Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

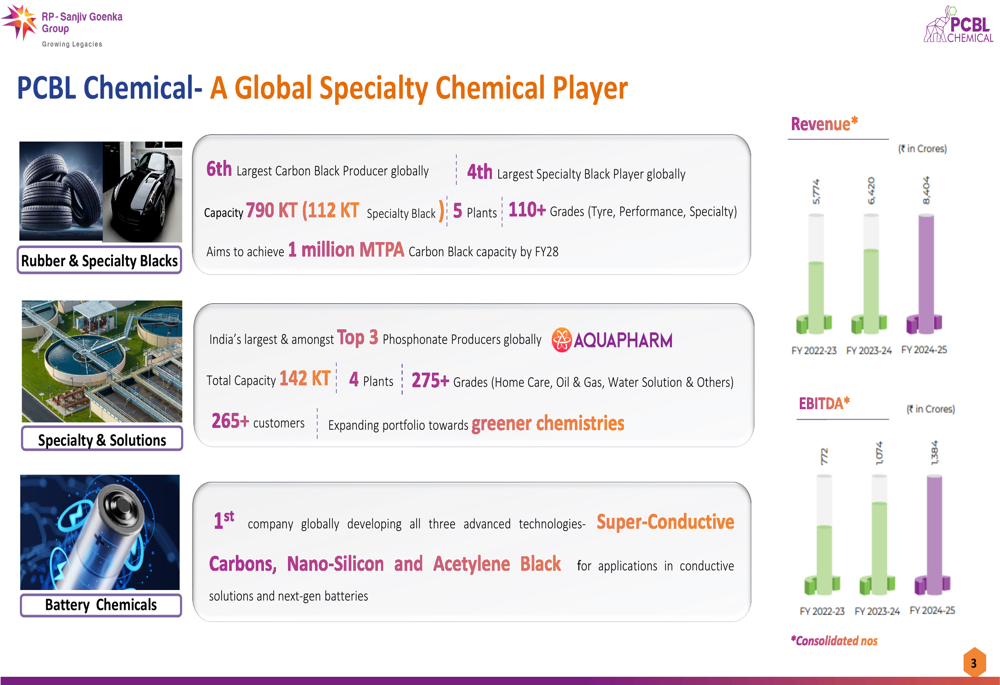

PCBL Chemical Ltd, the 6th largest carbon black producer globally, reported its Q2 FY26 results on October 17, 2025, showing improved operational metrics but facing significant margin pressure. The company’s stock fell 4.45% to 378.85 INR following the announcement, reflecting investor concerns over profitability despite volume growth. As part of the RP-Sanjiv Goenka Group with operations across 60+ countries, PCBL Chemical continues to navigate challenging market conditions while pursuing strategic expansion in specialty chemicals.

