BofA update shows where active managers are putting money

Introduction & Market Context

Pagaya Technologies Ltd. (NASDAQ:PGY) released its second quarter 2025 earnings presentation on August 7, showing substantial revenue growth and a significant turnaround to profitability. The fintech company, which uses artificial intelligence to help financial institutions manage risk and optimize lending decisions, saw its stock surge 15.27% in premarket trading to $36.15, building on momentum from its first profitable quarter earlier this year.

The Q2 results continue Pagaya’s transformation from a loss-making growth company to a profitable enterprise, with total revenue increasing 30% year-over-year while achieving $17 million in net income compared to a $75 million loss in the same period last year.

Quarterly Performance Highlights

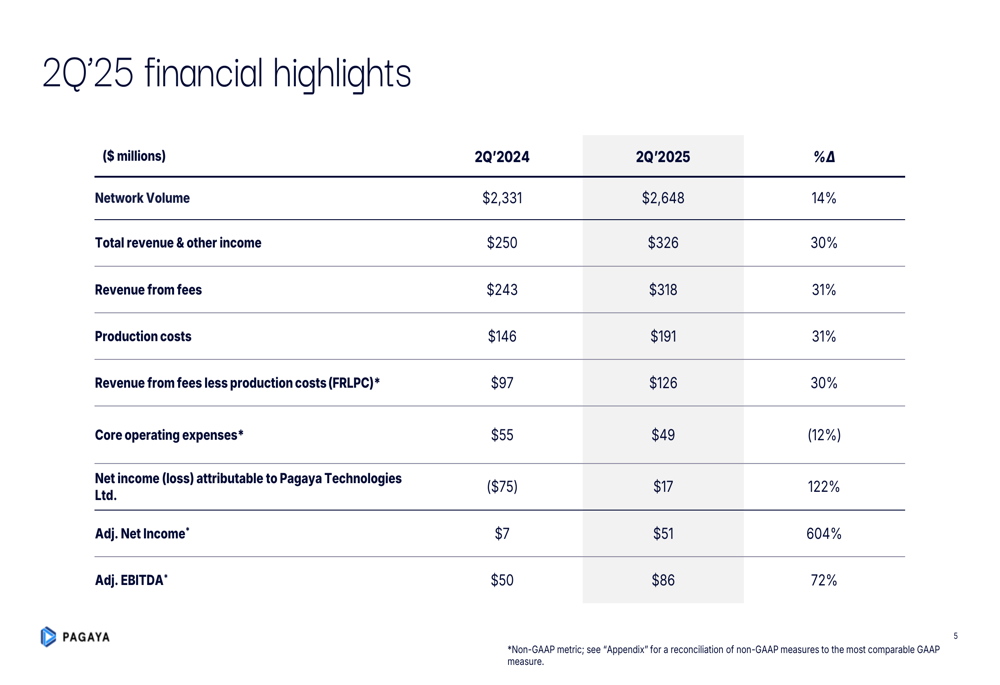

Pagaya reported impressive financial metrics across the board for Q2 2025. Network volume reached $2,648 million, representing a 14% increase from $2,331 million in Q2 2024. Total (EPA:TTEF) revenue grew by 30% to $326 million, driven by a 31% increase in fee revenue to $318 million.

As shown in the following comprehensive financial highlights table:

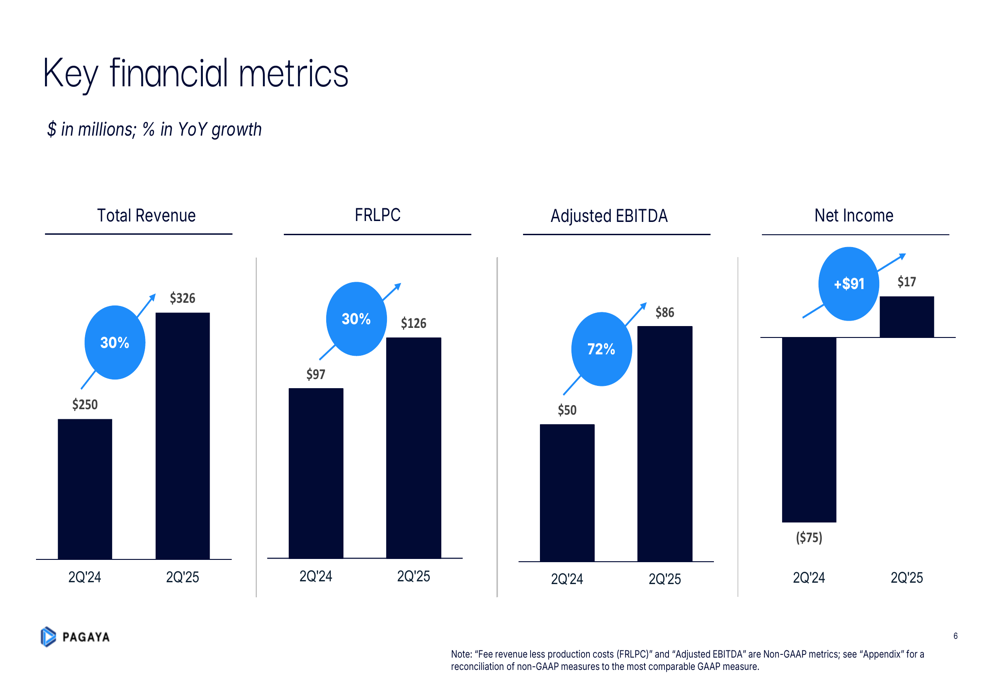

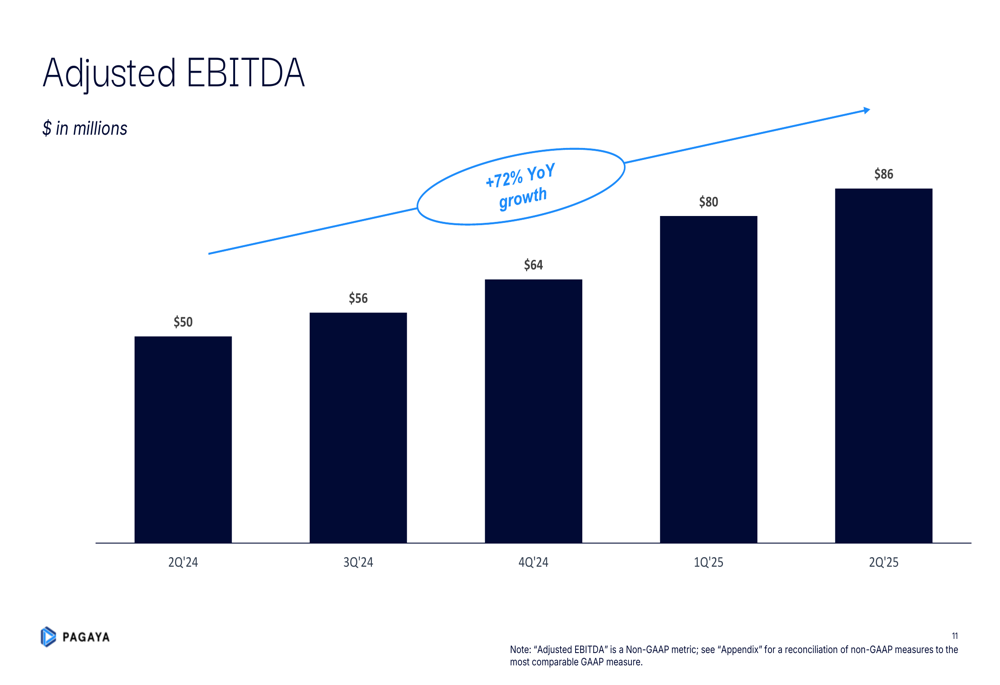

The company’s profitability metrics showed even more dramatic improvements. Adjusted net income surged by 604% to $51 million, while Adjusted EBITDA grew 72% to $86 million. Most notably, Pagaya achieved GAAP net income of $17 million, a $91 million improvement from the $75 million loss in Q2 2024.

