Asia stocks surge as tech extends rebound, Dec rate cut bets grow

Palo Alto Networks (NASDAQ:PANW) reported strong fourth-quarter fiscal year 2025 results on August 18, exceeding guidance across key metrics while announcing plans to expand into identity security through its acquisition of CyberArk. The cybersecurity leader demonstrated accelerating revenue growth and continued margin expansion as customers increasingly adopt its platform approach.

Quarterly Performance Highlights

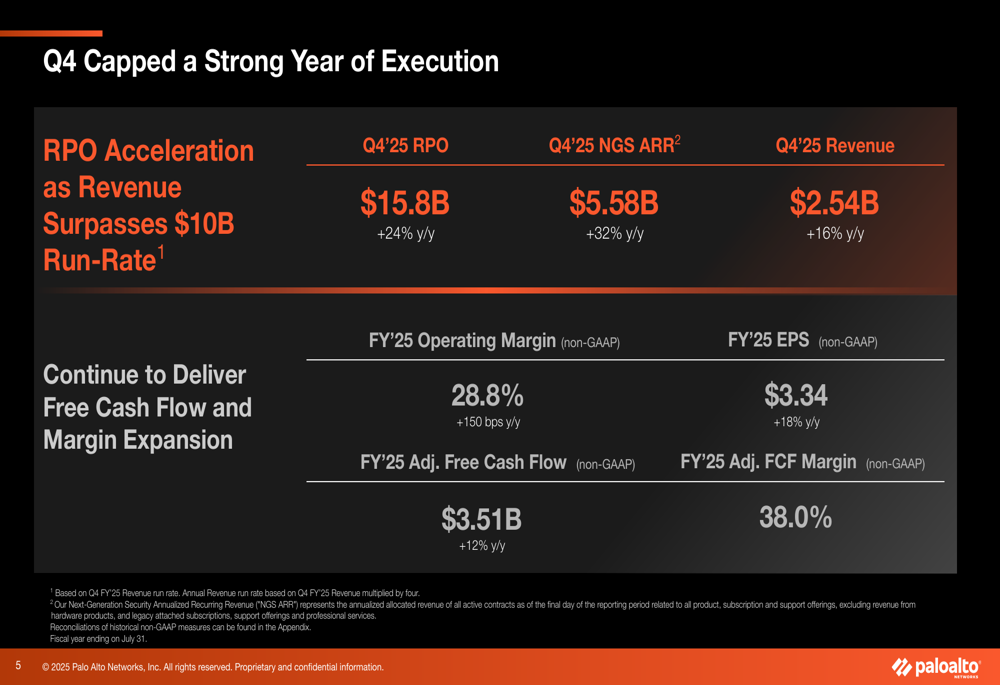

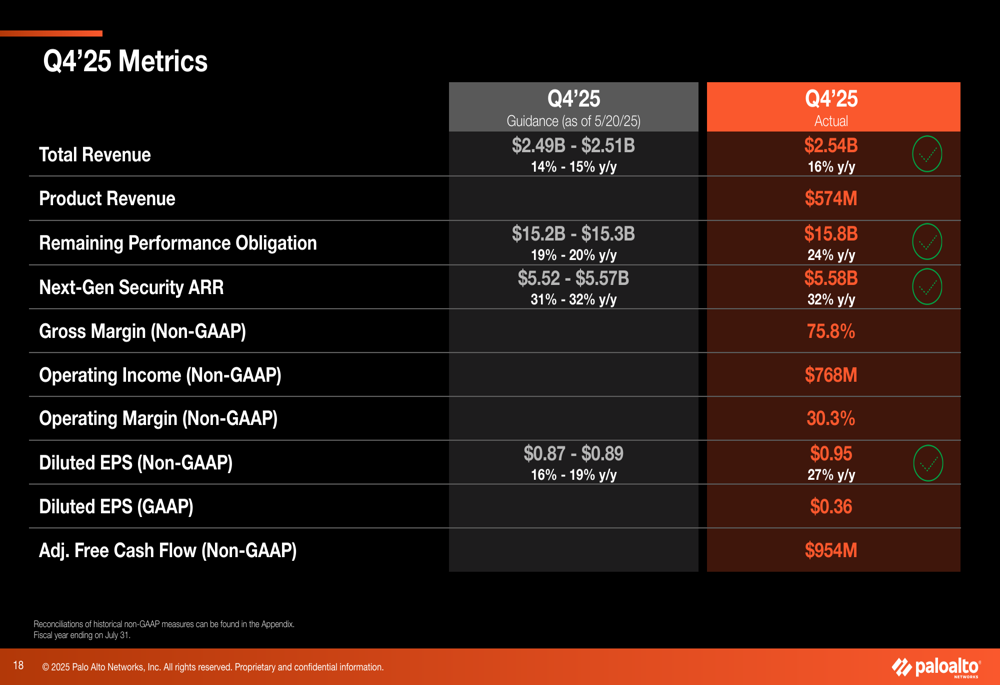

Palo Alto Networks delivered robust financial results for Q4 FY25, with revenue reaching $2.54 billion, representing 16% year-over-year growth and exceeding the company's guidance range of $2.49-$2.51 billion. This marks an acceleration from the 15% growth reported in the previous quarter.

