AZTR receives NYSE delisting warning over equity requirement

Par Pacific Holdings Inc (NYSE:PARR) presented its August 2025 investor slides highlighting the company’s strategic positioning, financial performance, and growth initiatives. The presentation comes after a mixed first quarter that saw the company’s stock rise despite an earnings miss, suggesting investors are focused on the company’s long-term strategy rather than short-term fluctuations.

Strategic Growth Through Acquisitions

Par Pacific has successfully transformed from a single refinery operation into a vertically integrated multi-site platform over the past decade. The company’s strategic acquisitions have expanded its footprint across the western United States, with operations in Hawaii, Washington, Montana, and Wyoming.

As shown in the following map highlighting the company’s expansion strategy:

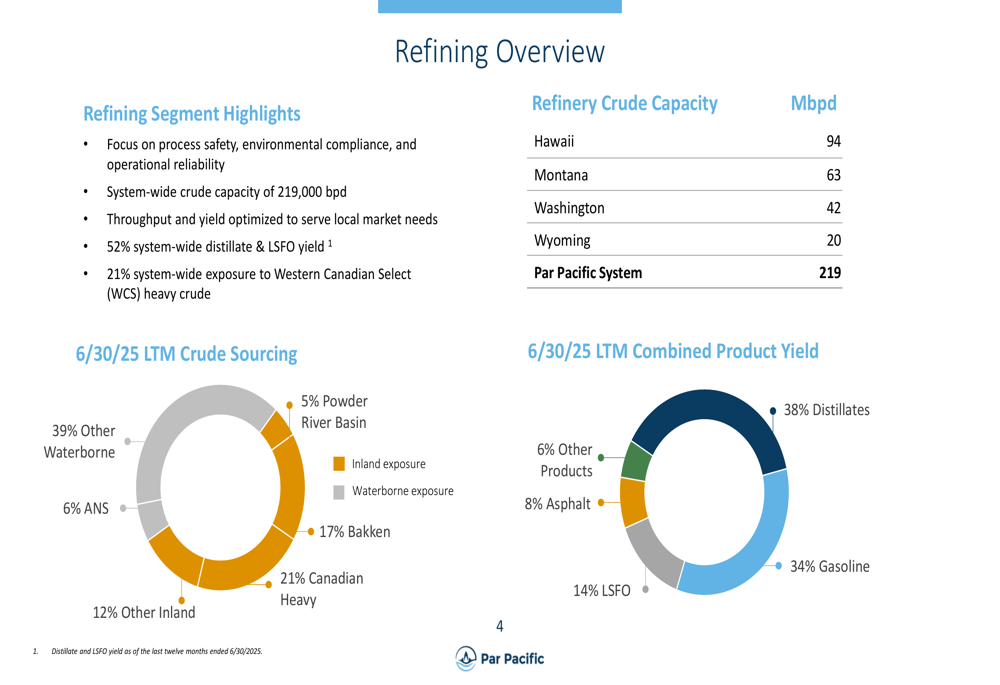

This geographic diversification has enabled Par Pacific to develop an integrated downstream system with 219,000 barrels per day of refining capacity. The company’s strategic focus on distillate production—which typically commands higher margins than gasoline—positions it favorably compared to industry peers.

The following chart illustrates Par Pacific’s advantaged distillate yield profile compared to competitors:

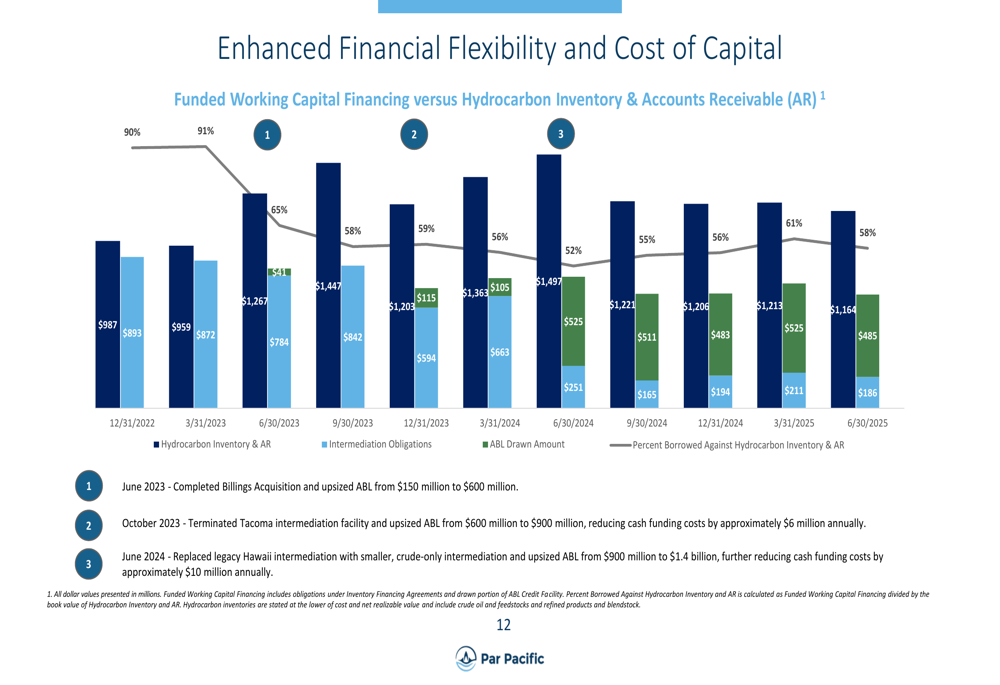

Financial Performance and Balance Sheet Strength

Par Pacific’s financial position has strengthened considerably, with total liquidity reaching $647 million as of June 30, 2025, up from $614 million at the end of 2024. This robust liquidity provides flexibility for both operations and strategic initiatives.

The company’s retail and logistics segments have shown consistent growth, providing stability to offset the inherent volatility in refining operations. Adjusted EBITDA from these segments has increased steadily over recent years.

The following chart demonstrates the growing contribution from retail and logistics segments:

This growth in stable income streams comes despite challenges in the first quarter of 2025, when the company reported a larger-than-expected loss of $0.94 per share, though revenue exceeded expectations at $1.75 billion. The stock’s 9.17% rise following that announcement suggests investors are focused on the company’s long-term strategy and diversified business model.

Par Pacific’s balance sheet has also improved significantly, with net working capital increasing from negative $338 million at the end of 2021 to positive $343 million by mid-2025.

The following charts illustrate the company’s strengthening financial position:

Renewable Energy Transition

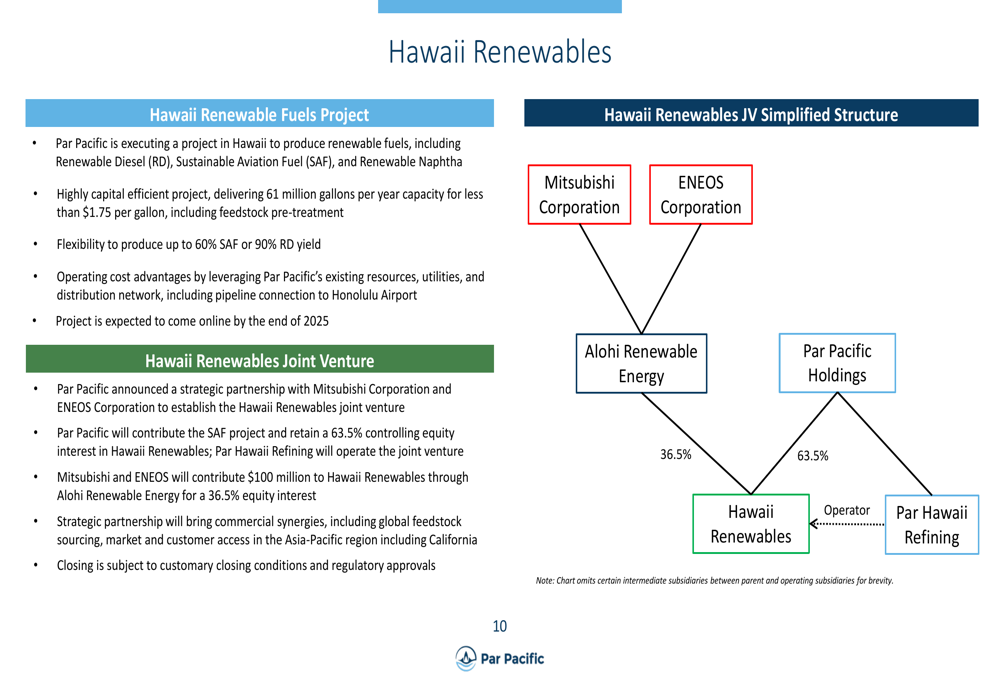

A key component of Par Pacific’s forward strategy is its Hawaii Renewable Fuels Project, which will produce both renewable diesel and sustainable aviation fuel (SAF) with a capacity of 61 million gallons per year. The project is expected to come online in late 2025, aligning with the timeline mentioned in the company’s Q1 2025 earnings call.

The company has formed a strategic joint venture with Mitsubishi Corporation and ENEOS Corporation, with Par Pacific maintaining a 63.5% interest in the Hawaii Renewables operation.

The following diagram illustrates the structure of this important joint venture:

This renewable fuels initiative positions Par Pacific to capitalize on the growing demand for lower-carbon transportation fuels, particularly in Hawaii where environmental regulations are stringent and the market for such products is favorable.

Mid-Cycle Financial Outlook

Par Pacific’s mid-cycle financial profile indicates the company’s earnings potential in normalized market conditions. The company projects mid-cycle adjusted EBITDA of $445-475 million, with refining contributing $340-370 million, logistics $115 million, and retail $70 million.

After accounting for maintenance capital expenditures, turnarounds, and cash interest, the company expects to generate $265-295 million in modified levered free cash flow.

The following table details the company’s mid-cycle financial projections:

Competitive Advantages and Market Position

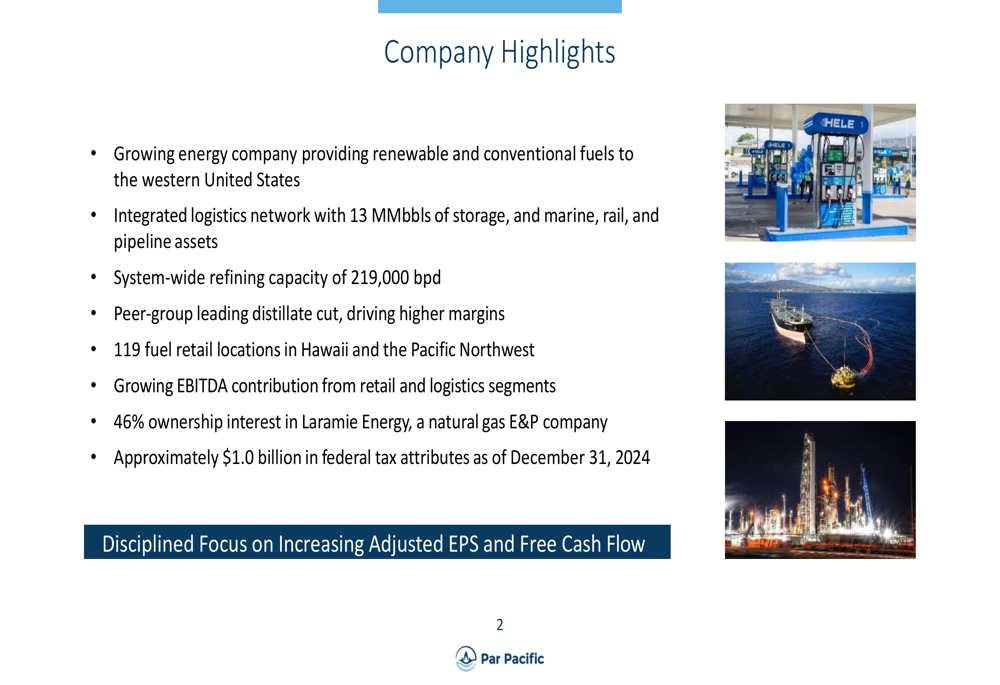

Par Pacific’s multimodal logistics system provides significant operational flexibility, allowing the company to optimize its supply chain and respond to market changes. The company operates 119 retail locations across Hawaii and the Pacific Northwest, with 33 company-operated convenience stores in Hawaii and 32 in Washington and Idaho.

The company’s refining operations are optimized for local market needs, with a system-wide distillate and low sulfur fuel oil yield of 52%, significantly higher than industry peers. This advantaged yield profile positions Par Pacific to benefit from typically stronger distillate margins.

Forward Outlook

Despite the earnings miss in Q1 2025, Par Pacific appears well-positioned for future growth. The company’s diversified business model, strong balance sheet, and strategic initiatives in renewable fuels provide multiple avenues for value creation.

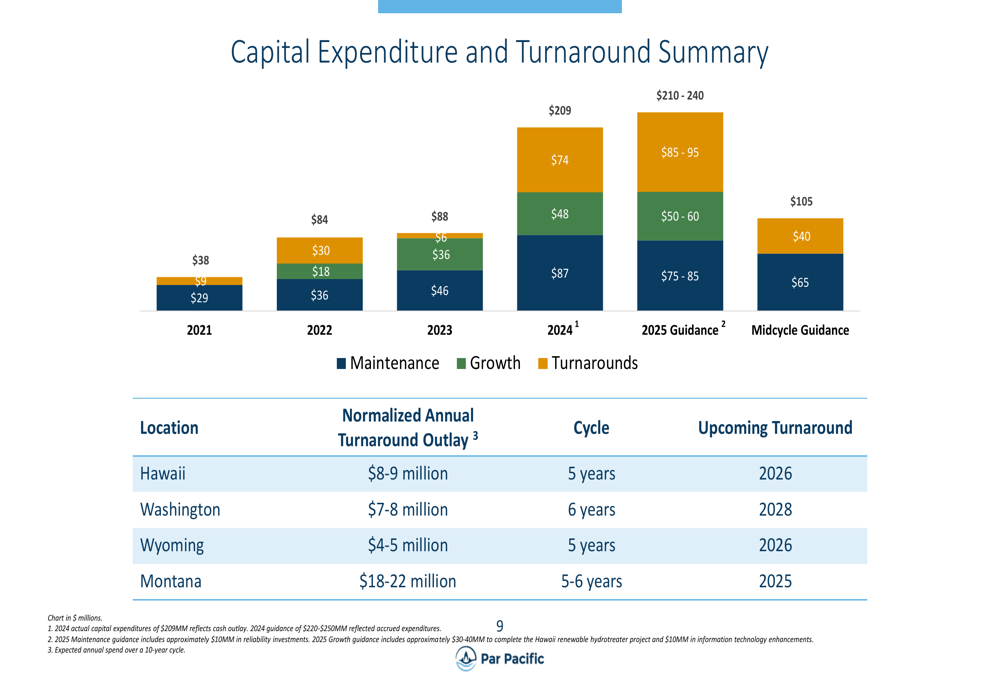

The company’s capital allocation strategy includes targeted growth investments, with $8-9 million allocated for Hawaii, $7-8 million for Washington, $4-5 million for Wyoming, and $18-22 million for Montana operations. The next major turnaround is scheduled for Montana in 2025, with Hawaii and Wyoming following in 2026.

Par Pacific’s approximately $1 billion in federal tax attributes as of December 31, 2024, should continue to enhance free cash flow by reducing tax liabilities. Combined with the company’s share repurchase program, which reduced outstanding shares by 5% in Q1 2025, these factors suggest a management focus on returning value to shareholders while investing in strategic growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.