Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

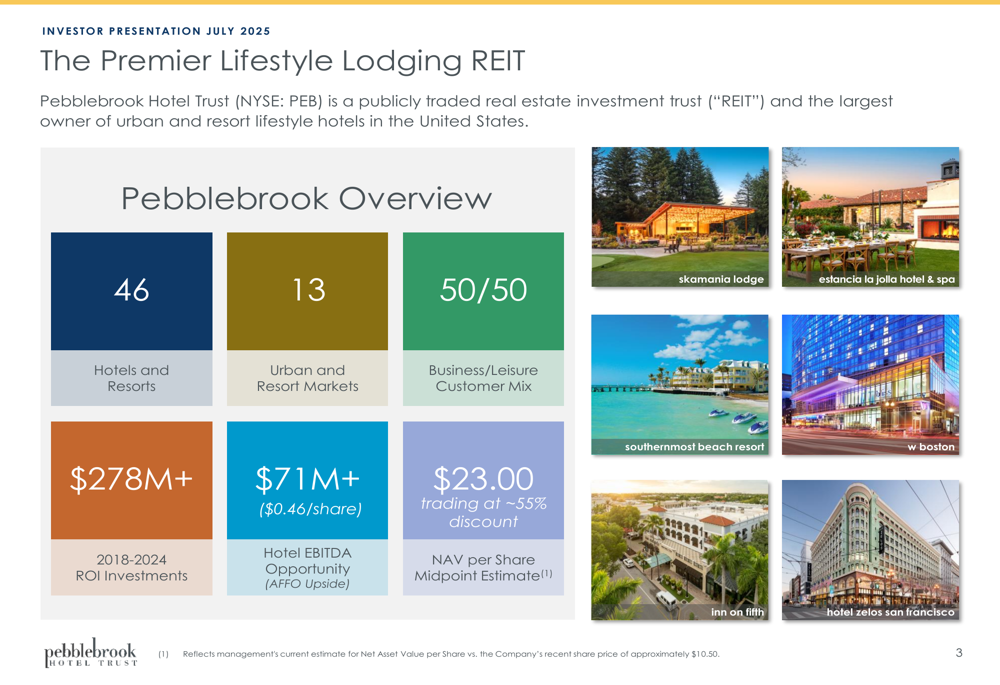

Pebblebrook Hotel Trust (NYSE:PEB) unveiled its July 2025 investor presentation highlighting the company’s strategic portfolio transformation and growth opportunities. The presentation comes after PEB reported strong Q1 2025 results that exceeded analyst expectations, with the company posting an EPS of -$0.37 versus the forecasted -$0.39 and revenue of $320.27 million against an expected $312.38 million.

Trading at approximately $10.64 in the aftermarket session, Pebblebrook shares remain significantly undervalued according to management’s estimates, creating what the company describes as an exceptional investment opportunity for value-oriented investors.

As shown in the following overview of Pebblebrook’s key statistics and market positioning:

Strategic Portfolio Transformation

Pebblebrook has undertaken a significant strategic repositioning of its portfolio, reducing exposure to urban and corporate transient markets while increasing its presence in leisure-oriented destinations. Since 2019, the company has acquired five upper upscale and luxury resorts for $802 million and divested 15 lower-quality urban properties for $1.2 billion.

This transformation has dramatically shifted the company’s EBITDA composition, with resort properties now contributing 45% of EBITDA (up from 17% pre-transformation) and urban properties decreasing to 55% (down from 83%). Geographically, East Coast properties now generate 54% of EBITDA (up from 38%), while West Coast contributions have declined to 43% (from 56%).

The company has also successfully reduced its exposure to the challenging San Francisco market, which saw a 19% decrease in EBITDA contribution. Meanwhile, San Diego (25%), Boston (22%), and Naples (12%) have emerged as the company’s top-performing markets.

