Stock market today: S&P 500 drops for fifth day as focus shifts to Powell’s speech

P10 Inc (NYSE:PX) released its first quarter 2025 earnings presentation on May 8, showing continued growth in fee-paying assets under management (FPAUM) while reporting mixed financial results. The alternative asset manager’s stock fell approximately 12.4% in premarket trading, suggesting investors may have been expecting stronger performance.

Executive Summary

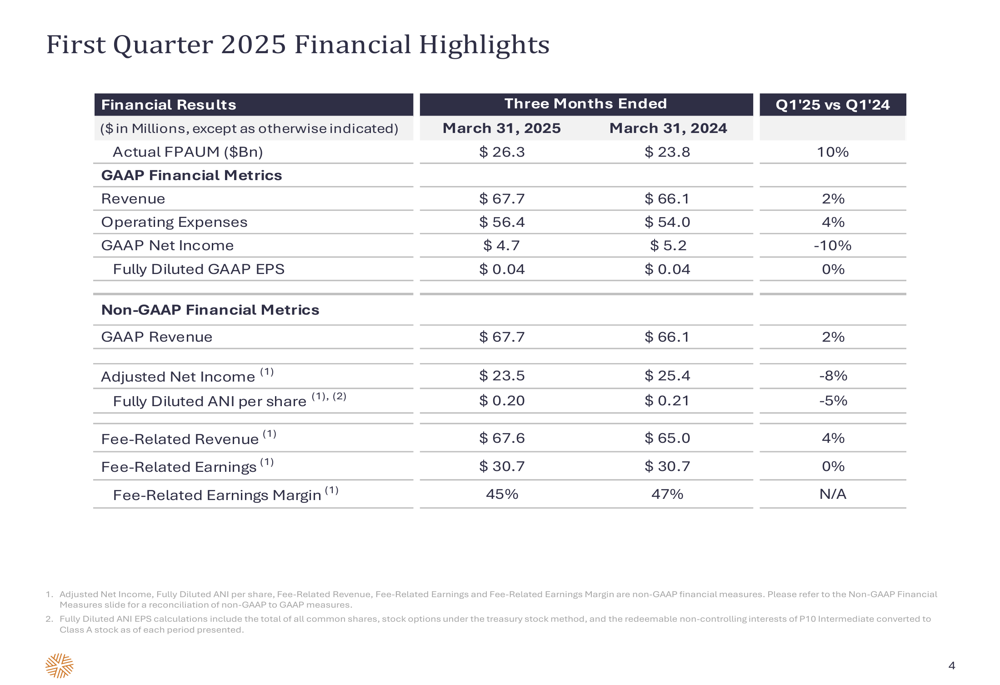

P10 reported a 10% year-over-year increase in FPAUM to $26.3 billion for Q1 2025, maintaining its trajectory toward long-term growth targets. However, financial results were more modest, with GAAP revenue up 2% to $67.7 million and GAAP net income down 10% to $4.7 million compared to the same period last year.

As shown in the following financial highlights chart, the company maintained its fully diluted GAAP EPS at $0.04 despite the decline in net income, while fee-related earnings remained flat at $30.7 million with a 45% margin:

"We’ve made significant progress on our strategic priorities," said Luke Sarsfield, Chairman and CEO of P10, who presented alongside EVP & CFO Amanda Coussens and EVP & CAO Mark Hood. The company highlighted its record fundraise and deployment of over $1.4 billion in FPAUM for the first three months of 2025, as well as the successful closing of its Qualitas Funds acquisition in April.

