Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Park Hotels & Resorts Inc (NYSE:PK) released its second quarter 2025 earnings presentation on August 1, revealing mixed results that disappointed investors despite a slight revenue beat. The lodging REIT, which owns 39 premium-branded hotels with approximately 25,000 rooms, reported a net loss for the quarter, missing analyst expectations and triggering a 1.88% decline in after-hours trading to $10.46.

The company’s stock has been trading within a 52-week range of $8.27 to $16.23, with the current price reflecting ongoing challenges in the hospitality sector. Following the earnings release, Park Hotels’ shares continued their downward trend during regular trading on August 1, falling 2.11% to close at $10.66.

Quarterly Performance Highlights

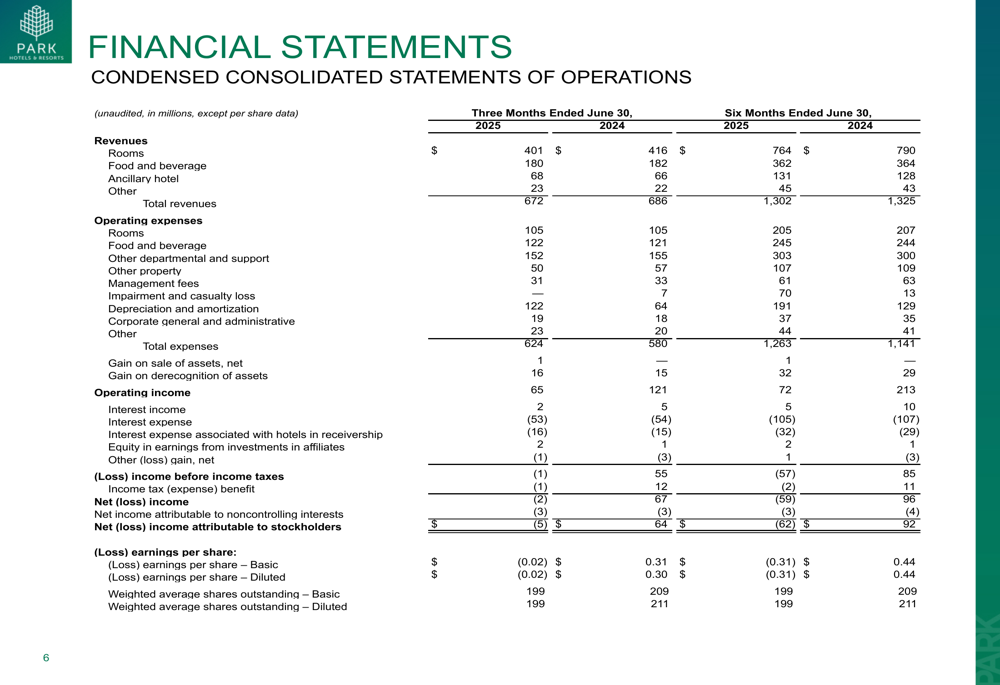

Park Hotels reported total revenues of $672 million for Q2 2025, slightly above analyst expectations of $670 million. However, this represented a decline from $686 million in the same quarter last year. More concerning was the company’s bottom line, which swung to a net loss of $5 million compared to a profit of $64 million in Q2 2024.

The earnings per share figure of -$0.02 significantly missed analyst forecasts of $0.21, resulting in a negative surprise of 109.52%. This disappointing performance was reflected in several key operational metrics, including a 1.6% year-over-year decrease in comparable RevPAR (Revenue Per Available Room) to $195.68.

As shown in the following consolidated statements of operations, the company’s profitability has deteriorated significantly compared to the prior year:

The company’s Adjusted EBITDA also declined to $183 million from $193 million in the prior year period, while the Comparable Hotel Adjusted EBITDA margin contracted to 29.6% from 30.4%. Despite these challenges, Park Hotels managed to maintain relatively stable Adjusted FFO per share at $0.64, compared to $0.65 in Q2 2024.