Investment Thesis and Growth Opportunities

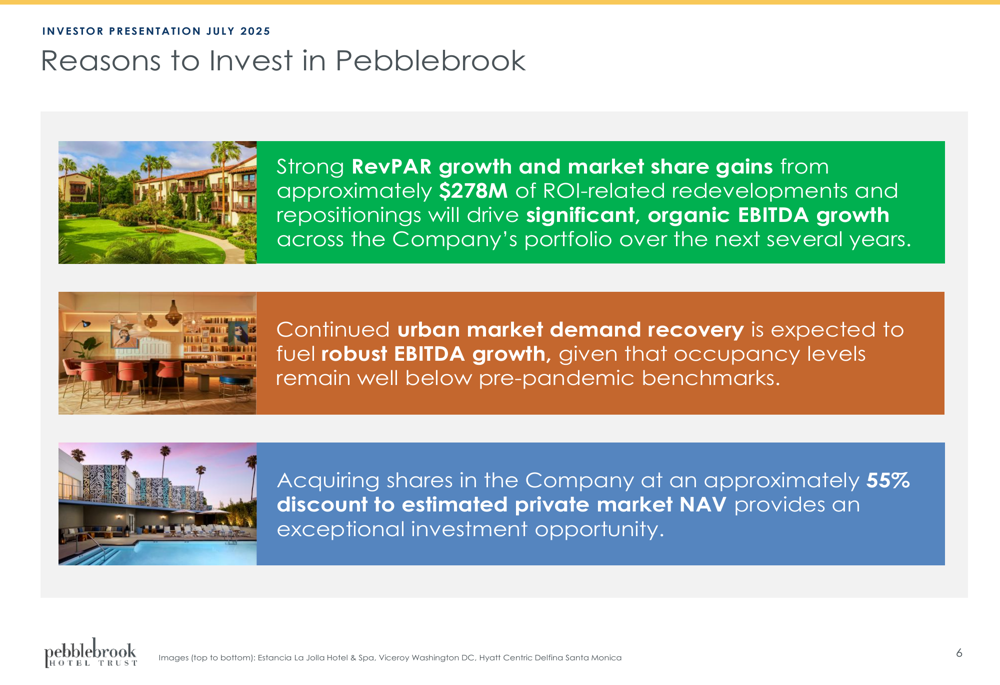

Pebblebrook’s investor presentation outlines three key reasons to invest in the company, emphasizing strong RevPAR growth potential, urban market recovery, and the significant discount to NAV at which shares currently trade.

The following slide clearly articulates the company’s investment thesis:

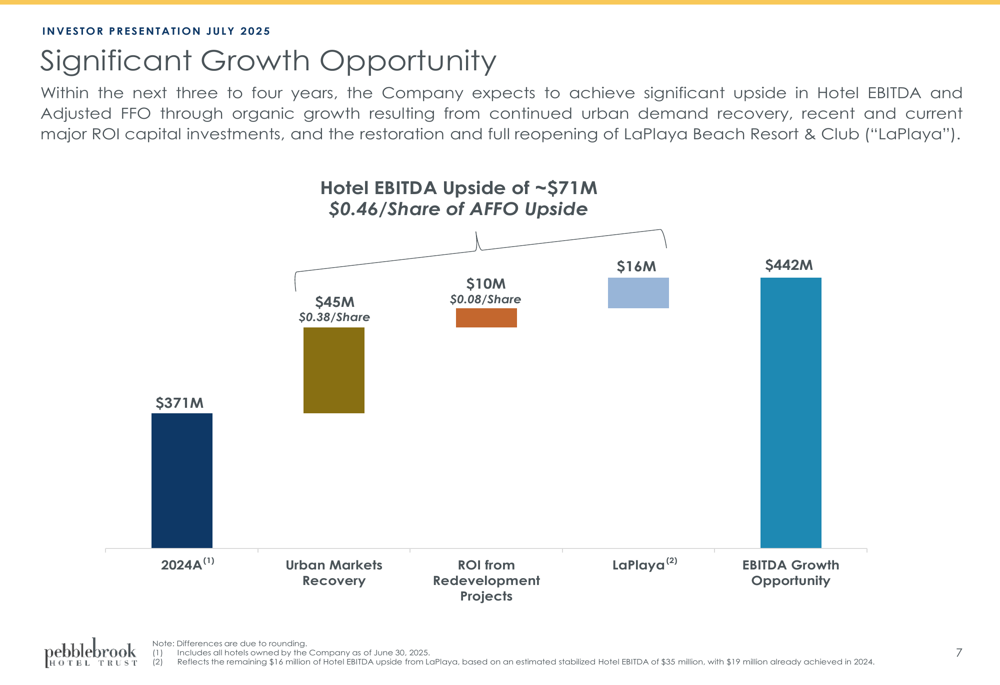

A central component of Pebblebrook’s growth strategy is the anticipated $71 million in Hotel EBITDA upside, equivalent to $0.46 per share in AFFO upside. This growth is expected to come from three main sources: continued urban markets recovery ($45 million), ROI from redevelopment projects ($10 million), and the full restoration of LaPlaya Beach Resort & Club ($16 million).

