Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Paladin Energy Ltd (ASX:PDN) released its June 2025 quarter presentation on July 23, showcasing a significant production increase at its Langer Heinrich Mine (LHM) in Namibia, despite facing headwinds from lower realized uranium prices. The company’s operational achievements come amid a uranium market that has seen substantial price appreciation over the past five years, with spot prices up 116% and term prices up 125%.

The quarter marks the end of Paladin’s 2025 fiscal year, with the company now setting ambitious production targets for FY2026 as it approaches the completion of its operational ramp-up at LHM. The presentation follows a Q3 earnings report that saw the company’s stock surge despite revenue missing forecasts, suggesting investor confidence in Paladin’s operational trajectory.

Quarterly Performance Highlights

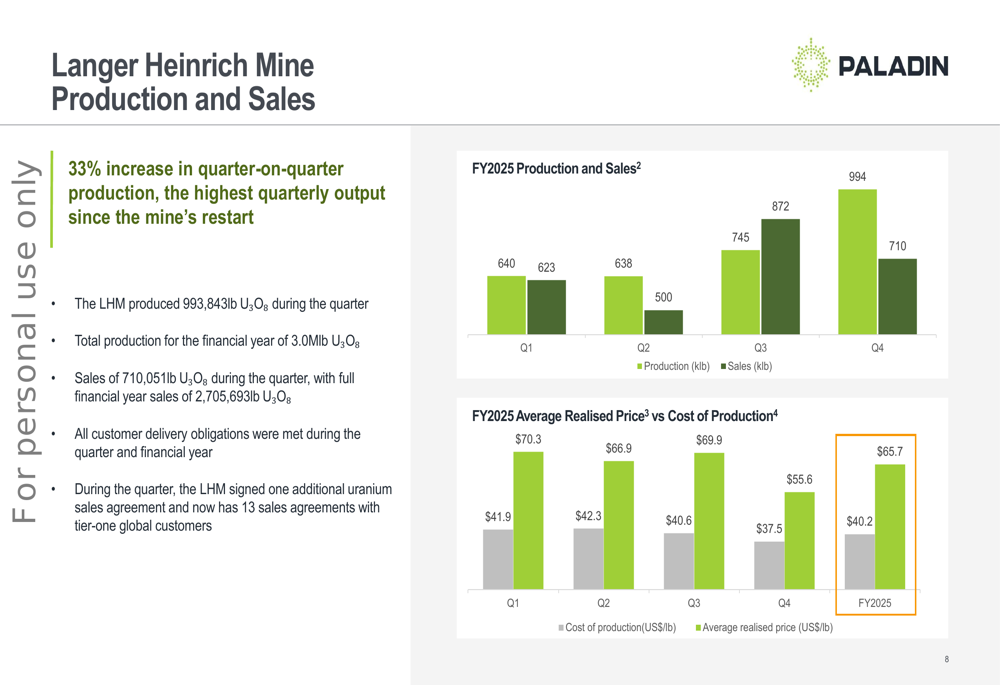

Paladin achieved a 33% quarter-on-quarter increase in uranium production at LHM, reaching 993,843 pounds of U3O8 in Q4 FY2025. This significant jump helped the company achieve a total annual production of 3.02 million pounds for the full fiscal year. The quarter also saw the highest crusher circuit throughput in the history of LHM operations.

As shown in the following quarterly production and sales chart:

While production surged, sales volume was lower at 710,051 pounds for the quarter, compared to 872,435 pounds in Q3. More concerning was the decline in average realized price, which fell to US$55.6 per pound in Q4 from US$69.9 in the previous quarter. This price drop was partially offset by continued improvement in production costs, which decreased to US$37.5 per pound from US$40.6 in Q3.

The processing plant demonstrated strong performance metrics, with plant recovery rate maintaining at 87% despite the significant increase in throughput:

Detailed Financial Analysis

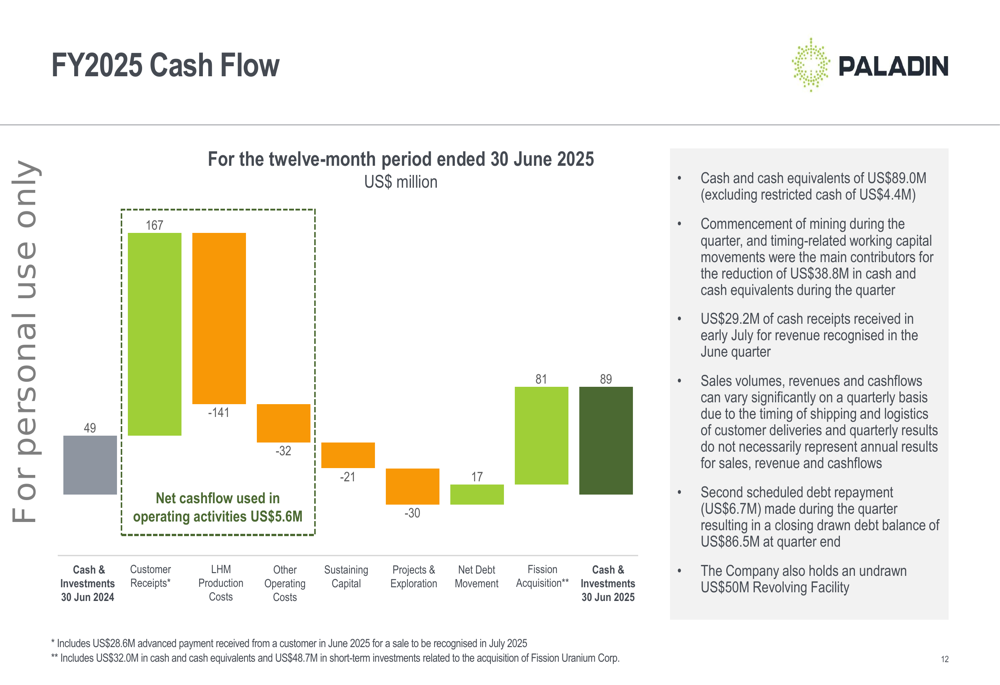

Paladin ended the fiscal year with US$89.0 million in cash and cash equivalents, excluding restricted cash of US$4.4 million. This represents an improvement from the US$49 million reported at the end of June 2024. The company also maintains an undrawn US$50 million revolving debt facility, providing additional financial flexibility.

The following cash flow waterfall chart illustrates the company’s financial movements throughout FY2025:

For the twelve-month period ended June 30, 2025, Paladin reported net cash used in operating activities of US$5.6 million. Customer receipts of US$167 million were largely offset by LHM production costs of US$141 million and other operating costs of US$32 million. The acquisition of Fission Uranium Corp (TSX:FCU) contributed US$81 million to the company’s cash position.

This financial performance represents a mixed picture when compared to the Q3 2025 earnings report, which showed revenue of US$60 million against a forecast of US$79 million. The presentation does not directly address this revenue shortfall, though the declining realized prices in Q4 suggest continued revenue challenges.

Strategic Initiatives & Outlook

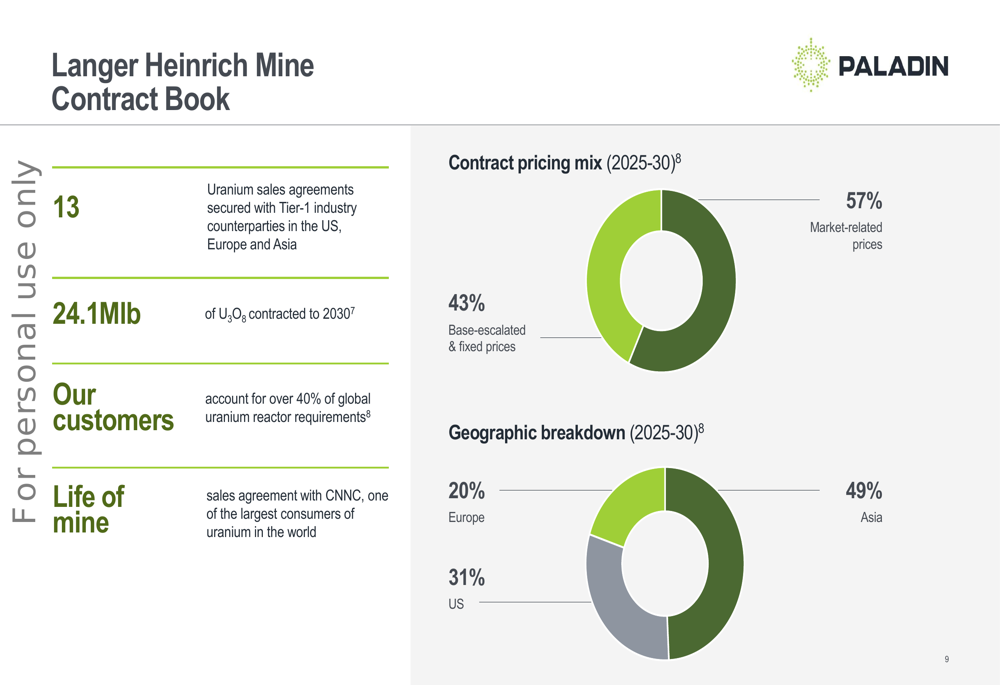

Paladin has established a robust contract book with 13 uranium sales agreements with Tier-1 industry counterparties across the US, Europe, and Asia. These customers reportedly account for 40% of global uranium reactor requirements, providing a stable foundation for future sales.

