Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Paysafe (NYSE:PSFE) presented its second quarter 2025 earnings results on August 12, 2025, revealing a mixed financial performance characterized by organic growth amid overall revenue decline. The payment solutions provider reported 5% organic revenue growth despite a 3% decrease in total revenue, primarily due to business disposals. The company maintained its full-year guidance while highlighting strategic initiatives in product innovation and partnerships.

Quarterly Performance Highlights

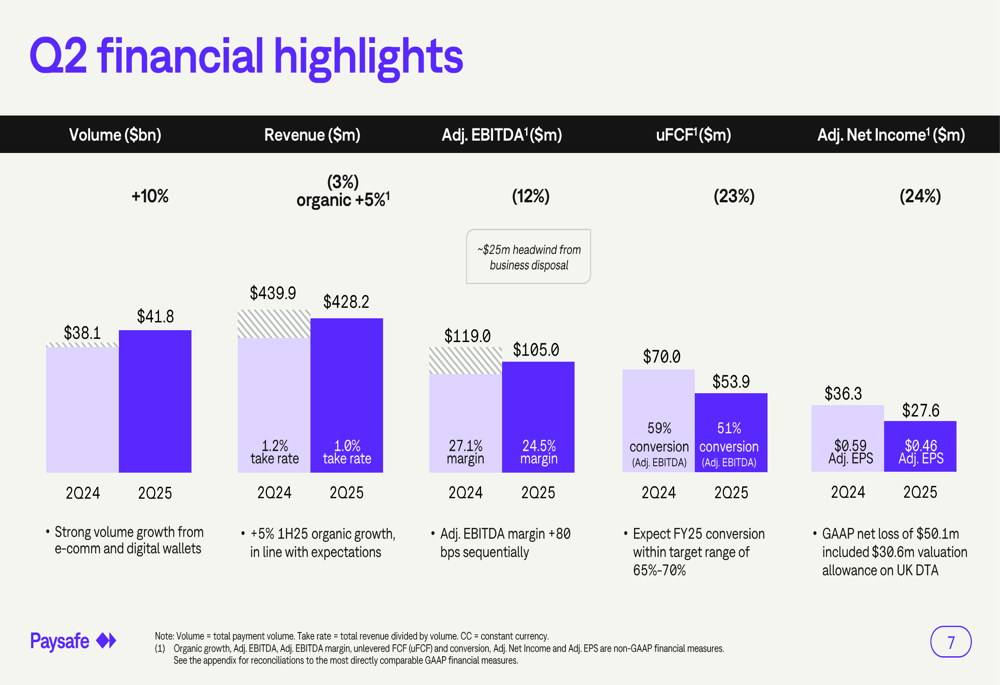

Paysafe reported Q2 2025 revenue of $428.2 million, representing a 3% year-over-year decrease from $439.9 million in Q2 2024. However, when excluding disposed business units, the company achieved 5% organic growth. Transaction (JO:NTUJ) volume increased by 10%, demonstrating continued momentum in payment processing activity.

As shown in the following comprehensive financial summary:

Adjusted EBITDA declined 12% to $105.0 million, with margins contracting from 27.1% to 24.5%. The company attributed this decline partially to a $25 million headwind from business disposal. Adjusted net income fell 24% to $27.6 million, with adjusted EPS decreasing from $0.59 to $0.46. Unlevered free cash flow decreased 23% to $53.9 million, with conversion rates dropping from 59% to 51%.