The following chart illustrates this potential EBITDA growth opportunity:

This growth projection aligns with the company’s Q1 2025 performance, which saw same-property hotel EBITDA of $62.3 million, exceeding the midpoint of guidance by $4.3 million. However, it’s worth noting that during the Q1 earnings call, CEO John Bortz expressed caution about potential economic slowdowns in the latter half of 2025, slightly reducing the company’s full-year outlook.

Urban Market Recovery Potential

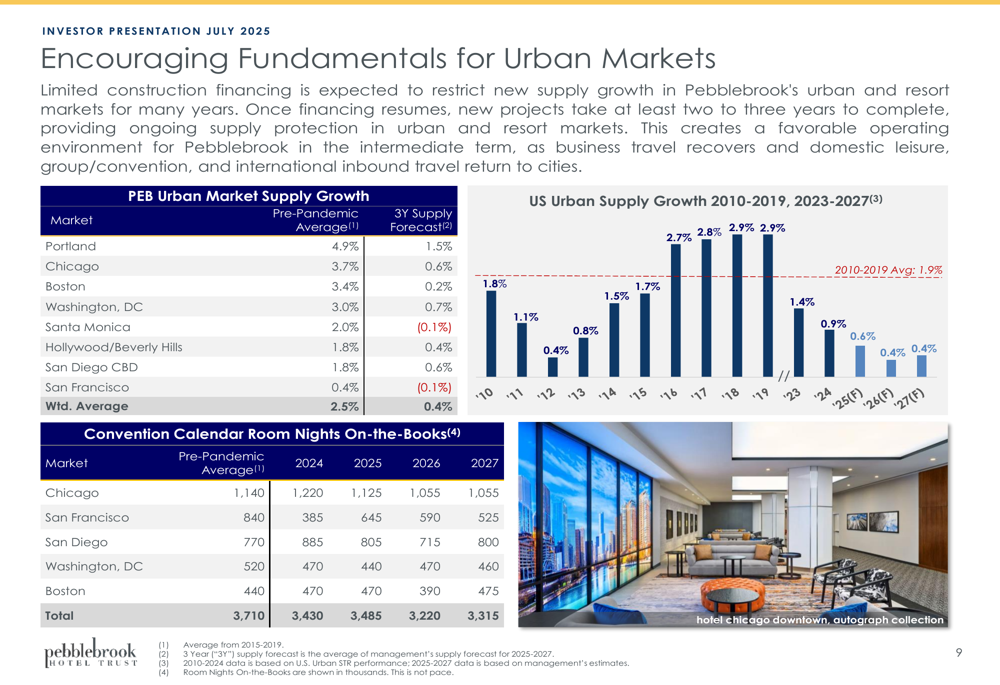

Despite the strategic shift toward resort properties, urban hotels still represent a significant portion of Pebblebrook’s portfolio and offer substantial recovery potential. The company points to encouraging fundamentals in urban markets, including limited new supply growth due to restricted construction financing and increasing convention calendar bookings.

The following table compares pre-pandemic supply growth with current forecasts, showing a dramatic reduction in new hotel development across Pebblebrook’s urban markets:

The company projects that urban hotel EBITDA could increase by more than $45 million as occupancy recovers from the current 71% to a projected 80%, with ADR rising from $280 to $287. This would drive RevPAR from $200 to $230 and boost urban hotel EBITDA from $213 million to $257 million.

