JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Park-Ohio Holdings Corp. (NASDAQ:PKOH) presented its first quarter 2025 earnings results on May 7, revealing a 3% year-over-year decline in revenue amid mixed performance across its business segments. The industrial supply chain management company and diversified manufacturer continues to navigate challenging market conditions, with its stock trading near 52-week lows.

The company’s shares closed at $21.14 on May 6, down 1.08% for the day, and have declined significantly from their 52-week high of $34.50. The stock has struggled in recent months following a disappointing fourth quarter 2024 that saw the company miss both EPS and revenue forecasts.

Quarterly Performance Highlights

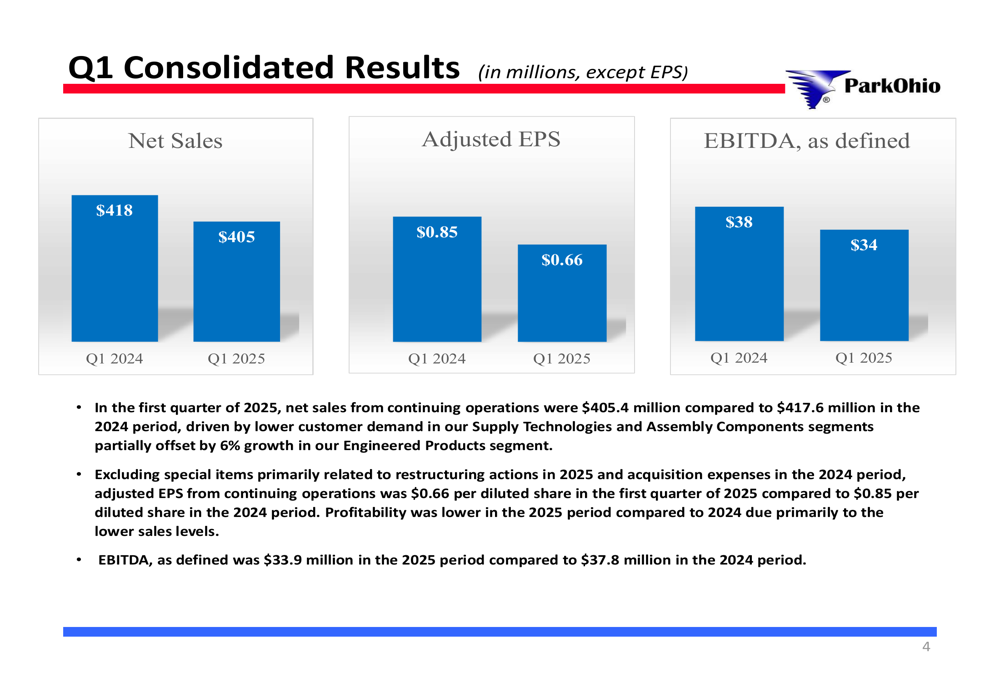

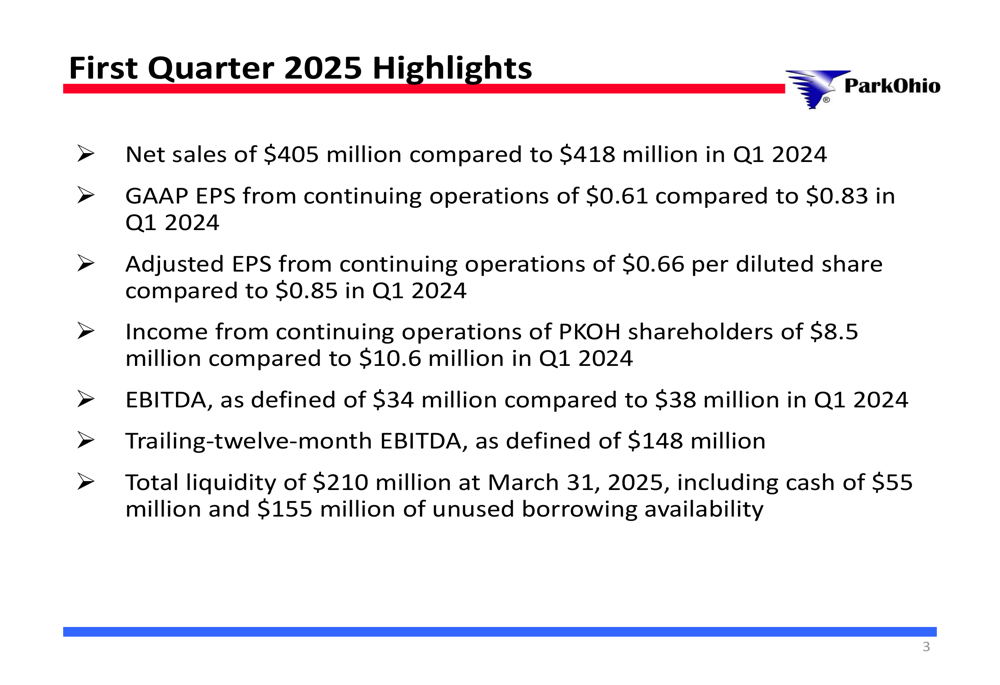

Park-Ohio reported net sales of $405 million for the first quarter of 2025, compared to $418 million in the same period last year. GAAP earnings per share from continuing operations fell to $0.61 from $0.83 in Q1 2024, while adjusted EPS declined to $0.66 from $0.85.

