Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

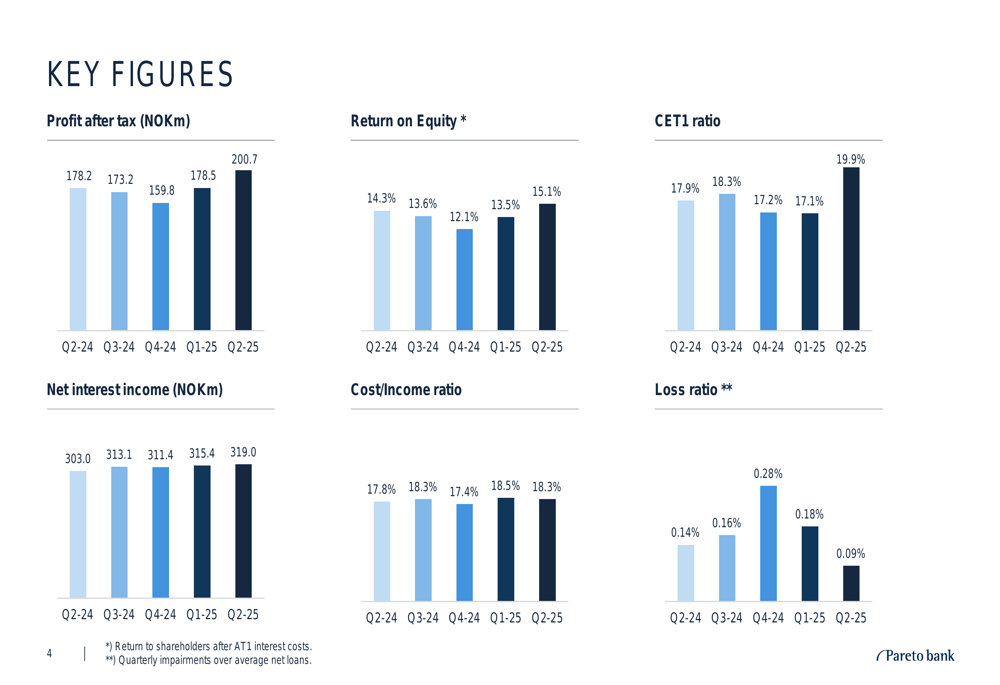

Pareto Bank ASA (OB:PARB) reported strong second-quarter 2025 results on July 18, with profit after tax rising 13% year-over-year to NOK 200.7 million. The Norwegian niche bank, which focuses on financing medium-sized enterprises, continues to deliver robust returns despite mixed conditions across its business segments.

The bank’s stock closed at NOK 87.20 on July 17, down 0.57% for the day but remaining near its 52-week high of NOK 88.50. Pareto Bank has significantly outperformed the broader Norwegian market, delivering a total return of 620% since inception compared to the OSEBX Index’s 202%.

Quarterly Performance Highlights

Pareto Bank achieved a return on equity of 15.1% in Q2 2025, up from 14.3% in the same quarter last year and exceeding its long-term target of 15%. Net interest income increased to NOK 319.0 million from NOK 303.0 million in Q2 2024, while earnings per share rose to NOK 2.44 from NOK 2.15.

As shown in the following chart of key financial metrics, the bank has demonstrated consistent improvement across most performance indicators over the past five quarters:

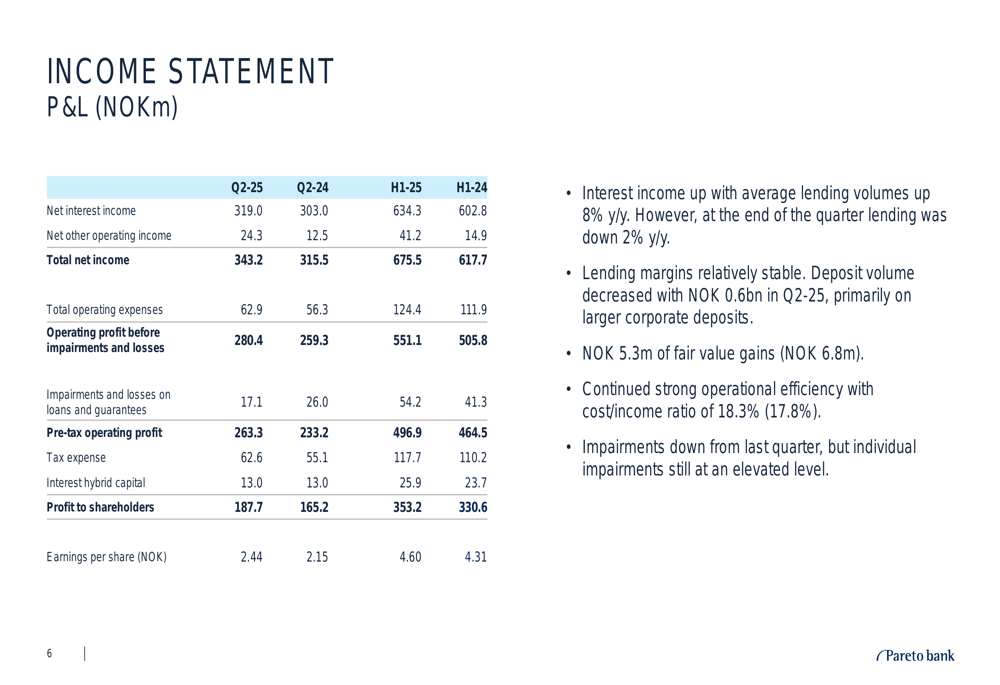

The bank’s income statement reveals solid growth in both quarterly and half-year results. Total (EPA:TTEF) net income for Q2 2025 reached NOK 343.2 million, up from NOK 315.5 million in Q2 2024, while operating profit before impairments grew to NOK 280.4 million from NOK 259.3 million.

Despite the positive profit trend, total lending at the end of Q2 2025 stood at NOK 19,249 million, down from NOK 19,585 million a year earlier. The bank cited significant redemptions and lower credit demand as factors behind this decline.

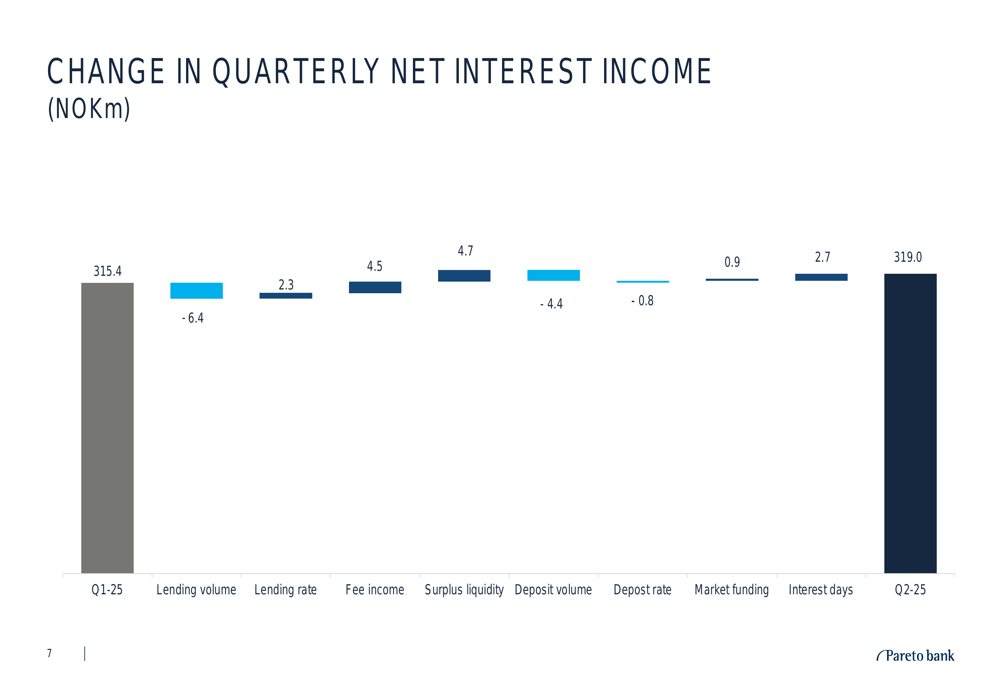

A detailed breakdown of the changes in quarterly net interest income shows that while lending volume had a negative impact of NOK 6.4 million, this was offset by improvements in fee income, surplus liquidity, and lending rates:

Business Segment Analysis

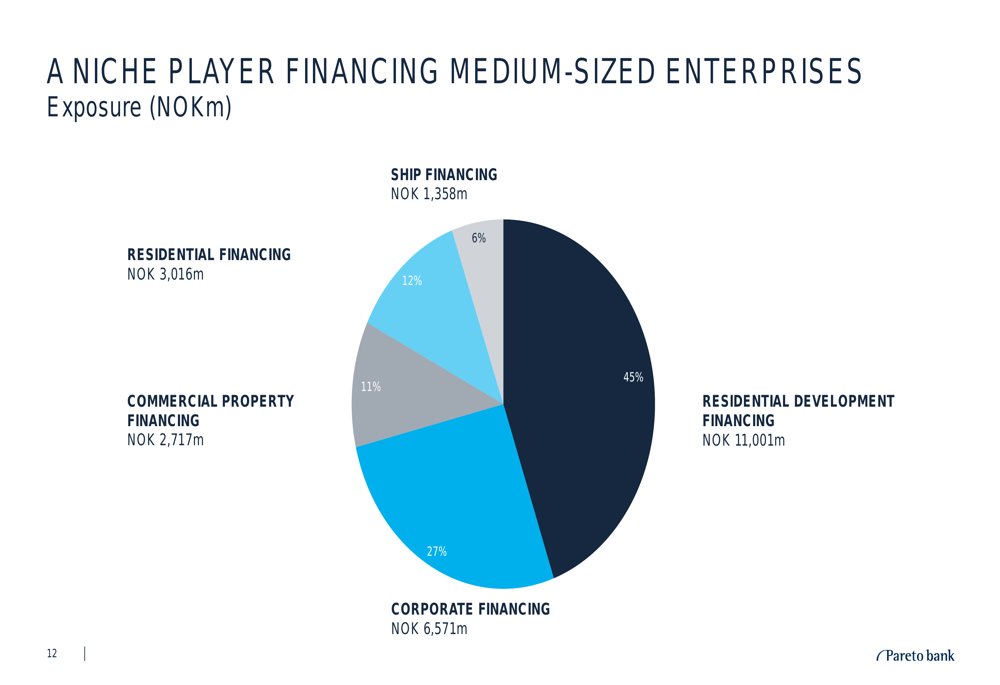

Pareto Bank operates as a niche player focusing on five key business areas. Residential development financing represents the largest exposure at 45% (NOK 11,001 million), followed by corporate financing at 27% (NOK 6,571 million), residential financing at 12% (NOK 3,016 million), commercial property financing at 11% (NOK 2,717 million), and ship financing at 6% (NOK 1,358 million).

The following chart illustrates the bank’s business mix:

Looking at quarterly trends across business segments, residential development financing has shown consistent growth over the past year, while ship financing and commercial property financing have declined:

The outlook varies significantly across business segments. In residential property financing, the bank expects decreased loan volume in Q3 2025 due to a persistently weak market with record low residential starts. The recent policy rate cut is expected to positively impact activity, but with limited effect in the near term.

Commercial property financing is projected to see subdued volume growth in Q3 2025 due to low transaction volumes and a high long-term rate outlook despite the recent rate cut. Corporate financing volume is expected to remain flat, while ship financing also anticipates flat volume after significant redemptions in the first half of 2025.