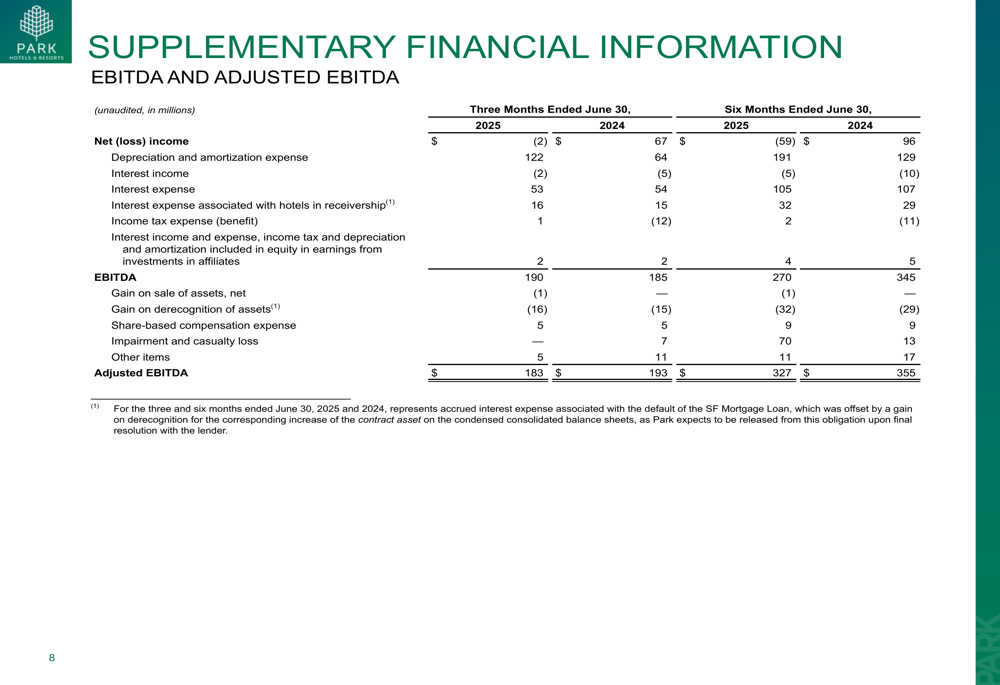

The following table provides a detailed breakdown of the company’s EBITDA performance:

Detailed Financial Analysis

Park Hotels’ balance sheet showed total assets of $8,870 million as of June 30, 2025, down from $9,161 million at the end of 2024. The company maintained a relatively stable debt level of $3,840 million, compared to $3,841 million at year-end 2024.

However, the company’s net debt increased to $3,671 million from $3,582 million, while its leverage ratio deteriorated, with Net Debt to TTM Comparable Adjusted EBITDA rising to 5.88x from 5.53x at the end of 2024. This increasing leverage comes at a time when the company’s operational performance is under pressure.

