US stock futures inch lower after Wall St marks fresh records on tech gains

Introduction & Market Context

PageGroup PLC (LSE:PAGE) released its Q2 and H1 2025 trading update on July 10, showing continued revenue pressure amid challenging global recruitment markets. The company’s shares rose 1.27% to 271.4 following the presentation, suggesting investors had already priced in the challenging conditions.

The global recruitment firm reported a 10.5% decline in constant currency gross profit for Q2, as ongoing market uncertainty and tariff-related concerns continued to impact hiring activity across most regions. Despite these headwinds, the company highlighted bright spots in the US and parts of Asia, while European markets faced more significant challenges.

Quarterly Performance Highlights

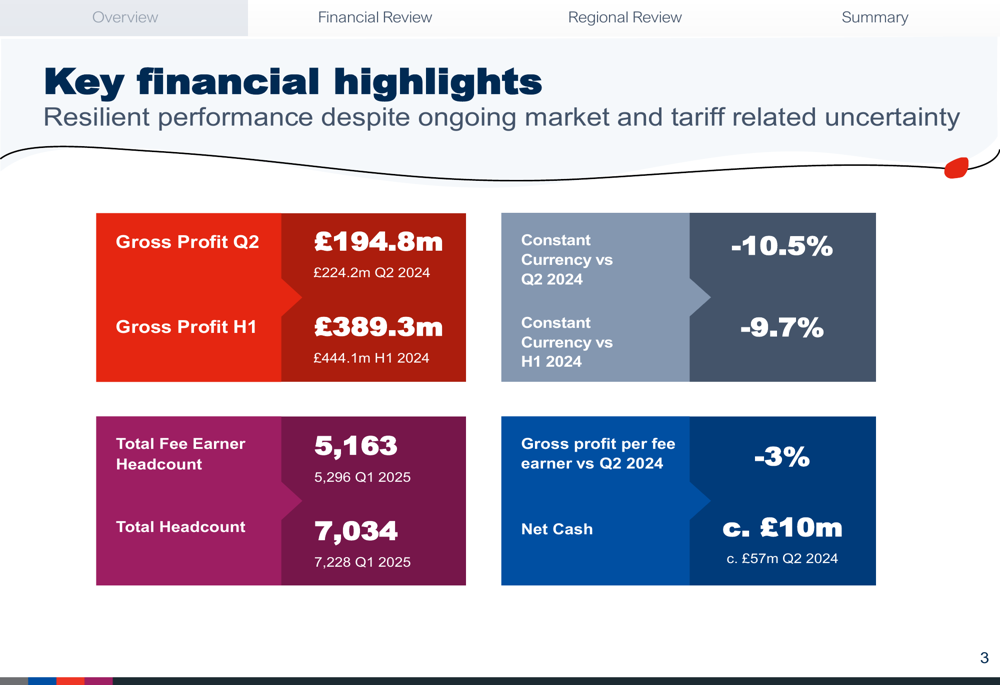

PageGroup reported Q2 2025 gross profit of £194.8 million, down 13.1% on a reported basis and 10.5% in constant currency compared to Q2 2024. For the first half of 2025, gross profit reached £389.3 million, representing a 9.7% constant currency decline from H1 2024.

As shown in the following financial highlights slide, the company’s net cash position deteriorated significantly to approximately £10 million, compared to £57 million in Q2 2024, largely due to the £37 million final dividend payment made in June:

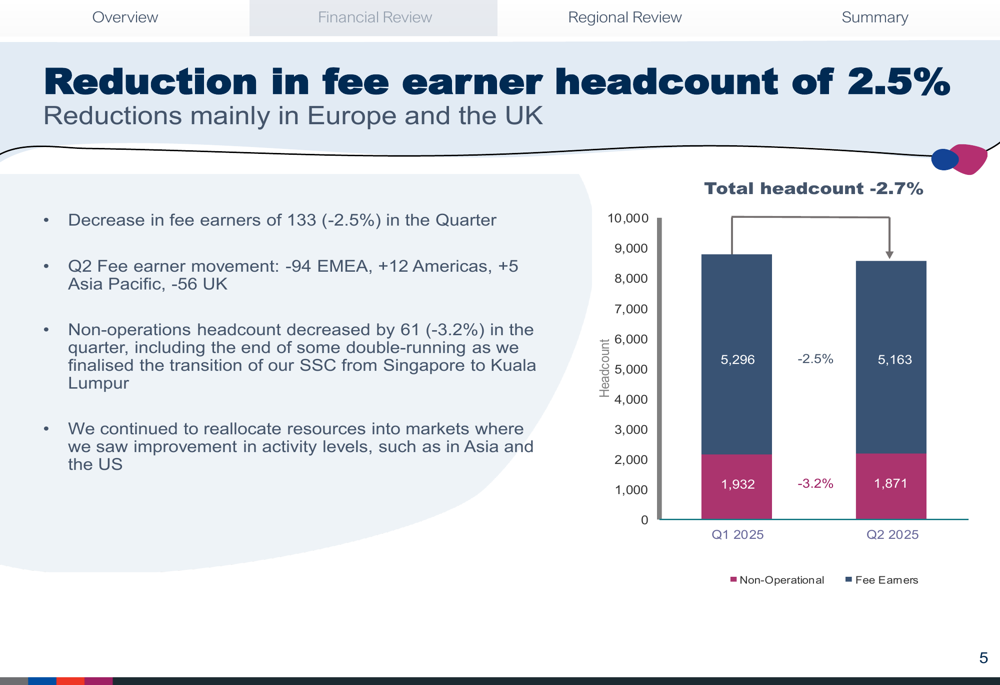

The company continued its strategic headcount reduction, with fee earner headcount decreasing by 133 (-2.5%) during the quarter to 5,163. Total (EPA:TTEF) headcount fell by 2.7% to 7,034. The reductions were primarily concentrated in Europe and the UK, reflecting the more challenging conditions in these markets.

As illustrated in the following headcount chart, both fee earner and non-operational staff numbers were reduced:

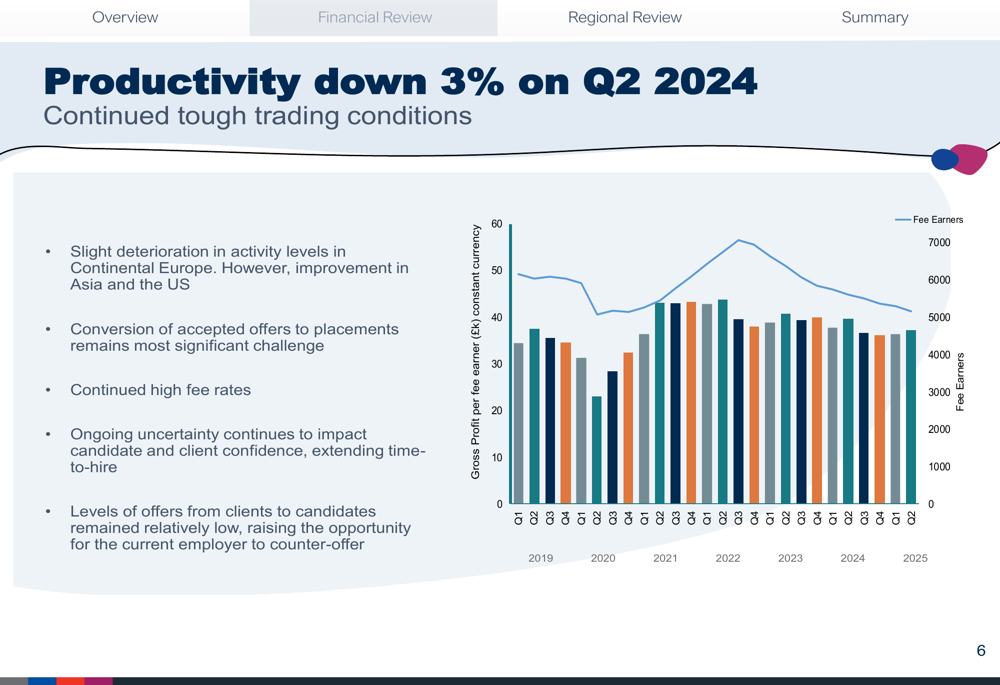

Productivity, measured as gross profit per fee earner, declined by 3% compared to Q2 2024. The company cited continued tough trading conditions, with the conversion of accepted offers to placements remaining the most significant challenge. Despite this, fee rates remained high, indicating the company has maintained pricing power.