Quarterly Performance Highlights

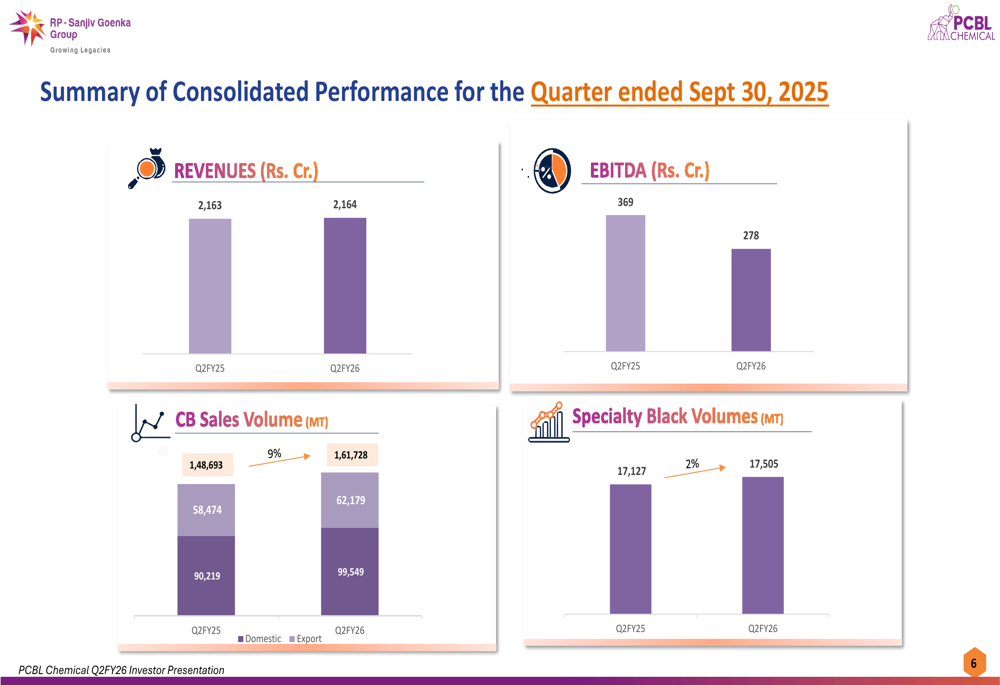

PCBL Chemical reported consolidated revenue of Rs. 2,164 crore for Q2 FY26, essentially flat compared to Rs. 2,163 crore in the same quarter last year. However, EBITDA declined significantly to Rs. 278 crore from Rs. 369 crore in Q2 FY25, indicating substantial margin compression. Profit before tax fell to Rs. 78 crore from Rs. 164 crore year-over-year, while profit after tax dropped to Rs. 62 crore from Rs. 123 crore in Q2 FY25.

As shown in the following chart comparing quarterly performance metrics:

The company achieved notable operational improvements, with carbon black sales volume increasing by 9% year-over-year to 161,728 MT and specialty black volume growing by 2% to 17,505 MT. This volume growth, however, failed to translate into improved financial performance due to external market pressures.

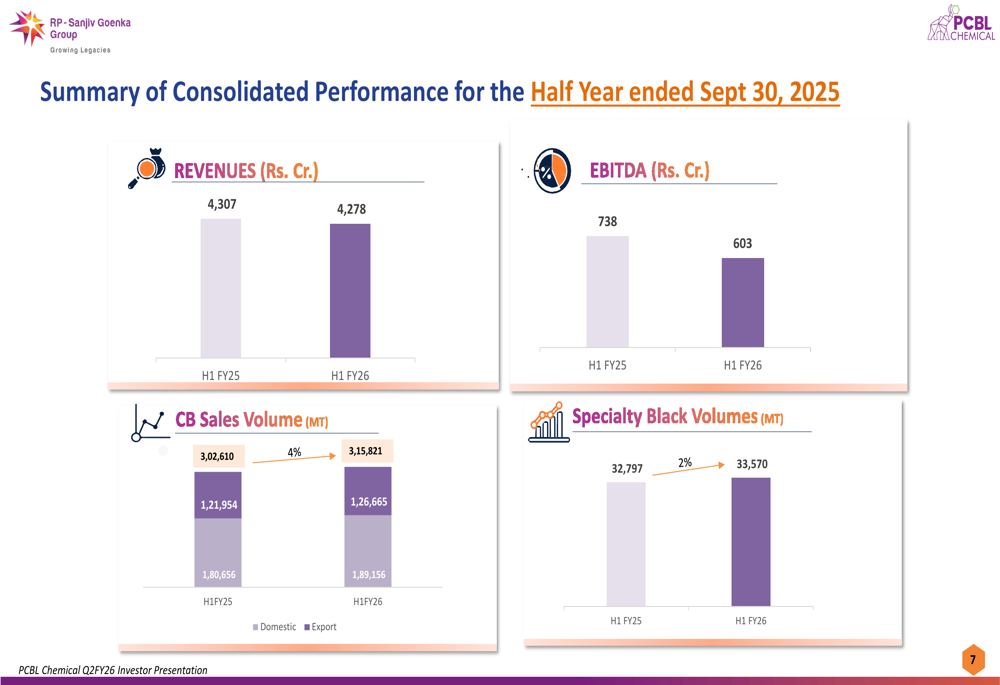

For the half-year period ended September 30, 2025, the company reported marginally lower revenue of Rs. 4,278 crore compared to Rs. 4,307 crore in H1 FY25, while EBITDA declined more significantly to Rs. 603 crore from Rs. 738 crore in the previous year.