The key financial metrics comparison visually demonstrates this transformation:

Strategic Business Evolution

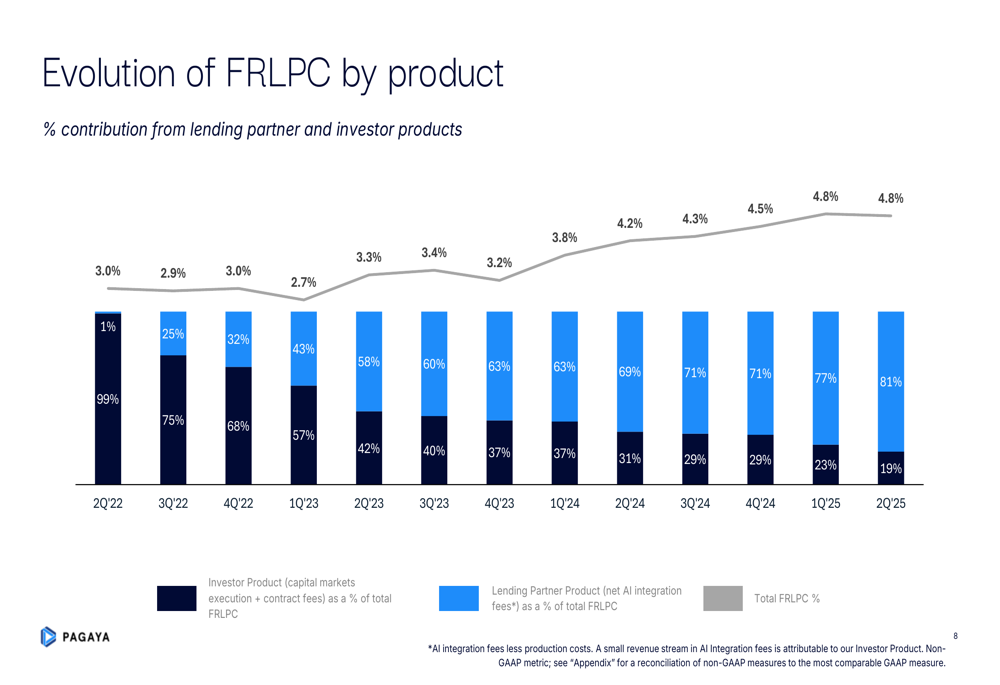

One of the most significant developments revealed in the presentation is Pagaya’s strategic shift from lending partner products to investor products. This evolution has fundamentally transformed the company’s revenue composition over the past three years.

As illustrated in the following chart, investor product FRLPC (Fee Revenue Less Production Costs) has grown from just 1% of total FRLPC in Q2 2022 to a dominant 81% in Q2 2025:

This strategic pivot has been accompanied by improvements in FRLPC as a percentage of network volume, which reached 4.8% in Q2 2025 compared to 4.2% in Q2 2024. The company is targeting an FRLPC percentage between 4.0% and 5.0% for 2025.

