60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

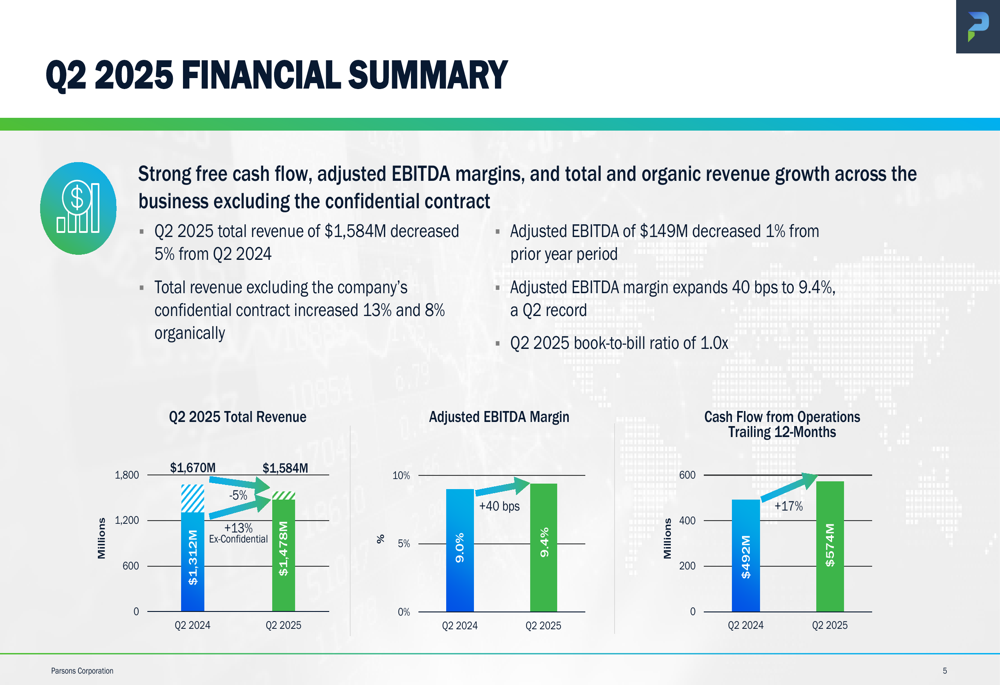

Parsons Corporation (NYSE:PSN) shares fell nearly 8% in premarket trading following the release of its second quarter 2025 earnings presentation on August 6, 2025. The company reported mixed results, with total revenue declining 5% year-over-year to $1.58 billion, though management emphasized 13% growth when excluding a confidential contract.

Quarterly Performance Highlights

Despite the headline revenue decline, Parsons highlighted several positive metrics in its presentation. The company achieved a record Q2 adjusted EBITDA margin of 9.4%, representing a 40 basis point expansion from the prior year period. However, adjusted EBITDA decreased slightly by 1% to $149 million compared to Q2 2024.

As shown in the following financial summary chart:

Cash flow performance remained strong, with cash flow from operations reaching $160 million in Q2 and trailing 12-month cash flow from operations increasing 17% to $612 million. The company also maintained a book-to-bill ratio of 1.0x, continuing its streak of achieving a trailing 12-month book-to-bill ratio of 1.0x or greater in every quarter since its IPO.

