IonQ reaches 1,000 patents milestone with new quantum computing grants

PayPal Holdings Inc . (NASDAQ:PYPL) presented its first quarter 2025 financial results on April 29, showing strong profitability metrics despite modest top-line growth. The company’s stock rose 4.71% in premarket trading following the release, suggesting investors responded positively to the results, particularly the significant earnings per share improvement and maintained full-year guidance.

Quarterly Performance Highlights

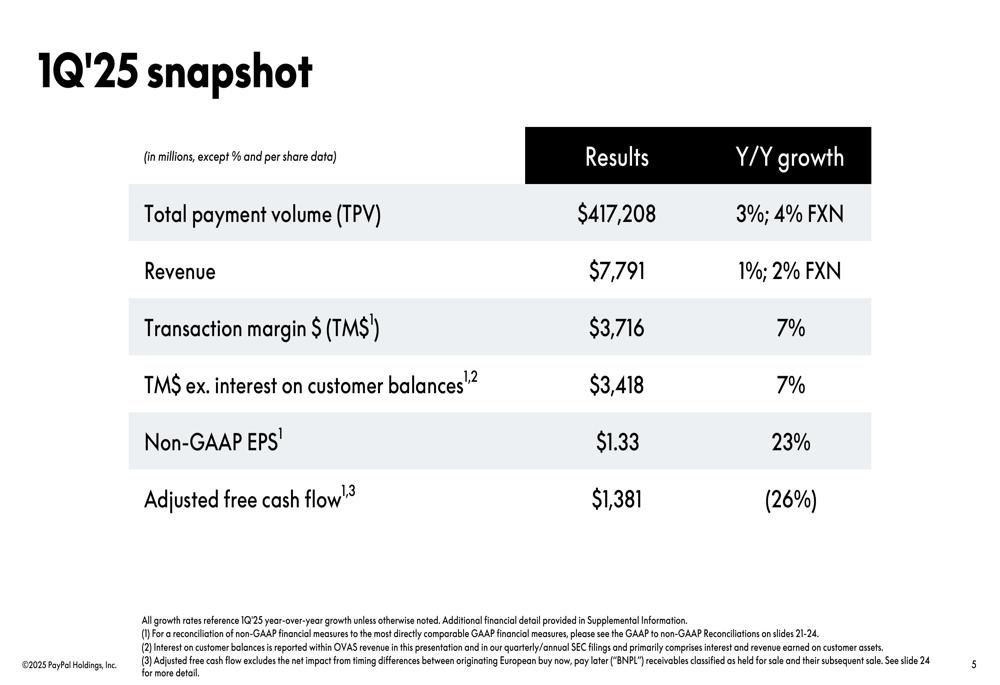

PayPal reported total payment volume (TPV) of $417.2 billion in Q1 2025, representing a 3% year-over-year increase (4% on a foreign exchange neutral basis). While revenue growth was modest at 1% (2% FXN), reaching $7.79 billion, the company delivered substantial improvements in profitability metrics.

Transaction (JO:NTUJ) margin dollars (TM$), a key measure of PayPal’s operational efficiency, grew 7% year-over-year to $3.72 billion. When excluding interest on customer balances, TM$ also increased by 7%, or 8% excluding the Leap Day impact. The transaction margin percentage improved significantly, rising 274 basis points to 47.7%.

As shown in the following financial snapshot, PayPal achieved impressive bottom-line growth with non-GAAP earnings per share increasing 23% to $1.33:

The company maintained its user base growth with active accounts reaching 436 million, up 2% year-over-year. Monthly active accounts also grew by 2% to 224 million. While the total number of payment transactions declined by 7% to 6.05 billion, transactions excluding payment service provider (PSP) activity increased by 6%, reflecting improved engagement in branded checkout and Venmo.

"We’re building on a strong foundation to start the year," noted the company in its presentation, highlighting that the new checkout experience now reaches over 45% of US transactions.