As shown in the following consolidated results chart:

The company’s EBITDA, as defined, was $34 million in Q1 2025, down from $38 million in Q1 2024. Income from continuing operations attributable to Park-Ohio shareholders decreased to $8.5 million from $10.6 million in the prior-year period.

The quarterly results continue a challenging trend for Park-Ohio, which had already reported disappointing results in Q4 2024 when it missed analyst expectations with an EPS of $0.67 against a forecast of $0.71.

Segment Analysis

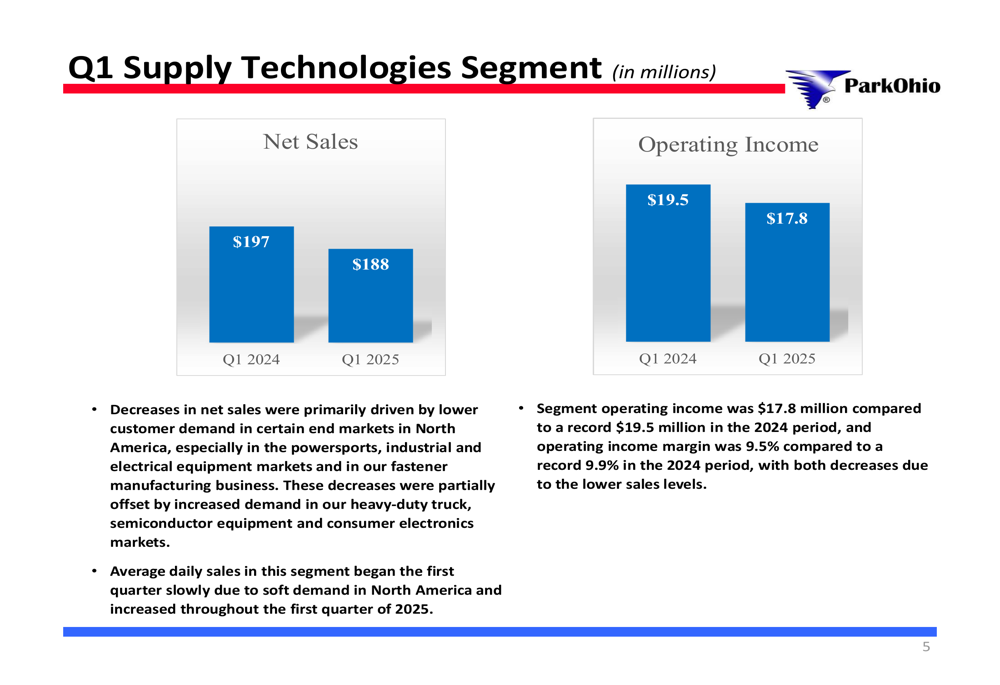

Park-Ohio’s three business segments showed divergent performance in the first quarter. The Supply Technologies segment, which provides supply chain management services, saw net sales decrease to $188 million from $197 million in Q1 2024. Operating income declined to $17.8 million from $19.5 million, with operating margin contracting from 9.9% to 9.5%.