The company's Remaining Performance Obligation (RPO) grew 24% year-over-year to $15.8 billion, while Next-Generation Security Annual Recurring Revenue (NGS ARR) increased 32% to $5.58 billion. Both metrics surpassed the company's guidance.

As shown in the following summary of key financial metrics:

Non-GAAP earnings per share came in at $0.95, significantly above the guidance range of $0.87-$0.89 and representing 27% year-over-year growth. The company maintained strong profitability with a non-GAAP operating margin of 30.3% for the quarter and 28.8% for the full fiscal year.

The comparison between guidance and actual results demonstrates the company's ability to exceed expectations:

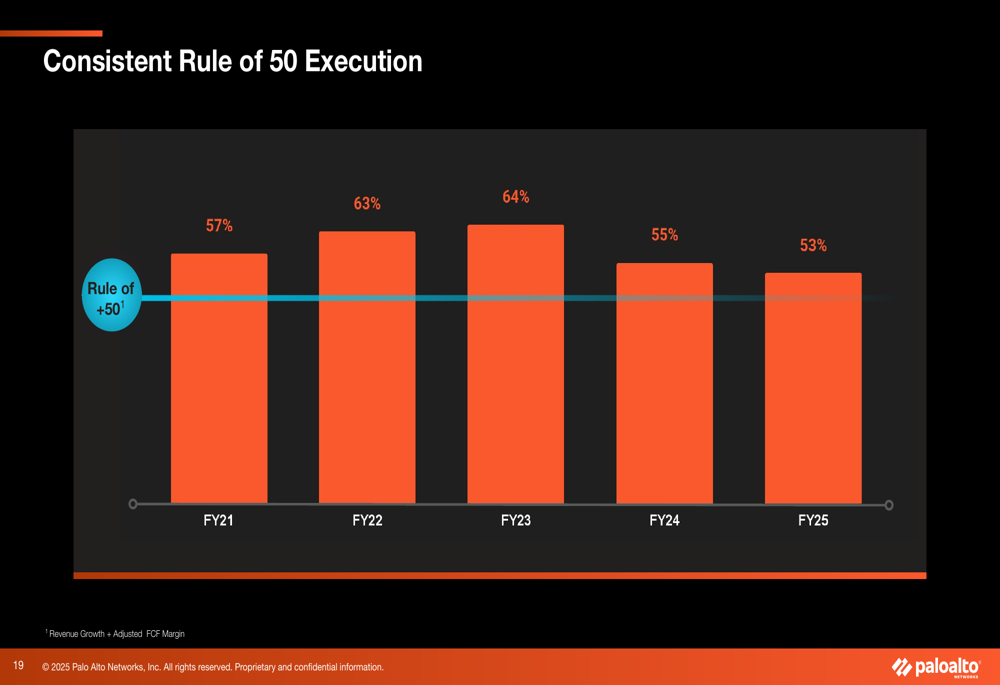

Palo Alto Networks has consistently achieved the "Rule of 50" (Revenue Growth + Adjusted FCF Margin) over the past five fiscal years, with FY25 delivering a combined score of 53%. This reflects the company's balanced approach to growth and profitability.

