Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Pareto Bank ASA (OB:PARB) reported a slight increase in profit for the first quarter of 2025, with earnings rising despite significantly higher impairments. The Norwegian niche bank, which specializes in property financing and corporate lending, saw its shares trade at NOK 72.40 on April 29, down 0.69% from the previous close.

The bank’s Q1 results reflect a balancing act between growing its loan book, particularly in residential development and Swedish operations, while maintaining strong capital ratios and managing increased credit risks in certain segments.

Quarterly Performance Highlights

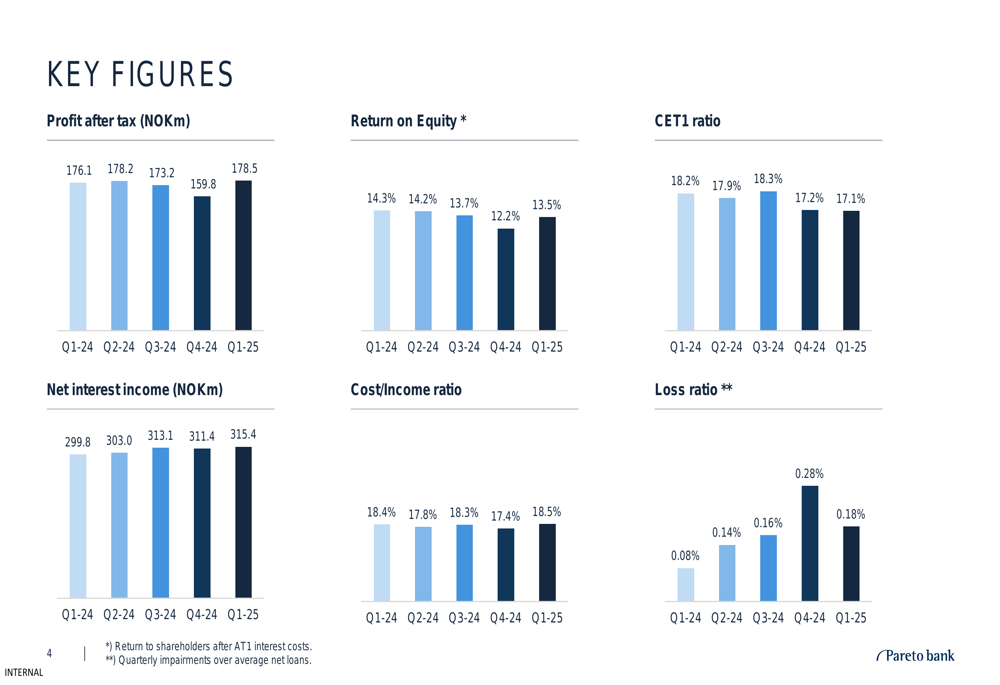

Pareto Bank reported profit after tax of NOK 178.5 million for Q1 2025, a modest increase from NOK 176.1 million in the same period last year. Return on equity declined to 13.5% from 14.3% in Q1 2024, reflecting the impact of higher impairments and a larger equity base.

Net interest income grew to NOK 315.4 million, up from NOK 299.8 million in Q1 2024, driven primarily by increased lending volumes. The bank maintained its strong operational efficiency with a cost/income ratio of 18.5%, virtually unchanged from 18.4% a year earlier.

As shown in the following chart of key financial figures, Pareto Bank has maintained relatively stable performance over the past five quarters, with some fluctuation in profitability:

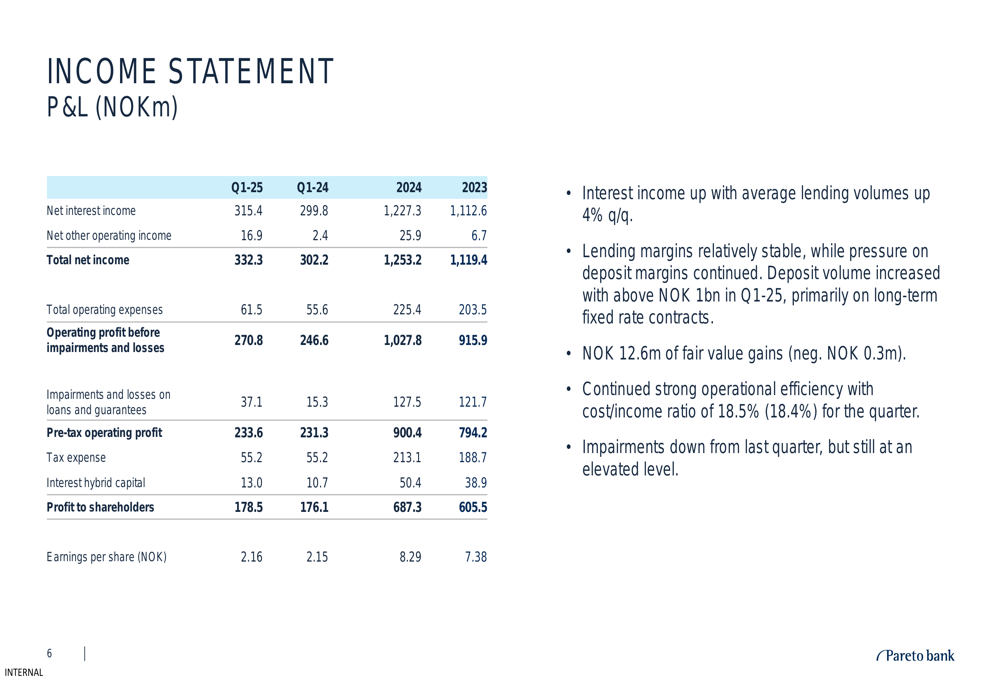

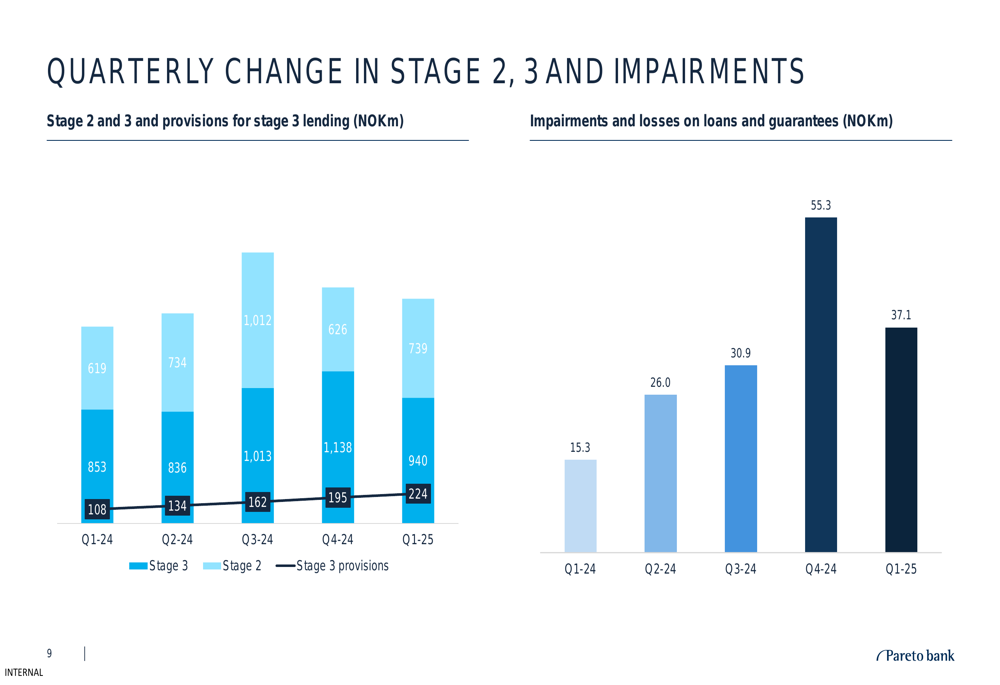

Total (EPA:TTEF) impairments increased significantly to NOK 37.1 million, up from NOK 15.3 million in Q1 2024, though down from NOK 55.3 million in the previous quarter. Individual impairments accounted for NOK 29.4 million, primarily within residential property development.

