Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Paysafe (NYSE:PSFE) presented its first quarter 2025 earnings results on May 13, 2025, revealing a mixed financial performance characterized by declining reported revenue but positive organic growth. The payment solutions provider continues to navigate a strategic shift toward its unified wallet platform while focusing on product innovation, sales efficiency, new partnerships, and network leverage to drive future growth.

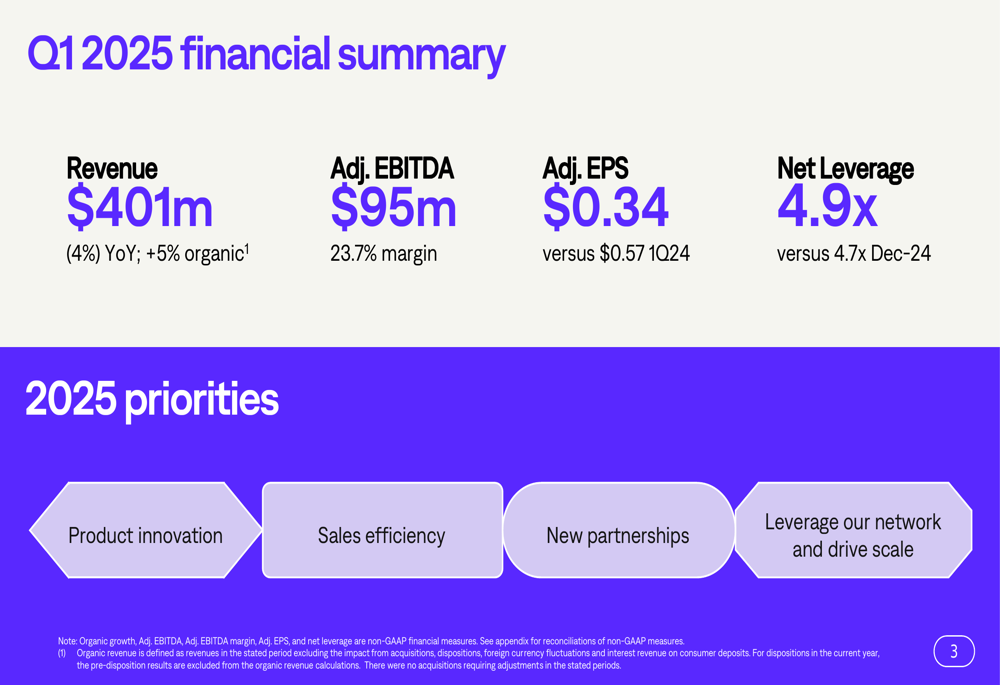

The company reported a 4% year-over-year decline in revenue to $401 million, while highlighting 5% organic growth after adjusting for business disposals, currency fluctuations, and interest revenue. Despite the organic growth, Paysafe saw declines in profitability metrics, with adjusted EBITDA falling 15% to $95 million and adjusted EPS dropping to $0.34 from $0.57 in the prior-year period.

