TSX tick higher after index ends prior session near two-week high

Introduction & Market Context

Pangaea Logistics Solutions (NASDAQ:PANL) released its first quarter 2025 earnings presentation on May 13, revealing a challenging start to the year despite the company’s continued ability to outperform industry benchmarks. The dry bulk shipping operator reported a net loss while maintaining its strategy of focusing on specialized cargo routes and expanding its fleet capabilities through recent acquisitions.

The company’s stock reacted negatively in after-hours trading, dropping 2.71% to $4.30, following a 10.22% gain during the regular session. This mixed performance reflects investor uncertainty about Pangaea’s near-term prospects despite its long-term strategic positioning.

Quarterly Performance Highlights

Pangaea reported a GAAP net loss of $2.0 million, or $0.03 per share, for the first quarter of 2025, a significant decline from the $11.7 million profit reported in the same period last year. Adjusted net loss came in at $2.2 million, or $0.03 per share, compared to adjusted earnings of $0.14 per share in Q1 2024.

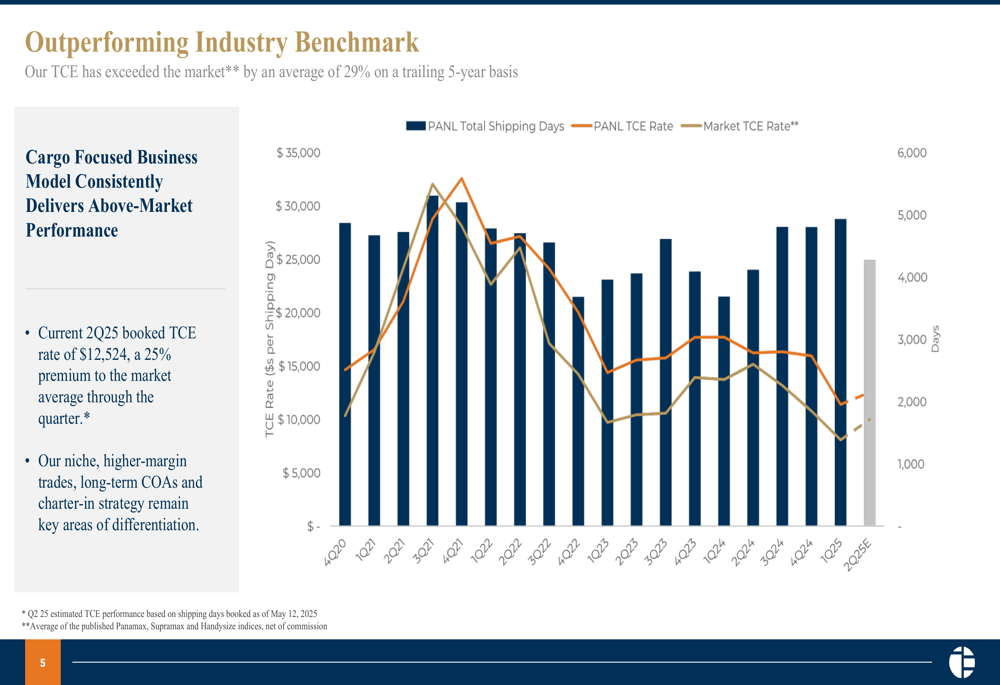

Despite these challenges, the company highlighted that its Time Charter Equivalent (TCE) rates outperformed benchmark Panamax, Supramax, and Handysize indexes by 33%, demonstrating its ability to secure premium rates in a difficult market.