Detailed Financial Analysis

The bank’s income statement shows solid top-line growth, with total net income reaching NOK 332.3 million in Q1 2025, compared to NOK 302.2 million in the same quarter last year. This 10% increase was driven by both higher net interest income and improved other operating income.

The detailed breakdown of the income statement reveals the key drivers of performance:

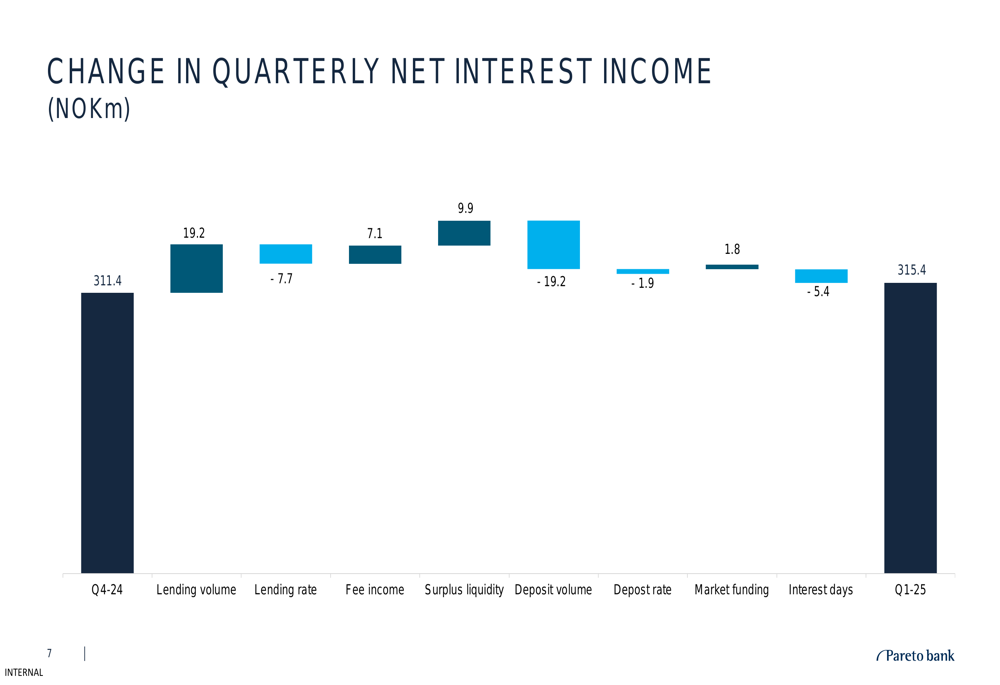

A waterfall analysis of the quarterly change in net interest income shows that lending volume contributed positively with NOK 19.2 million, while deposit volume had a negative impact of NOK 19.2 million. The bank also benefited from higher fee income and improved returns on surplus liquidity:

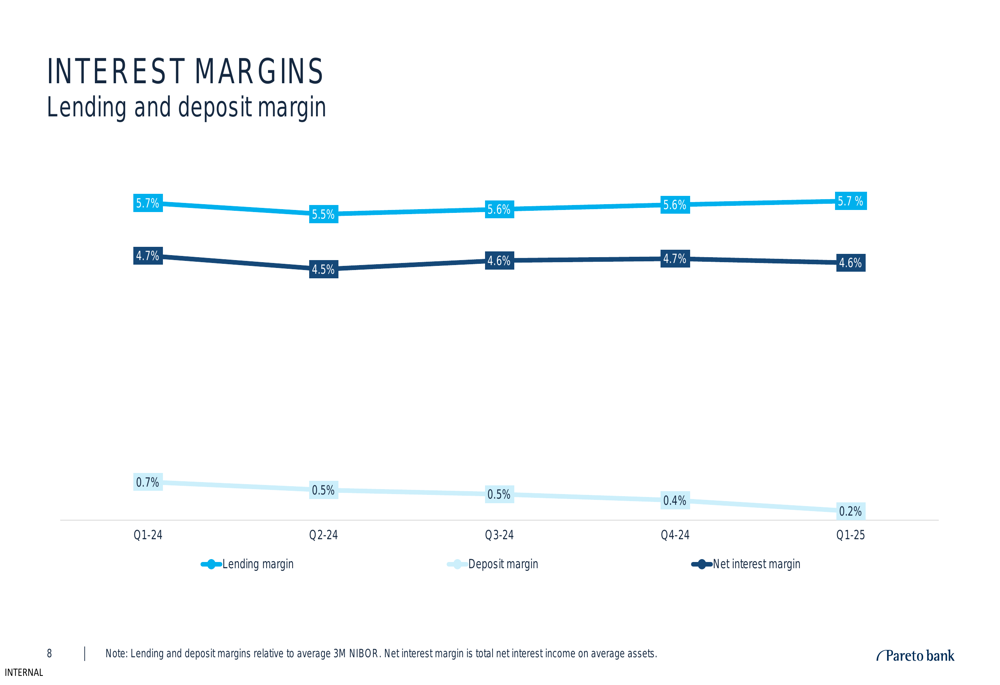

Interest margins remained relatively stable year-over-year, with the lending margin at 5.7% in both Q1 2024 and Q1 2025. However, the deposit margin decreased significantly from 0.7% to 0.2%, reflecting competitive pressures in the deposit market:

The quarterly trend in impairments shows a concerning pattern of increasing credit losses, though Q1 2025 saw some improvement compared to the previous quarter:

Business Area Update

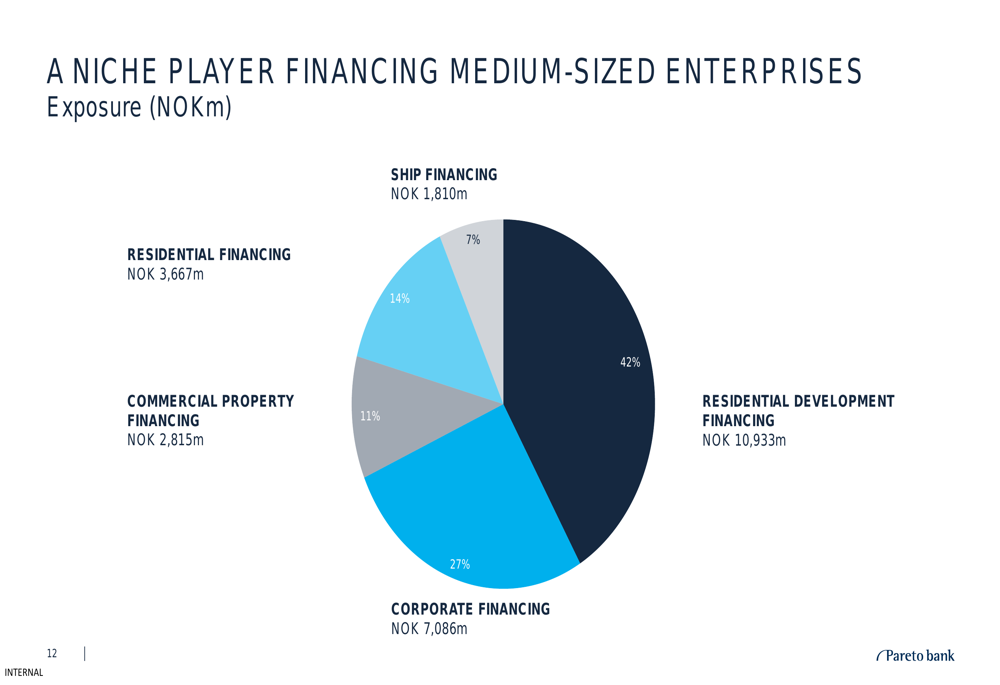

Pareto Bank’s loan portfolio remains heavily weighted toward property financing, with residential development accounting for 42% of total exposure. Corporate financing represents 27%, followed by residential financing (14%), commercial property (11%), and ship financing (7%).