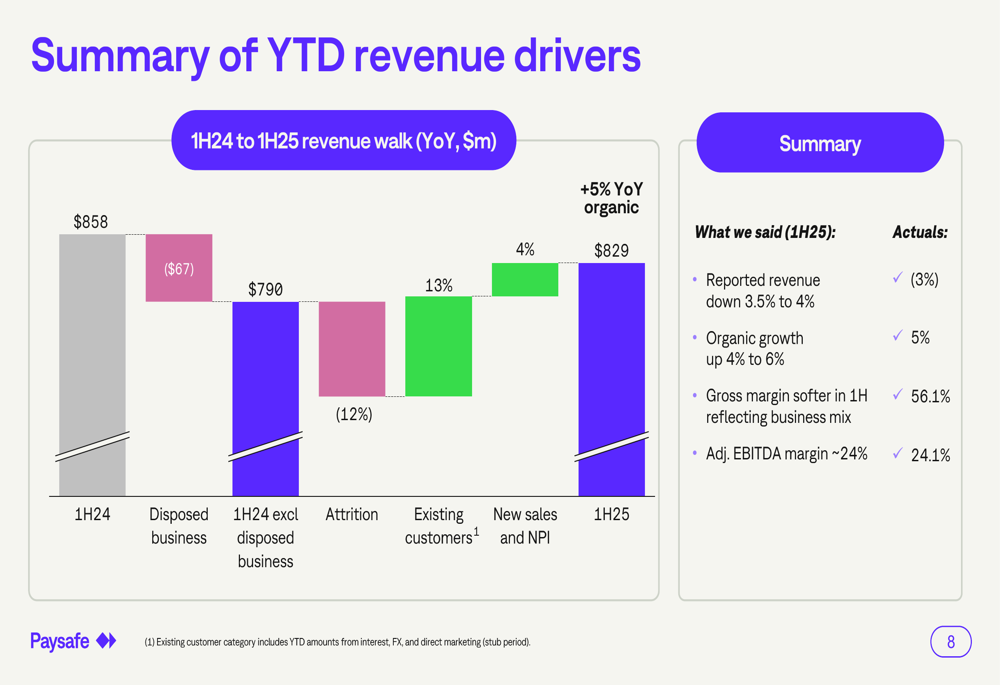

The company’s revenue trajectory for the first half of 2025 is illustrated in this waterfall chart:

This visualization demonstrates how Paysafe’s disposed business created a $67 million revenue headwind, while organic growth from existing customers (+13%) and new sales and product initiatives (+4%) helped offset attrition (-12%), resulting in 5% year-over-year organic growth for the first half of 2025.

Segment Performance Analysis

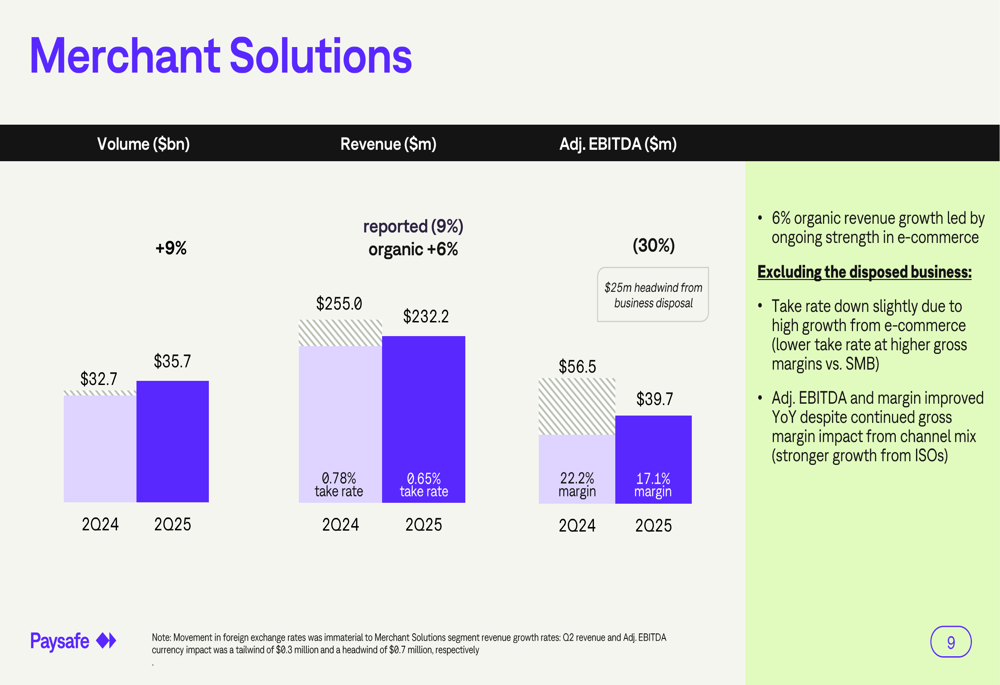

Paysafe’s two main business segments showed divergent performance. The Merchant Solutions segment experienced a 9% reported revenue decline to $232.2 million, though organic growth reached 6% when excluding disposed businesses:

The segment’s adjusted EBITDA decreased to $39.7 million, with margin compression from 22.2% to 17.1%. Management noted that e-commerce strength continued, with revenue increasing 32% year-over-year to $51.5 million. The company also reported that North America iGaming is on track to surpass $100 million in revenue for 2025, with enterprise deals up 19% year-over-year.