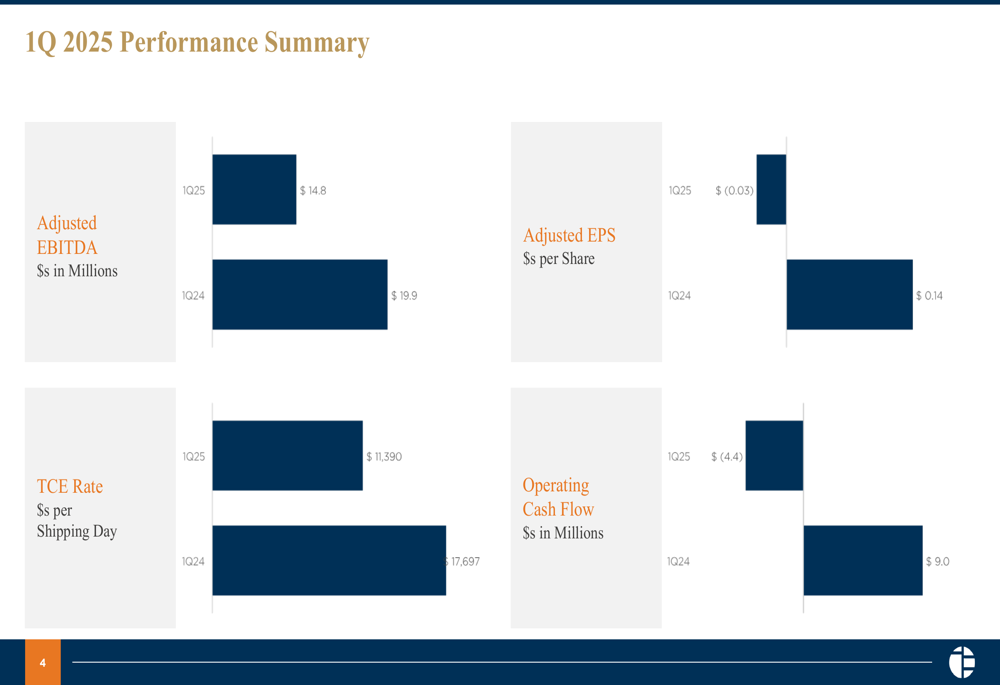

As shown in the following performance summary comparing Q1 2025 to Q1 2024:

The company’s Adjusted EBITDA decreased to $14.8 million in Q1 2025 from $19.9 million in the prior year period, while TCE rates fell to $11,390 from $17,697. Operating cash flow turned negative at -$4.4 million compared to positive $9.0 million in Q1 2024.

Pangaea has consistently maintained a premium over market rates, as illustrated in this five-year comparison of TCE rates:

As of May 12, 2025, the company had booked 4,275 days at an average of $12,524 per day for the second quarter, representing a 25% premium to benchmark indexes, suggesting some improvement in the current quarter.

Strategic Initiatives

A key development highlighted in the presentation was the successful integration of the Strategic Shipping Inc. (SSI) dry bulk fleet, which Pangaea acquired in late 2024. This acquisition significantly expanded the company’s presence in the handysize segment, providing greater scale and diversification.

The strategic rationale behind the SSI fleet merger is outlined in the following slide:

The acquisition added 15 handysize vessels to Pangaea’s fleet, bringing the total owned fleet to 41 vessels across multiple size categories. Management emphasized that this expansion strengthens their dry bulk operations team and provides greater operational flexibility.

CEO Mark Silinowski had previously noted during the Q4 2024 earnings call that the company "always look[s] for work that pays a little more than market," highlighting Pangaea’s focus on specialized cargo and challenging trade routes that command premium rates.

