Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Owlet Inc. (NYSE:OWLT) presented its Q2 2025 financial results on August 7, 2025, revealing robust growth and improved profitability that exceeded market expectations. The baby monitoring technology company saw its shares rise 10% in after-hours trading following the presentation, with the stock closing at $7.81 before the announcement.

The company has maintained its upward trajectory from Q1, when it reported 43.1% year-over-year revenue growth. This quarter’s results reflect Owlet’s continued success in expanding its product adoption and subscription services while making strategic inroads into healthcare channels.

Quarterly Performance Highlights

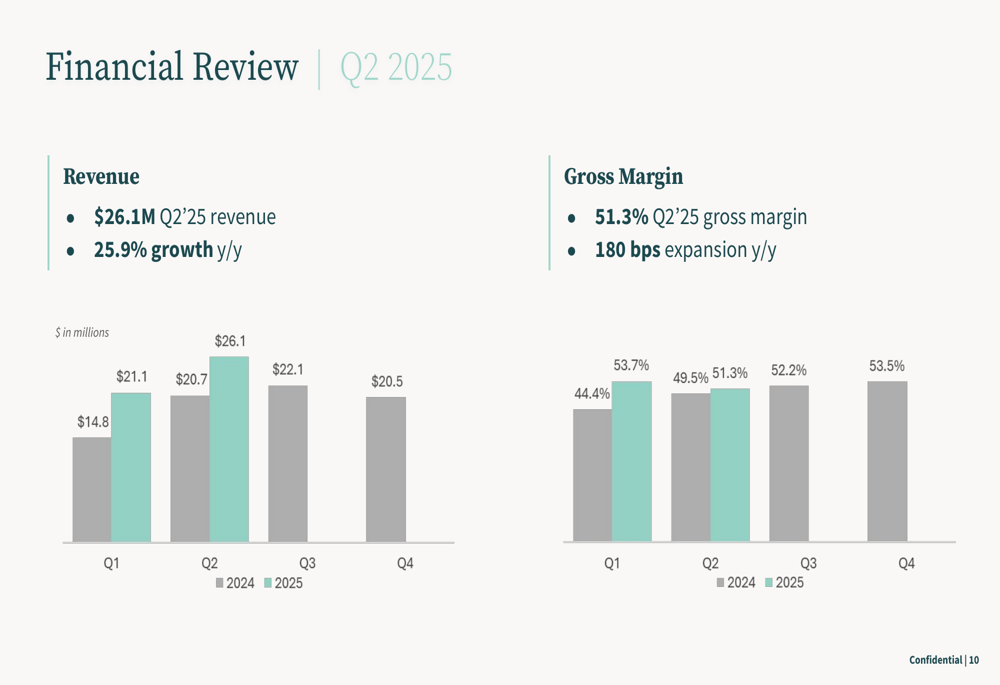

Owlet reported Q2 2025 revenue of $26.1 million, representing a 25.9% increase compared to the same period last year. This growth exceeded analyst expectations and demonstrated the company’s strong market position in the baby monitoring category.

As shown in the following chart of quarterly revenue progression, Owlet has maintained consistent growth momentum:

Gross margin expanded to 51.3%, marking the ninth consecutive quarter of improvement with a 180 basis point increase year-over-year. This consistent margin expansion highlights the company’s improving operational efficiency despite facing increased tariff costs.