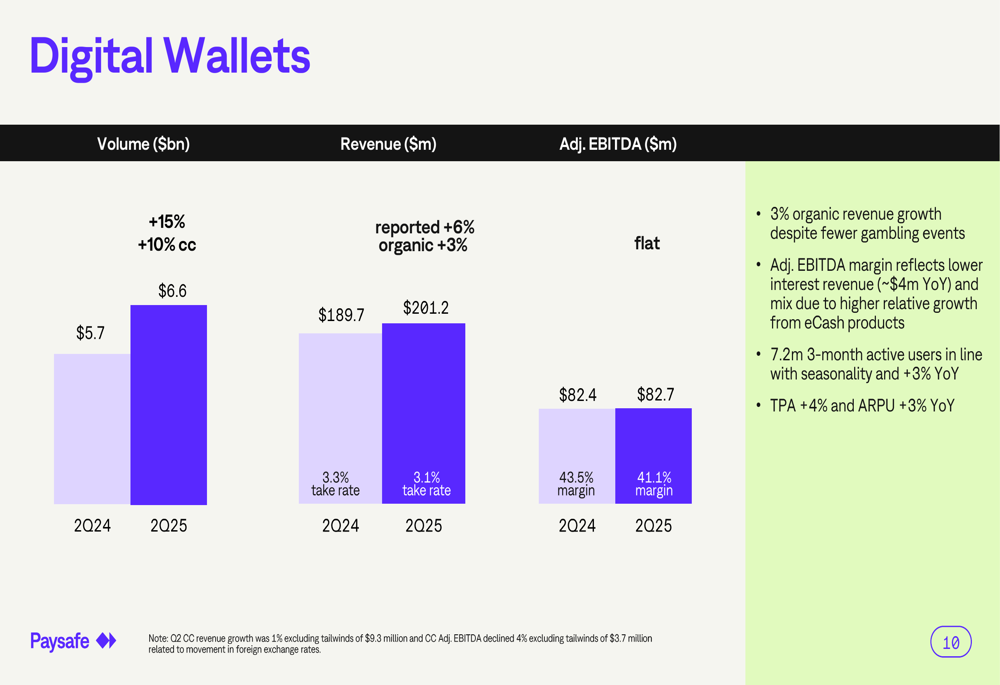

In contrast, the Digital Wallets segment demonstrated stronger performance with 6% reported revenue growth to $201.2 million (3% organic growth):

Digital Wallets maintained stable adjusted EBITDA at $82.7 million, though margins contracted slightly from 43.5% to 41.1%. The segment reported 7.2 million three-month active users, representing 3% year-over-year growth, with transactions per active user increasing 4% and average revenue per user growing 3%.