Financial Position and Capital Allocation

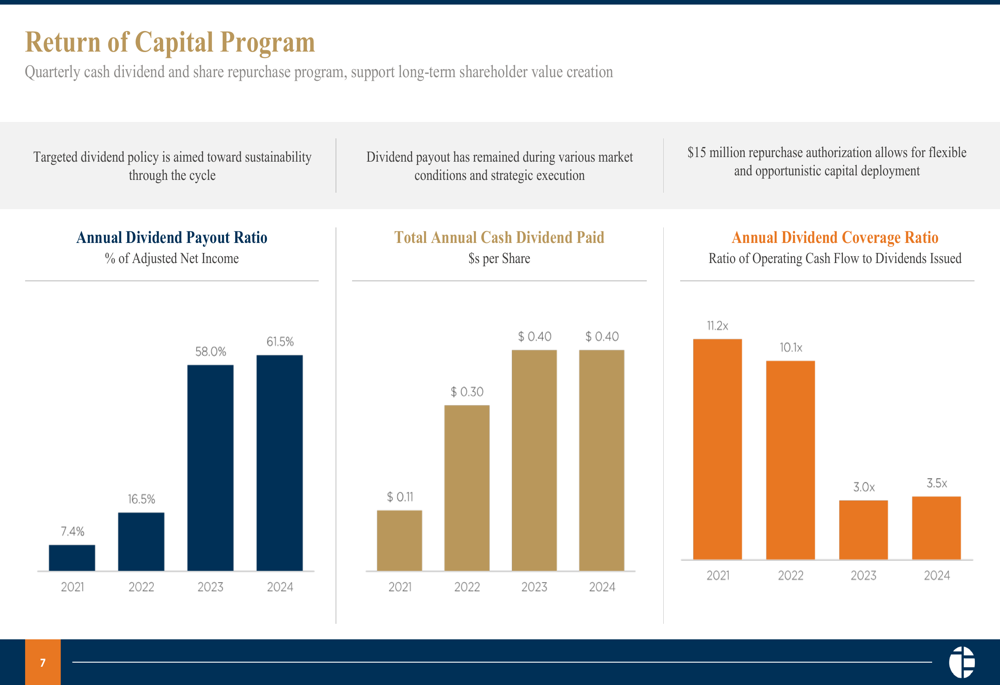

Despite the challenging quarter, Pangaea announced a new $15 million share repurchase program and maintained its quarterly dividend of $0.05 per share, demonstrating confidence in its long-term financial position.

The company’s return of capital program has evolved significantly over recent years, with the dividend payout ratio increasing from 7.4% of adjusted net income in 2021 to 61.5% in 2024:

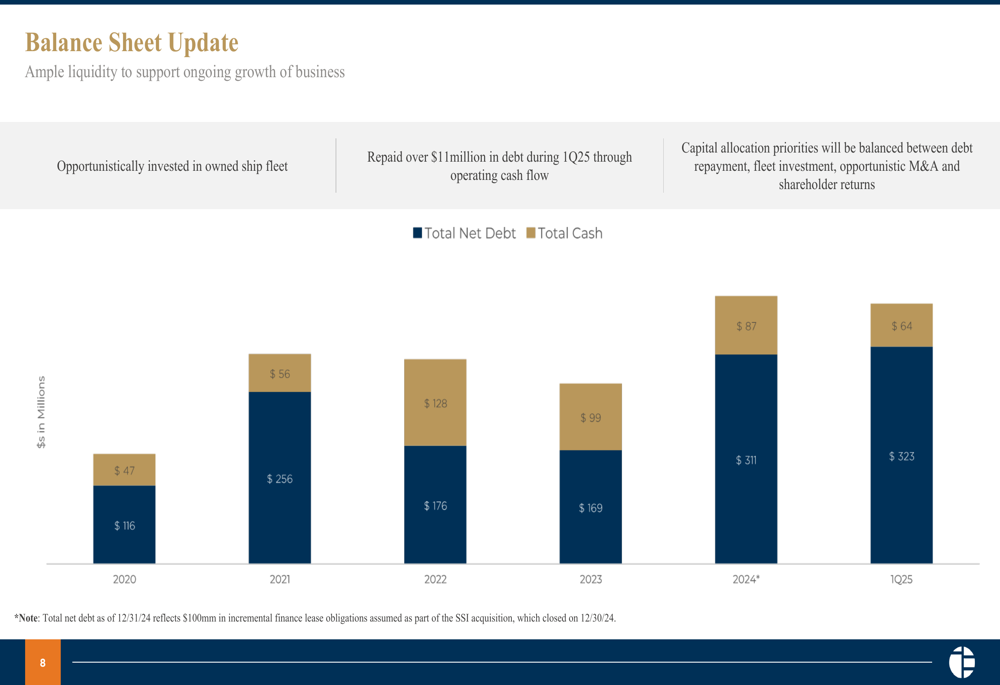

However, Pangaea’s balance sheet shows increasing leverage following the SSI acquisition. Total (EPA:TTEF) net debt rose to $323 million as of March 31, 2025, up from $311 million at year-end 2024, while cash declined to $64 million from $87 million over the same period.

