Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Owens & Minor Inc (NYSE:OMI) released its second-quarter 2025 earnings presentation on August 11, highlighting the company’s financial outlook and strategic direction for the remainder of the year. The presentation comes after the healthcare solutions company’s stock jumped 12.36% to $7.09 on August 8, though it remains significantly below its 52-week high of $16.63.

The company’s presentation follows a first quarter in which Owens & Minor beat earnings expectations with EPS of $0.23 versus a forecasted $0.20, despite slightly missing revenue projections. The healthcare products and services provider continues to navigate industry-wide challenges, including tariff pressures and competitive market dynamics.

Financial Outlook for 2025

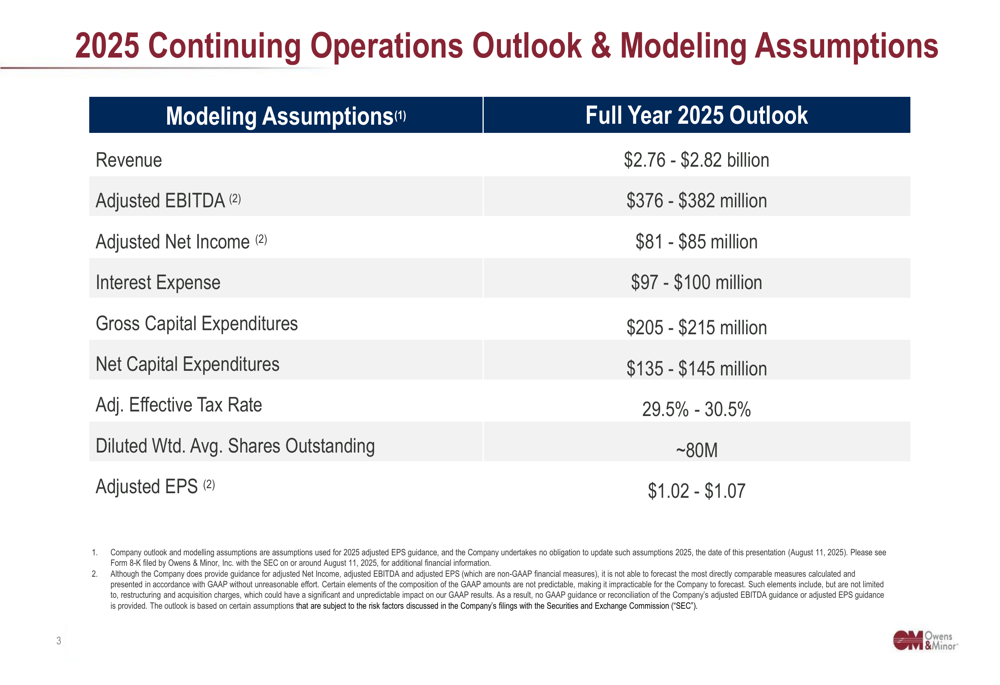

Owens & Minor’s Q2 presentation maintains a steady outlook for the full year 2025, projecting revenue between $2.76 billion and $2.82 billion. This guidance aligns with the company’s performance trajectory from Q1, where it reported $2.63 billion in revenue, representing a 1% year-over-year increase.

The company’s detailed financial projections for 2025 include:

The adjusted EBITDA outlook of $376-$382 million suggests continued operational efficiency, building on the 5% increase in adjusted EBITDA reported in Q1. Similarly, the projected adjusted net income of $81-$85 million indicates management’s confidence in maintaining the 20% growth in adjusted net income observed earlier this year.

With adjusted EPS guidance of $1.02-$1.07, Owens & Minor appears positioned to deliver consistent earnings performance, though investors should note the significant interest expense projection of $97-$100 million, which will impact bottom-line results.

Capital Allocation and Investment Strategy

The presentation reveals substantial planned capital expenditures for 2025, with gross capital expenditures projected at $205-$215 million and net capital expenditures at $135-$145 million. These investment levels suggest Owens & Minor is continuing to prioritize growth initiatives and operational improvements despite market challenges.

This capital allocation strategy aligns with statements made during the Q1 earnings call, where management indicated that the planned acquisition of RoTEK is expected to close in the first half of 2025. The significant capital expenditure outlook likely incorporates integration costs and strategic investments related to this acquisition.

Growth Expectations and Challenges

Consistent with previous guidance, Owens & Minor appears to be maintaining its expectation that approximately 70% of earnings and cash flow will be generated in the second half of 2025. This back-loaded financial performance projection underscores the importance of the coming quarters for meeting full-year targets.

The company continues to face headwinds, particularly from tariffs, which were identified in Q1 as representing a $100-$150 million exposure primarily affecting the Products and Healthcare Services (NASDAQ:HCSG) segment. The Q2 presentation does not explicitly address these challenges, focusing instead on the overall financial outlook.

Legal Considerations and Forward-Looking Statements

The presentation includes standard safe harbor language regarding forward-looking statements and non-GAAP financial measures, cautioning investors about placing undue reliance on projections.

This disclaimer is particularly relevant given the company’s ambitious second-half performance expectations and the volatile market environment. The safe harbor statement emphasizes that the company specifically disclaims any obligation to update or revise forward-looking statements, providing management with flexibility should market conditions change.

Market Reaction and Investment Perspective

While the presentation itself does not provide information on immediate market reaction to the Q2 results, the recent stock performance context is noteworthy. The 12.36% jump in share price just prior to the earnings presentation suggests positive market sentiment, though the stock remains well below its 52-week high, indicating continued investor caution.

The projected adjusted effective tax rate of 29.5%-30.5% and approximately 80 million diluted weighted average shares outstanding provide additional context for investors evaluating Owens & Minor’s financial outlook and potential earnings growth.

For investors, the Q2 presentation reinforces the company’s strategic focus on operational efficiency and growth in key segments like Patient Direct, which showed 6% revenue growth in Q1. However, the substantial capital expenditure plans and significant interest expense projections highlight ongoing financial challenges that may impact profitability in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.