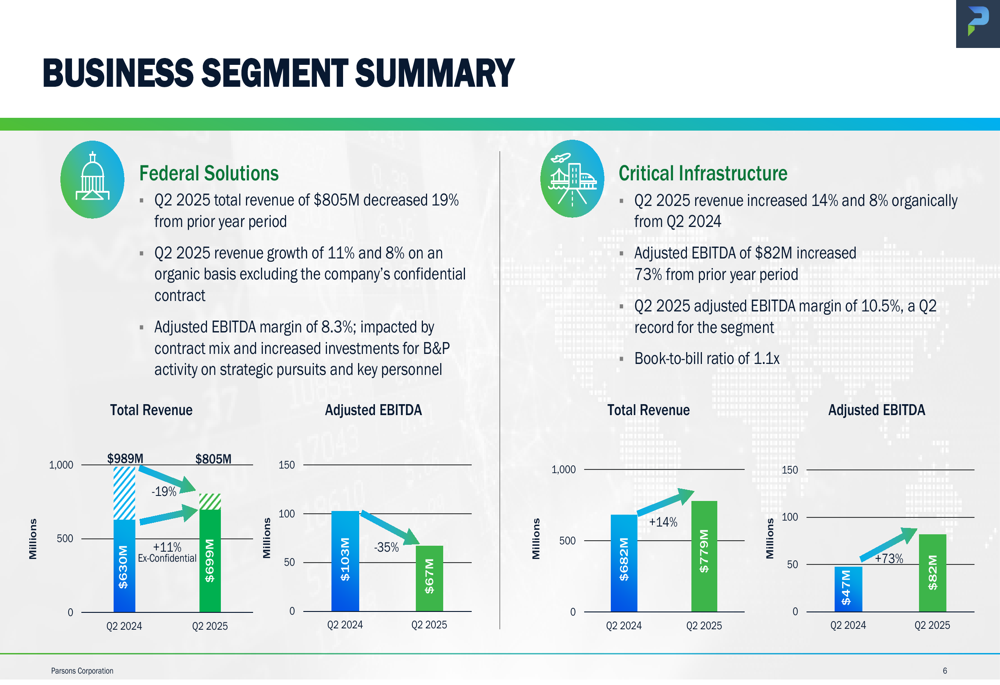

The company's performance varied significantly between its two business segments. The Federal Solutions segment experienced a 19% revenue decline to $805 million, though Parsons noted an 11% increase (8% organic) when excluding the confidential contract. Meanwhile, the Critical Infrastructure segment demonstrated robust growth with revenue increasing 14% (8% organic) to $937 million and adjusted EBITDA surging 73% year-over-year to $82 million.

The following segment breakdown illustrates these contrasting performances:

Strategic Initiatives and Contract Wins

Parsons highlighted its alignment with key administration priorities, positioning itself to capitalize on significant government spending initiatives. The company's presentation emphasized its involvement in areas receiving substantial funding under the reconciliation bill, including FAA modernization ($12.5 billion), border security ($160+ billion), and munitions production ($25 billion).

The company reported several major contract wins during the quarter, including:

- A $176 million single-award contract with the U.S. Army Corps of Engineers for design-build services

- A $138 million task order for cyber operations under the Defense Threat Reduction Agency

- A $134 million extension for remediation projects on the Giant Mine program in Canada

Parsons also completed the acquisition of Chesapeake Technology International (CTI) for $89 million, described as consistent with its strategy of pursuing accretive acquisitions. The company maintained a net debt leverage ratio of 1.5x, suggesting continued financial flexibility for future acquisitions.

Forward-Looking Statements and Guidance

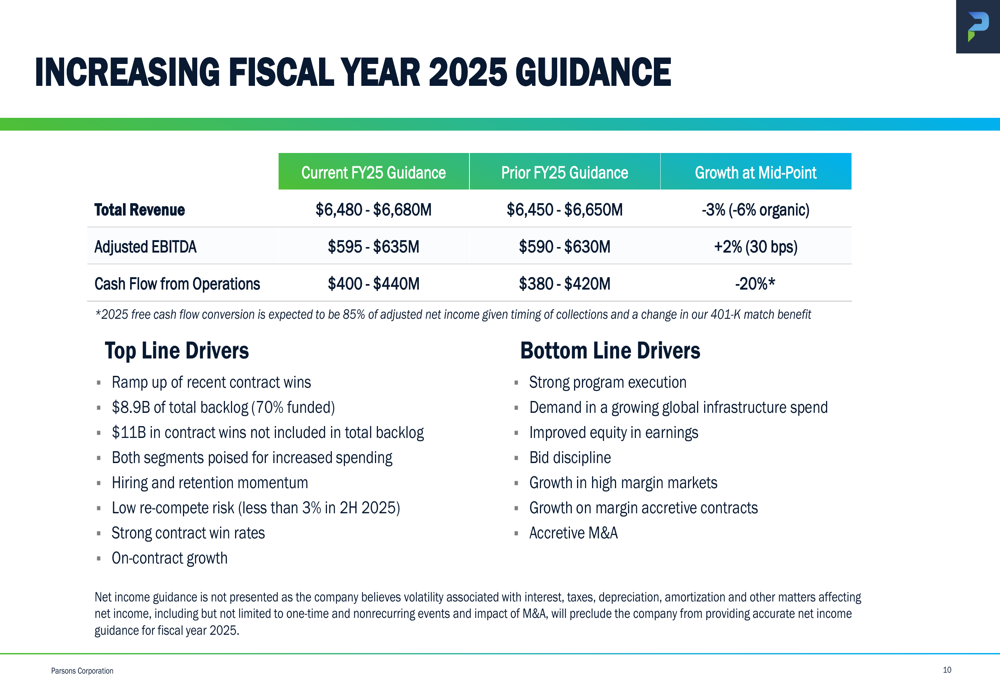

In a positive development, Parsons increased its fiscal year 2025 guidance across all key metrics. The updated outlook, compared to prior guidance, is presented in the following chart:

The company now expects total revenue of $6.48-6.68 billion (previously $6.45-6.65 billion), adjusted EBITDA of $595-635 million (previously $590-630 million), and cash flow from operations of $400-440 million (previously $380-420 million).

