Street Calls of the Week

Payoneer Global Inc. (NASDAQ:PAYO) shares jumped 11.54% in premarket trading after the cross-border payments company presented its Q2 2025 results on August 6, showing accelerated revenue growth and strong profitability metrics. The positive reception follows a disappointing Q1 when the company missed earnings expectations and temporarily suspended guidance due to concerns about potential tariff impacts.

Quarterly Performance Highlights

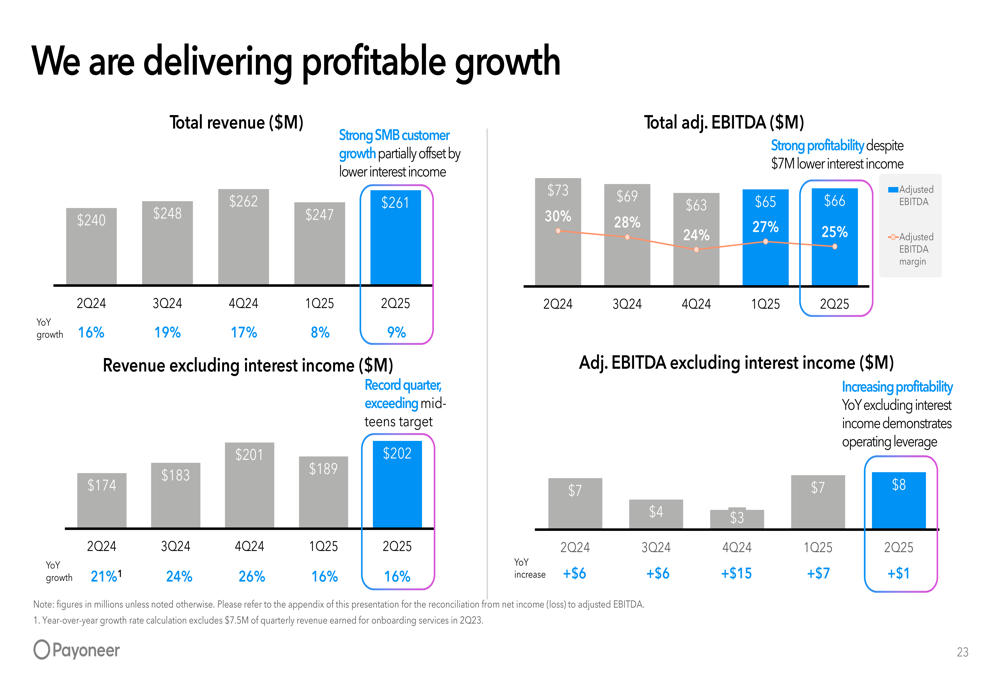

Payoneer reported Q2 2025 revenue of $261 million, representing 9% year-over-year growth. More importantly, revenue excluding interest income reached $202 million, growing at an impressive 16% compared to the same period last year. The company maintained solid profitability with adjusted EBITDA of $66 million, translating to a 25% margin.

As shown in the following chart of quarterly revenue and profitability metrics:

The company’s SMB customer take rate continued its upward trajectory, reaching 1.20% in Q2 2025 compared to 1.11% in Q2 2024. This improvement reflects Payoneer’s strategic focus on higher-value services and optimized pricing strategies.

"We are investing in the future of trade, global, regulated, diverse and powered by entrepreneurs," CEO John Kaplan emphasized during the company’s Q1 earnings call, a strategy that appears to be bearing fruit in Q2 results.

Strategic Growth Initiatives

Payoneer’s presentation highlighted its three-phase journey to become the comprehensive financial stack for global SMBs. Having established itself as a cross-border payments provider (2005-2017) and expanded into B2B payments with additional capabilities (2018-2024), the company is now focused on becoming the comprehensive financial solution for cross-border SMBs worldwide.