The following chart illustrates the Supply Technologies segment performance:

The company attributed the decline to "lower customer demand in certain end markets in North America," though it noted that average daily sales began slowly but increased throughout the quarter.

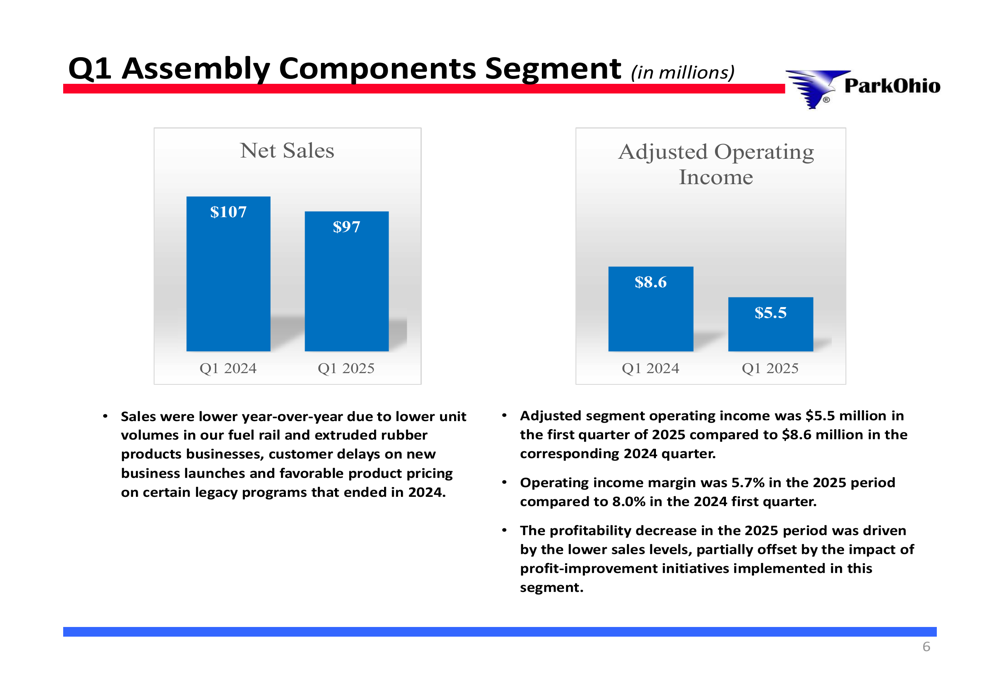

The Assembly Components segment, which manufactures components for the transportation industry, experienced the steepest decline. Sales fell to $97 million from $107 million in Q1 2024, while adjusted operating income dropped to $5.5 million from $8.6 million, as shown here:

The company cited "lower unit volumes in our fuel rail and extruded rubber products businesses, customer delays on new business launches and favorable product pricing on certain legacy programs that ended in 2024" as reasons for the decline. Operating margin contracted significantly from 8.0% to 5.7%.