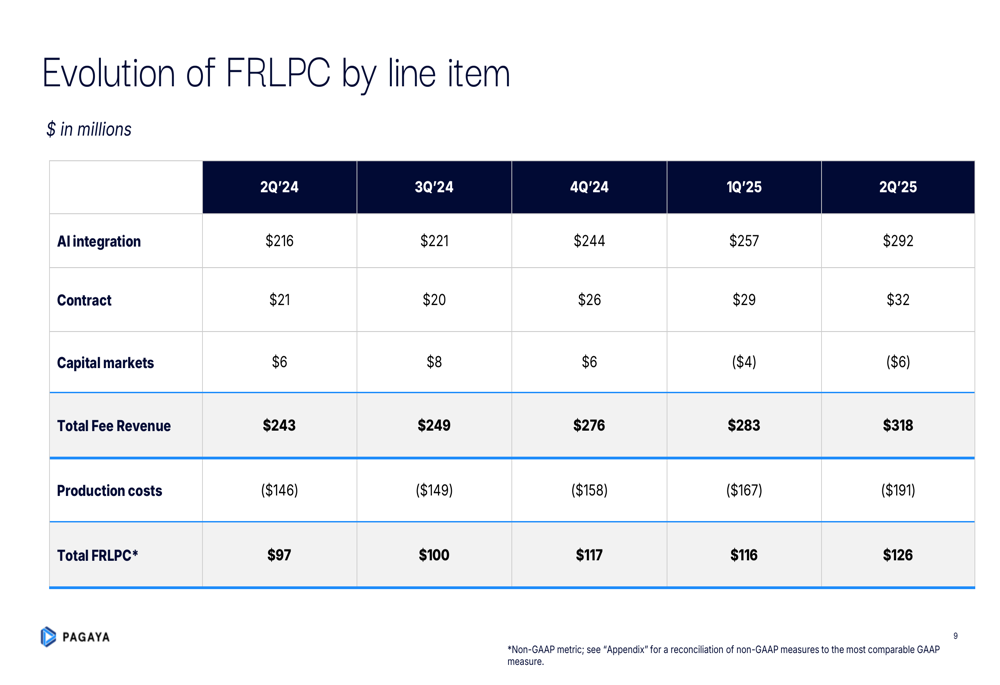

The detailed breakdown of FRLPC by line item shows how different revenue streams have evolved:

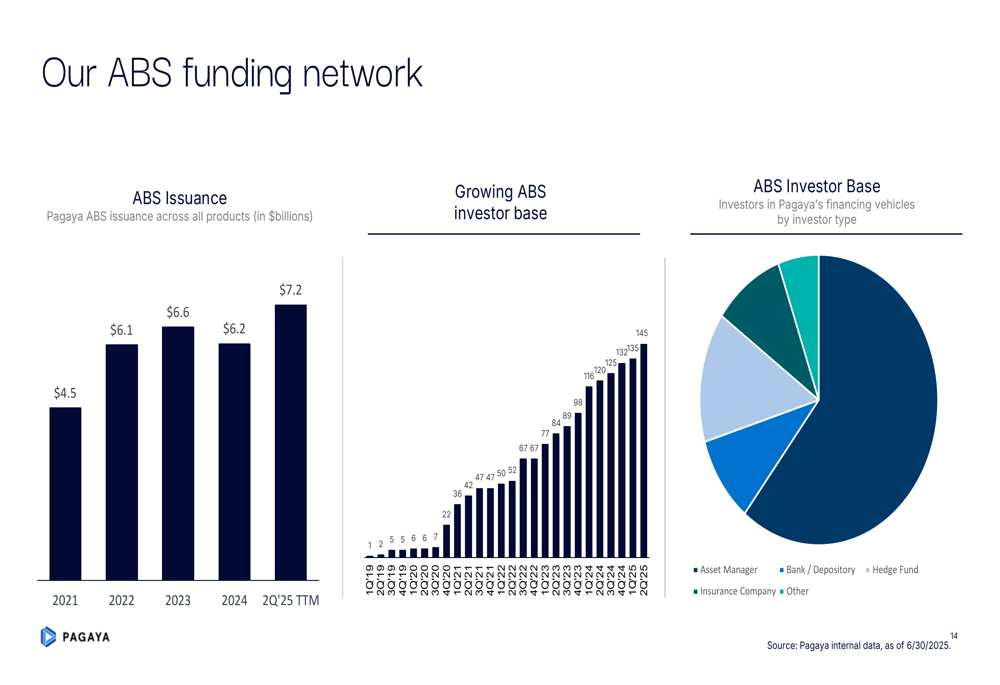

Pagaya’s funding capabilities have also strengthened, with $7.2 billion in asset-backed securities (ABS) issuance over the trailing twelve months ending Q2 2025, up from $6.2 billion in 2024. The company has diversified its ABS investor base, which now includes asset managers, banks, hedge funds, and insurance companies.