The following chart illustrates the half-year performance comparison:

Segment Performance

Carbon Black Operations

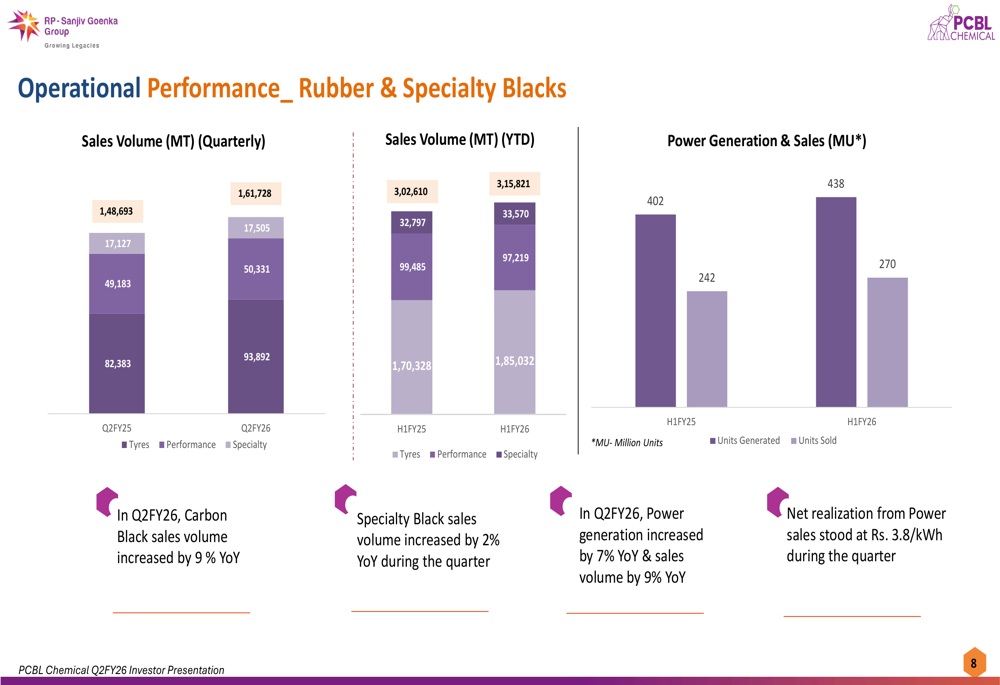

PCBL Chemical maintained strong operational performance in its core carbon black business despite market challenges. The company achieved 99% capacity utilization across its facilities, with power generation increasing by 7% year-over-year. The working capital cycle improved by 12 days, releasing approximately Rs. 240 crore of cash, demonstrating effective financial management amid challenging conditions.

The operational metrics for rubber and specialty blacks show consistent growth in volumes:

According to the earnings call, US tariffs have affected approximately 2,000 tonnes of carbon black exports, while fluctuating crude oil prices have impacted profit margins. Management expressed confidence that "this phase has largely bottomed out," with expectations for "steady recovery in profitability in coming quarters."

