Japan records surprise trade deficit in July as exports weaken further

Introduction & Market Context

Ovintiv Inc. (NYSE:OVV) delivered strong operational results in the second quarter of 2025, exceeding production guidance while spending less capital than anticipated. The company, which positions itself as "a Permian and Montney oil powerhouse," reported significant improvements in operational efficiency and raised its full-year production outlook while simultaneously reducing capital expenditure guidance.

The results come amid a period of strategic focus on balancing shareholder returns with debt reduction, as Ovintiv continues to leverage its multi-basin portfolio across the Permian, Montney, and Anadarko regions. The company’s performance demonstrates resilience in a commodity price environment where efficiency and capital discipline remain paramount.

Quarterly Performance Highlights

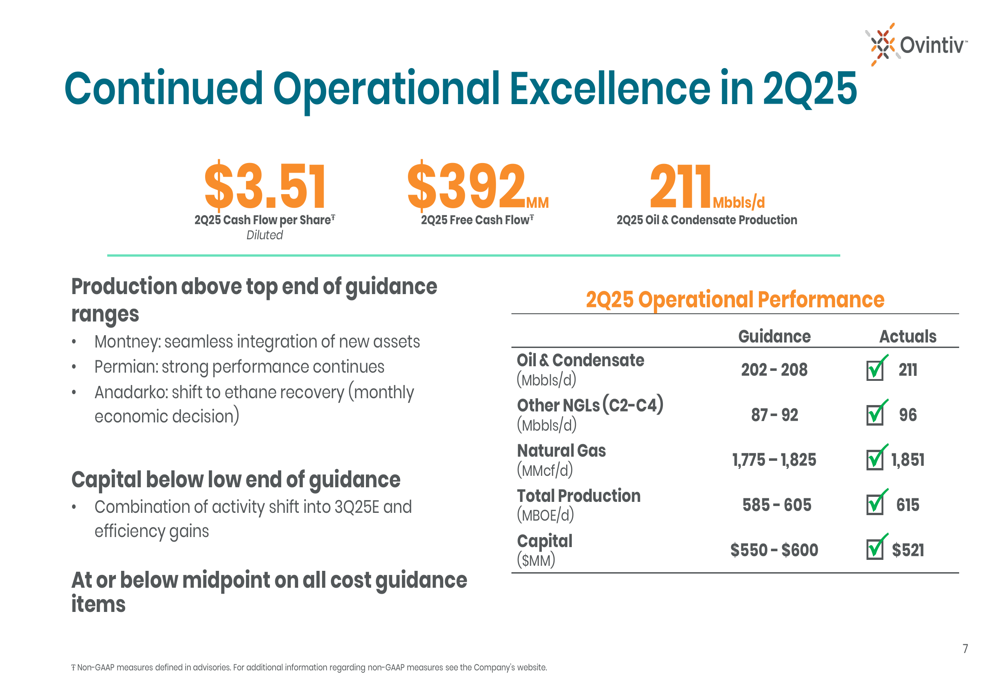

Ovintiv significantly outperformed its second-quarter guidance across all production metrics while keeping capital spending below the low end of its forecast range. Oil and condensate production reached 211 Mbbls/d, exceeding the guidance range of 202-208 Mbbls/d, while total production hit 615 MBOE/d, surpassing the 585-605 MBOE/d guidance.

As shown in the following operational performance comparison, the company achieved these production gains while spending less than anticipated on capital:

The company generated $392 million in free cash flow during the quarter, with cash flow per share reaching $3.51. This strong cash generation was driven by operational excellence, particularly in the Permian basin and newly integrated Montney assets, as well as a shift to ethane recovery in the Anadarko basin.