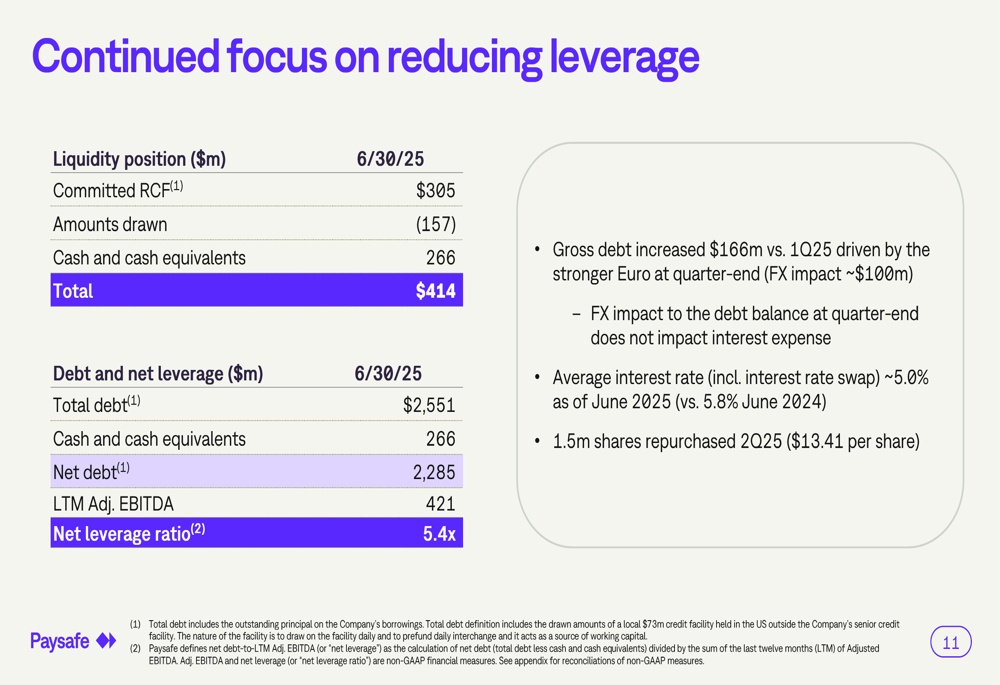

Balance Sheet and Leverage

Despite stating a continued focus on reducing leverage, Paysafe’s net leverage ratio increased to 5.4x from 4.9x in March 2025. The company attributed this partly to foreign exchange impacts, as shown in the following debt summary:

Total (EPA:TTEF) debt stood at $2.55 billion, with cash and cash equivalents of $266 million resulting in net debt of $2.29 billion. The company noted that gross debt increased $166 million versus Q1 2025, driven primarily by a stronger Euro at quarter-end (approximately $100 million FX impact). Paysafe maintained liquidity of $414 million and reported an average interest rate of approximately 5.0%, down from 5.8% in June 2024. During the quarter, the company repurchased 1.5 million shares at an average price of $13.41 per share.

Strategic Initiatives

Paysafe highlighted several strategic priorities for 2025, including product innovation, sales efficiency, new partnerships, and network leverage. The company is expanding its geographic footprint with local wallet use cases in Peru and enhancing user engagement through features like "Sports Corner" with live odds.

The company’s eCash business showed strong momentum with 37% revenue growth year-to-date from the online store. Paysafe also announced new partnerships with mobile and retail banks including BBVA (BME:BBVA), Revolut, and Deutsche Bank (ETR:DBKGn) to broaden its reach.