The company’s growth strategy centers on five key pillars: prioritizing ideal customer profiles, expanding in underserved regions, investing in high-value products, facilitating access to complementary solutions, and optimizing pricing. This approach has yielded tangible results, including 8% growth in ideal customer profiles (ICPs), approximately 30% revenue growth in APAC and LATAM regions, and 42% volume growth in B2B services.

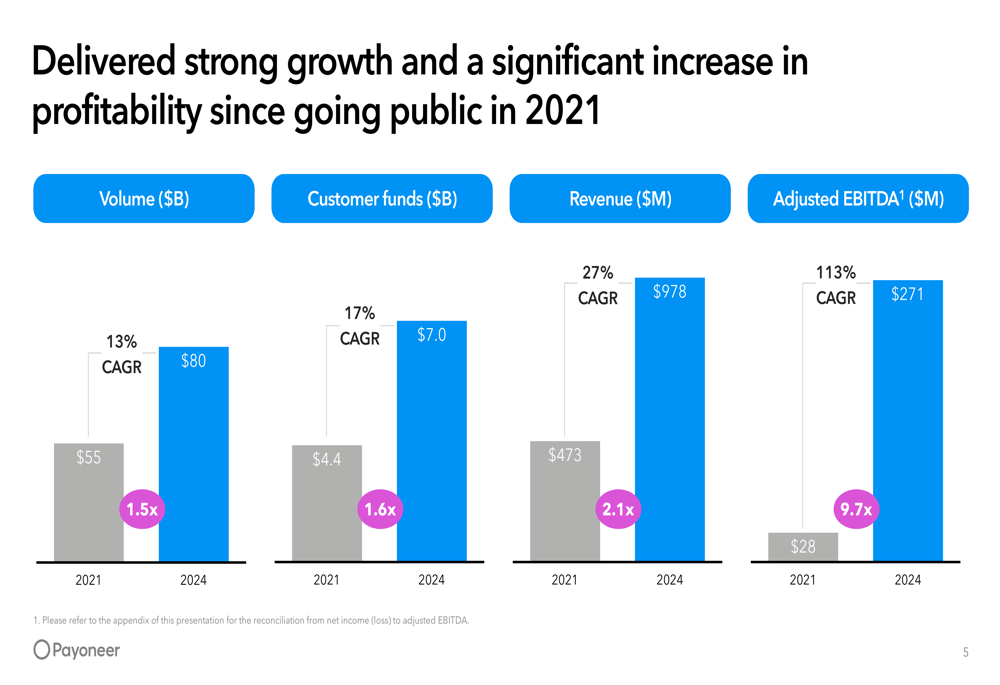

The following chart illustrates Payoneer’s impressive growth trajectory since going public in 2021:

Diversified Business Model

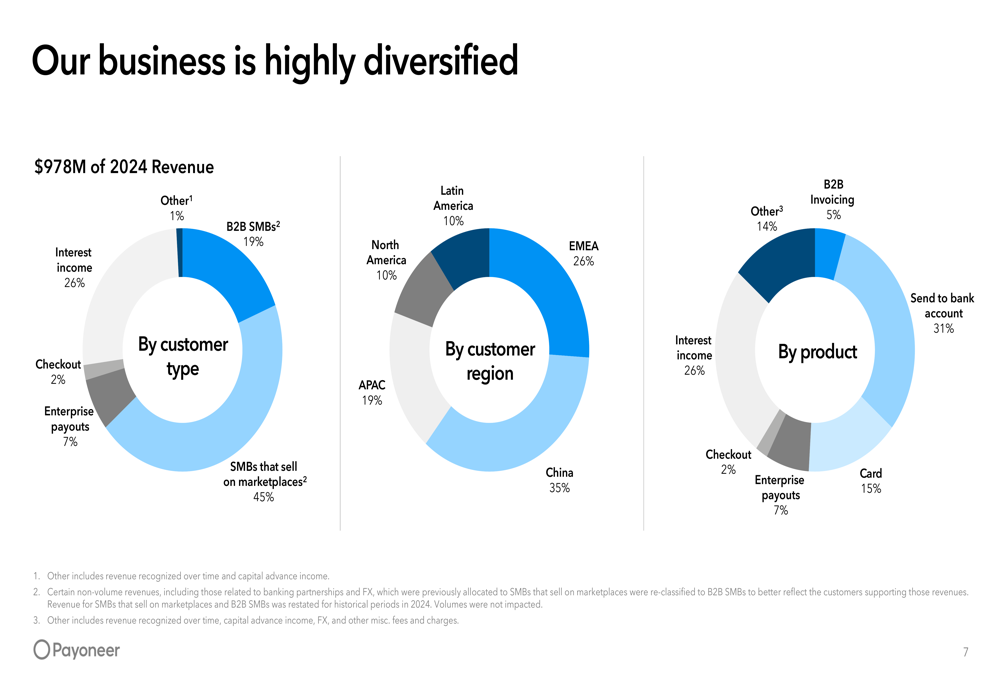

A key strength of Payoneer’s business is its diversification across customer types, regions, and products. The company’s 2024 revenue of $978 million was well-distributed, reducing dependency on any single market segment.

The following breakdown shows Payoneer’s revenue diversification:

This diversification helps insulate the company from regional economic fluctuations and provides multiple growth avenues. Notably, the company has been focusing on expanding in high-take-rate regions such as APAC and LATAM, which have shown revenue growth of 27% and 31% respectively, compared to just 6% in North America.

Customer Focus and ARPU Expansion

Payoneer has strategically focused on its Ideal Customer Profiles (ICPs) - customers processing between $500-$10,000 per month and those processing over $10,000 per month. These segments generate approximately 75% of total revenue despite representing a smaller portion of the customer base.

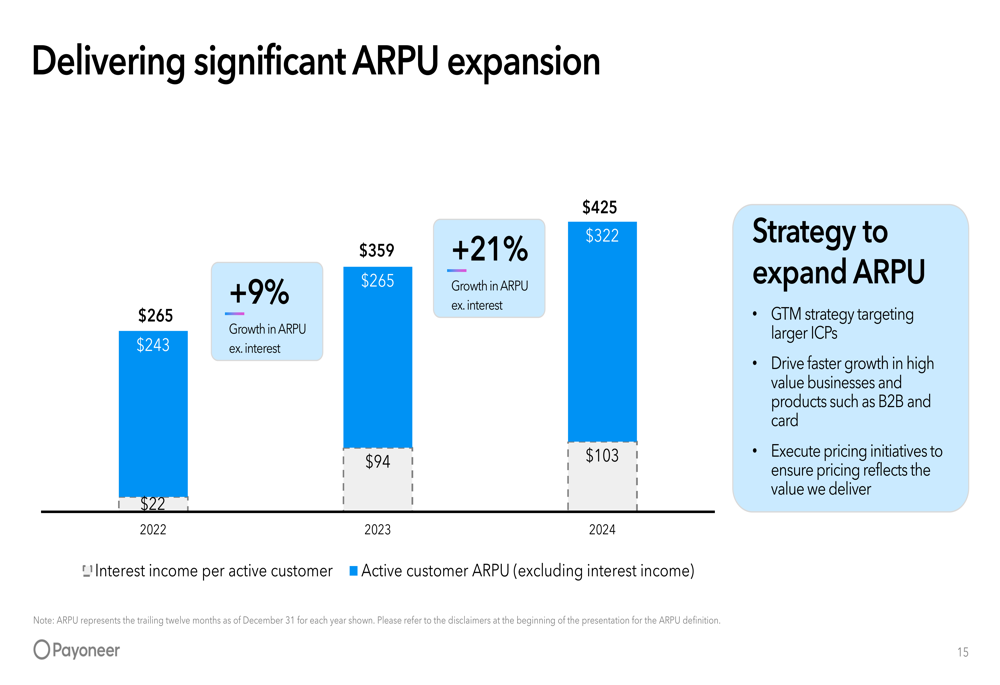

The company reported 559,000 active ICPs in Q2 2025, a 2% year-over-year increase. More impressively, Payoneer has achieved significant ARPU (Average Revenue Per User) expansion, with ARPU increasing from $265 in 2022 to $425 in 2024.