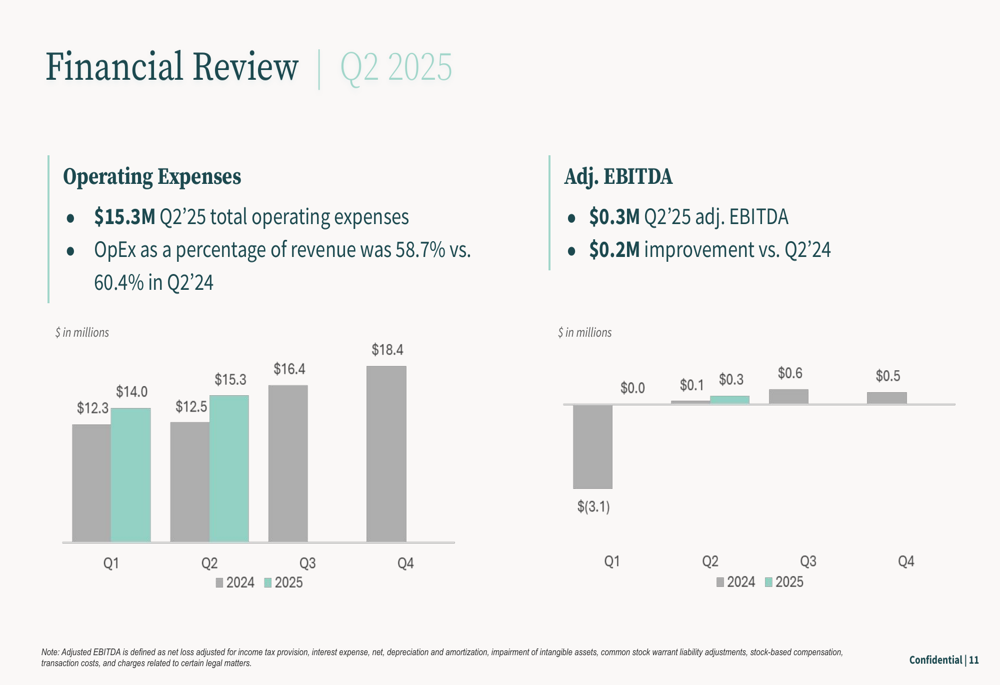

The company achieved adjusted EBITDA of $0.3 million, a $0.2 million improvement compared to Q2 2024. This represents the fifth consecutive quarter of adjusted EBITDA growth and profitability, as illustrated in this financial performance chart:

Product and Subscription Growth

Owlet’s flagship Dream Sock product continued to gain market traction with domestic sell-through growth of 37% year-over-year and registry additions increasing by 54%. The product maintained a strong Net Promoter Score (NPS) of 73+, indicating high customer satisfaction.

The company achieved record-setting performance during Amazon (NASDAQ:AMZN) Prime Day, becoming the #1 seller in the baby monitor category in both the U.S. and U.K. markets. U.S. sales grew 72% year-over-year, while U.K. sales surged by an impressive 144%.

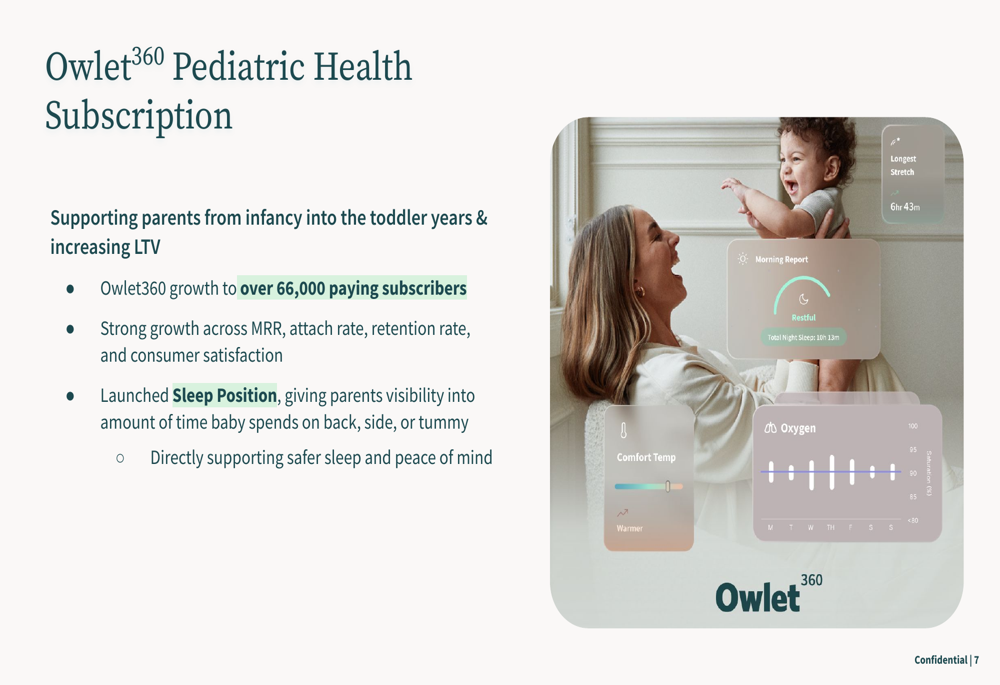

The Owlet360 pediatric health subscription service has emerged as a significant growth driver, with the company reporting over 66,000 paying subscribers. The service has shown strong performance across key metrics including monthly recurring revenue (MRR), attach rate, retention rate, and consumer satisfaction.