Quarterly Performance Highlights

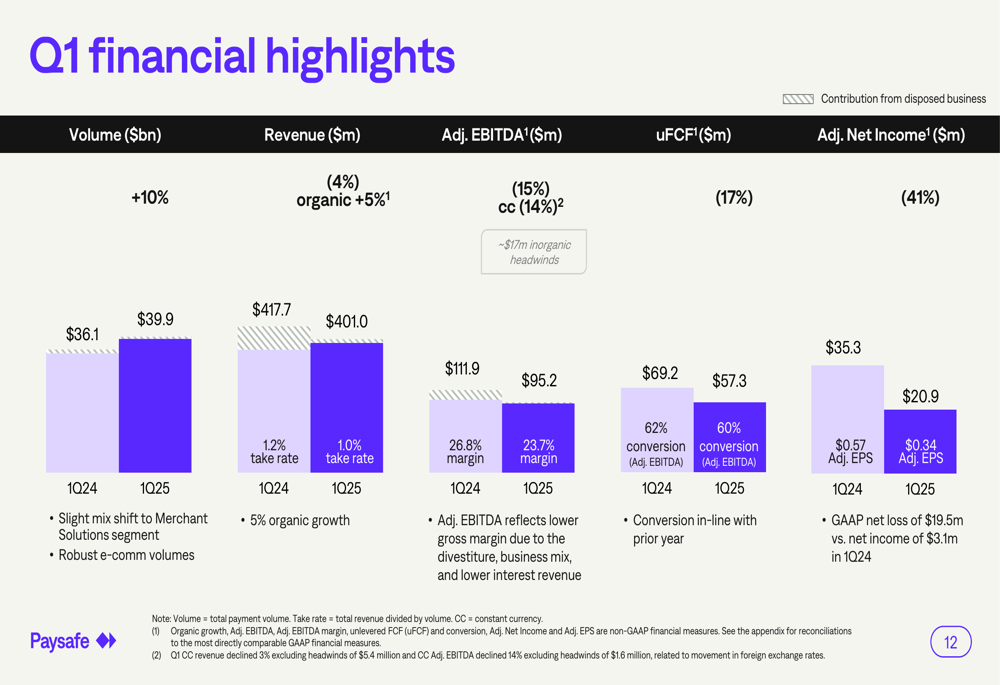

Paysafe’s Q1 2025 financial results showed transaction volume growth of 10% to $39.9 billion, demonstrating continued expansion in payment processing activity despite the revenue decline. The company maintained a take rate of 1.0% and a conversion rate of 60%, in line with the previous year.

As shown in the following financial summary from the presentation:

The company’s adjusted EBITDA margin compressed to 23.7% from 26.8% in the prior-year period, while net leverage increased slightly to 4.9x from 4.7x at the end of 2024. Paysafe continued its debt reduction efforts with a $23 million principal debt prepayment during the quarter, while also repurchasing 613,000 shares for $10 million at an average price of $16.32.

A detailed breakdown of Q1 financial metrics reveals the extent of the year-over-year changes:

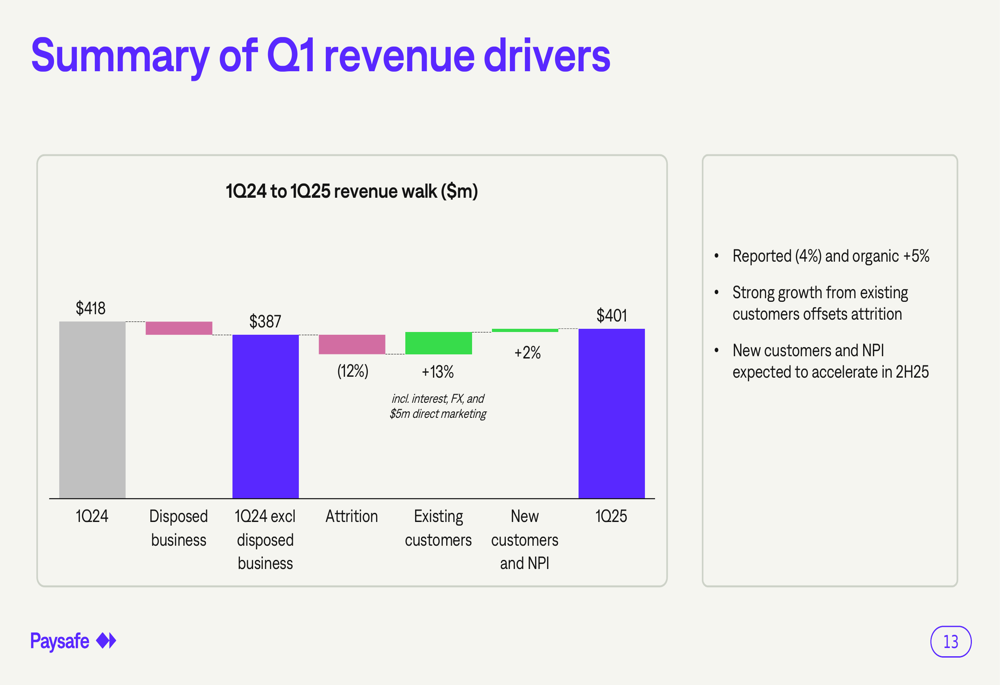

The company’s revenue decline can be attributed primarily to business disposals, as illustrated in the following waterfall chart showing the key drivers of revenue change from Q1 2024 to Q1 2025:

While attrition reduced revenue by 12%, this was offset by 13% growth from existing customers (including interest, FX, and $5 million in direct marketing) and 2% growth from new customers and new product initiatives. The company noted that new customer acquisition and product initiatives are expected to accelerate in the second half of 2025.

Segment Performance Analysis

Paysafe’s business is divided into two main segments: Merchant Solutions and Digital Wallets, which showed divergent performance in the quarter.

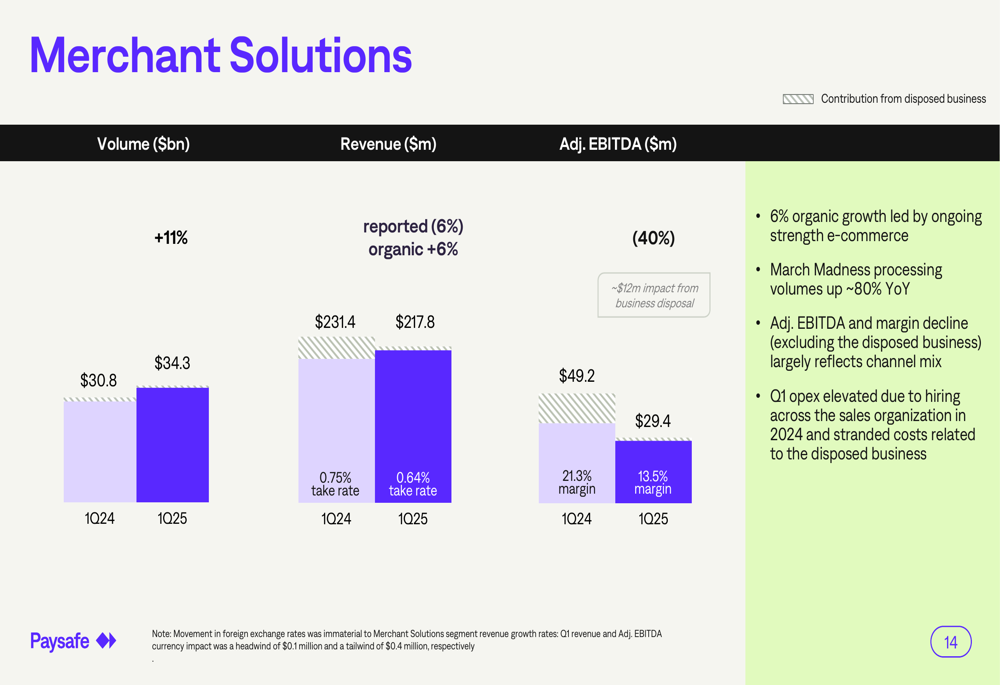

The Merchant Solutions segment, which processed $34.3 billion in volume (+11%), generated revenue of $217.8 million (+6% organic) but saw a significant decline in adjusted EBITDA to $29.4 million (-40%). The company attributed this profitability decline to channel mix and elevated operating expenses due to sales organization hiring in 2024 and stranded costs related to disposed business.