Quarterly Performance Highlights

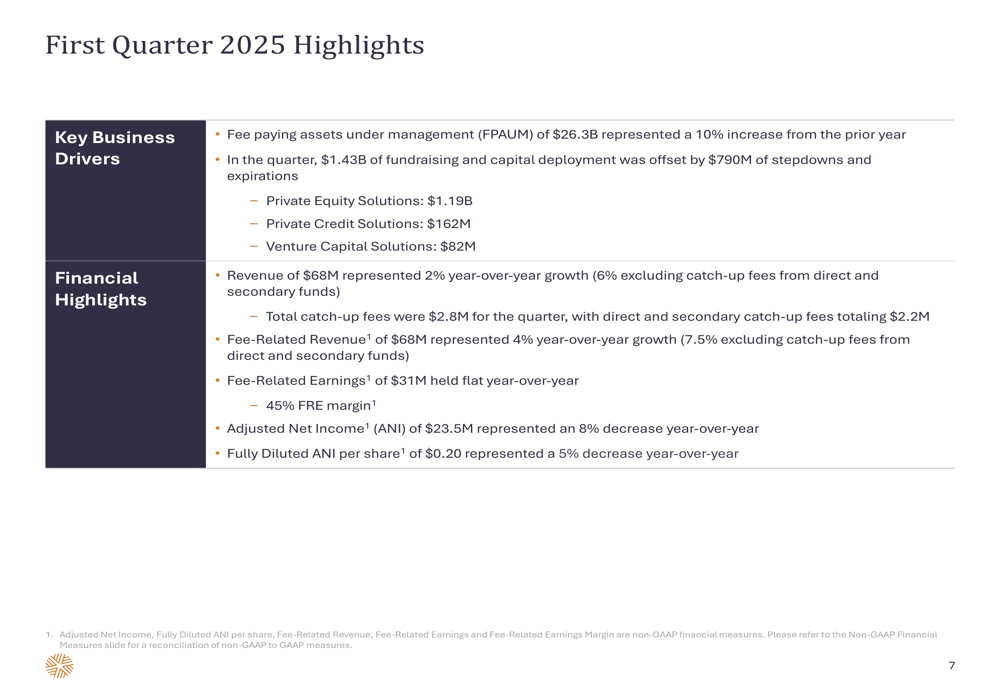

P10’s business drivers for Q1 2025 showed strong fundraising activity, with $1.43 billion raised and deployed during the quarter. This was partially offset by $790 million in stepdowns and expirations across the company’s three main investment categories.

The following chart illustrates the company’s key business drivers and financial highlights for the quarter:

Fee-related revenue increased by 4% year-over-year to $67.6 million, or 7.5% excluding catch-up fees. Total (EPA:TTEF) catch-up fees for the quarter were $2.8 million. While fee-related earnings remained flat at $31 million, adjusted net income declined by 8% to $23.5 million, with fully diluted ANI per share down 5% to $0.20.

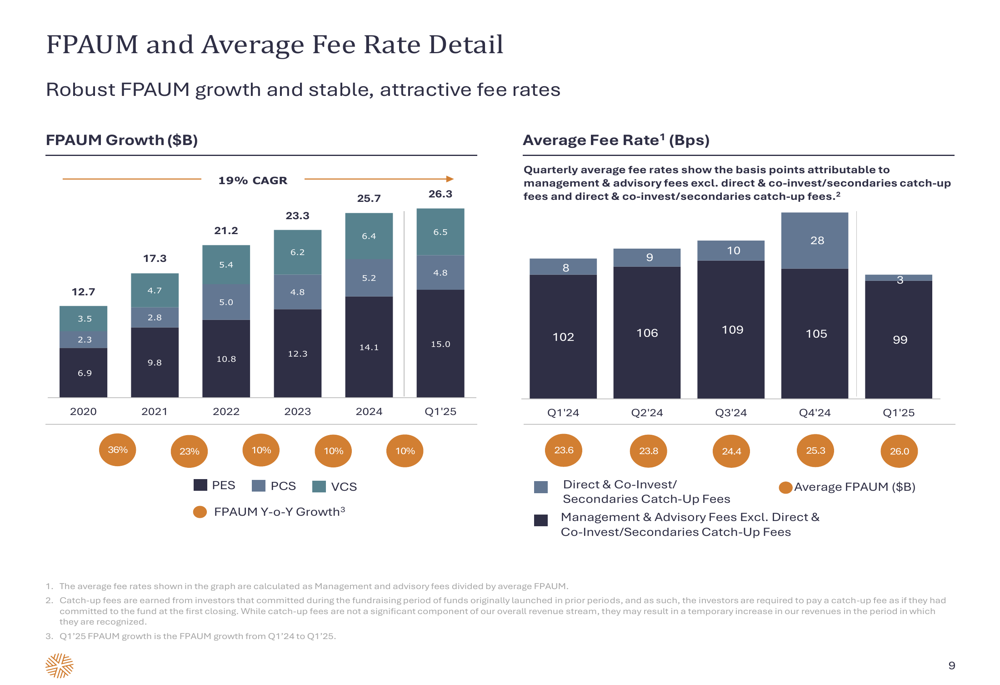

P10’s FPAUM has shown consistent growth over the past five years, with a 19% compound annual growth rate (CAGR) since 2020. However, the average fee rate has declined slightly from 102 basis points in Q1 2024 to 99 basis points in Q1 2025, as illustrated in this chart:

Strategic Initiatives

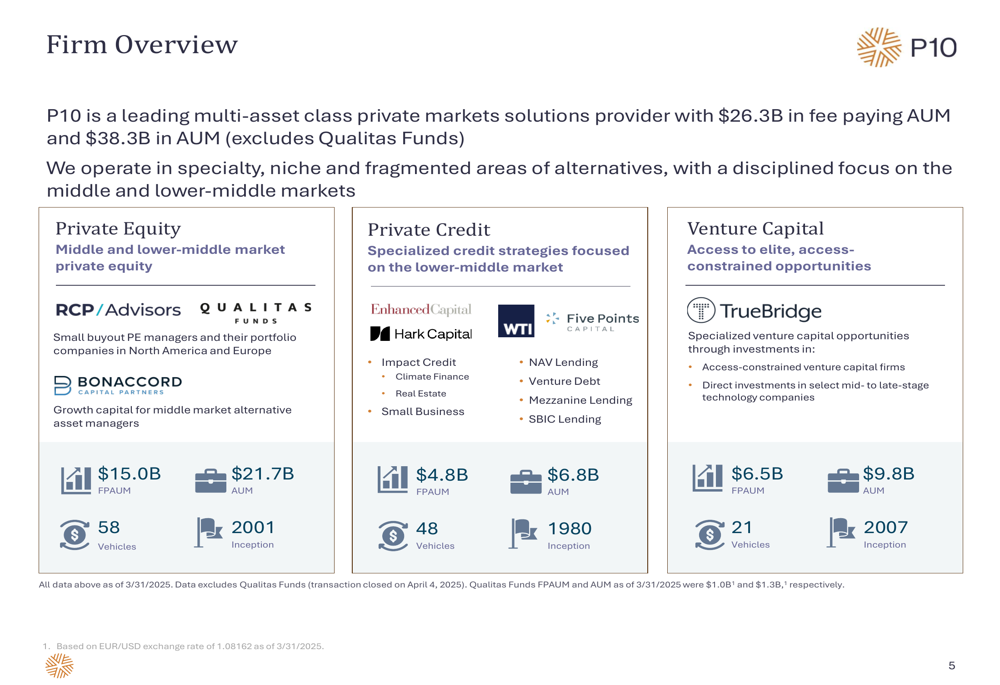

P10 continues to position itself as a leading multi-asset class private markets solutions provider, with a diversified platform across private equity, private credit, and venture capital. The firm’s overview shows its focus on specialty, niche, and fragmented areas of alternatives in the middle and lower-middle markets:

A significant milestone during the quarter was the closing of RCP Advisors’ RCP Direct V fund at approximately $994 million. Additionally, the company completed its previously announced acquisition of Qualitas Funds in April, which adds $1.0 billion in FPAUM and $1.3 billion in AUM to P10’s platform.

The company also strengthened its board with the appointment of Jennifer Glassman and Stephen Blewitt as independent directors, furthering its corporate governance objectives.