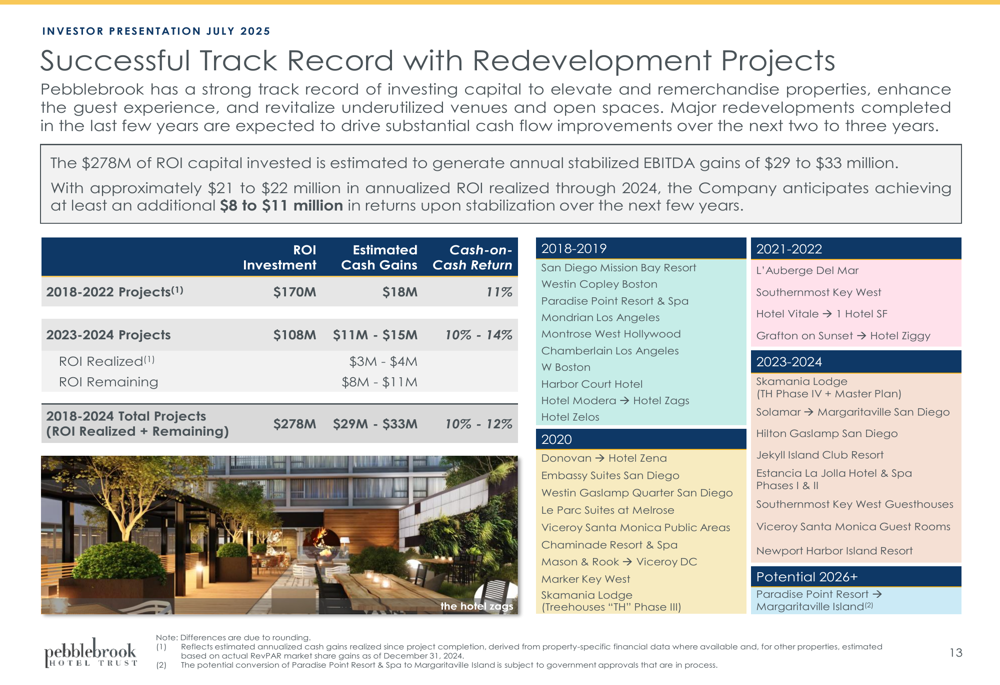

ROI Investments and Redevelopment Projects

Pebblebrook has invested approximately $278 million in ROI-related redevelopments and repositionings, which are expected to generate annual stabilized EBITDA gains of $29 to $33 million. With approximately $21 to $22 million in annualized ROI realized through 2024, the company anticipates achieving at least an additional $8 to $11 million in returns upon stabilization over the next few years.

The company’s track record with redevelopment projects demonstrates strong returns, with 2018-2022 projects generating an 11% cash return on a $170 million investment, and 2023-2024 projects expected to yield 10-14% returns on a $108 million investment.

The following slide details the company’s redevelopment track record:

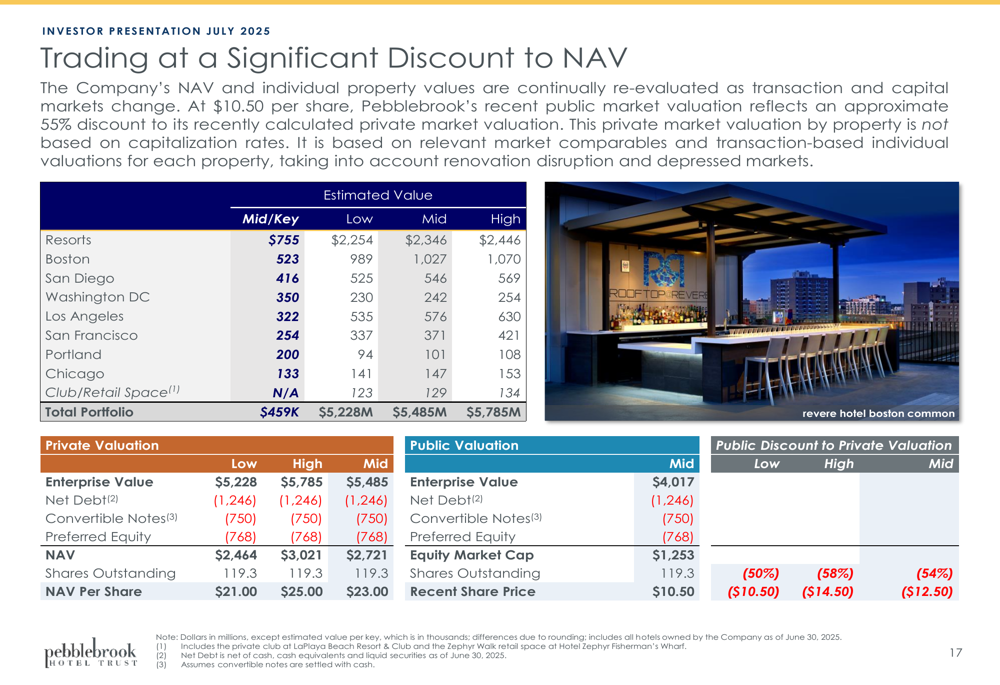

Valuation and Financial Position

Perhaps the most compelling aspect of Pebblebrook’s investment case is the significant discount at which its shares trade relative to estimated NAV. According to management’s calculations, at a recent share price of approximately $10.50, Pebblebrook trades at a 55% discount to its estimated private market value of $23.00 per share (midpoint).