Strategic Initiatives

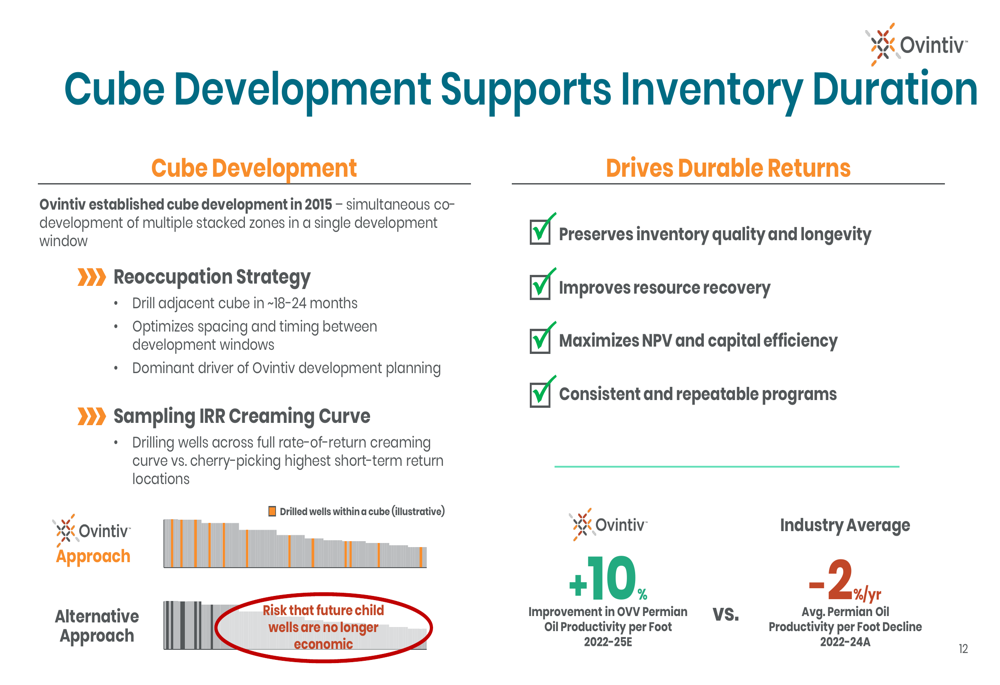

Ovintiv’s "cube development" strategy continues to deliver superior results compared to industry averages. This approach involves the simultaneous co-development of multiple stacked zones in a single window, which the company has been implementing since 2015.

The company’s presentation highlights how this strategy is yielding tangible benefits in the Permian basin, where Ovintiv has achieved a 10% improvement in oil productivity per foot from 2022 to 2025, compared to an industry average decline of 2% per year:

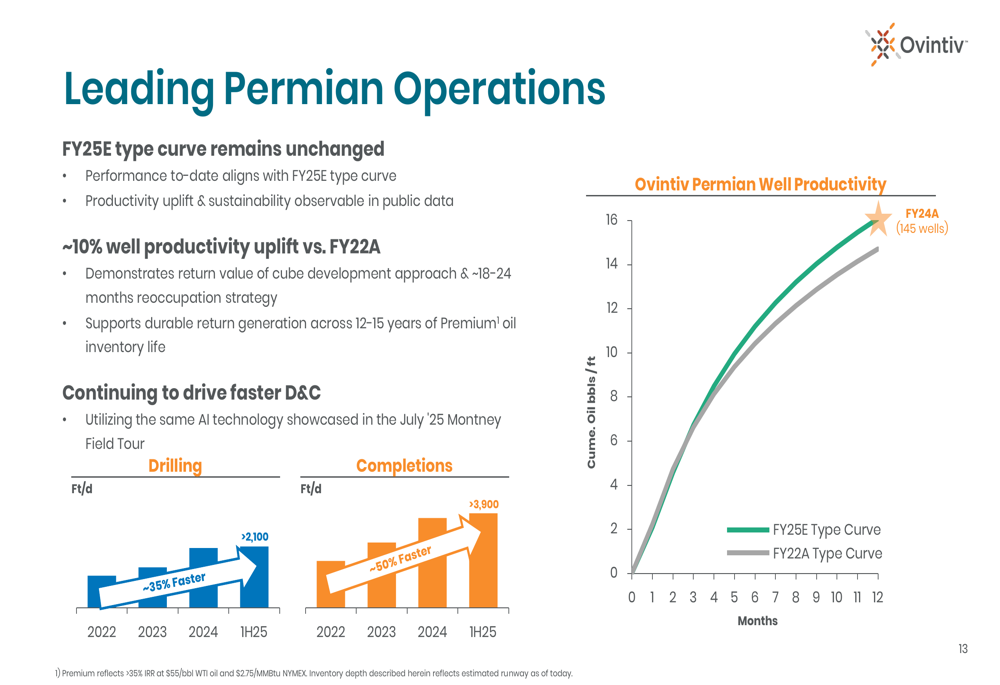

In the Permian, Ovintiv has made significant strides in operational efficiency, with drilling speeds approximately 35% faster than in FY2022 and completion speeds 50% faster over the same period. These improvements support the company’s claim of having 12-15 years of premium oil inventory in the region:

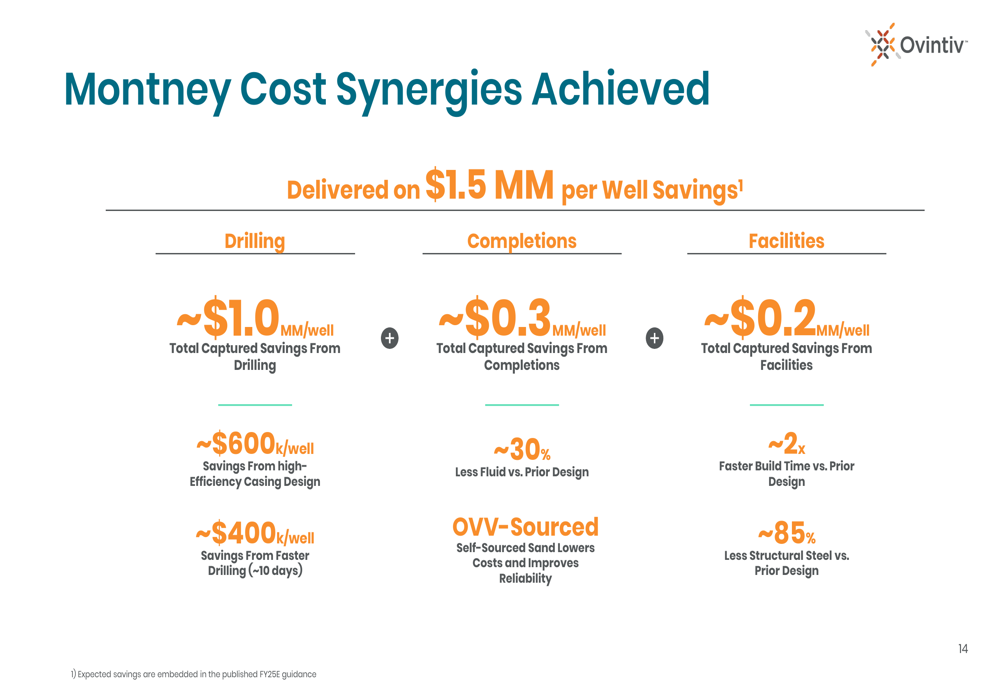

The integration of acquired Montney assets is progressing well, with the company achieving its targeted $1.5 million per well cost savings. These savings come from multiple areas:

Financial Outlook

Ovintiv has updated its full-year 2025 guidance, increasing production expectations while reducing capital expenditure forecasts. The company now expects to produce 205-209 Mbbls/d of oil and condensate (up from 202-208 Mbbls/d) while reducing its capital spending range to $2,125-2,175 million (down $50 million from the previous midpoint).