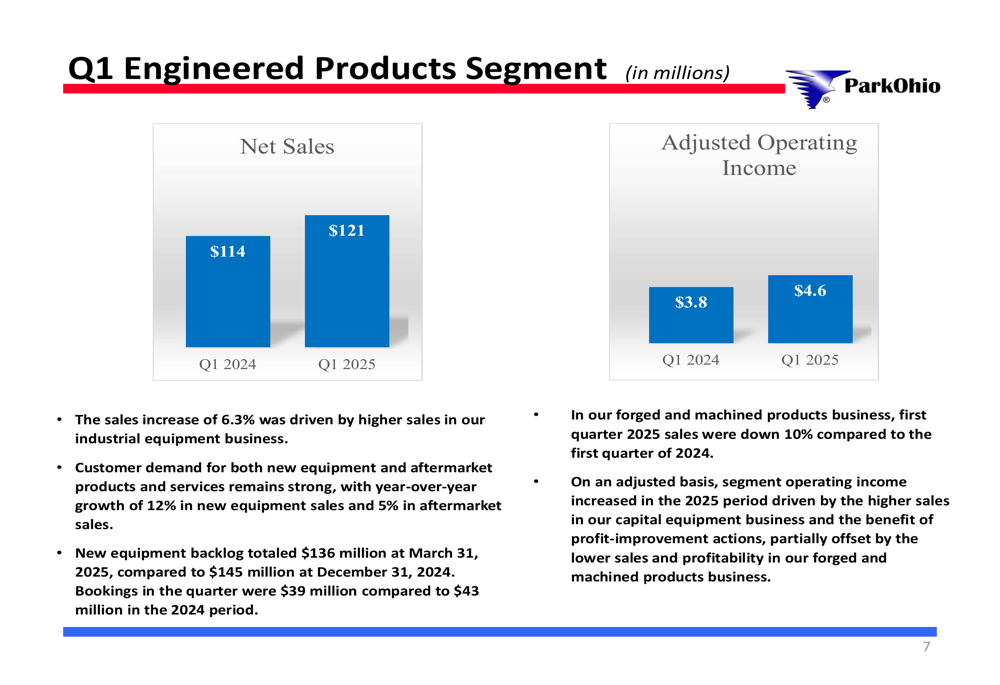

In contrast, the Engineered Products segment was the sole bright spot, with sales increasing 6.3% to $121 million from $114 million in Q1 2024. Adjusted operating income rose to $4.6 million from $3.8 million:

This growth was driven primarily by higher sales in the industrial equipment business, with year-over-year growth of 12% in new equipment sales and 5% in aftermarket sales. However, the segment’s forged and machined products business saw a 10% decline in sales compared to Q1 2024.

Forward Outlook & Guidance

Despite the challenging first quarter, Park-Ohio maintained a cautiously optimistic outlook for the full year 2025. The company projects net sales in the range of $1.6 billion to $1.7 billion and adjusted earnings per share between $3.00 and $3.50.

The company’s first quarter highlights and key metrics are summarized in the following slide:

Management acknowledged the current macroeconomic uncertainty and potential impact of tariffs but expressed confidence in improved free cash flow generation for the year. The company continues to assess the impact of added costs caused by tariffs but believes many of its businesses are well-positioned to benefit from increased localized sourcing in the United States.

This outlook aligns with statements made during the Q4 2024 earnings call, where the company projected revenue growth of 2-4% for 2025. However, the first quarter results showing a 3% decline suggest that achieving this annual growth target may require significant improvement in subsequent quarters.

Financial Position

Park-Ohio maintained a strong liquidity position at the end of Q1 2025, with total liquidity of $210 million, including $55 million in cash and $155 million in unused borrowing availability. This robust liquidity provides the company with financial flexibility as it navigates challenging market conditions.

The company’s trailing twelve-month EBITDA stood at $148 million, reflecting the cumulative impact of recent quarterly performance. While the company didn’t specifically address its debt position in the presentation, previous reports indicated that Park-Ohio operates with a significant debt burden, which remains a consideration for investors.

The non-GAAP reconciliations provided in the presentation detail how the company calculates its adjusted metrics, including the $0.66 adjusted EPS figure, which excludes restructuring charges and their tax effects.

As Park-Ohio moves forward in 2025, investors will be watching closely to see if the company can reverse the negative trends in its Supply Technologies and Assembly Components segments while continuing to build on the positive momentum in Engineered Products.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.