Strategic Initiatives

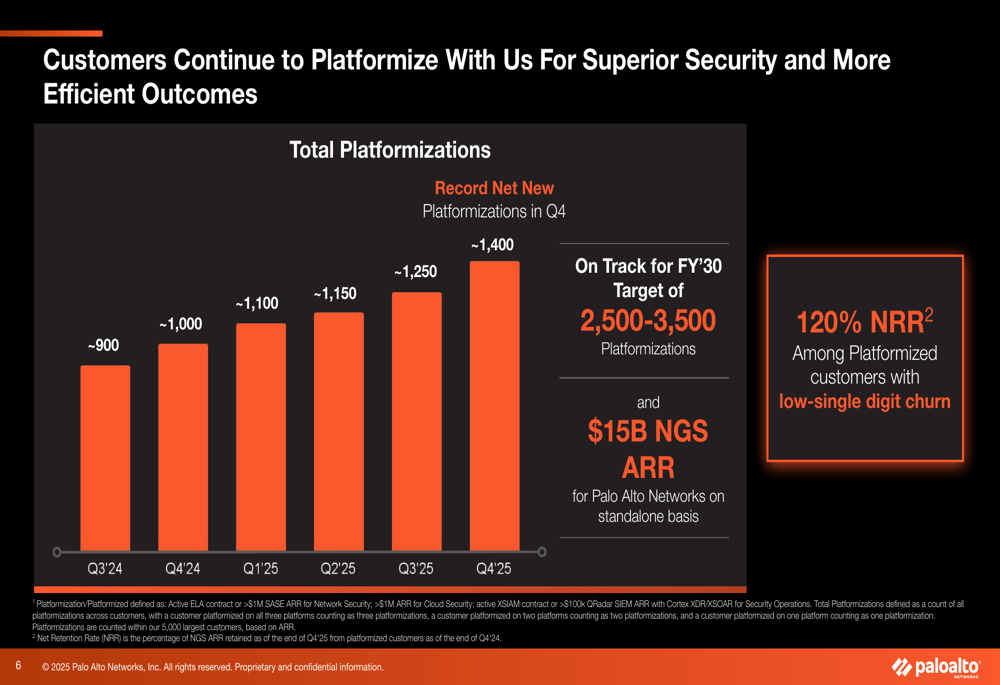

A key driver of Palo Alto Networks' success has been its platformization strategy, which focuses on consolidating customers' security needs across its portfolio. The number of platformized customers has grown steadily, reaching approximately 1,400 in Q4 FY25, up from around 900 in Q3 FY24.

As illustrated in the following chart tracking platformization growth:

These platformization efforts have resulted in significant large deal wins. The company highlighted several major customer wins in Q4, including a $111 million deal with a global consulting firm, a $61 million deal with a global financial services firm, and a $33 million deal with a large US insurance provider.

The details of these major deals are shown below:

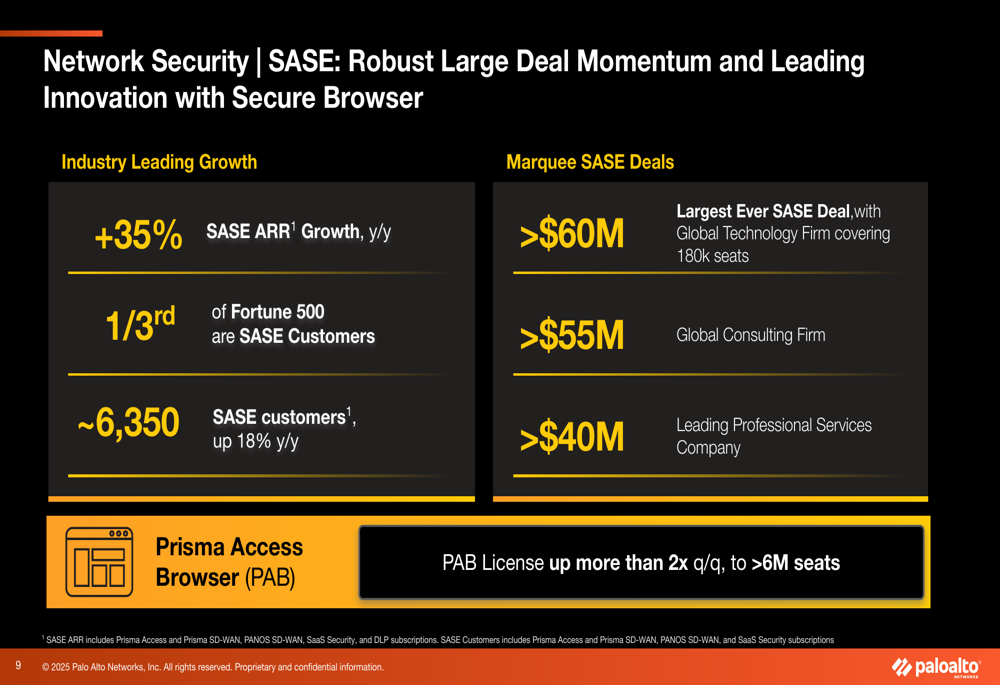

Within the Network Security business, Palo Alto Networks is seeing a shift toward software and Secure Access Service Edge (SASE) solutions. More than 60% of Q4 Network Security bookings came from SASE and software products, with Network Security NGS ARR growing approximately 35% year-over-year to $3.9 billion.

The company reported strong momentum in its SASE business, with 35% year-over-year ARR growth and approximately 6,350 total SASE customers, up 18% from the previous year. Notably, one-third of Fortune 500 companies are now SASE customers, and the company closed its largest-ever SASE deal of over $60 million with a global technology firm.

The SASE business highlights are shown in this slide:

CyberArk Acquisition & Future Strategy

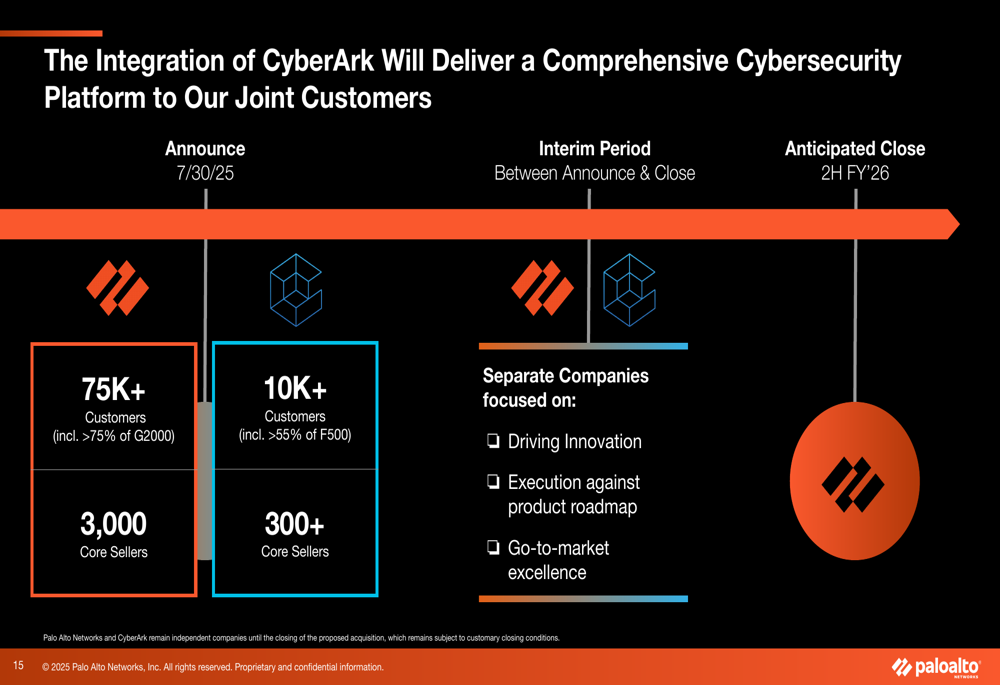

On July 30, 2025, Palo Alto Networks announced its acquisition of CyberArk, a leader in identity security and privileged access management. The company views identity as a key control and enforcement point similar to network security, with the acquisition expected to close in the second half of FY26.

