Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

PAVmed Inc . (NASDAQ:PAVM) presented its Q1 2025 business update on May 15, 2025, highlighting a dramatic financial turnaround with net income of $18.6 million compared to a loss of $18.5 million in the same period last year. Despite these positive results, the company’s stock fell 15.45% on the day of the presentation, trading at $0.62 per share, reflecting ongoing market skepticism about the medical technology company’s long-term prospects.

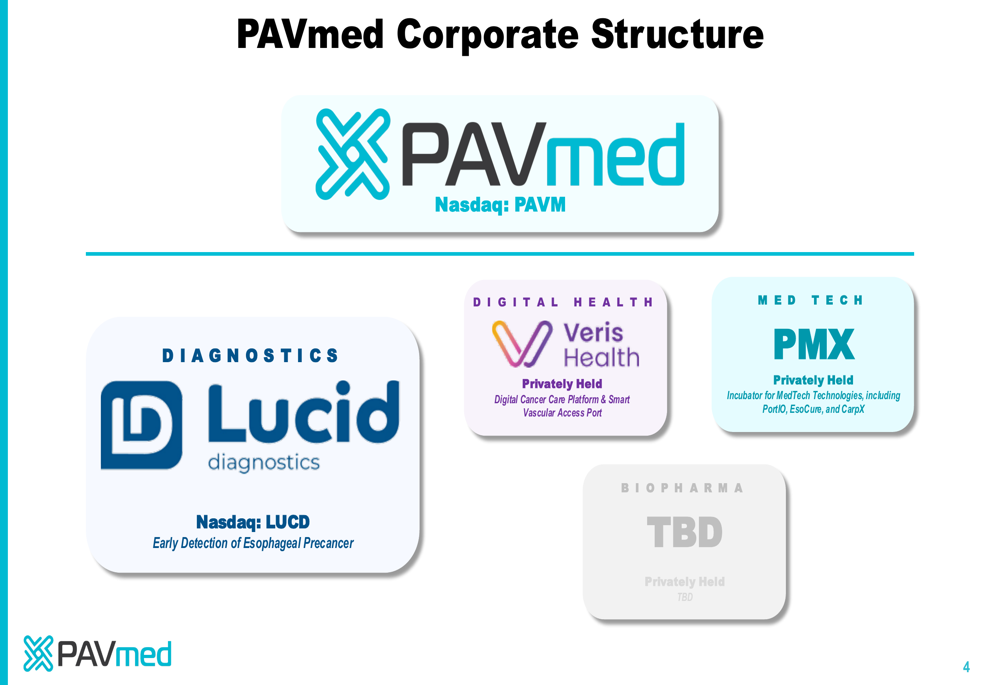

The presentation, delivered by Chairman & CEO Lishan Aklog, MD, and President & CFO Dennis McGrath, outlined the company’s corporate structure, financial improvements, and strategic initiatives across its subsidiaries. PAVmed operates as a parent company with several subsidiaries focused on different medical technology areas.

As shown in the following corporate structure chart, PAVmed’s business spans diagnostics, digital health, and medical device technologies:

Quarterly Performance Highlights

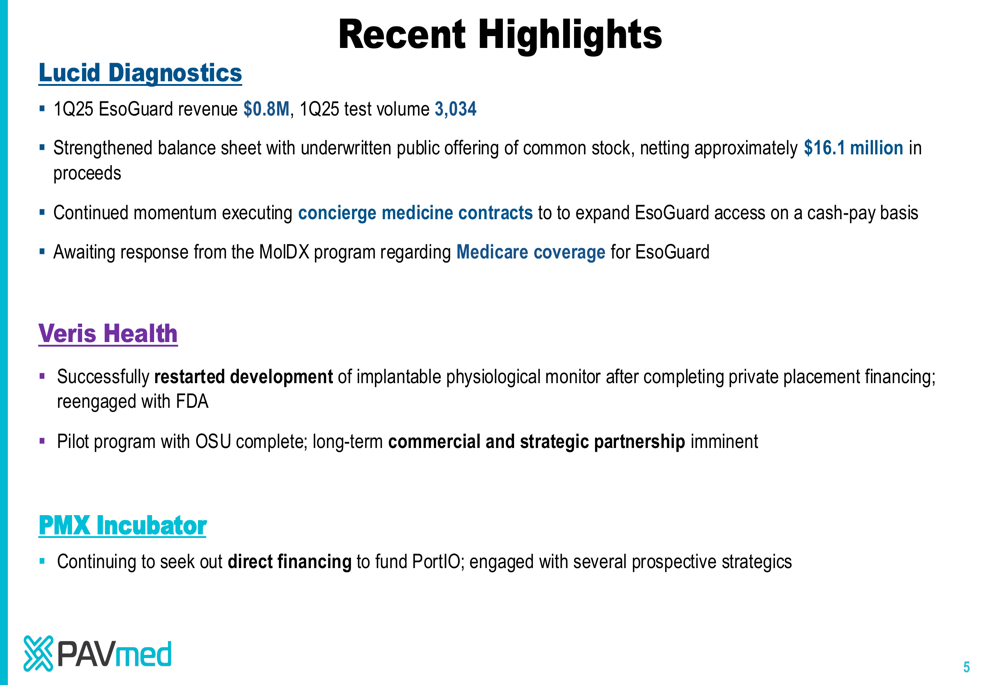

PAVmed reported significant financial improvements in Q1 2025, most notably a dramatic shift to profitability. The company highlighted several key achievements across its business units, including continued progress with its EsoGuard diagnostic test and the restart of development for its implantable physiological monitor after securing financing.

The company’s recent highlights across its subsidiaries show progress in both operational and financial areas:

Revenue from EsoGuard tests reached $0.8 million in Q1 2025, with a test volume of 3,034. While the company continues to await a response from the MolDX program regarding Medicare coverage, it has expanded access through concierge medicine contracts on a cash-pay basis.

