Nvidia set to lose $180 billion in market value today as Meta weighs Google chips

Introduction & Market Context

Pangaea Logistics Solutions (NASDAQ:PANL) released its second quarter 2025 earnings presentation on August 8, highlighting the company's ability to navigate challenging dry bulk shipping market conditions. While reporting a net loss for the quarter, Pangaea emphasized its continued outperformance of industry benchmarks and strategic fleet expansion initiatives.

The dry bulk shipping sector has faced significant headwinds in 2025, with market rates declining substantially year-over-year. Despite these challenges, Pangaea has maintained its operational advantage through its integrated shipping-logistics model and specialized fleet capabilities.

Quarterly Performance Highlights

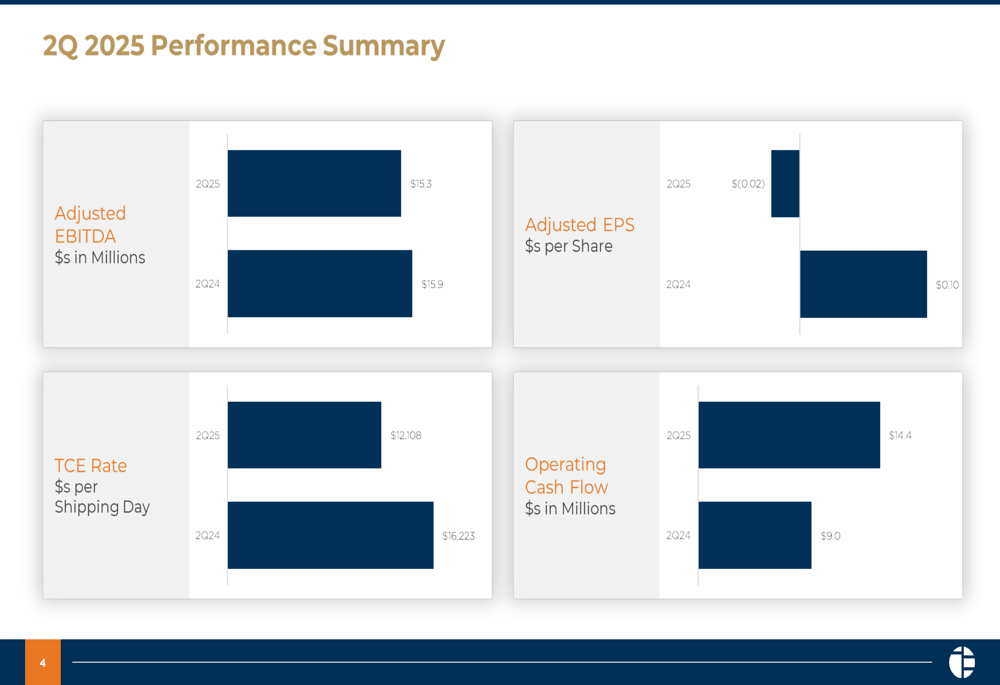

Pangaea reported a GAAP net loss of $2.7 million ($0.04 per share) for Q2 2025, compared to net income of $3.7 million in Q2 2024. On an adjusted basis, the company posted a net loss of $1.4 million ($0.02 per share), contrasting with the positive adjusted EPS of $0.10 in the same period last year.

Despite the profitability decline, Adjusted EBITDA remained relatively stable at $15.3 million, only slightly below the $15.9 million reported in Q2 2024. Operating cash flow showed significant improvement, increasing to $14.4 million from $9.0 million in the prior year period.

As shown in the following performance summary chart:

The company's Time Charter Equivalent (TCE) rate decreased to $12,108 in Q2 2025 from $16,223 in Q2 2024, reflecting broader market conditions. However, this rate still outperformed benchmark Panamax, Supramax, and Handysize indices by 17%, demonstrating Pangaea's operational advantages.