The following chart demonstrates this substantial ARPU growth:

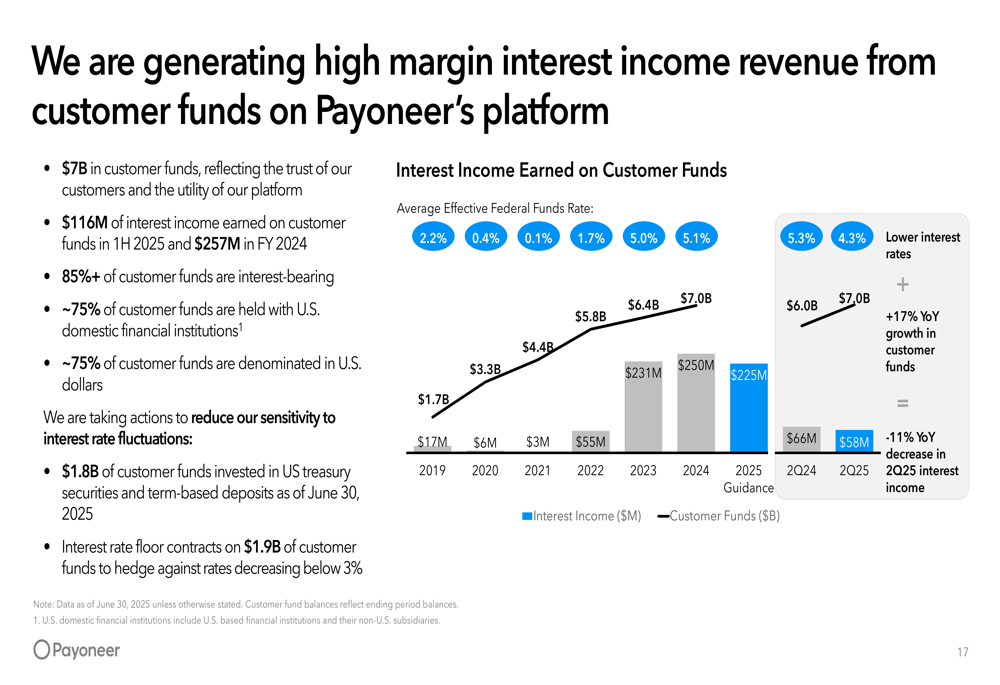

Interest Income as Revenue Driver

An increasingly important component of Payoneer’s revenue stream is interest income generated from customer funds. With $7 billion in customer funds, the company earned $116 million in interest income during the first half of 2025 and $257 million in FY 2024.

The following chart shows the growth in customer funds and corresponding interest income:

For 2025, Payoneer expects to generate $225-$250 million in interest income from approximately $7.0 billion in customer funds, providing a stable revenue source alongside its transaction-based income.