Management cited several factors supporting this improved outlook, including:

- Ramp up of recent contract wins

- Record backlog of $8.9 billion (70% funded)

- Additional $11 billion in contract wins not included in total backlog

- Strong program execution

- Growth in high-margin markets

- Accretive M&A activity

Market Reaction and Analysis

Despite the raised guidance and positive adjusted metrics, investors appeared focused on the overall revenue decline, sending Parsons shares down 7.78% to $71.01 in premarket trading. This reaction follows a period of volatility for the stock, which had gained 3.22% to close at $77.00 in the previous session.

The market response may reflect concerns about the company's reliance on adjusted figures and growth calculations that exclude the confidential contract. While Parsons maintains a strong backlog and has improved its full-year outlook, the significant revenue decline in the Federal Solutions segment raises questions about the sustainability of growth in this area.

The Q2 results follow a challenging first quarter, where Parsons missed revenue forecasts but exceeded earnings expectations. The company's performance continues to show a divergence between headline numbers and adjusted metrics, creating a complex picture for investors to evaluate.

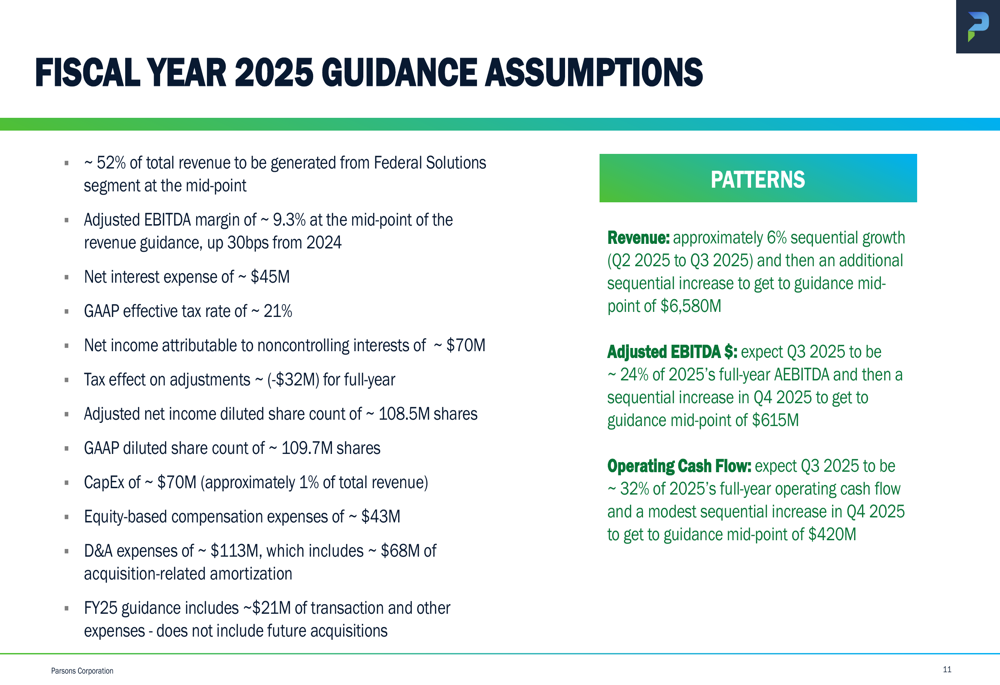

Looking ahead, Parsons expects approximately 52% of total revenue to come from the Federal Solutions segment, with an adjusted EBITDA margin of approximately 9.3% for the full year. The company's guidance assumptions, detailed below, provide additional context for its outlook:

While Parsons faces near-term challenges, particularly related to the confidential contract impacting its Federal Solutions segment, the company's strong backlog, improving margins, and robust cash flow generation suggest potential for recovery as it executes on its strategic initiatives and capitalizes on infrastructure and defense spending priorities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.