The contract pricing mix and geographic distribution are illustrated below:

The company has 24.1 million pounds of U3O8 contracted through 2030, with a pricing mix that includes 57% market-related prices and 43% base-escalated and fixed prices. This balanced approach provides some protection against market volatility while allowing participation in potential price increases.

On the operational front, mining commenced in April with the G2A pit serving as the primary source of freshly mined ore. Mining operations for FY2026 are expected to concentrate in the G-pit area, with minor activity planned for the F and J pits later in the financial year.

Forward-Looking Guidance

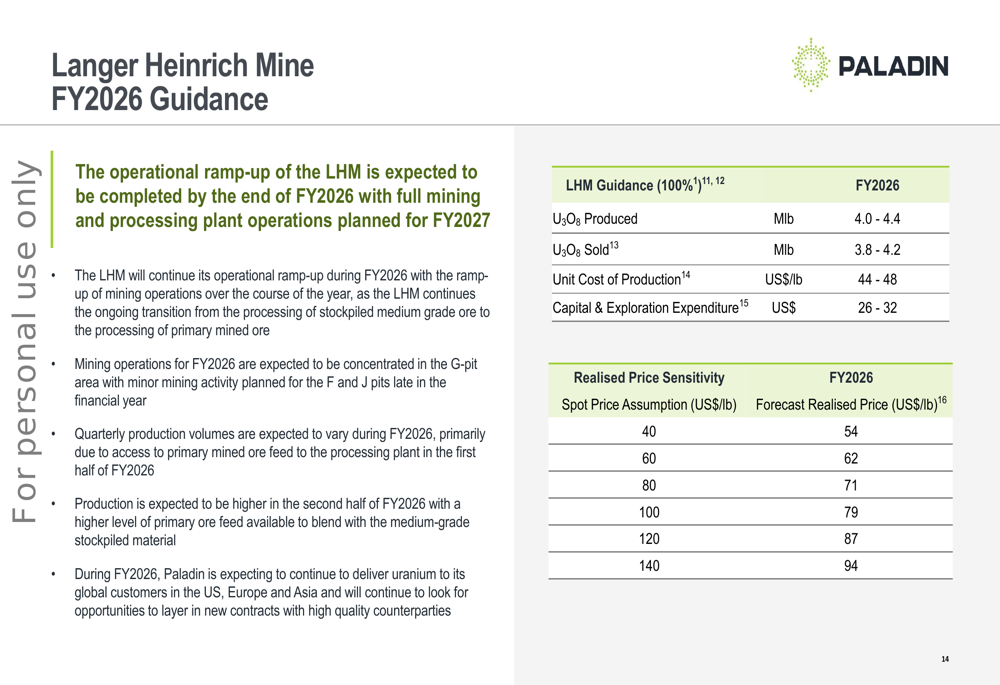

Paladin has provided ambitious guidance for FY2026, targeting production of 4.0-4.4 million pounds of U3O8, representing a potential increase of up to 46% from FY2025 levels. Sales are projected at 3.8-4.2 million pounds.

The detailed FY2026 guidance is presented below:

Unit cost of production is expected to increase to US$44-48 per pound, up from the FY2025 average of US$40.2. This projected cost increase likely reflects the transition to full mining operations, as the company notes that the operational ramp-up of LHM is expected to be completed by the end of FY2026.

The company also provided a realized price sensitivity analysis, showing how different spot price assumptions would affect realized prices. At a spot price of US$80 per pound, Paladin projects a realized price of US$71 per pound, reflecting the impact of its contract mix.

Production volumes are expected to vary quarterly during FY2026, with higher production anticipated in the second half as more primary ore feed becomes available to blend with medium-grade stockpiled material. The company commenced FY2026 with an estimated 2.2 million tonnes of stockpiled medium-grade ore and approximately 49% of its planned mining fleet capacity in operation, with the remaining fleet scheduled for delivery in late 2025.

In leadership news, Paul Hemburrow has been appointed Managing Director and Chief Executive Officer, effective September 1, 2025, signaling continuity in the company’s strategic direction as it completes its operational ramp-up phase and moves toward full production capacity.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.