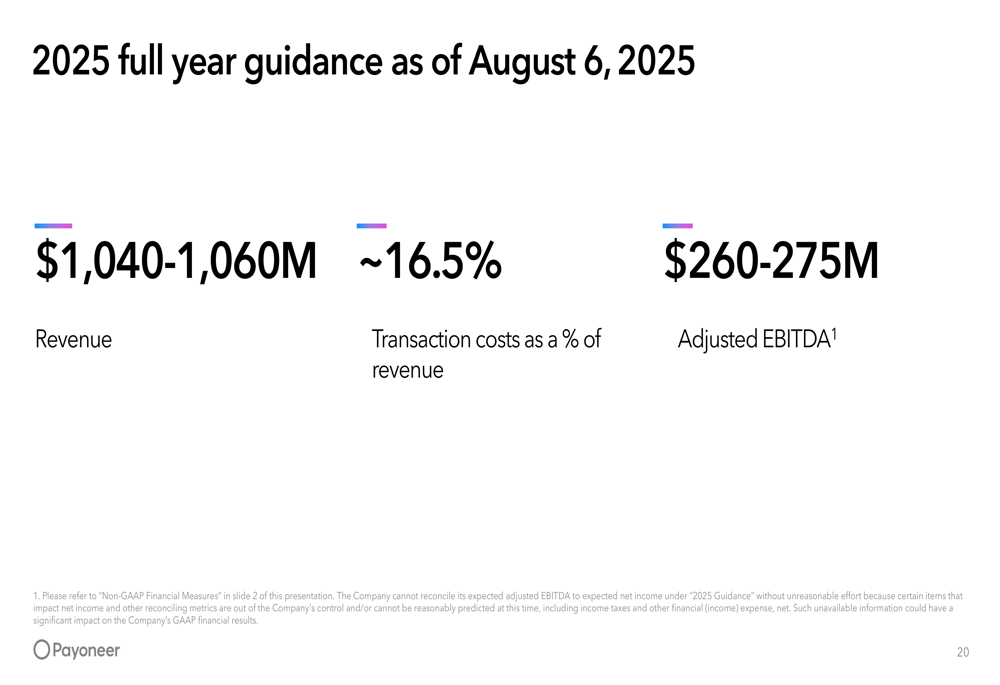

2025 Guidance and Long-Term Outlook

After temporarily suspending guidance following Q1 results due to concerns about potential tariff impacts, Payoneer has reinstated its full-year 2025 guidance. The company now projects revenue of $1,040-1,060 million and adjusted EBITDA of $260-275 million, with transaction costs estimated at approximately 16.5% of revenue.

As shown in the guidance summary:

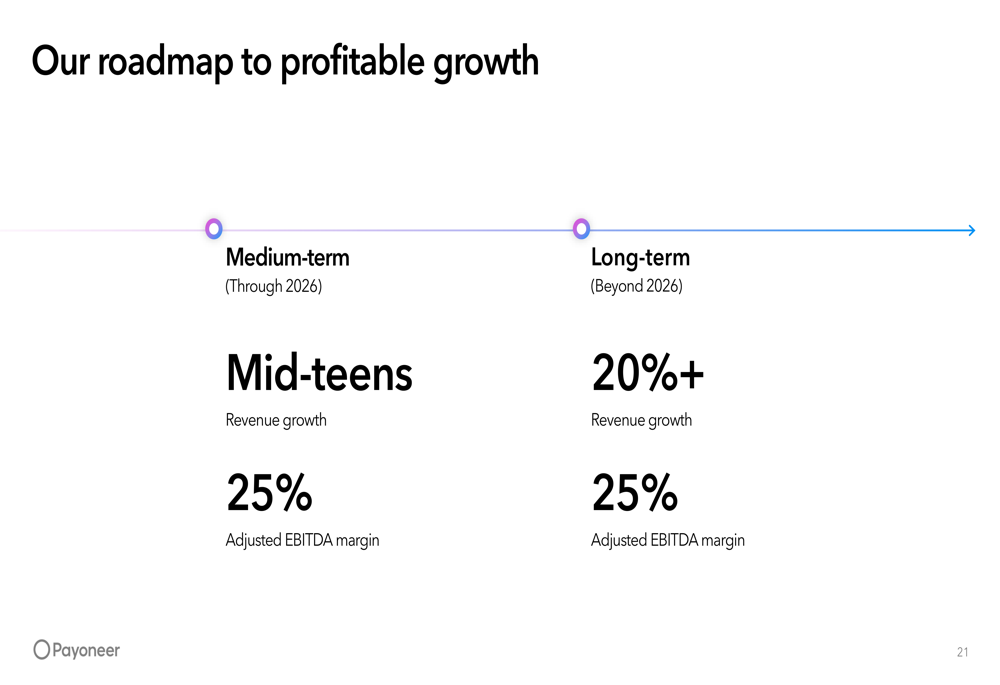

Looking beyond 2025, Payoneer has outlined ambitious but achievable targets. Through 2026, the company aims for mid-teens revenue growth and a 25% adjusted EBITDA margin. Beyond 2026, it targets 20%+ revenue growth while maintaining the 25% adjusted EBITDA margin.

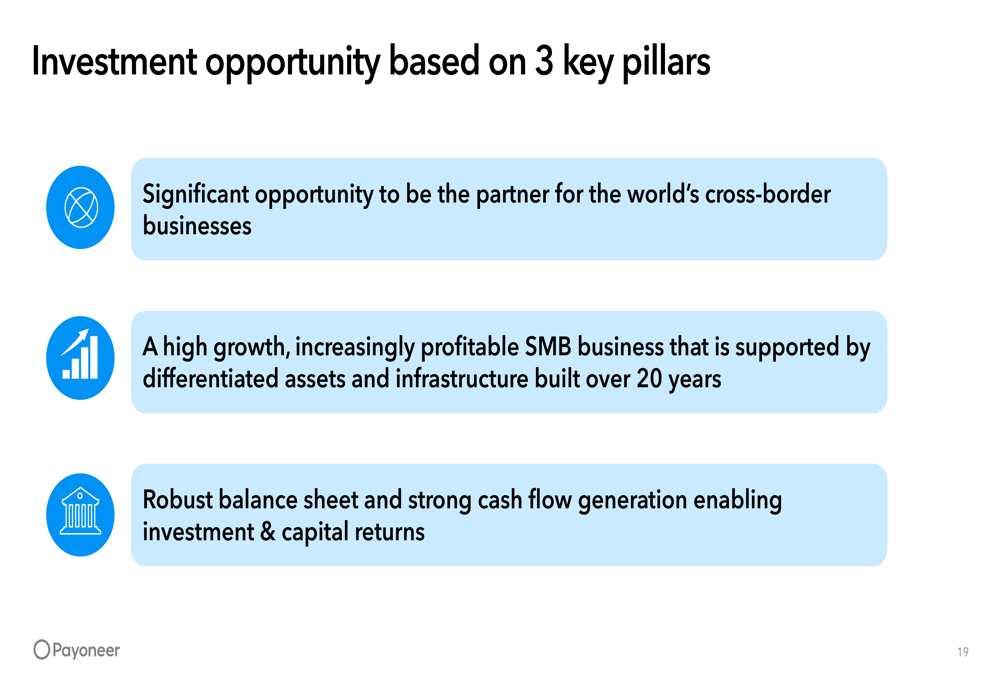

Investment Thesis

Payoneer presents a compelling investment case based on three key pillars: a significant opportunity in cross-border business payments, a high-growth and increasingly profitable SMB business built on differentiated infrastructure, and a robust balance sheet with strong cash flow generation.

The following slide summarizes this investment thesis:

Market Reaction and Outlook

The market’s positive reaction to Payoneer’s Q2 results, with shares up 11.54% in premarket trading, suggests investors are reassured by the company’s performance and guidance after Q1’s disappointment. The stock, which had declined 33.2% over the past six months according to previous reports, appears to be regaining momentum.

Payoneer’s ability to maintain strong revenue growth while generating substantial profitability positions it well in the competitive fintech landscape. The company’s focus on cross-border SMBs, global reach across 190+ countries, and expanding product suite provide multiple avenues for continued growth.

As global trade continues to evolve amid changing economic conditions and regulatory environments, Payoneer’s diversified business model and strong financial position should allow it to navigate challenges while capitalizing on long-term opportunities in digital commerce and cross-border payments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.