Detailed Financial Analysis

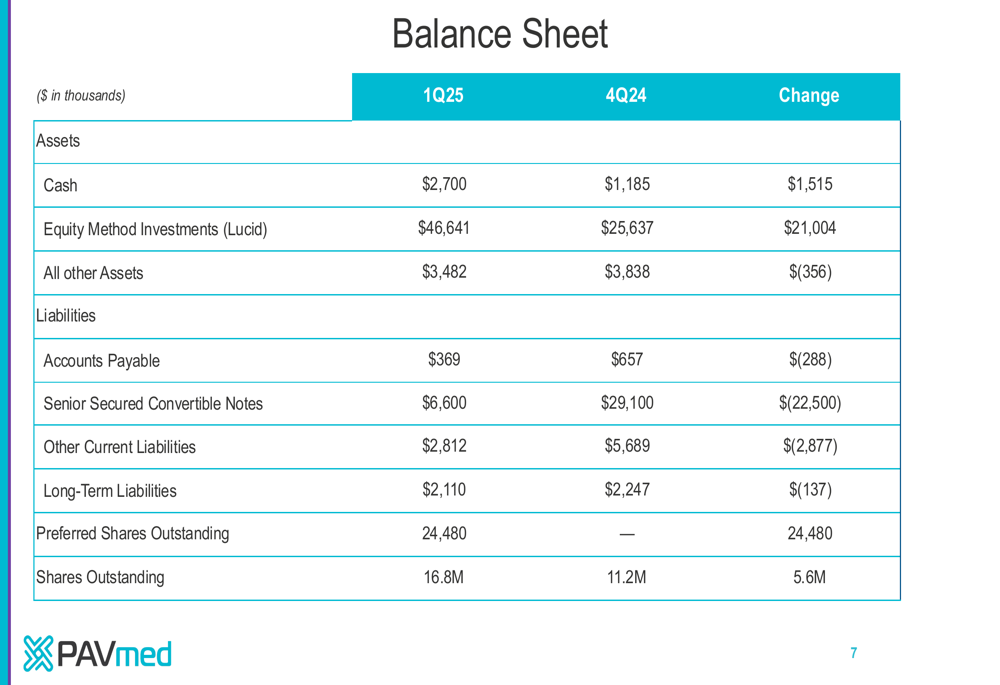

PAVmed’s balance sheet showed substantial improvement in Q1 2025, with cash increasing to $2.7 million from $1.2 million in Q4 2024. The most significant change was in the company’s debt structure, with Senior Secured Convertible Notes reduced by $22.5 million to $6.6 million. This restructuring, which involved exchanging 80% of outstanding debt for preferred equity, has significantly strengthened the company’s financial position.

The detailed balance sheet shows these improvements clearly:

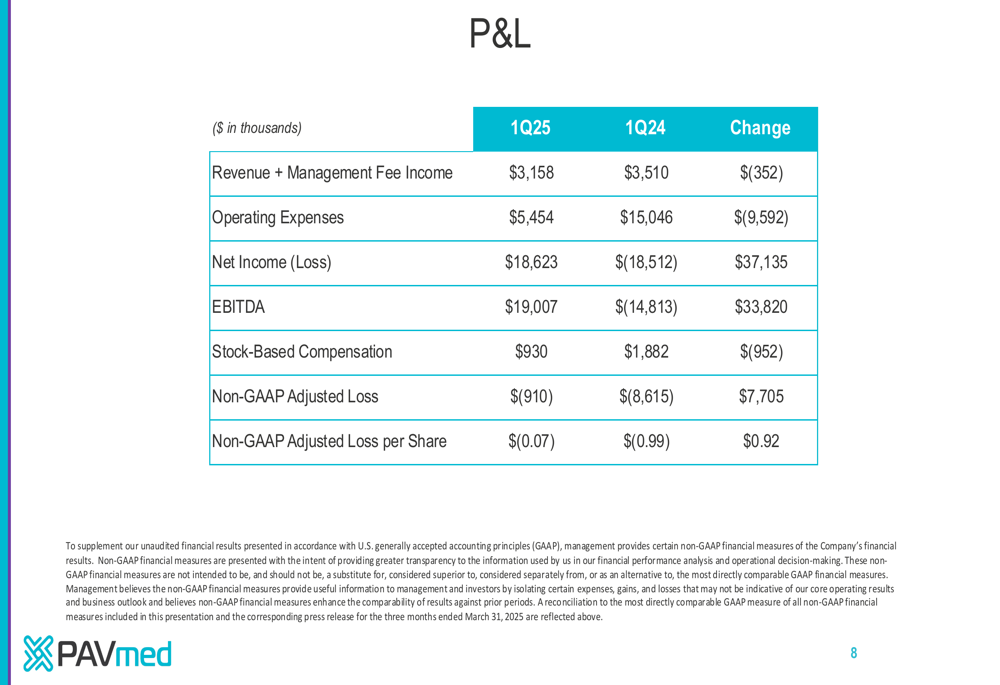

The income statement reveals the dramatic turnaround in PAVmed’s financial performance. Despite a slight decrease in revenue and management fee income to $3.16 million (down from $3.51 million in Q1 2024), the company reported net income of $18.62 million compared to a loss of $18.51 million in the same period last year. This improvement was driven by significantly reduced operating expenses and a substantial gain from the company’s investment in Lucid (NASDAQ:LCID) Diagnostics.

The P&L statement details these financial metrics:

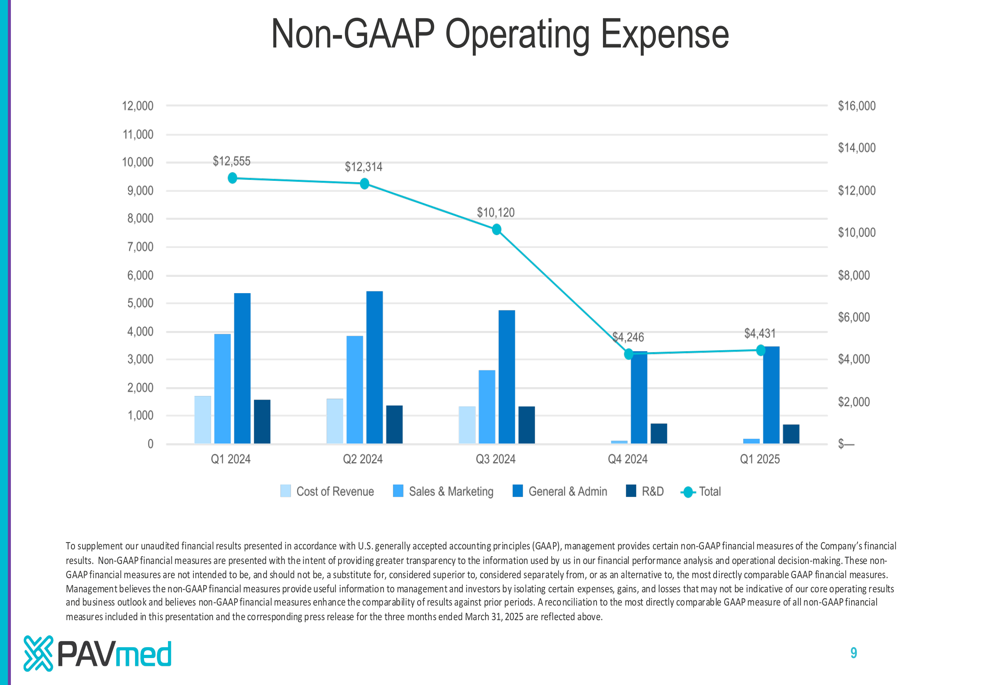

A key factor in PAVmed’s improved financial performance has been its consistent reduction in operating expenses over the past five quarters. Non-GAAP operating expenses have decreased from $12.56 million in Q1 2024 to $4.43 million in Q1 2025, representing a 65% reduction. This cost-cutting has been implemented across all major expense categories, including R&D, general and administrative, and sales and marketing.

The following chart illustrates this consistent downward trend in operating expenses:

Strategic Initiatives

PAVmed’s strategic initiatives center around the development and commercialization of its subsidiaries’ products. Lucid Diagnostics , which is publicly traded (NASDAQ:LUCD), strengthened its balance sheet with an underwritten public offering that netted approximately $16.1 million. The company is focusing on expanding access to its EsoGuard test for early detection of esophageal precancer.

Veris Health has successfully restarted development of its implantable physiological monitor after completing private placement financing. The company has reengaged with the FDA and completed a pilot program with Ohio State University, with a long-term commercial and strategic partnership described as "imminent." According to the earnings call transcript, this partnership is expected to enroll 1,000 patients in its first year, with plans for 300 Verus implants following regulatory clearance.

For its PMX incubator subsidiary, which houses technologies including PortIO, EsoCure, and CarpX, PAVmed is seeking direct financing to fund continued development, particularly for PortIO. The company reported engagement with several prospective strategic partners.

Forward-Looking Statements

PAVmed’s outlook remains cautiously optimistic, with several potential catalysts on the horizon. The company expects a decision on Medicare coverage for its EsoGuard product "imminently," which could significantly impact revenue growth. For Veris Health, the company is targeting an FDA filing for its implantable monitor in the first half of 2026.

Despite these positive developments, PAVmed faces several challenges. The earnings article noted concerning metrics including negative gross profit margins of -61.6% and a current ratio of just 0.06, suggesting potential liquidity concerns despite the improved cash position. The significant stock price decline following the presentation indicates that investors may be focusing on these underlying challenges rather than the headline net income figure.

Analyst price targets for PAVmed range widely from $4 to $19.50, reflecting diverse views on the company’s potential. With a market capitalization of approximately $22.75 million and a year-to-date stock performance of +16.35% prior to the Q1 presentation, PAVmed remains a speculative investment in the medical technology sector, balancing promising technological innovations against financial and regulatory uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.