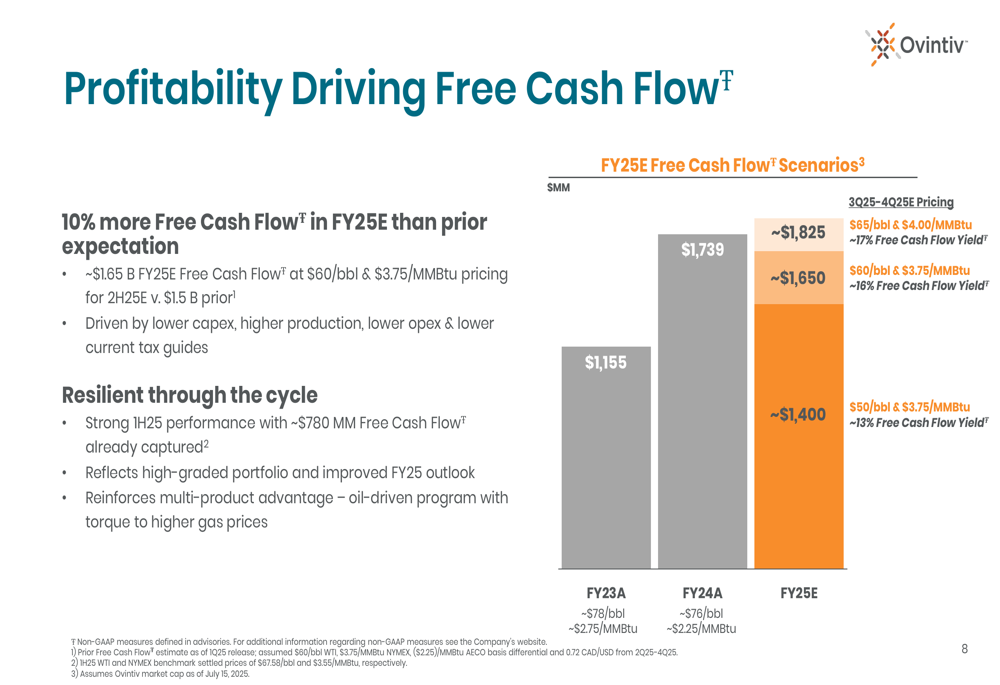

The company projects free cash flow of approximately $1.65 billion for FY2025, assuming $60/bbl WTI and $3.75/MMBtu NYMEX natural gas prices, representing a free cash flow yield of approximately 16%. This outlook reflects a 10% improvement from prior expectations, driven by lower capital expenditures, higher production, and reduced operating expenses:

Ovintiv is also working to diversify its natural gas exposure, particularly in the Montney region. The company has secured its first exposure to JKM (Asian LNG index) through a two-year contract for 50 MMcf/d, additional Chicago exposure through a 10-year contract for 100 MMcf/d, and enhanced AECO physical deals through late 2027. These agreements should help improve realized prices for Montney gas production, which achieved 177% of AECO or 72% of NYMEX in the first half of 2025.

Shareholder Returns & Debt Reduction

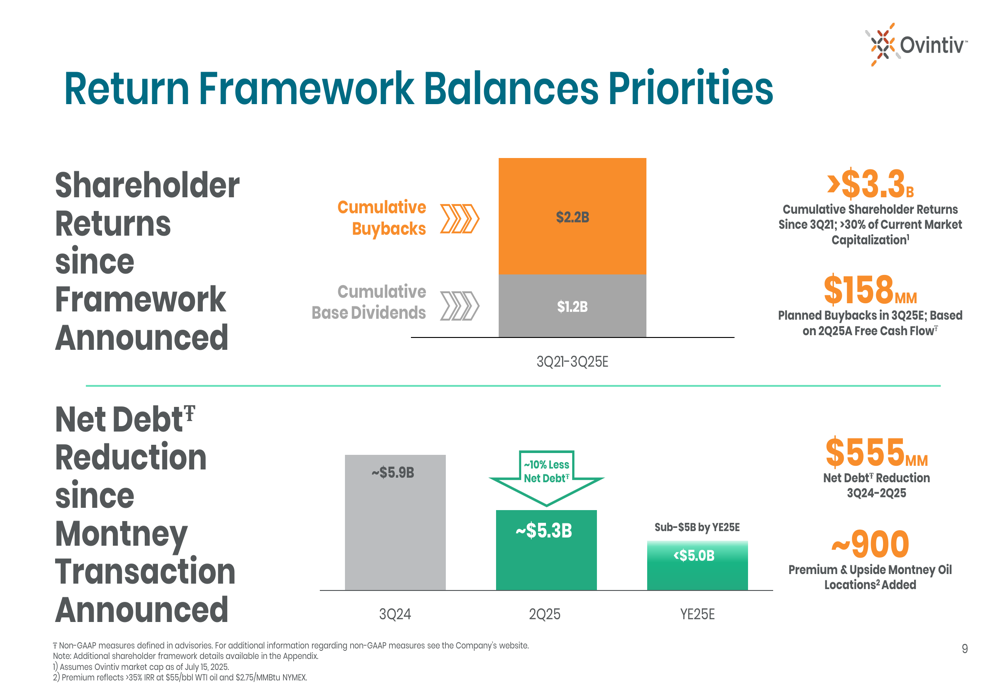

Ovintiv continues to balance shareholder returns with debt reduction as part of its capital allocation framework. Since the third quarter of 2021, the company has returned over $3.3 billion to shareholders, representing more than 30% of its current market capitalization. This includes $2.2 billion in share buybacks and $1.2 billion in base dividends.