The strategic rationale and integration timeline for the CyberArk acquisition are illustrated below:

The combined company will serve a broader customer base, with Palo Alto Networks bringing 75,000+ customers (including more than 75% of the Global 2000) and CyberArk adding 10,000+ customers (including more than 55% of the Fortune 500).

Forward-Looking Statements

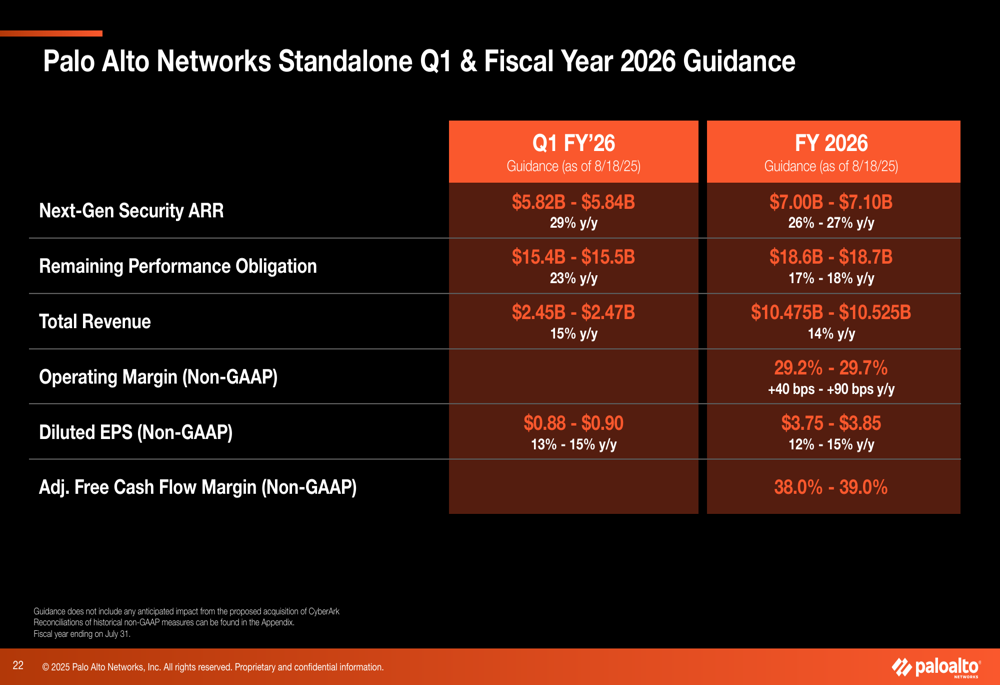

Looking ahead to fiscal year 2026, Palo Alto Networks provided guidance for standalone operations (excluding the CyberArk acquisition). The company expects revenue to reach $10.475-$10.525 billion, representing 14% year-over-year growth, with NGS ARR projected to grow 26-27% to $7.00-$7.10 billion.

The detailed guidance for Q1 and full-year FY26 is presented here:

For the combined company (including CyberArk), Palo Alto Networks is targeting a free cash flow margin of over 40% by FY28, supported by continued operating margin expansion, transition to deferred payments, and a capital-light business model.

The company identified multiple growth drivers for FY26, including double-digit product revenue growth driven by software products, continued SASE momentum with large enterprise customers, and rapid growth in XSIAM (its AI-driven security operations platform) at scale.

Palo Alto Networks' stock closed at $177.09 on August 18, 2025, down 0.41% for the day, but rose 0.54% in after-hours trading following the earnings release. The stock has traded between $144.15 and $210.39 over the past 52 weeks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.