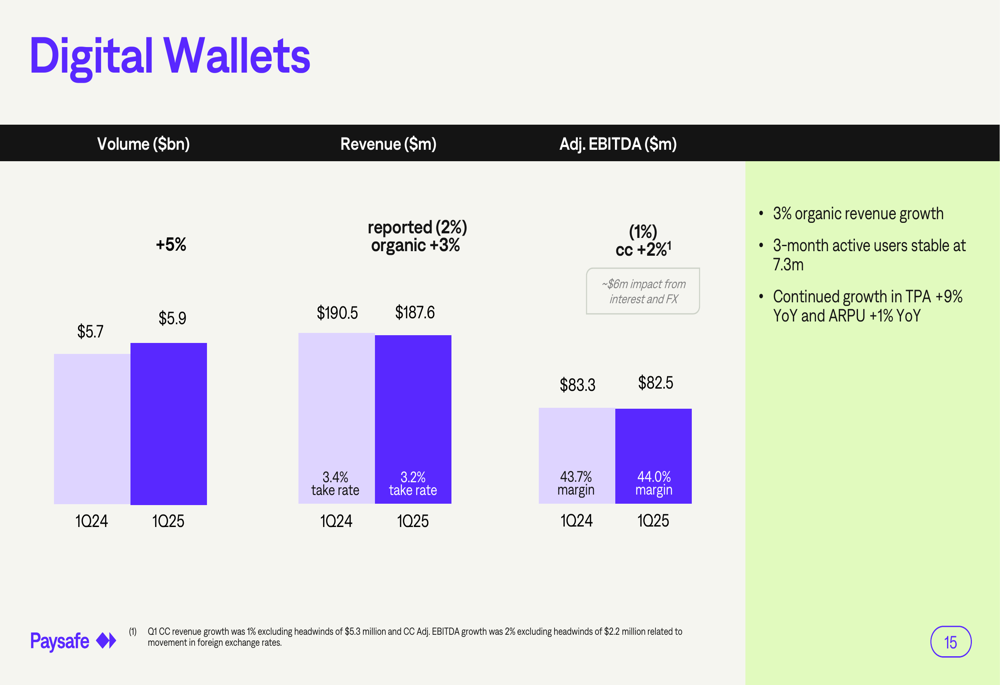

Meanwhile, the Digital Wallets segment demonstrated more stable performance with volume of $5.9 billion (+5%), revenue of $187.6 million (+3% organic), and adjusted EBITDA of $82.5 million (-1%). This segment maintained a significantly higher take rate of 3.2% compared to Merchant Solutions’ 0.64%, as well as a much stronger adjusted EBITDA margin of 44.0% versus 13.5% for Merchant Solutions.

The Digital Wallets segment maintained stable 3-month active users at 7.3 million, with continued growth in transactions per active user (+9% YoY) and average revenue per user (+1% YoY).