Strategic Initiatives

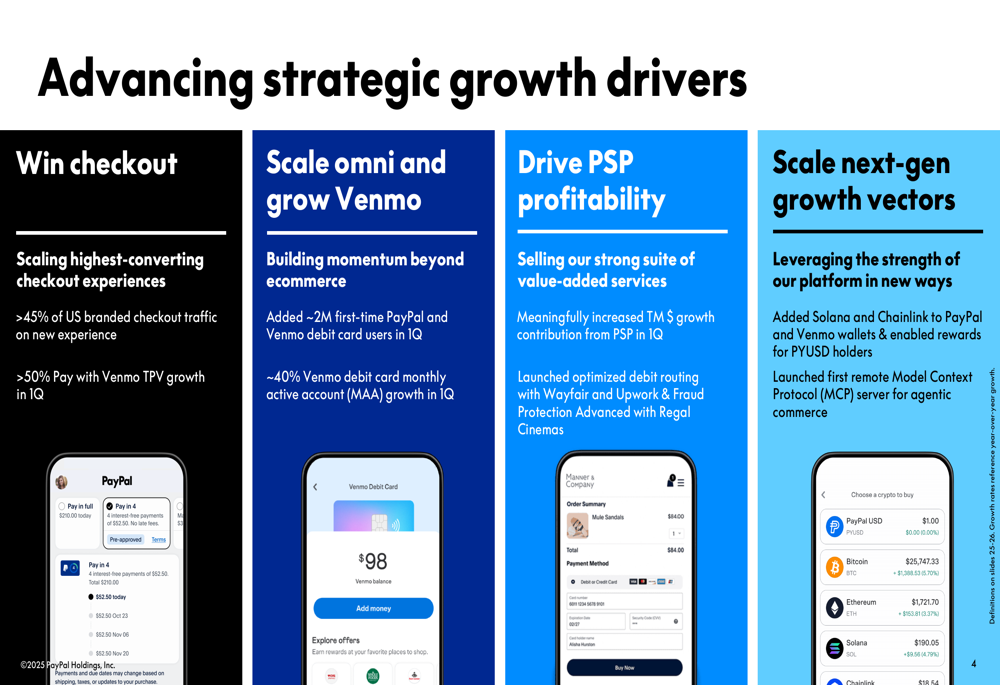

PayPal outlined four key strategic growth drivers that are showing promising results. The company is focusing on winning in checkout, scaling omni-channel capabilities, driving PSP profitability, and developing next-generation growth vectors.

The following slide details these strategic initiatives and their progress:

In the checkout space, PayPal is scaling its highest-converting experiences, with over 45% of US branded checkout traffic now on the new experience. Pay with Venmo TPV growth exceeded 50% in Q1, demonstrating strong momentum in this area.

The company is also building momentum beyond e-commerce, adding approximately 2 million first-time PayPal and Venmo debit card users in Q1. Venmo debit card monthly active accounts grew by approximately 40% year-over-year, while overall debit card TPV growth exceeded 60%.

On the payment service provider front, PayPal reported meaningfully increased TM$ growth contribution from PSP in Q1. The company launched optimized debit routing with Wayfair (NYSE:W) and Upwork (NASDAQ:UPWK), as well as Fraud Protection Advanced with Regal Cinemas.

In next-generation growth vectors, PayPal added Solana and Chainlink to PayPal and Venmo wallets and enabled rewards for PYUSD holders. The company also launched its first remote Model Context Protocol (MCP) server for agentic commerce.