The increase in net debt reflects $100 million in incremental finance lease obligations assumed as part of the SSI acquisition, which closed on December 30, 2024. This represents a significant change from the $86.8 million cash position reported in the Q4 2024 earnings announcement.

Industry Outlook and Positioning

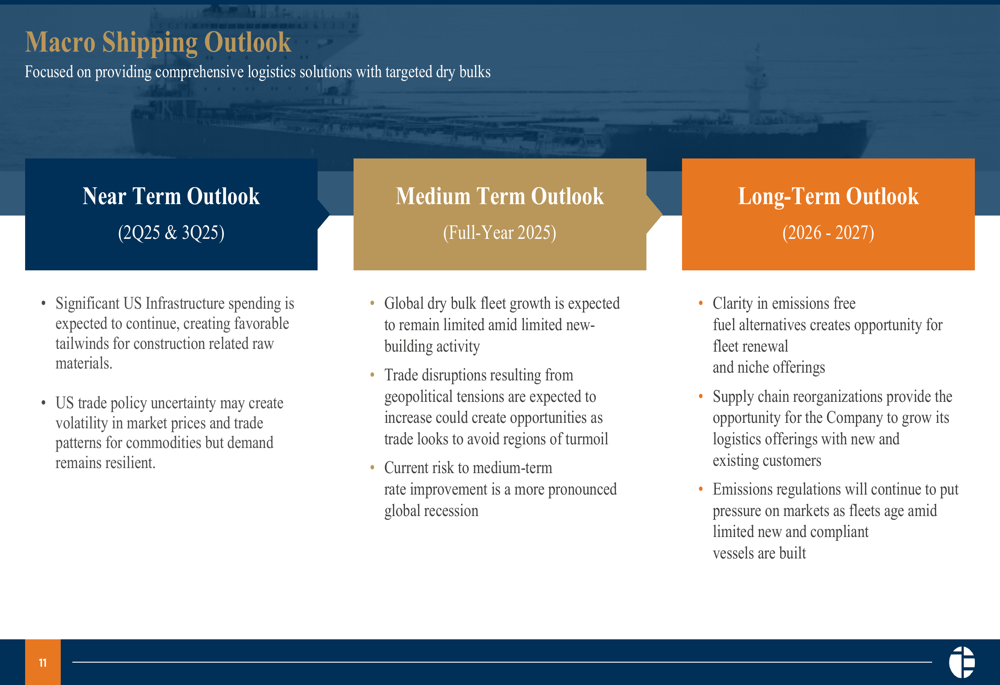

Pangaea provided a detailed outlook for the shipping industry across different time horizons, highlighting both opportunities and challenges:

In the near term (Q2 and Q3 2025), the company expects to benefit from significant US infrastructure spending but notes uncertainty around US trade policies. For the full year 2025, management anticipates global dry bulk fleet growth alongside potential trade disruptions and recession risks.

Looking further ahead to 2026-2027, Pangaea is focused on emissions regulations, supply chain reorganizations, and the development of emissions-free fuel alternatives.

The company maintains that its integrated shipping-logistics model, leading position in Ice-Class trades, and long-term cargo contracts provide significant competitive advantages. Management emphasized that these factors, along with their focus on consistently high fleet utilization, should enable Pangaea to continue outperforming industry benchmarks despite current market challenges.

While the first quarter results represent a step back from the strong performance seen in Q4 2024, when the company exceeded EPS and revenue forecasts, Pangaea’s strategic positioning and consistent outperformance of industry benchmarks suggest potential for recovery as market conditions evolve through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.