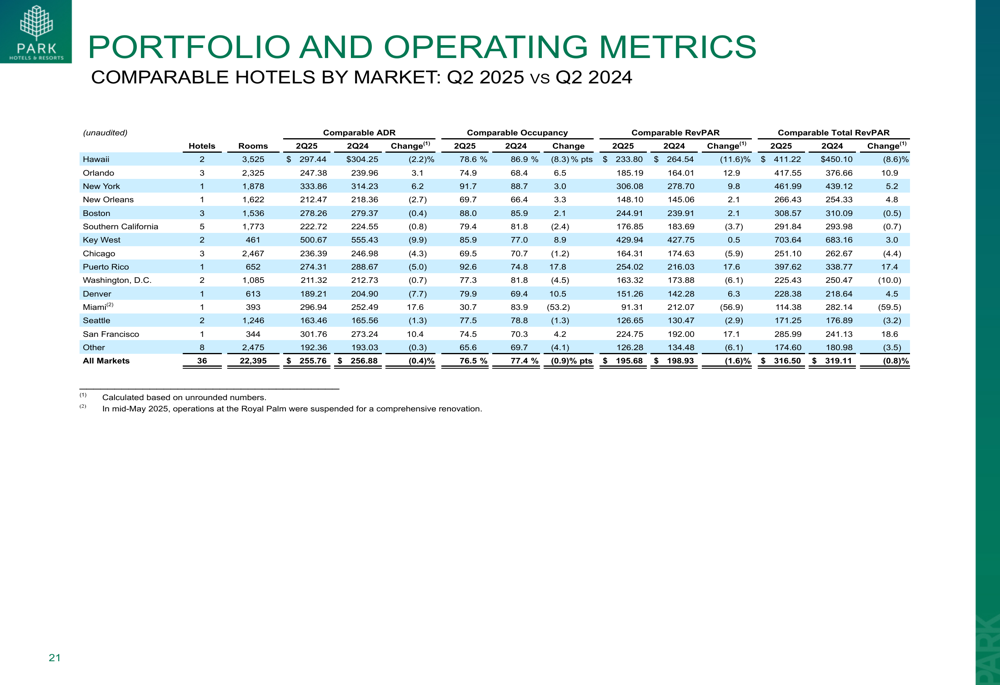

The following slide details the company’s market performance across its portfolio, highlighting the challenges in maintaining RevPAR and occupancy rates:

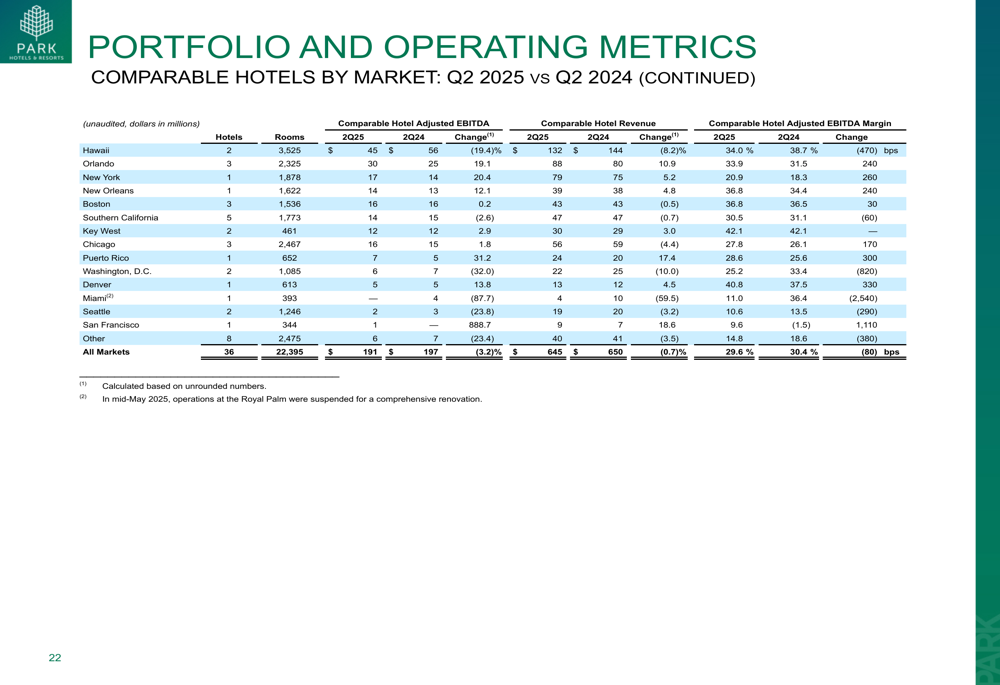

The company’s profitability metrics by market show varying performance, with some markets outperforming others:

Strategic Initiatives

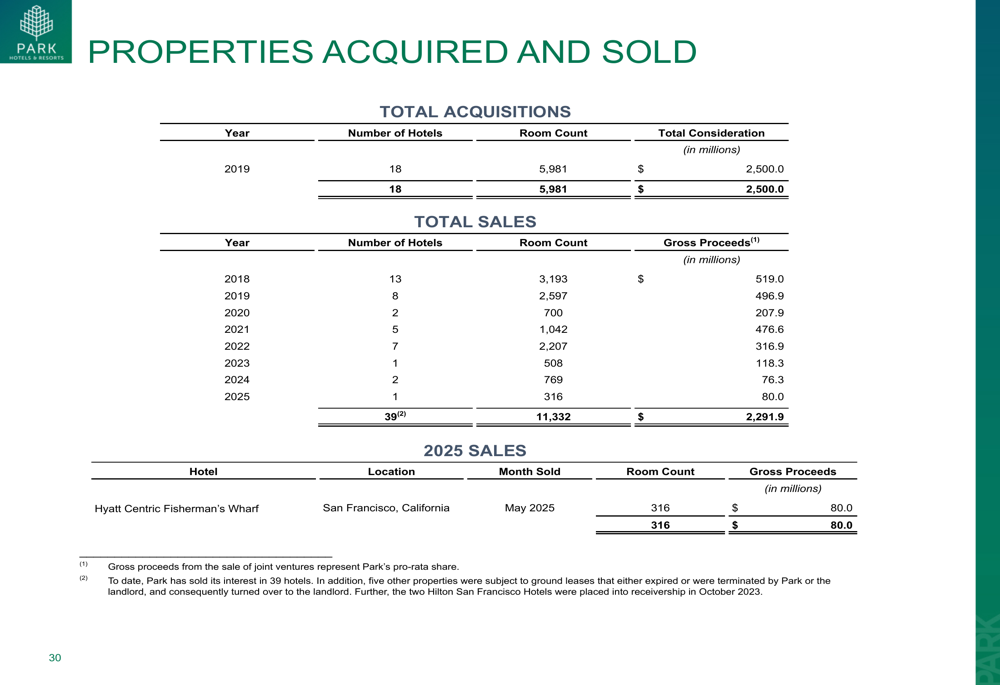

Park Hotels continues to refine its portfolio through strategic asset sales. In May 2025, the company sold the Hyatt Centric Fisherman’s Wharf in San Francisco for $80 million. This transaction is part of a broader strategy that has seen the company divest 39 hotels with 11,332 rooms for a total of $2,291.9 million since 2018.

The following slide summarizes the company’s acquisition and disposition activity:

During the earnings call, CEO Tom Baltimore emphasized the company’s focus on strategic priorities and cost management, stating, "We are laser focused on our strategic priorities and excited about Q3, Q4 and closing out 2025 on a high note." He also noted, "We remain very, very confident in the team’s ability to continue to take cost out of the business."

The company is also undertaking renovations at several properties, including the Royal Palm, which may impact short-term results but are expected to drive future growth.