Aquapharm Chemical

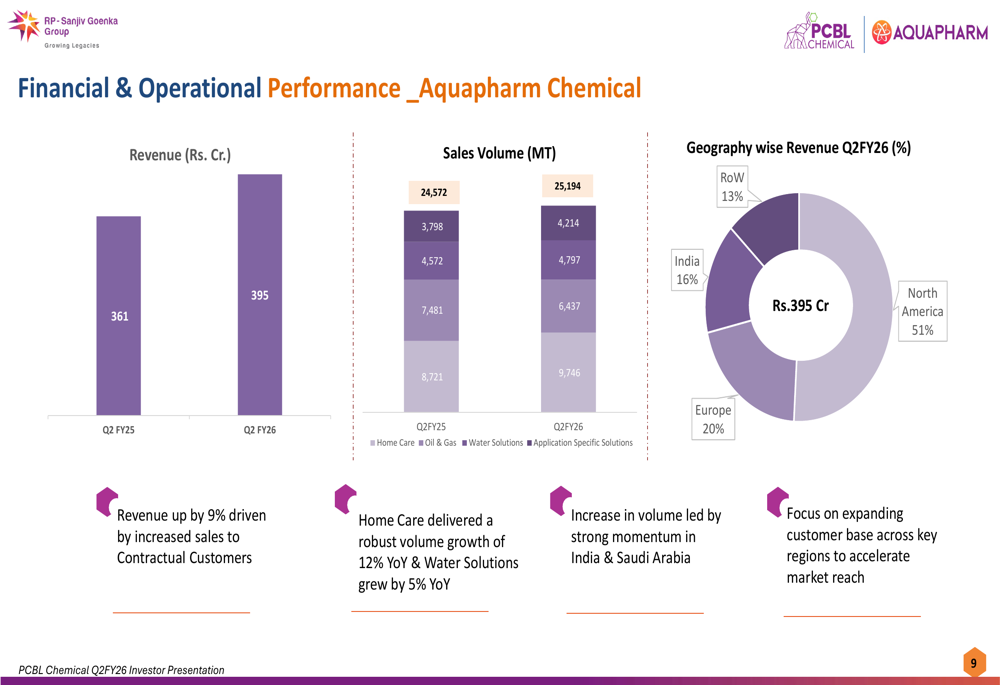

The Aquapharm Chemical segment showed stronger performance, with revenue increasing 9% year-over-year to Rs. 395 crore in Q2 FY26, driven by higher sales to contractual customers. Sales volume grew to 25,194 MT from 24,572 MT in Q2 FY25, with particularly strong performance in home care products (12% YoY growth) and water solutions (5% YoY growth).

The geographic revenue breakdown for Aquapharm Chemical demonstrates the segment’s global reach:

North America remains the largest market at 51% of segment revenue, followed by Europe (20%), India (16%), and rest of world (13%). Management highlighted increased volume in India and Saudi Arabia as key growth drivers, with plans to further expand the customer base across key regions.

Strategic Initiatives

PCBL Chemical continues to position itself as a multi-chemistry specialty chemical player with diversified offerings across various sectors. The company’s revenue is derived from tyre and tyre specialty (48%), performance products (24%), specialty black (11%), and oil and gas applications (17%).

The company’s strategic positioning and diversified product portfolio are illustrated here:

Looking ahead, PCBL Chemical is targeting a 50% capacity addition over the next five years across all product segments. The company is also expanding its specialty chemical portfolio toward higher-margin products while focusing on operational efficiencies and R&D innovation.

The future outlook strategy is outlined in this visualization:

A significant focus area is the company’s Nanovace subsidiary, which is making strides in battery materials and energy storage solutions. Nanovace has secured a US patent for nanomaterial processes to enhance energy storage and established a pilot plant in Palej, Gujarat. The specialty black line dedicated for super-conductive grades is expected to start commercial production in November 2025.

Forward-Looking Statements

Management expects improved EBITDA per ton in upcoming quarters as market conditions stabilize. For the Aquapharm segment, the company anticipates reaching an EBITDA exit rate of Rs. 75 crore by the end of the financial year.

The company’s long-term strategy focuses on capacity expansion, portfolio diversification toward high-margin products, and R&D innovation in rubber, specialty blacks, green chelates, polymers, and battery materials. PCBL Chemical also expects to benefit from recent GST rate cuts in India, which should support growth in the auto sector.

Despite current challenges, management remains optimistic about the company’s ability to navigate market headwinds and return to a growth trajectory in the coming quarters. However, investors appear cautious, as reflected in the stock’s current price of 378.85 INR, well below its 52-week high of 498.4 INR, suggesting that the market will be looking for concrete evidence of the anticipated profitability recovery in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.