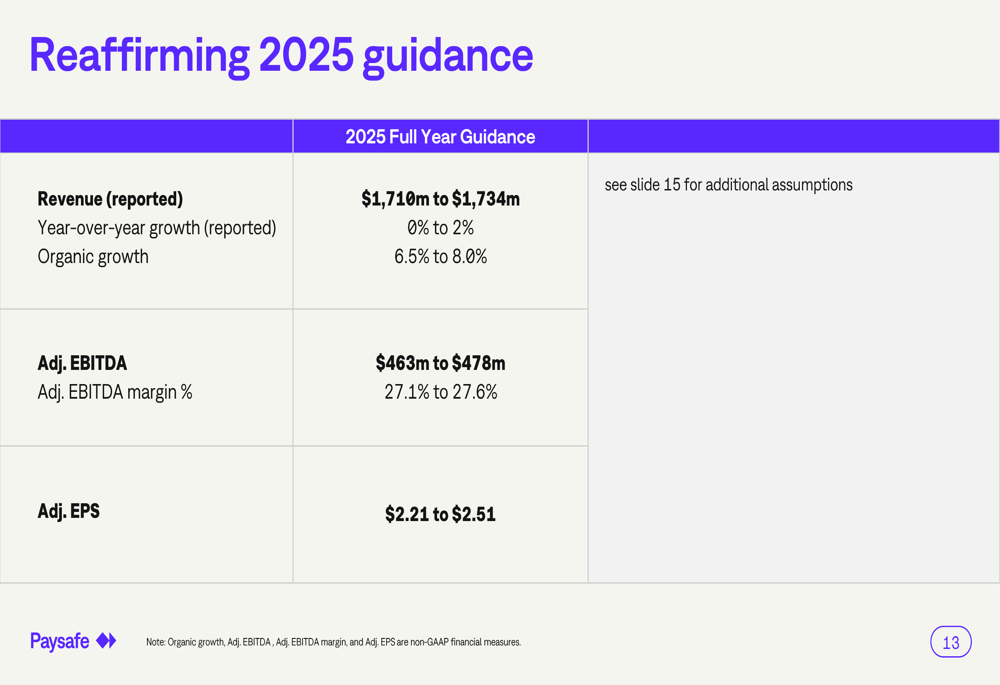

Forward-Looking Statements

Paysafe reaffirmed its full-year 2025 guidance as illustrated in the following slide:

The company expects revenue between $1,710 million and $1,734 million, representing 0% to 2% reported growth and 6.5% to 8.0% organic growth. Adjusted EBITDA is projected between $463 million and $478 million, with margins of 27.1% to 27.6%. Adjusted EPS guidance remains at $2.21 to $2.51.

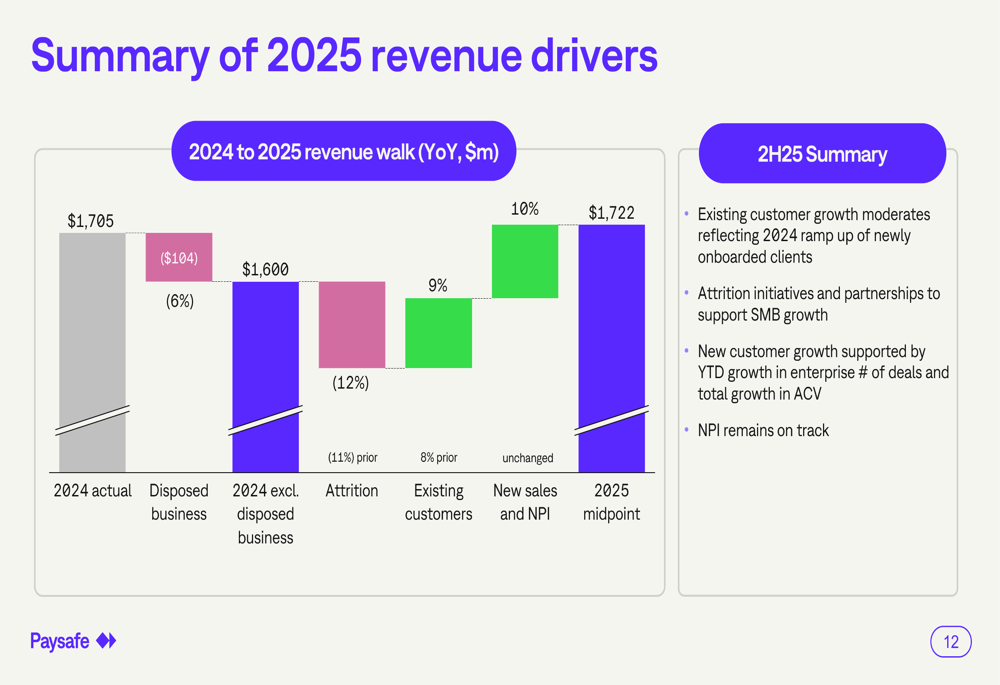

Management provided additional insight into revenue drivers for the full year 2025:

This projection shows how Paysafe expects to grow from $1,705 million in 2024 to $1,722 million in 2025 (midpoint), with disposed business creating a $104 million headwind offset by growth from existing customers (9%) and new sales and product initiatives (10%), while managing attrition (-12%).

Conclusion

Paysafe’s Q2 2025 results present a mixed picture of organic growth amid overall revenue decline and profitability challenges. While the company demonstrated strength in digital wallets and e-commerce, it faces headwinds from business disposals and segment margin compression. The increase in net leverage ratio contradicts the stated focus on debt reduction, though some of this was attributed to currency fluctuations.

As Paysafe maintains its full-year guidance and continues to invest in strategic initiatives, investors will likely monitor whether the company can accelerate organic growth while improving profitability and making meaningful progress on leverage reduction in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.