Capital Position & Shareholder Returns

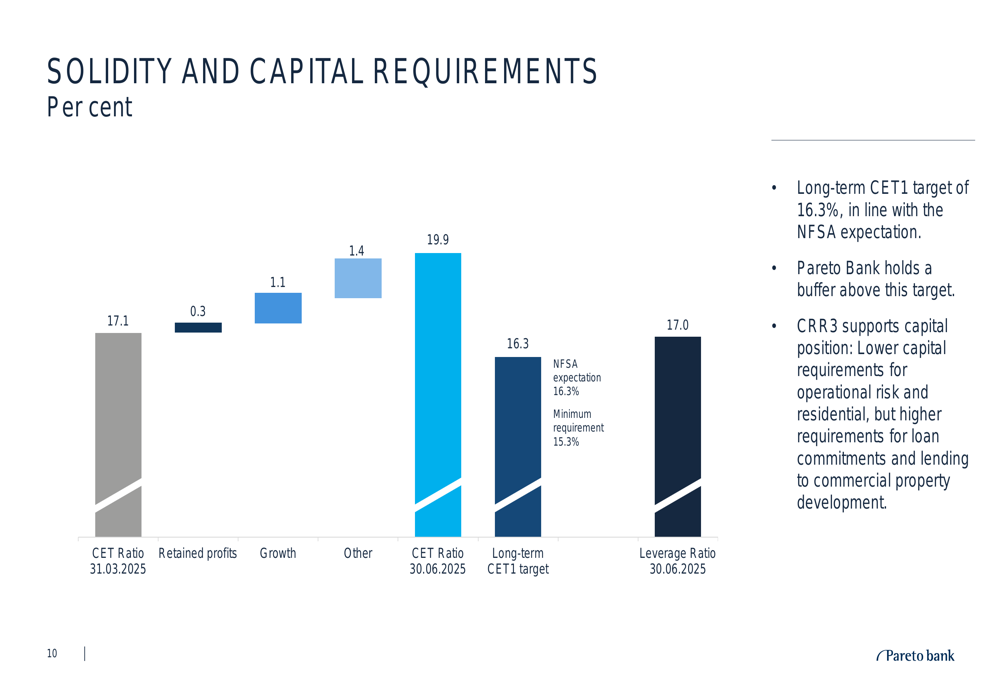

Pareto Bank significantly strengthened its capital position in Q2 2025, with the CET1 ratio increasing to 19.9% from 17.1% in the previous quarter. This improvement was driven by retained profits, growth effects, and the implementation of CRR3 regulations, which had a positive impact on capital requirements.

The following chart illustrates the changes in the bank’s CET1 ratio:

The bank maintains a long-term CET1 target of 16.3%, in line with the Norwegian Financial Supervisory Authority’s expectations, and currently holds a comfortable buffer above this target. The leverage ratio stands at 17.0%.