Market Outperformance

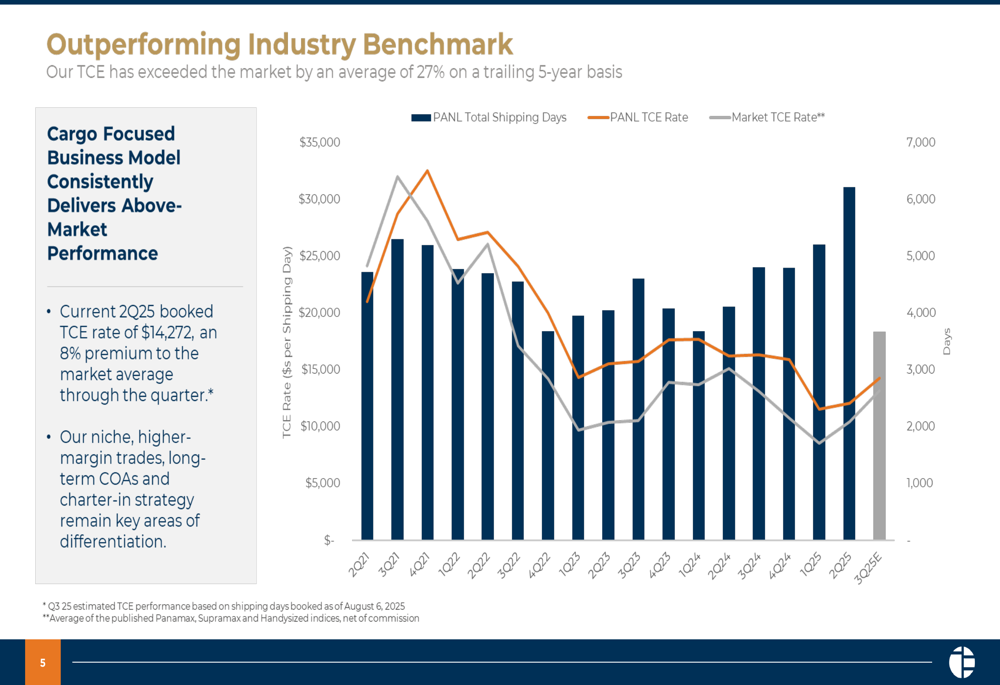

A key highlight of Pangaea's presentation was its consistent ability to generate premium returns compared to industry benchmarks. The company has outperformed market TCE rates by an average of 27% on a trailing 5-year basis, showcasing the effectiveness of its business model.

This outperformance is illustrated in the following chart, which tracks Pangaea's TCE rates against market averages since Q1 2021:

Looking ahead, Pangaea has already booked 3,671 shipping days as of August 6, 2025, at an average rate of $14,272 per day, suggesting potential improvement in the third quarter.

Strategic Initiatives

Pangaea has continued its fleet expansion strategy, building on significant vessel acquisitions made in recent years. During 2021-2022, the company purchased seven vessels for $245 million, followed by three vessels for $83 million and the acquisition of 15 vessels for 18.06 million shares in 2023-2024.

Recent transactions include the sale of the Strategic Endeavor for $7.7 million and the purchase of the remaining 49% equity ownership of Seamar Management for $2.7 million. Additionally, the company has begun financing the Strategic Spirit and Strategic Vision for $9 million each, with these transactions expected to close in Q3 2025.

The following slide details the company's vessel acquisition strategy:

Balance Sheet and Capital Return

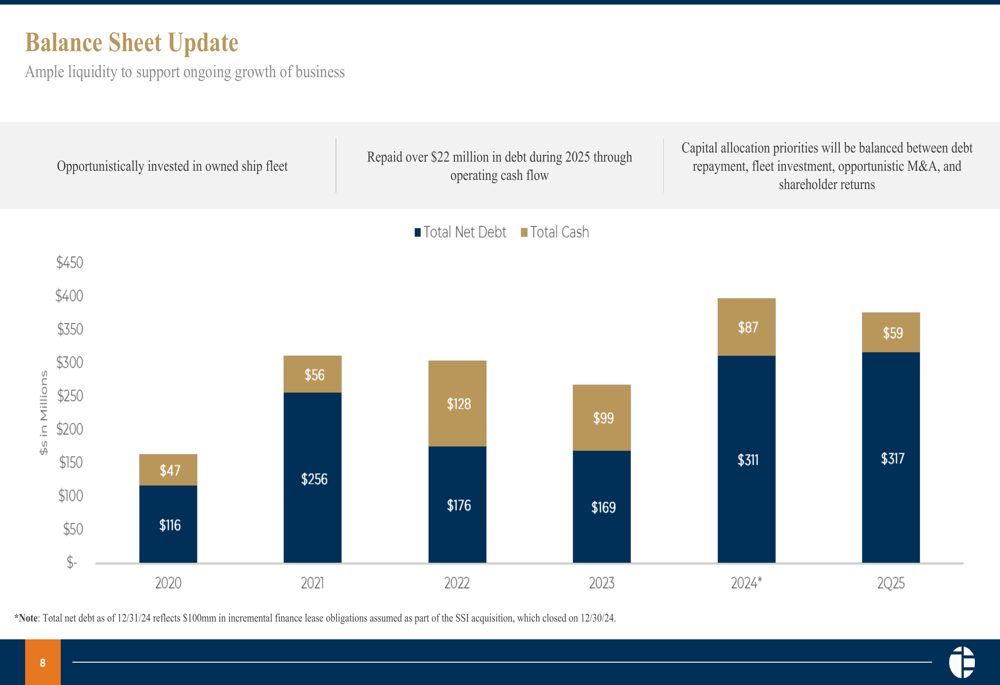

Pangaea's balance sheet reflects its significant fleet investments, with total net debt of $317 million and cash of $59 million as of Q2 2025. This represents an increase from the net debt position of $311 million at the end of 2024, partly due to the Strategic Shipping Inc. (SSI) acquisition which added approximately $100 million in incremental finance lease obligations.

The company's balance sheet evolution is illustrated in this chart:

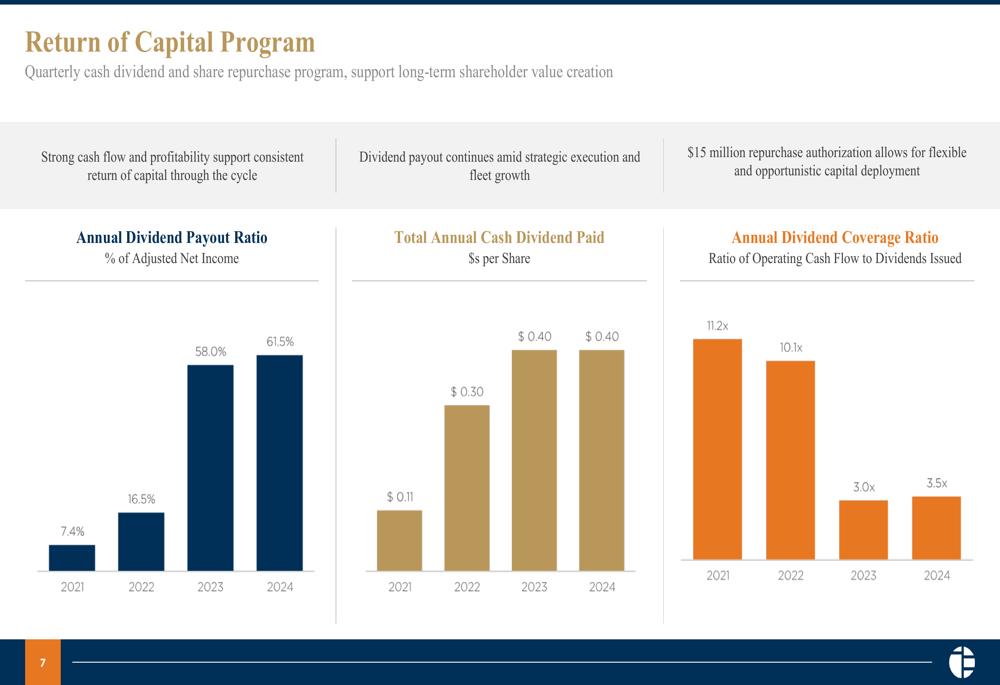

Despite the challenging market environment, Pangaea has maintained its commitment to shareholder returns. The company repurchased $1 million in shares during Q2 2025 at an average price of $4.96 per share. This follows a pattern of increasing dividend payouts, with the annual dividend payout ratio rising from 7.4% of adjusted net income in 2021 to 61.5% in 2024.

The following chart details Pangaea's return of capital program:

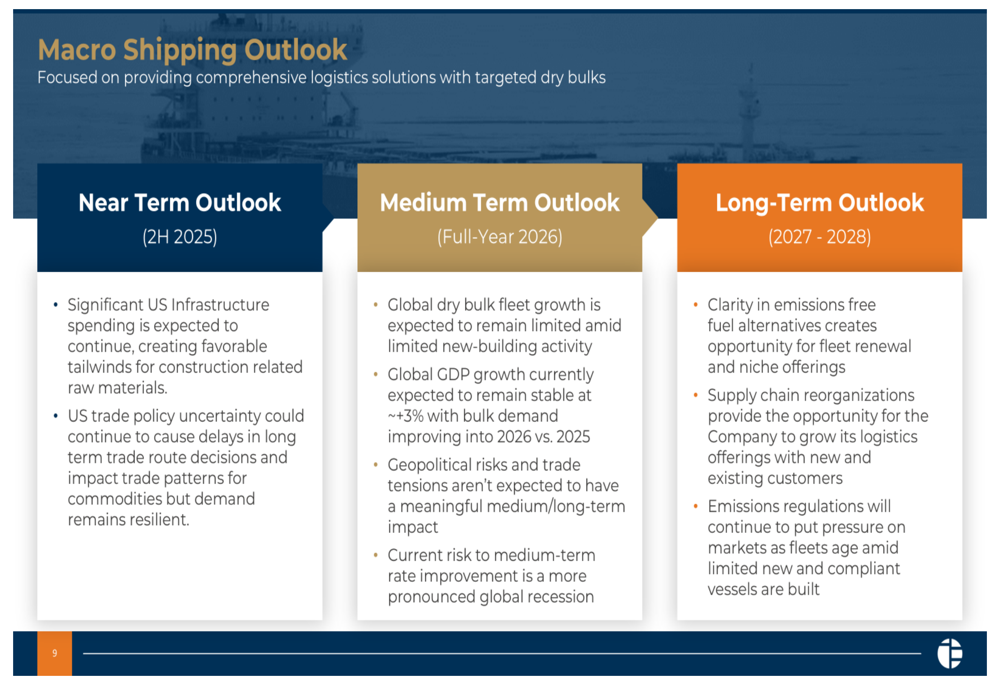

Forward-Looking Statements

Pangaea's presentation outlined its market outlook across different time horizons. In the near term (second half of 2025), the company expects significant US infrastructure spending to support demand, though potential delays due to US trade policy remain a concern.

For the medium term (full-year 2026), Pangaea anticipates limited dry bulk fleet growth and stable global GDP growth, with risks stemming from geopolitical tensions and the possibility of a global recession.

The long-term outlook (2027-2028) focuses on emissions regulations, with the company expecting greater clarity in emissions-free fuel alternatives and continued supply chain reorganizations.

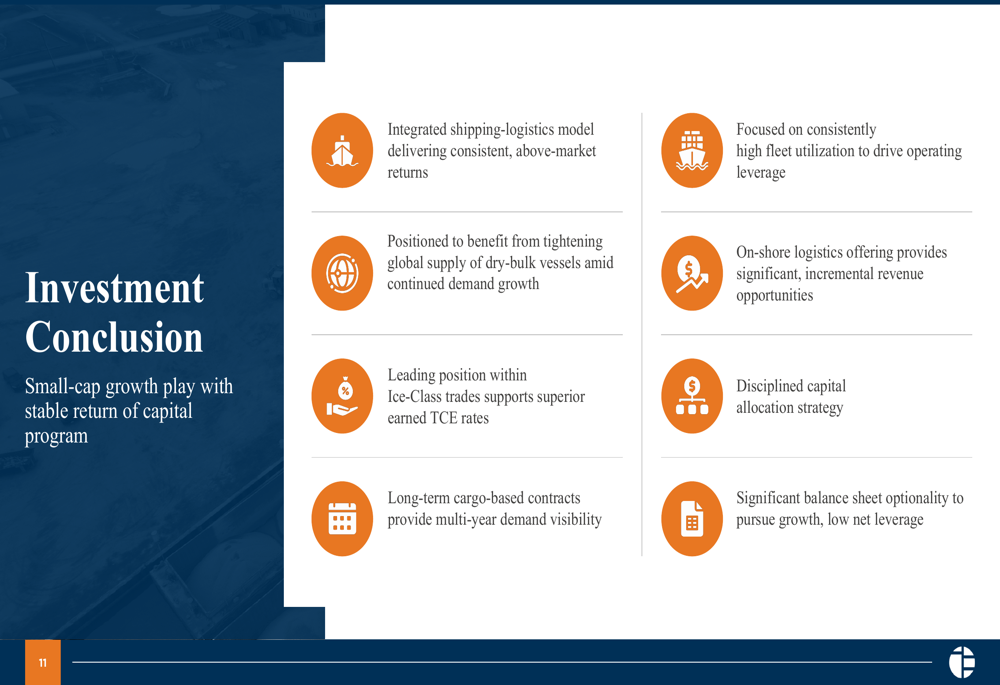

Investment Thesis

Pangaea concluded its presentation by emphasizing key factors that support its investment thesis. These include its integrated shipping-logistics model, leading position within Ice-Class trades, long-term cargo-based contracts, consistently high fleet utilization, and disciplined capital allocation strategy.

The company believes these strengths position it well to navigate current market challenges while capitalizing on future opportunities as global dry bulk vessel supply tightens.

The stock closed at $4.83 on August 7, 2025, down 2.23% for the day. Year-to-date, Pangaea's shares have traded between a 52-week low of $3.93 and a high of $7.50, reflecting the volatile nature of the shipping sector and broader market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.