Detailed Financial Analysis

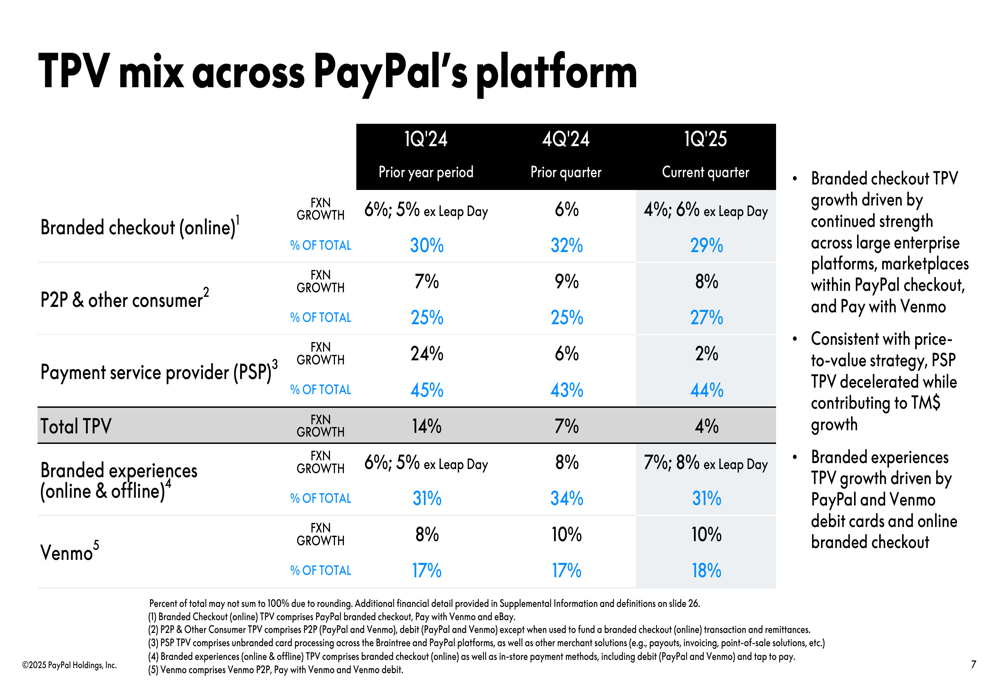

A closer examination of PayPal’s TPV mix reveals interesting trends across different segments of the business. Branded checkout (online) TPV grew 6% excluding Leap Day, while branded experiences TPV (including both online and offline) increased by 8% excluding Leap Day. Venmo continued its strong performance with 10% TPV growth, now representing 18% of total TPV.

The following table provides a comprehensive breakdown of TPV across PayPal’s platform:

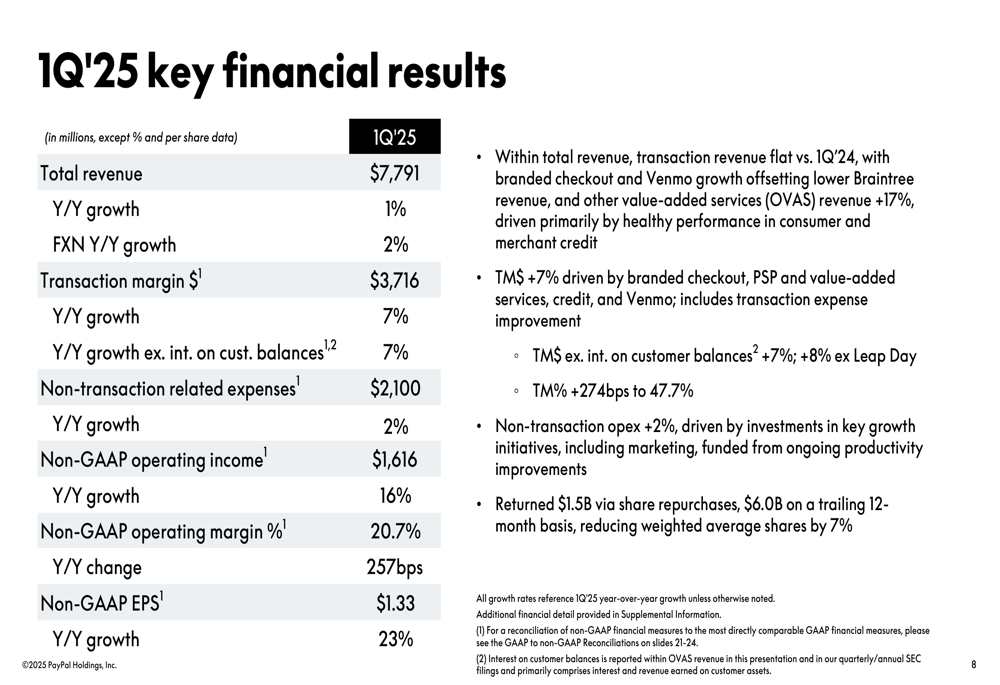

PayPal’s financial results show strong profitability improvements despite modest revenue growth. Transaction revenue was flat compared to Q1 2024, with branded checkout and Venmo growth offsetting lower Braintree revenue. Other value-added services (OVAS) revenue grew 17%, driven primarily by healthy performance in consumer and merchant credit.