The following detailed valuation analysis breaks down the company’s estimated property values by market:

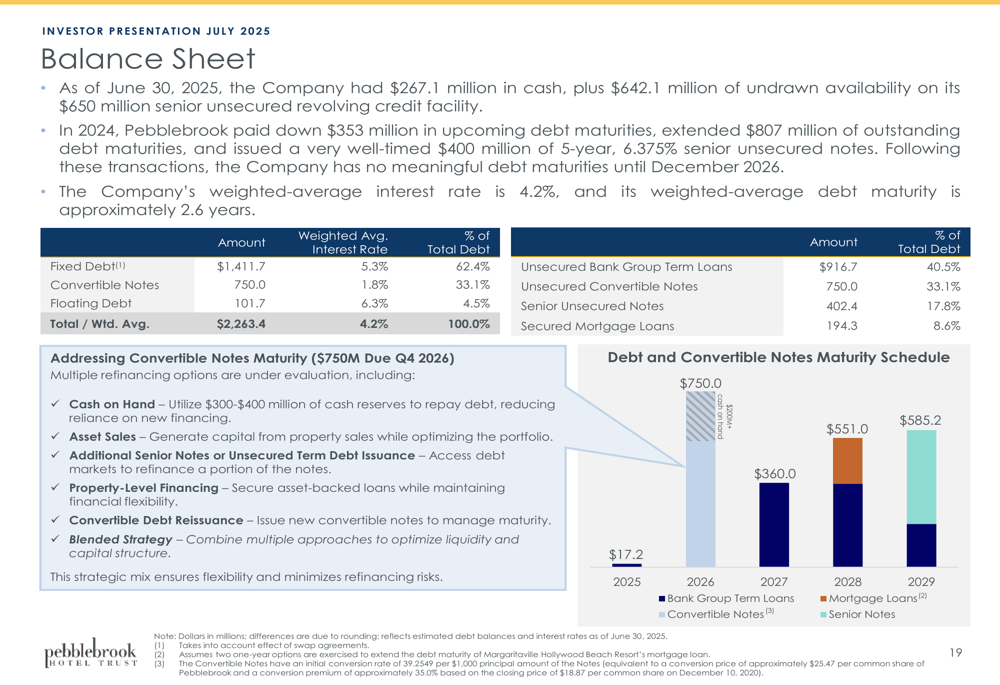

Pebblebrook maintains a solid balance sheet with $267.1 million in cash as of June 30, 2025, plus $642.1 million of undrawn availability on its $650 million senior unsecured revolving credit facility. The company’s weighted-average interest rate is 4.2%, and its weighted-average debt maturity is approximately 2.6 years.

The following slide details the company’s debt maturity schedule and key financial metrics:

This strong financial position provides Pebblebrook with flexibility to navigate potential economic headwinds, as highlighted by CEO John Bortz during the Q1 earnings call: "We’re generating substantial free cash flow. And if conditions should deteriorate further, we certainly have the flexibility, the liquidity, and the experience to adapt quickly."

Outlook and Challenges

While Pebblebrook’s presentation paints an optimistic picture of growth opportunities, management has expressed caution about potential economic slowdowns in the latter half of 2025. During the Q1 earnings call, the company slightly reduced its full-year outlook, citing uncertainty around major economic policies that could lead to "a pause or a reduction in spending and investment, including for travel."

Key challenges identified include economic uncertainty, weakness in government-related travel, potential decline in international inbound travel, continued softness in urban RevPAR, and rising expenses necessitating efficient cost management strategies.

Conclusion

Pebblebrook Hotel Trust’s July 2025 investor presentation highlights the company’s successful strategic transformation toward resort properties and away from challenged urban markets. With $71 million in potential EBITDA upside, strong Q1 2025 performance, and shares trading at a significant discount to NAV, management makes a compelling case for investment despite near-term economic uncertainties.

The company’s solid balance sheet and flexible capital strategy position it to weather potential economic headwinds while continuing to execute on its redevelopment initiatives and capitalize on the ongoing recovery in urban markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.