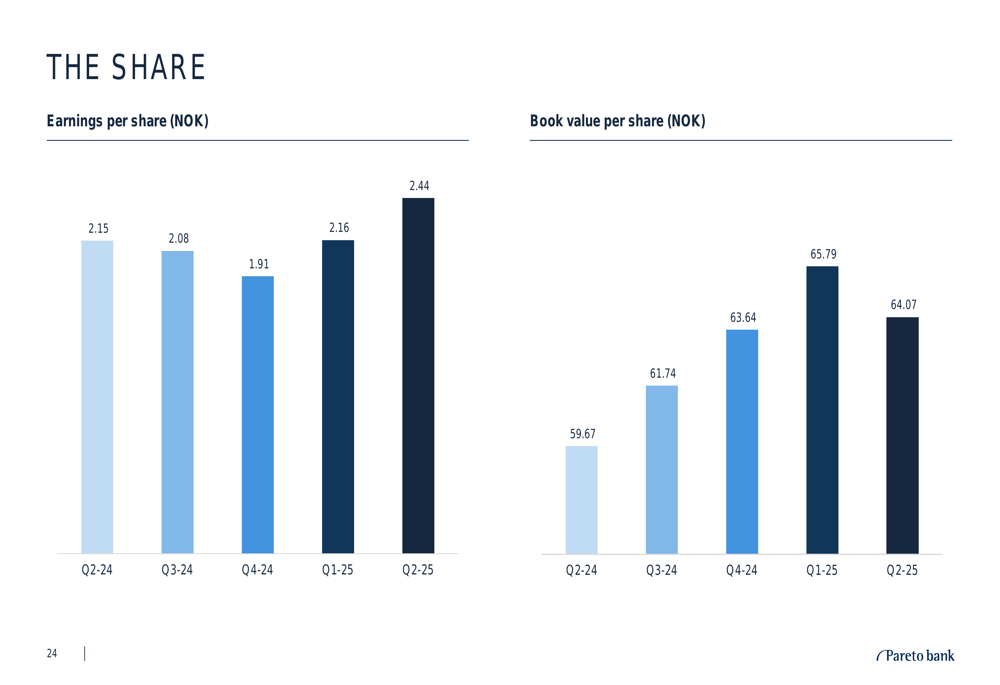

Pareto Bank has a dividend payout target of minimum 50%, which it has consistently met or exceeded in recent years. The bank’s earnings per share and book value per share have shown steady growth:

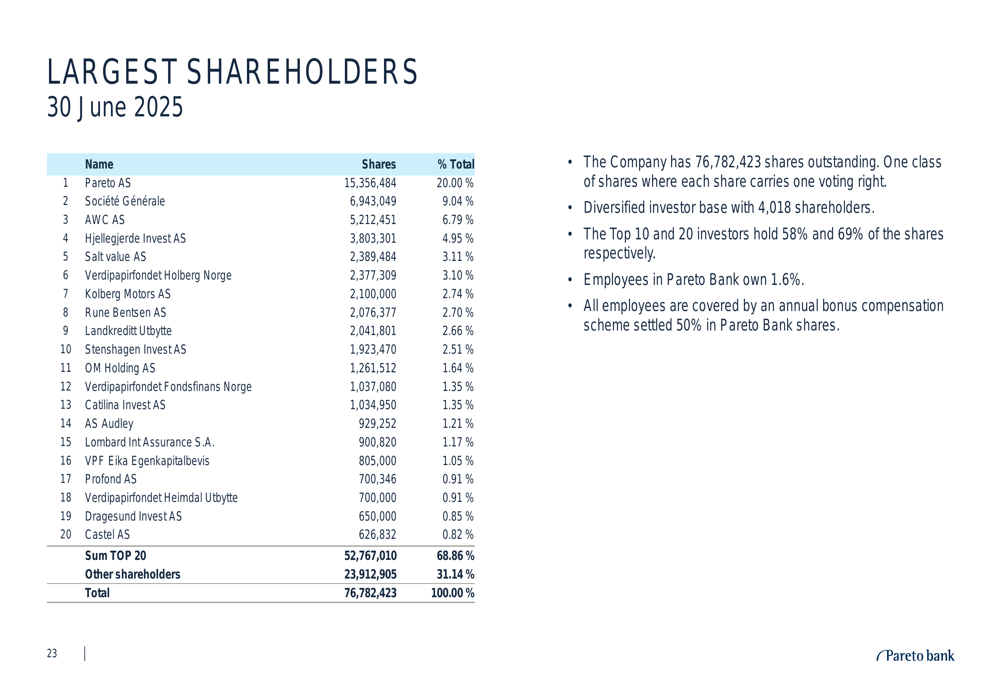

The bank’s shareholder base is diversified with 4,018 shareholders, though relatively concentrated with the top 20 investors holding 68.86% of shares. Pareto AS is the largest shareholder with 20% ownership.

Forward Outlook

While Pareto Bank delivered strong financial results in Q2 2025, management provided a cautious outlook for the coming quarters. The bank expects flat or decreased lending volumes across most business segments in Q3 2025 due to market conditions and significant loan redemptions.

In the residential property segment, which represents the bank’s largest exposure, management highlighted a persistently weak market with record low residential starts and noted that more time is needed to meet pre-sale requirements given the weak demand for new builds. The recent policy rate cut is expected to have a positive but limited effect in the short term.

The corporate financing segment is expected to see flat volume development in Q3 2025, with the bank maintaining a selective credit practice due to differences in activity and profitability across industries. Despite near-term challenges, management emphasized that Pareto Bank remains an attractive partner for medium-sized businesses and sees good long-term growth prospects.

Overall, Pareto Bank’s niche strategy continues to deliver strong returns despite challenging market conditions in some segments. The bank’s robust capital position and consistent profitability provide a solid foundation for navigating the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.