The following chart illustrates the bank’s exposure by sector:

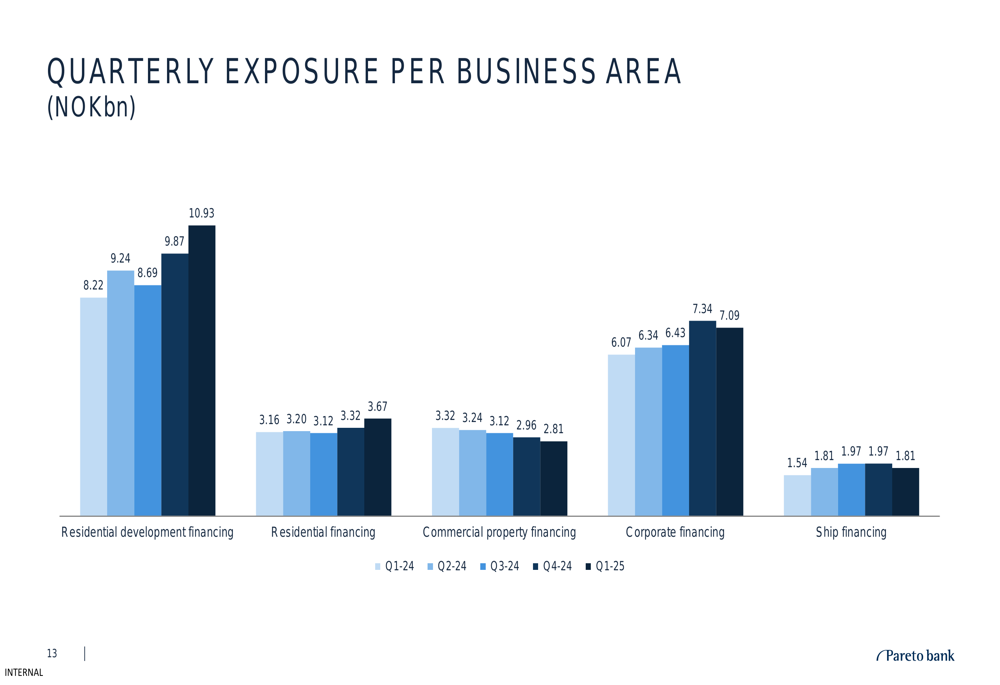

The bank has experienced strong growth in residential development financing, which increased to NOK 10.93 billion in Q1 2025 from NOK 8.22 billion a year earlier. Corporate financing also saw significant growth, reaching NOK 7.09 billion compared to NOK 6.07 billion in Q1 2024:

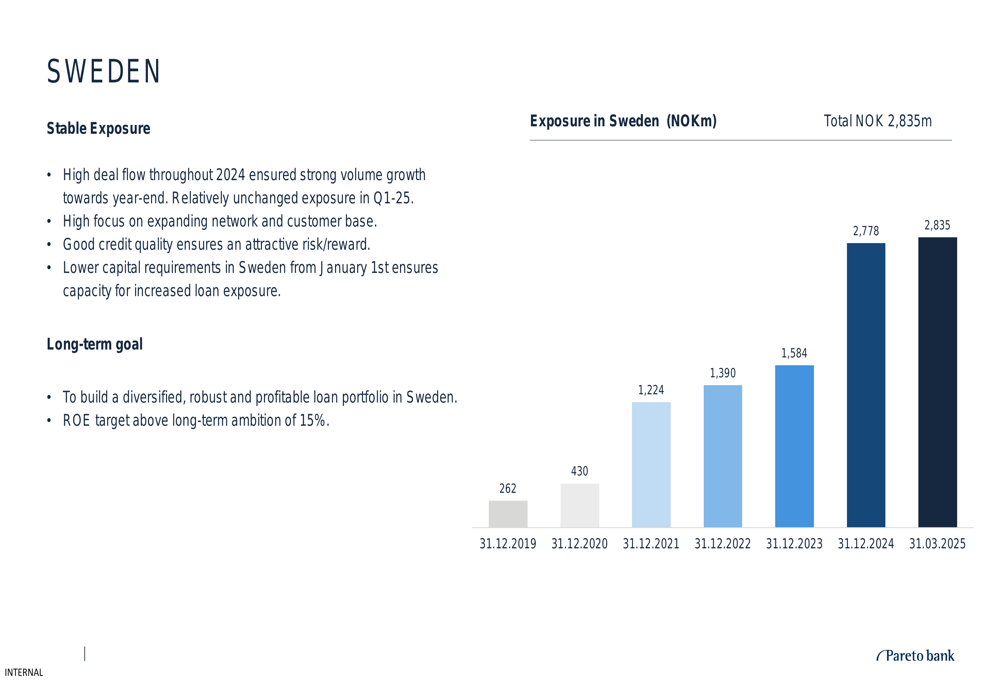

A notable strategic focus for Pareto Bank has been its expansion into Sweden, where exposure has grown steadily in recent years. Swedish operations now account for NOK 2.84 billion of the bank’s total lending, representing approximately 13.6% of the loan book:

Capital Position & Outlook

Pareto Bank maintains a strong capital position, with a CET1 ratio of 17.1% as of March 31, 2025, well above its long-term target of 16.3%. This provides a buffer against potential credit losses and supports future growth.

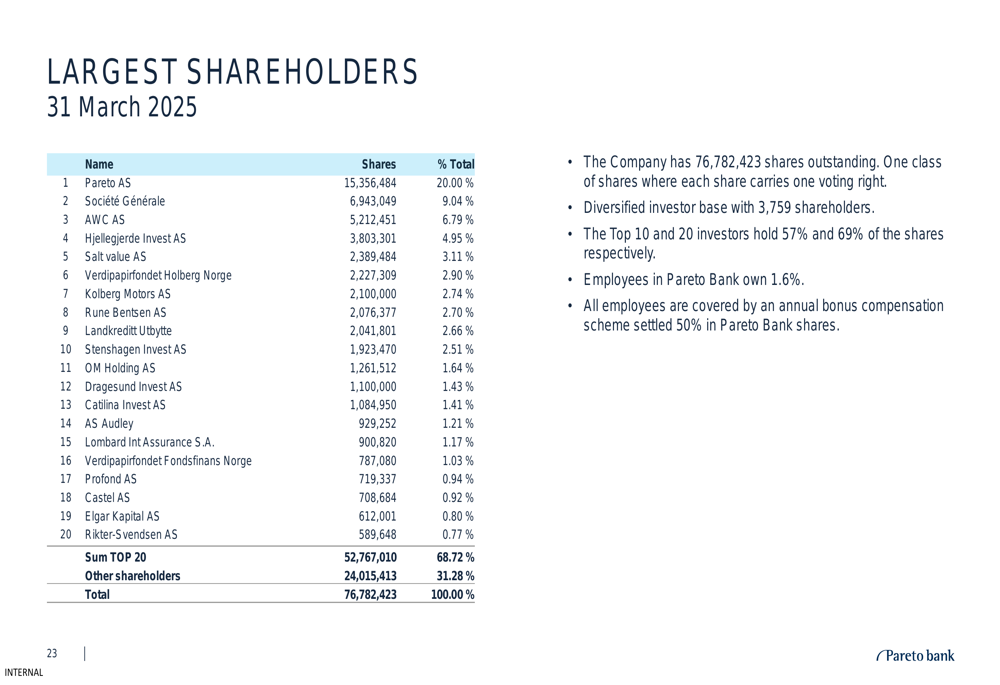

The bank’s shareholder structure remains stable, with Pareto AS as the largest shareholder holding 20% of the shares. The top 20 shareholders collectively own 68.72% of the bank:

Looking ahead, Pareto Bank expects continued growth in residential property financing in Q2 2025, while commercial property and ship financing volumes are projected to remain flat or decrease slightly. The bank maintains its long-term ROE target of 15%, though current performance at 13.5% falls somewhat short of this ambition.

The bank’s strong capital position, diversified loan portfolio, and efficient operations provide a solid foundation for navigating potential challenges in the Norwegian and Swedish property markets, though rising impairments will require careful monitoring in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.