Regional Performance Analysis

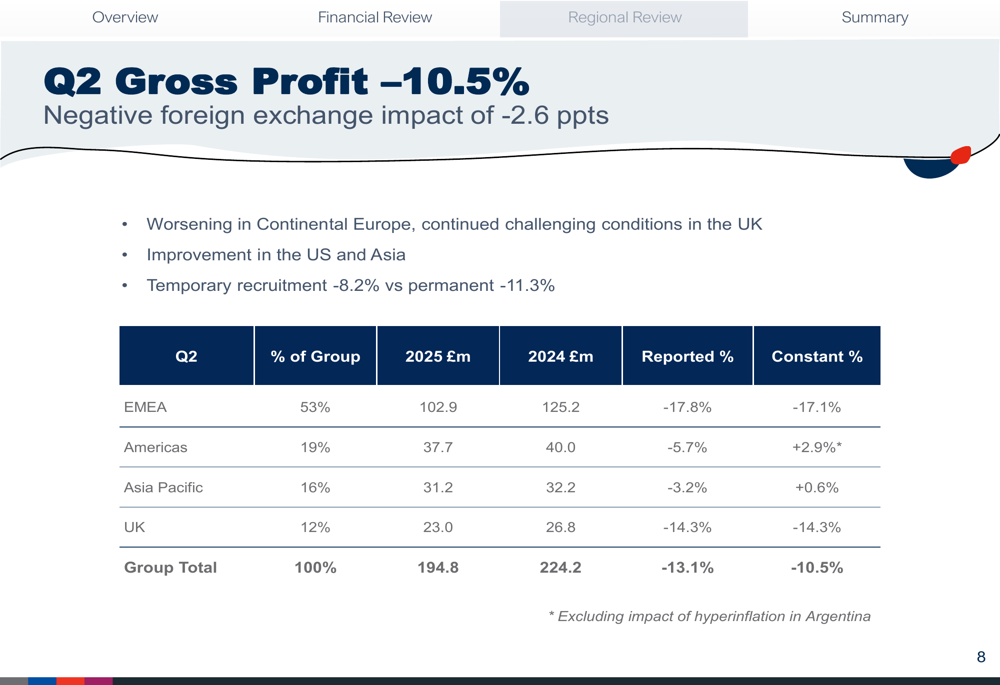

PageGroup’s performance varied significantly by region, with the Americas and Asia Pacific showing signs of improvement while Europe and the UK continued to struggle. The following chart provides a comprehensive breakdown of gross profit by region:

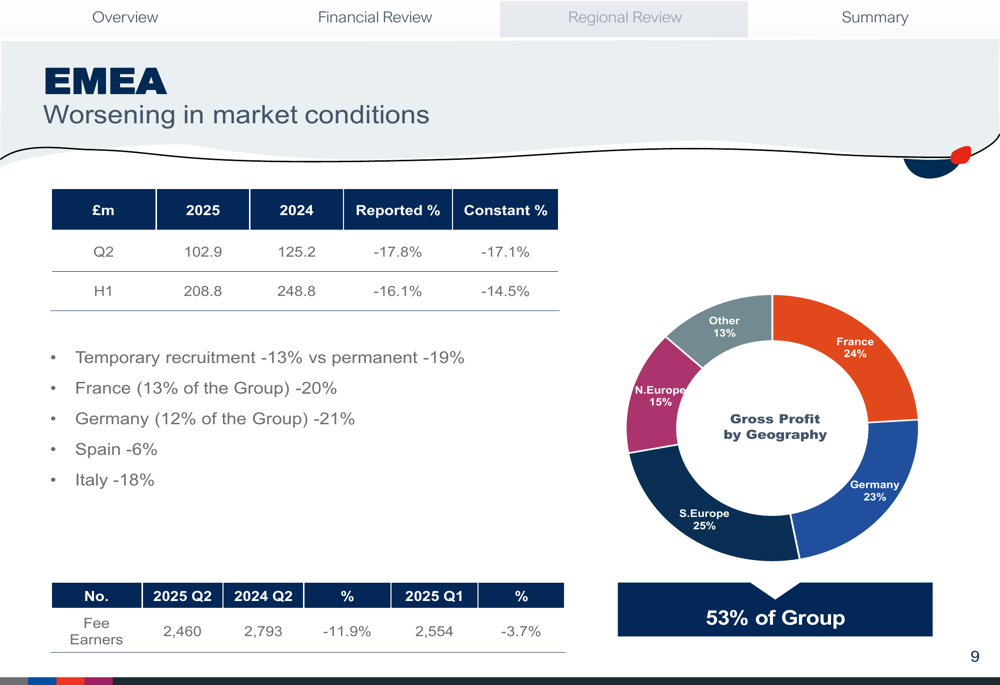

EMEA, which represents 53% of the group’s gross profit, experienced the steepest decline at 17.1% in constant currency. France (-20%) and Germany (-21%), which together account for nearly half of the EMEA region, were particularly hard hit. The company cited worsening market conditions throughout the region as the primary factor.

In contrast, the Americas region, representing 19% of group profit, showed a 2.9% increase in constant currency (excluding the impact of hyperinflation in Argentina). This growth was driven by a strong 14% increase in the US market, which marked its third consecutive quarter of growth. Latin America, however, declined by 9%.

Asia Pacific (16% of group profit) showed early signs of recovery, with a modest 0.6% increase in constant currency. Within the region, performance was mixed: Greater China declined by 5% (with Mainland China down 17% but Hong Kong up 16%), while South East Asia (+10%) and India (+13%) delivered strong growth. Japan remained flat, while Australia declined by 13%.

The UK market (12% of group profit) continued to face challenges, with gross profit down 14.3%. The company attributed this to subdued levels of client and candidate confidence in the region.

Strategic Initiatives

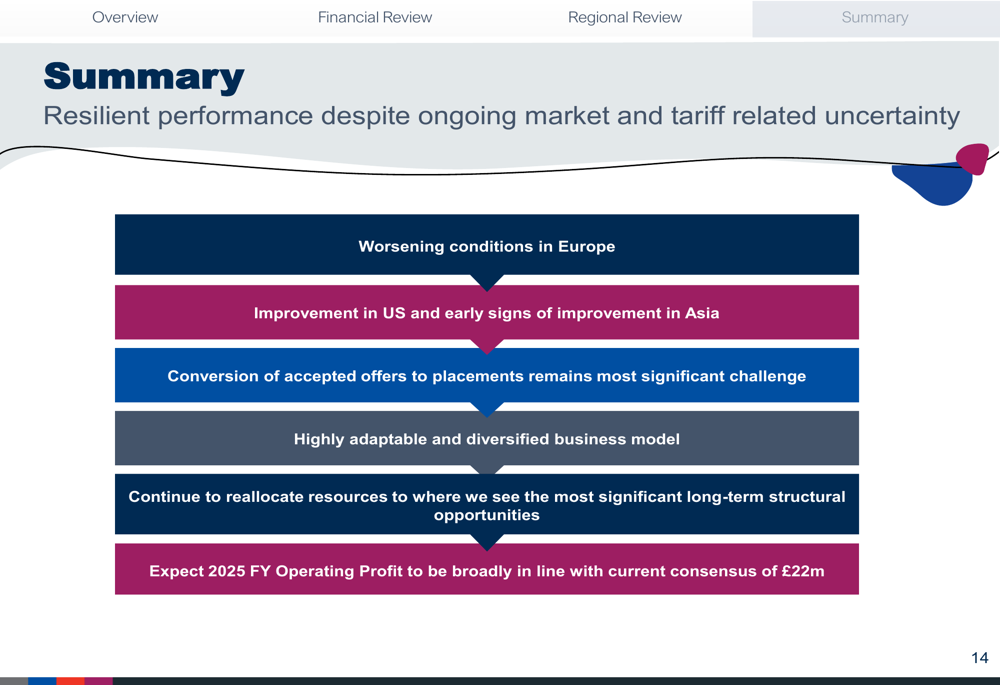

PageGroup emphasized its "highly adaptable and diversified business model" as a key strength in navigating the challenging market conditions. The company is continuing to reallocate resources toward markets with the strongest long-term structural opportunities, particularly the US, which has shown consistent improvement.