Strategic Initiatives and Partnerships

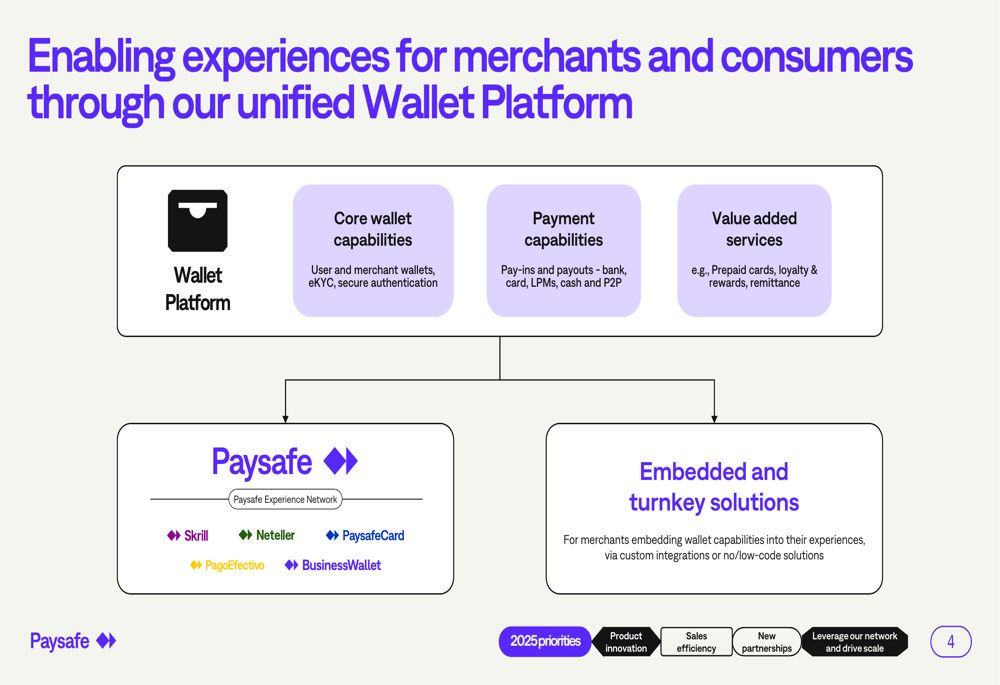

Paysafe’s strategic focus centers on its unified wallet platform, which integrates core wallet capabilities, payment capabilities, and value-added services across multiple brands including Skrill, Neteller, PaysafeCard, PagoEfectivo, and BusinessWallet.

The following diagram illustrates the company’s unified wallet platform strategy:

During the quarter, Paysafe announced several new partnerships to bolster sales and product distribution across different segments:

1. For SMB customers, the company launched integration with Clover Capital to provide improved access to capital

2. For Enterprise and e-commerce, Paysafe enhanced its ISV offering with PayFac-as-a-Service solutions through Tilled

3. For Consumer services, the company strengthened the PaysafeCard network in Ireland through S SELFPAY

The company also reported strong enterprise sales performance, with 31% revenue growth in e-commerce and 102 enterprise wins secured during the quarter. Enterprise productivity improved with over 20% increase in annual contract value per active representative.