The company recently enhanced the subscription offering with a new Sleep Position feature that gives parents visibility into the amount of time a baby spends on back, side, or tummy, supporting safer sleep practices. The following image illustrates the Owlet360 interface and functionality:

Strategic Healthcare Expansion

Owlet is strategically expanding beyond consumer markets into medical and healthcare channels. The company is developing insurance-reimbursed health monitors for high-risk babies and creating Owlet Connect, a proprietary enterprise data integration platform.

This platform will enable real-time sharing of BabySat data with pediatricians and integration into clinical workflows, electronic medical record (EMR) systems, and research databases. The company highlighted a strategic alliance with Children’s Hospital of The King’s Daughter (CHKD) that leverages Owlet products and the Owlet Connect platform.

Financial Analysis

Operating expenses for Q2 2025 were $15.3 million, representing 58.7% of revenue compared to 60.4% in the same period last year. This improvement in operational efficiency, combined with gross margin expansion, contributed to the positive adjusted EBITDA result.

The company’s quarterly financial trends show consistent improvement in profitability metrics, with adjusted EBITDA progressing from negative $3.1 million in Q1 2024 to positive $0.3 million in Q2 2025. This progression aligns with the company’s stated goal of sustainable profitability.

Updated Guidance and Outlook

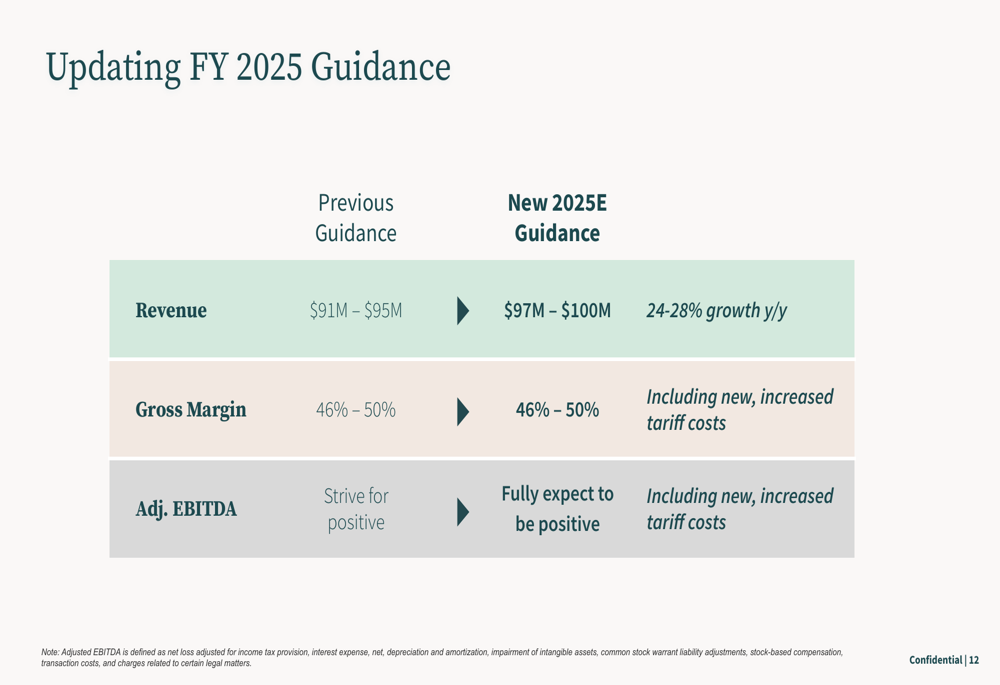

Based on strong first-half performance, Owlet has raised its full-year 2025 revenue guidance to $97-$100 million, representing 24-28% year-over-year growth. This is a significant increase from the previous guidance of $91-$95 million provided during the Q1 earnings call.

The company maintained its gross margin guidance at 46-50%, which accounts for new, increased tariff costs. Importantly, management now "fully expects" adjusted EBITDA to be positive for the full year, upgrading from the previous outlook of "striving for positive" adjusted EBITDA.

The following table details the updated guidance compared to previous projections:

The raised guidance reflects management’s confidence in continued growth across both product sales and subscription services, despite potential headwinds from increased tariffs. With consecutive quarters of improving financial metrics and expanding market presence, Owlet appears well-positioned to maintain its growth trajectory through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.