The following chart illustrates the growth in Pagaya’s ABS funding network:

Operational Efficiency Improvements

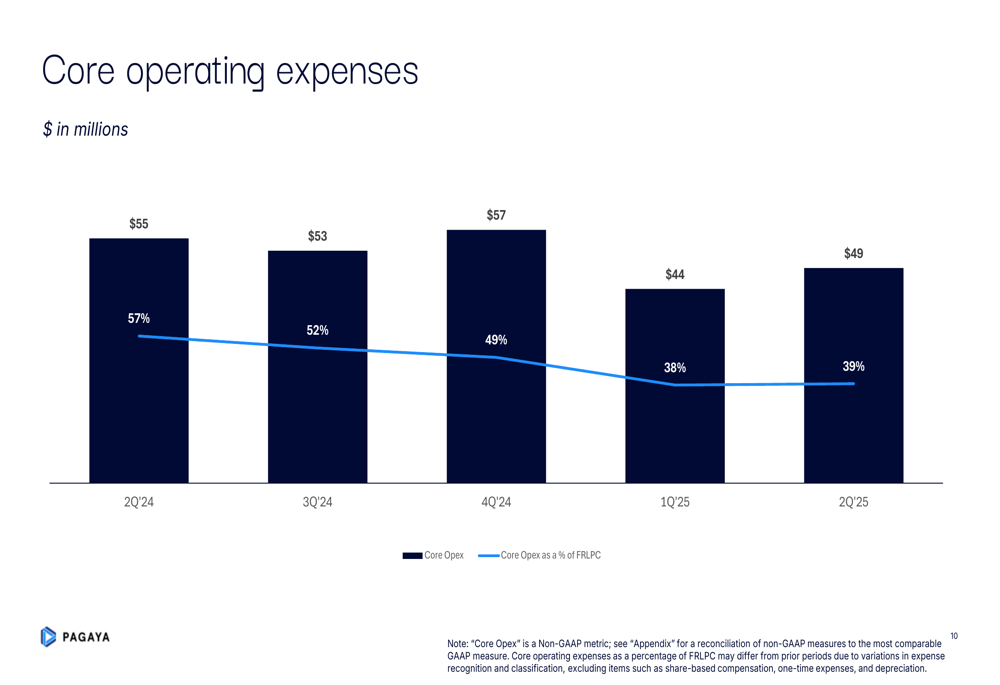

Alongside revenue growth, Pagaya has demonstrated significant operational efficiency improvements. Core operating expenses decreased by 12% year-over-year to $49 million in Q2 2025, down from $55 million in Q2 2024. More importantly, these expenses as a percentage of FRLPC improved dramatically from 57% to 39%, indicating better operating leverage.

This trend is clearly visible in the following chart:

The combination of revenue growth and cost discipline has resulted in substantial Adjusted EBITDA expansion, reaching $86 million in Q2 2025, a 72% increase from $50 million in Q2 2024:

Pagaya’s AI-driven approach continues to scale, with the company evaluating 238 billion applications in Q2 2025 while maintaining a conversion rate of approximately 1%. This massive data processing capability underscores the company’s technological advantage in credit decisioning.

Forward-Looking Statements

While the presentation did not include specific updated guidance for the remainder of 2025, Pagaya’s Q1 earnings call had previously set ambitious targets for the full year, including network volume between $9.5 billion and $11 billion and total revenue ranging from $1.175 billion to $1.3 billion.

The Q2 results appear to position the company well to achieve these targets, with network volume for the first half of 2025 already exceeding $5 billion and revenue on pace to reach the projected range.

Pagaya’s sensitivity analysis for investments in loans and securities indicates the company is preparing for potential stress scenarios, with management estimating the impact of 10-30%+ reductions in expected cash flows. This prudent approach to risk management may help insulate the company from potential economic headwinds.

The company’s transformation from a loss-making entity to a profitable business appears to be gaining momentum, with Q2 2025 representing another significant step in Pagaya’s evolution. Investors have responded positively to these developments, as evidenced by the substantial premarket stock price increase following the release of these results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.