Forward Outlook

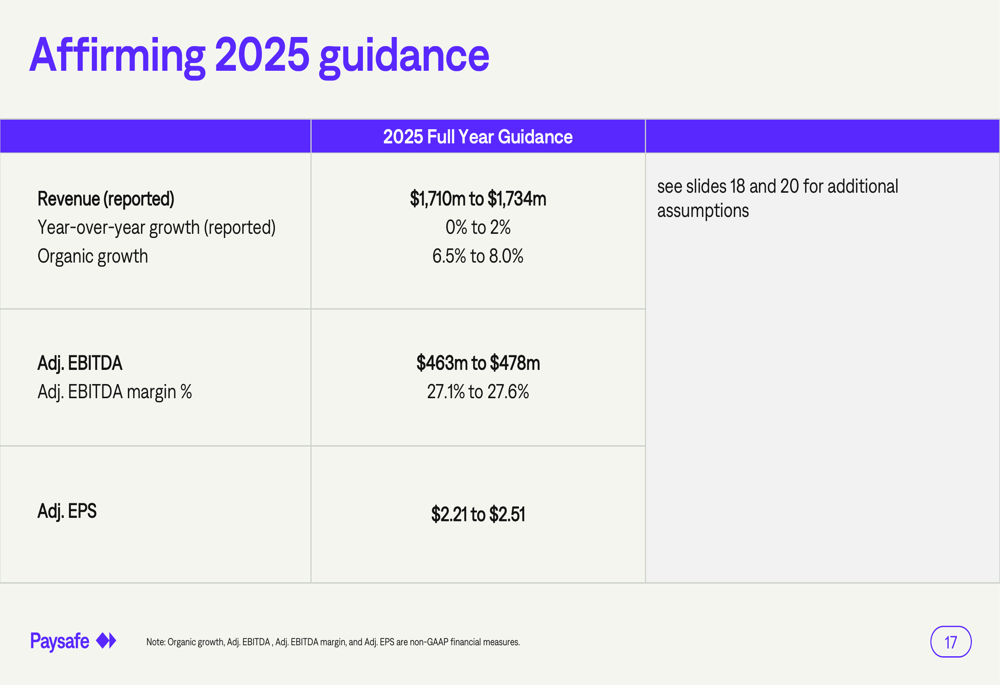

Paysafe affirmed its full-year 2025 guidance, projecting revenue of $1.710-1.734 billion (0-2% year-over-year growth, 6.5-8.0% organic growth), adjusted EBITDA of $463-478 million (27.1-27.6% margin), and adjusted EPS of $2.21-2.51.

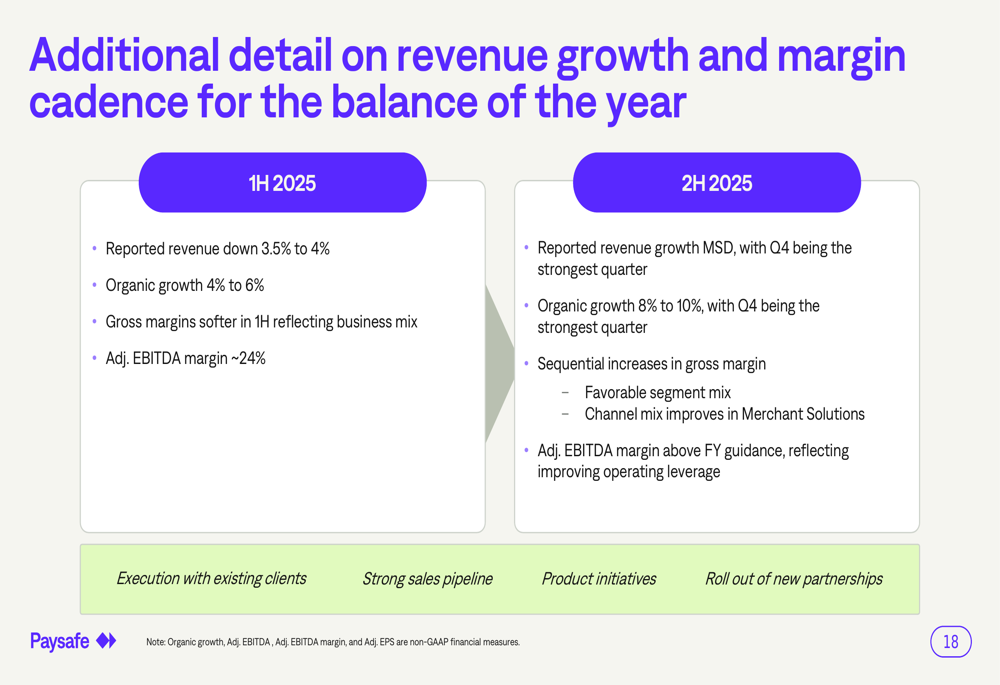

The company expects performance to strengthen in the second half of 2025, with the fourth quarter projected to be the strongest. For the first half of 2025, reported revenue is expected to decline 3.5-4%, with organic growth of 4-6% and adjusted EBITDA margin of approximately 24%. In contrast, the second half is anticipated to show mid-single-digit reported revenue growth with organic growth of 8-10%, along with sequential increases in gross margin and adjusted EBITDA margin above the full-year guidance.

Management identified several drivers to achieve this projected acceleration, including execution with existing clients, a strong sales pipeline, product initiatives, and the roll-out of new partnerships. The company’s focus on reducing leverage remains a priority, with the current net leverage ratio at 4.9x compared to a year-end 2024 level of 4.7x.

Despite the current challenges in reported financial metrics, Paysafe’s management remains confident in the company’s strategic direction and ability to deliver improved performance in the latter part of 2025, driven by its unified wallet platform strategy and expanding partnerships across key verticals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.