Forward-Looking Statements

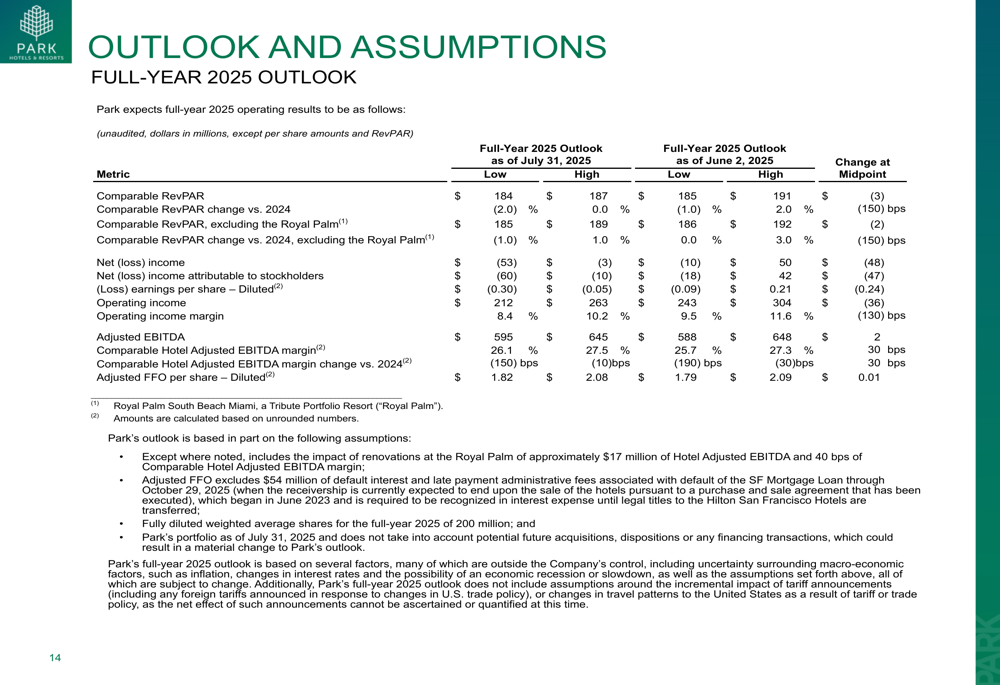

Park Hotels provided a cautious outlook for the full year 2025, projecting a net loss range of $53 million to $3 million and Comparable RevPAR of $184 to $187. The company expects Adjusted EBITDA between $595 million and $645 million, with Adjusted FFO per share projected to be between $1.82 and $2.08.

The detailed outlook is presented in the following slide:

Management anticipates a mixed performance for the remainder of the year, with expected RevPAR declines in Q3 but growth of 3-5% in Q4. The company cited several external risks to its outlook, including macroeconomic trends and tariff considerations.

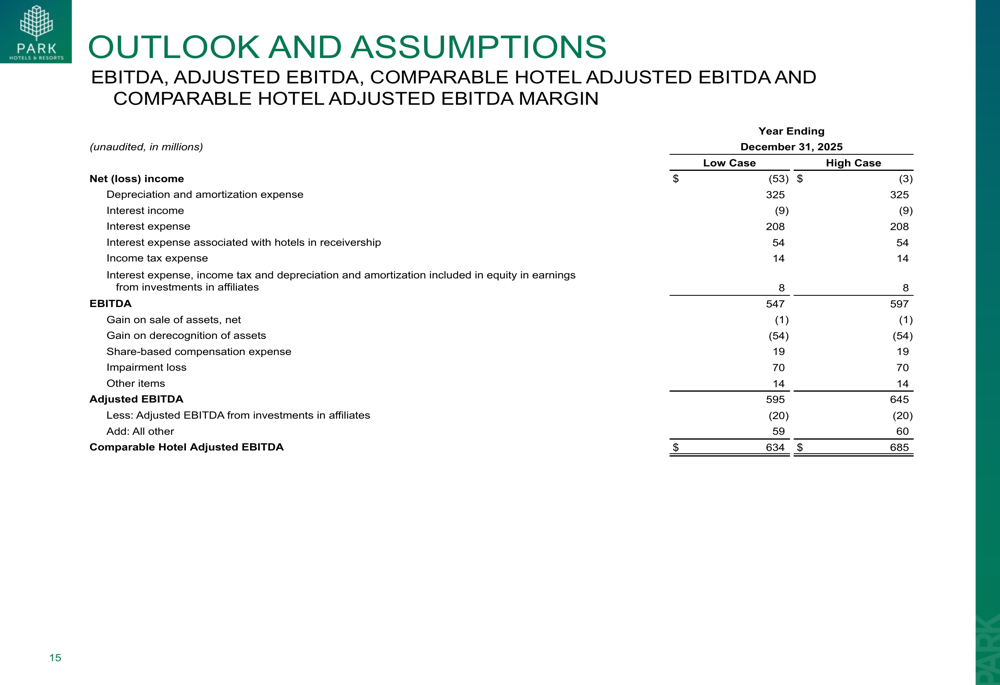

The company’s forward-looking EBITDA projections show the potential range of outcomes based on different scenarios:

While Park Hotels faces near-term challenges, management remains optimistic about the company’s long-term prospects, highlighting its strategic positioning in key markets and ongoing initiatives to enhance property values and operational efficiency. However, investors appear concerned about the company’s ability to navigate the current environment, as reflected in the stock’s performance following the earnings release.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.