The ongoing headcount reduction strategy reflects this adaptive approach, with the company focusing on maintaining productivity while rightsizing operations in underperforming regions. According to the earnings call, PageGroup plans to cut an additional 120-150 fee earners per quarter as part of this strategy.

The following summary slide highlights the company’s key strategic focus areas:

Forward-Looking Statements

Despite the challenging Q2 results, PageGroup maintained its full-year outlook, expecting 2025 operating profit to be "broadly in line with current consensus of £22 million." This suggests management believes the worst of the market downturn may be behind them, particularly given the improving conditions in the US and parts of Asia.

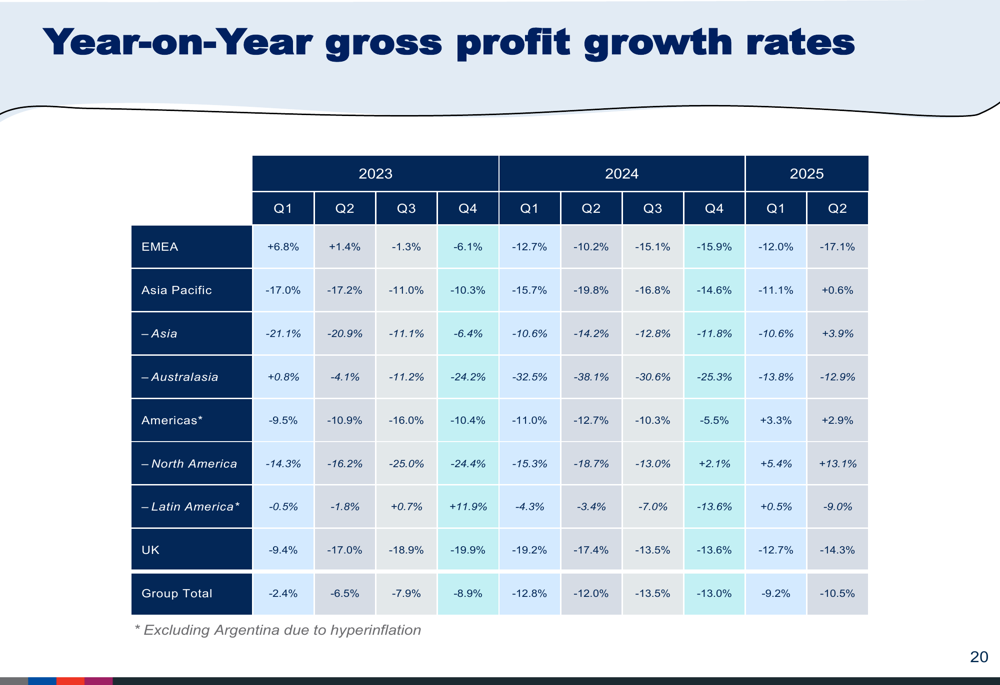

The company’s year-on-year gross profit growth rates provide important context for understanding the current trajectory:

This historical data shows that while most regions continue to experience year-on-year declines, the rate of decline has begun to moderate in several key markets, particularly in Asia Pacific and North America, which have returned to positive growth in recent quarters.

CFO Kelvin Stagg characterized the quarter as a "resilient performance despite ongoing market uncertainty," while acknowledging the continued challenges in converting accepted offers to placements. The company expects its net cash position to improve to £60-70 million by year-end, following the significant reduction seen in Q2 due to dividend payments.

As PageGroup navigates through this challenging period, investors will be closely watching for signs of broader market recovery and the company’s ability to capitalize on growth opportunities in its stronger regional markets while effectively managing costs in underperforming areas.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.