-year to $351 million. This was partially offset by strong performance in the transit segment, which grew 5.6% to $106 million.

The following chart illustrates the organic revenue breakdown between these segments:

The billboard segment’s performance was negatively impacted by the expiration of the NY MTA Billboard Contract, which contributed $6.8 million in Q2 2024 but nothing in Q2 2025. Additionally, the LA Billboard Contract revenue decreased from $6.5 million to $4.5 million.

Despite the revenue decline, billboard adjusted OIBDA margin improved slightly to 38.3% from 37.8% in the prior year, demonstrating effective cost management. The transit segment showed even more impressive margin improvement, with adjusted OIBDA margin increasing to 6.8% from 4.5% a year earlier.

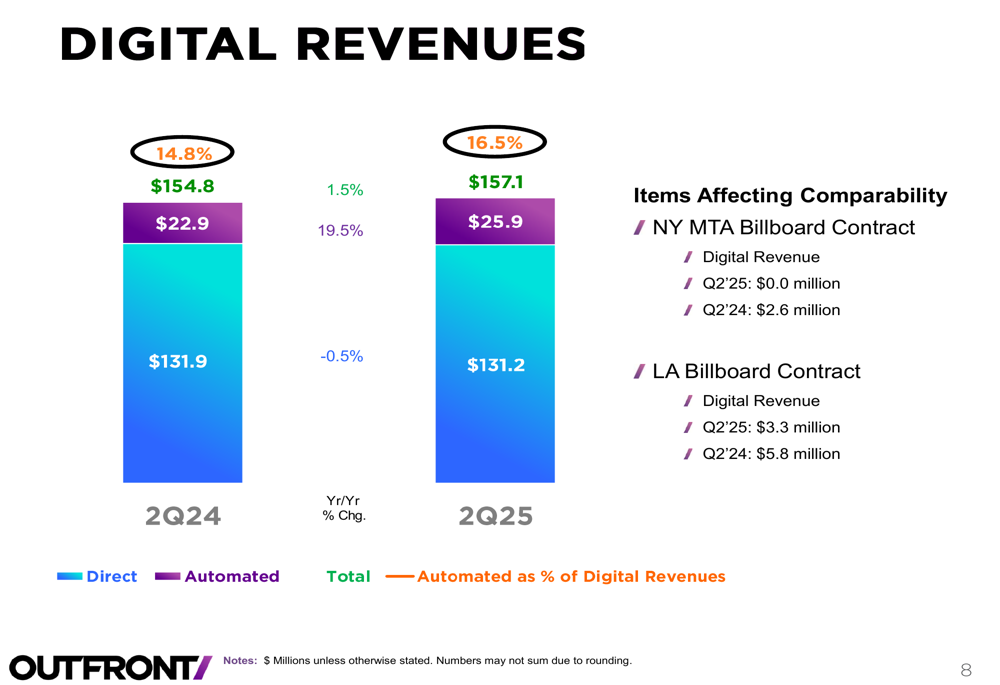

Digital Transformation Progress

Digital revenue continues to be a bright spot for Outfront Media, representing an increasing portion of the company’s business. The breakdown of billboard revenues between static and digital formats shows:

While digital billboard revenue declined slightly from $112.2 million to $107.2 million, digital transit revenue increased from $42.6 million to $49.9 million. Overall, digital revenue as a percentage of total transit revenue increased to 46.9% from 42.3% in the prior year.

The company’s automated digital revenue also showed growth, increasing from $22.9 million to $25.9 million, representing 16.5% of total digital revenues compared to 14.8% a year earlier:

This shift toward automated digital advertising aligns with broader industry trends toward programmatic ad buying and suggests Outfront is making progress in its digital transformation efforts.

Organizational Changes

A significant portion of the presentation focused on organizational restructuring, indicating the company is taking proactive steps to address market challenges. Key changes include rebranding the "National" sales team as "Enterprise" and "Local" as "Commercial," along with centralizing operations and real estate functions.

The company has also reduced its regional structure from four regions to three and made several key management appointments, including promoting Mark Bonanni to Chief Revenue Officer for Commercial Sales and hiring Jim Norton as Chief Revenue Officer for Enterprise Sales.

These changes appear designed to streamline operations, reduce costs, and better position the company to capitalize on growth opportunities in digital and transit advertising.

Balance Sheet and Outlook

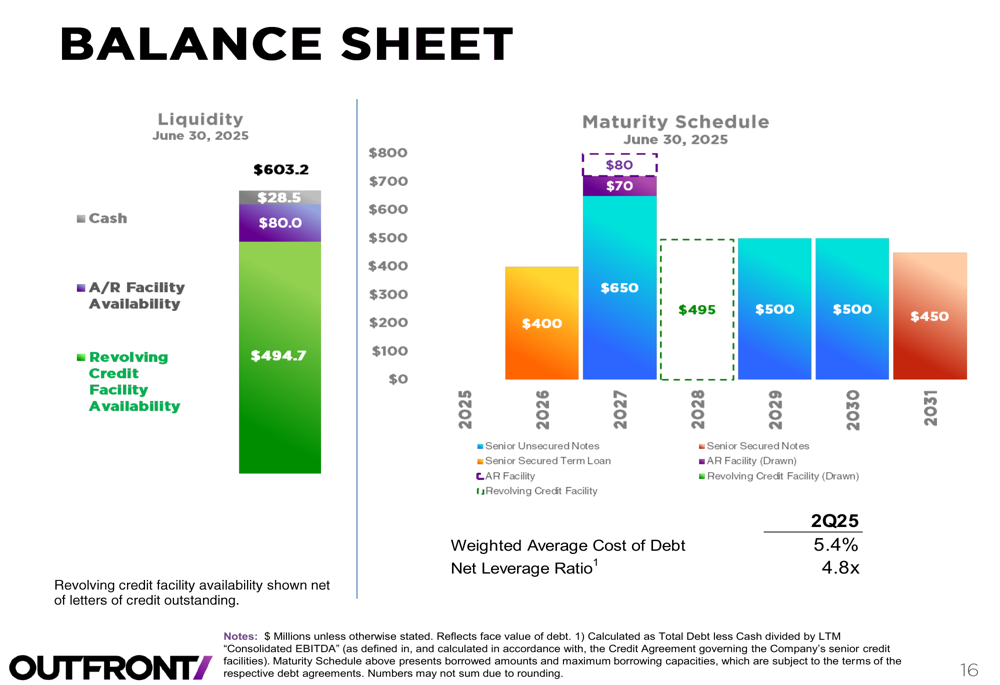

Outfront Media maintained a solid liquidity position with $28.5 million in cash and $494.7 million available under its credit facilities. The company’s debt maturity schedule shows a well-structured profile with no significant near-term maturities:

The weighted average cost of debt stands at 5.4%, with a net leverage ratio of 4.8x. This represents a manageable debt level for the company, though slightly higher than some industry peers.

Capital expenditures increased to $25.7 million from $18.5 million in the prior year, with growth capex accounting for most of the increase ($18.7 million vs. $11.8 million). This suggests the company continues to invest in future growth despite current challenges.

The company’s AFFO of $85.3 million, while only slightly higher than the previous year, indicates sufficient cash flow to maintain its dividend, which remained at $0.30 per share following the Q1 results.

Looking ahead, Outfront’s focus on digital transformation and transit segment growth, combined with organizational restructuring, positions the company to potentially improve performance in the second half of 2025, particularly if advertising spending stabilizes or increases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.