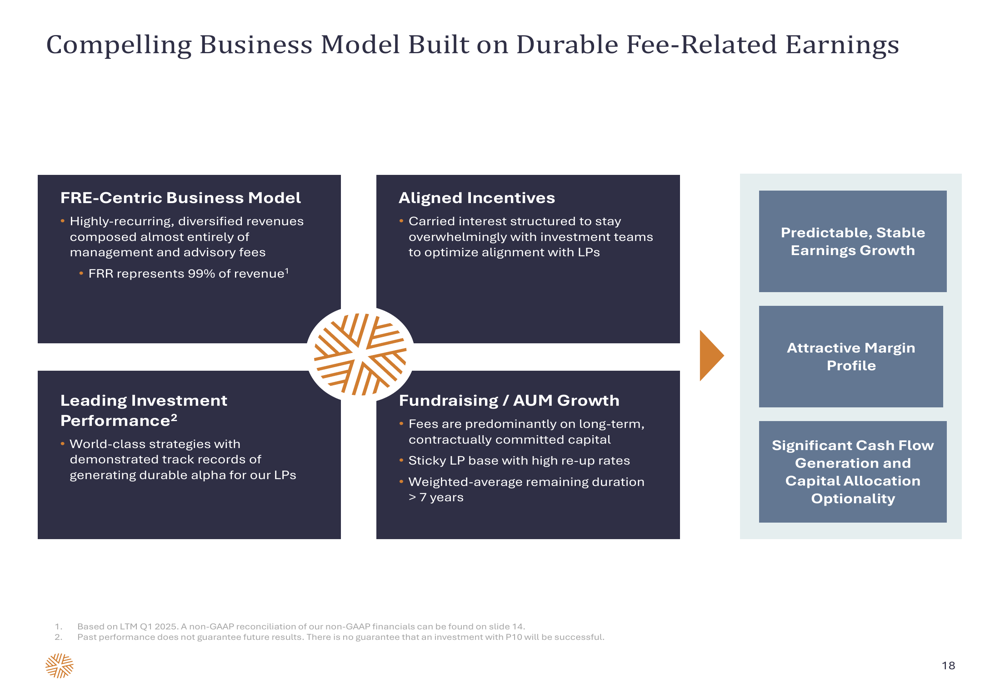

P10’s business model continues to focus on durable fee-related earnings, with highly recurring, diversified revenues primarily from management and advisory fees. The company emphasizes its aligned incentives, leading investment performance, and stable AUM growth as key components of its strategy:

Detailed Financial Analysis

On the balance sheet front, P10 declared a quarterly cash dividend of $0.0375 per share, representing a 7% increase. The company reported $355 million in outstanding debt, consisting of a $325 million term loan and $30 million drawn on its revolver. Cash and equivalents stood at $74 million.

During the quarter, P10 repurchased 1,215,106 shares at an average price of $12.31, with $28.5 million remaining under its repurchase authorization. The company has 75,816,282 Class A shares and 34,621,889 Class B shares outstanding.

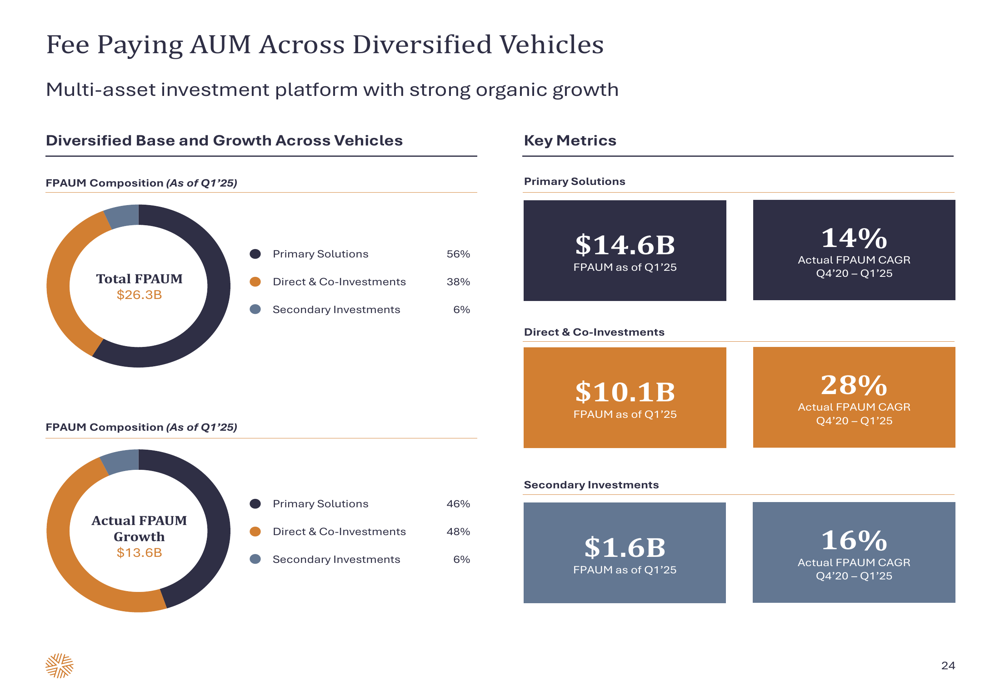

P10’s fee-paying AUM is diversified across various investment vehicles, with primary solutions making up 56% of the total $26.3 billion FPAUM, direct & co-investments 38%, and secondary investments 6%:

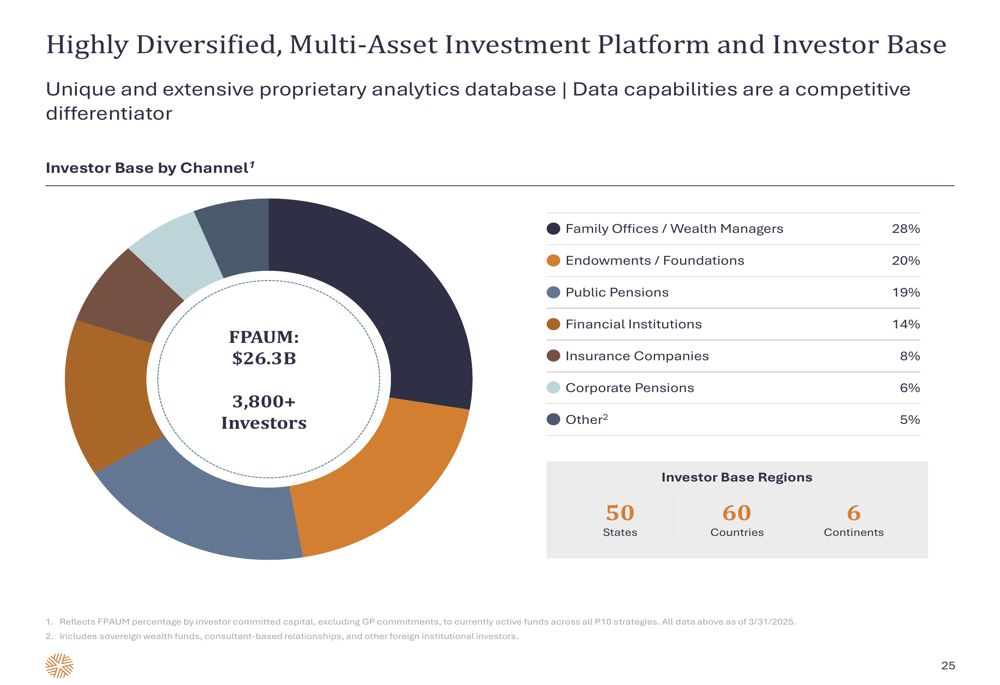

The company also boasts a highly diversified investor base spanning family offices, wealth managers, endowments, public pensions, financial institutions, insurance companies, and corporate pensions. With over 3,800 investors across 50 states, 60 countries, and 6 continents, P10 has built a global platform:

Forward-Looking Statements

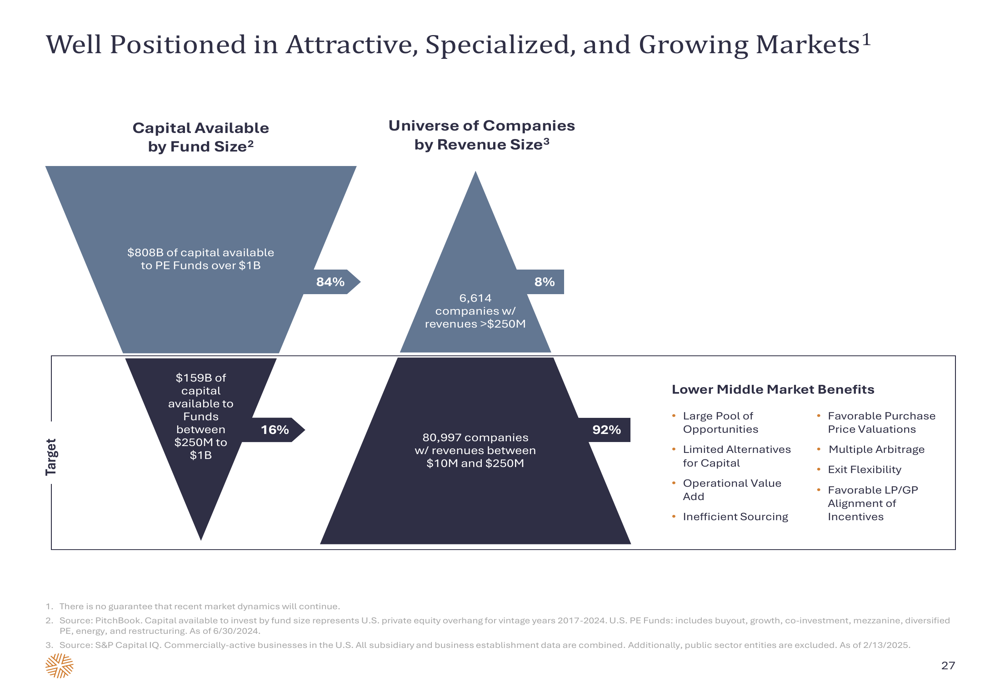

P10 believes it is well-positioned in attractive, specialized, and growing markets. The company highlights the disparity between capital availability and investment opportunities in the lower middle market, where 92% of companies (with revenues between $10M and $250M) receive only 16% of available private equity capital:

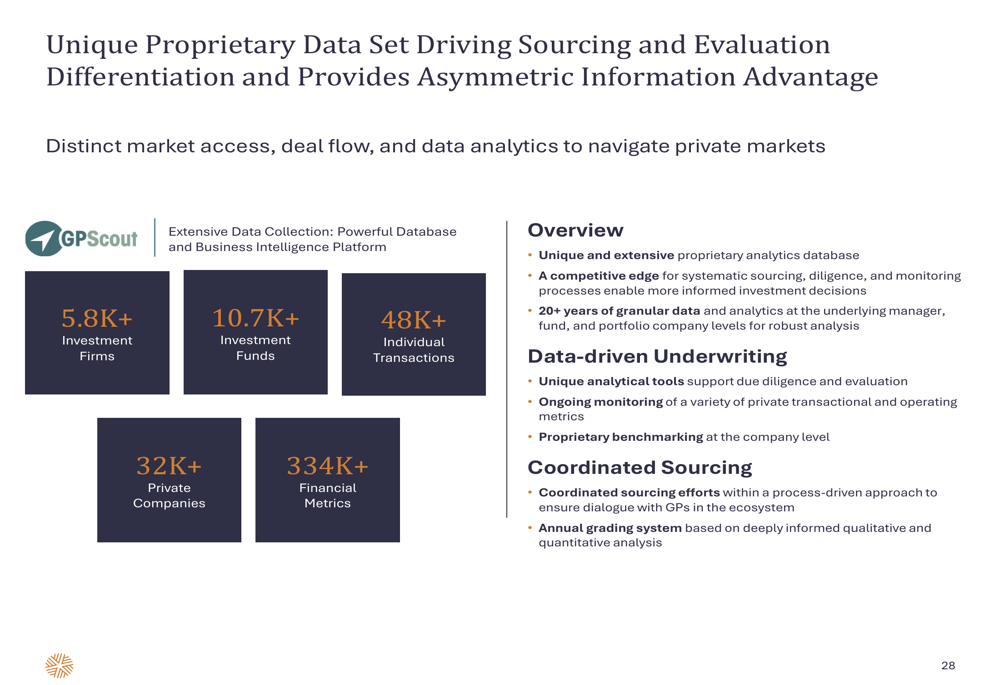

A key competitive advantage for P10 is its proprietary data set, which includes information on 5.8K+ investment firms, 10.7K+ investment funds, 48K+ individual transactions, 32K+ private companies, and 334K+ financial metrics. This extensive database provides business intelligence that drives sourcing and evaluation:

Despite the mixed financial results for Q1 2025, P10 remains committed to its long-term growth strategy, focusing on driving increased organic growth, re-accelerating M&A activity, achieving operational efficiencies, and delivering enhanced transparency to investors.

The market’s negative reaction to the earnings presentation, as evidenced by the premarket trading decline, suggests investors may have been expecting stronger financial performance or more optimistic guidance. However, the continued growth in FPAUM and strategic acquisitions indicate P10 is maintaining its focus on building a diversified alternative asset management platform for the long term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.