Based on its strong Q2 free cash flow, the company plans to execute $158 million in share buybacks during the third quarter of 2025. At the same time, Ovintiv remains committed to debt reduction, having decreased net debt by $555 million from Q3 2024 to Q2 2025, with a target to reduce net debt below $5 billion by year-end 2025:

Forward-Looking Statements

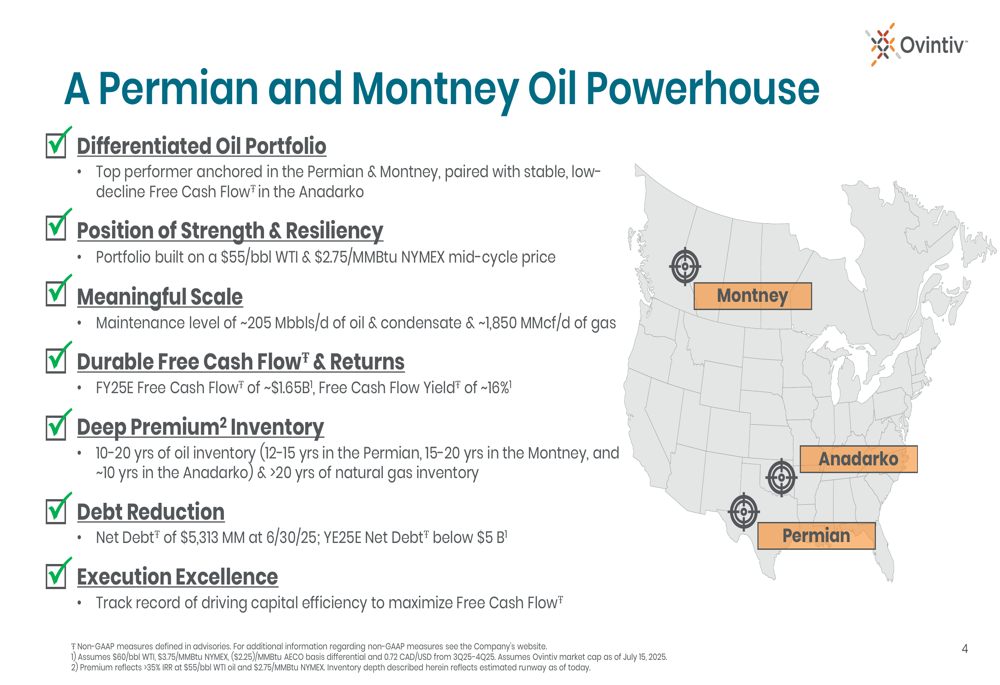

Ovintiv emphasizes its long-term inventory depth and quality as a key pillar of its durable returns strategy. The company claims to have 10-20 years of premium oil inventory and more than 20 years of natural gas inventory across its multi-basin portfolio. This inventory is supported by a breakeven of less than $40/bbl WTI with base dividend.

The company’s portfolio was built on mid-cycle price assumptions of $55/bbl WTI and $2.75/MMBtu NYMEX, providing resilience through commodity price cycles. Ovintiv maintains that its maintenance level production is approximately 205 Mbbls/d of oil and condensate and 1,850 MMcf/d of natural gas.

As illustrated in the company’s overview slide, Ovintiv positions itself as a leader in both the Permian and Montney regions, with stable free cash flow generation from the Anadarko basin:

Looking ahead to the third quarter of 2025, Ovintiv expects to produce 202-208 Mbbls/d of oil and condensate, 94-98 Mbbls/d of other NGLs, and 1,875-1,925 MMcf/d of natural gas, with capital spending of $525-575 million. The company anticipates a step-up in natural gas volumes in the second half of 2025 as Western Canada gas systems constraints ease with the ramp-up of LNG Canada.

Ovintiv’s presentation demonstrates a continued focus on operational excellence, capital efficiency, and balanced capital allocation between shareholder returns and debt reduction, positioning the company to deliver sustainable free cash flow through varying commodity price environments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.