Non-transaction related expenses increased by just 2% year-over-year to $2.1 billion, reflecting the company’s focus on productivity improvements while investing in key growth initiatives. This disciplined approach to expenses, combined with revenue growth and transaction margin improvement, led to a 16% increase in non-GAAP operating income to $1.62 billion. The non-GAAP operating margin expanded by 257 basis points to 20.7%.

The following slide details these key financial results:

PayPal continued its strong capital return program, repurchasing $1.5 billion in shares during Q1, bringing the trailing 12-month total to $6.0 billion. These repurchases reduced the weighted average share count by 7%, contributing to the strong EPS growth.

Forward-Looking Statements

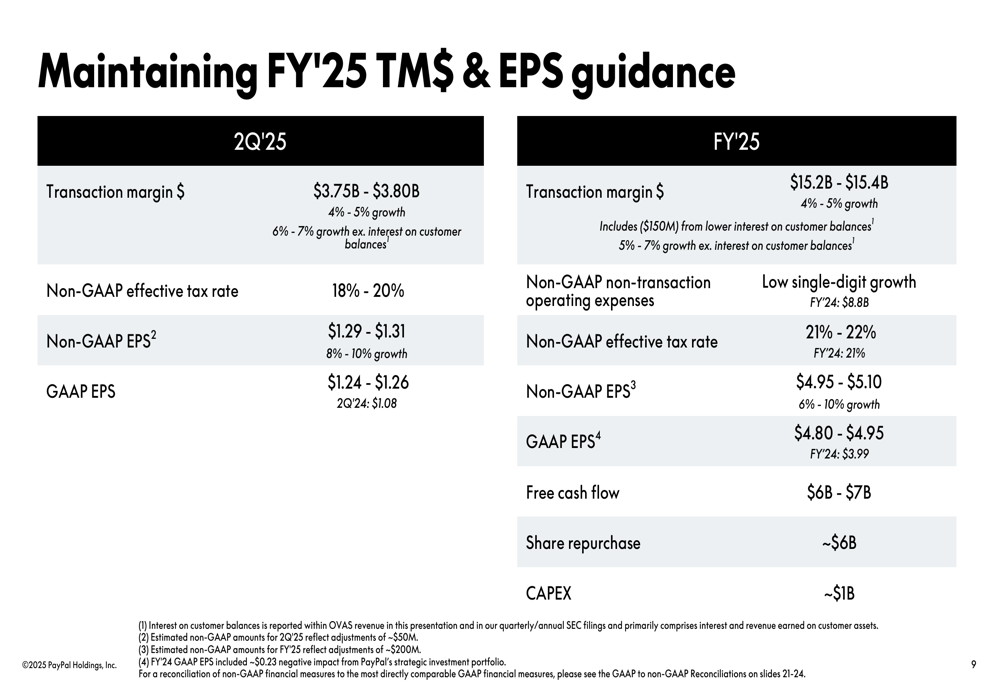

Despite the strong Q1 performance, PayPal is maintaining its full-year 2025 guidance due to global macroeconomic uncertainty. For the second quarter of 2025, the company expects transaction margin dollars of $3.75-$3.80 billion (4-5% growth, or 6-7% excluding interest on customer balances) and non-GAAP EPS of $1.29-$1.31 (8-10% growth).

For the full year 2025, PayPal continues to project:

- Transaction margin dollars of $15.2-$15.4 billion (4-5% growth, or 5-7% excluding interest on customer balances)

- Low single-digit growth in non-GAAP non-transaction operating expenses

- Non-GAAP EPS of $4.95-$5.10 (6-10% growth)

- Free cash flow of $6-$7 billion

- Share repurchases of approximately $6 billion

The following guidance slide provides additional details:

"We delivered another quarter of profitable growth," PayPal stated in its presentation summary. "We’re making meaningful progress on our strategic transformation, focused on driving scale and adoption of innovations to deliver for our customers."

The company emphasized its proven foundation with multiple growth drivers including branded checkout, Venmo, omni-channel capabilities, PSP, and next-generation growth vectors. While noting a strong start to Q2, management is maintaining full-year guidance due to global macroeconomic uncertainty.

PayPal’s Q1 2025 results demonstrate the company’s ability to drive profitability improvements even as payment volume growth moderates. With strategic initiatives showing positive momentum and a disciplined approach to expenses, PayPal appears well-positioned to navigate the uncertain global economic environment while continuing to deliver value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.