Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Pegasystems Inc. (NASDAQ:PEGA) released its Q2 2025 investor presentation on July 23, highlighting strong growth in its subscription business and significant improvements in cash flow generation. The enterprise software company, which specializes in AI decisioning and workflow automation, has been executing a multi-year transition from perpetual licenses to a subscription-based model.

The presentation comes as PEGA shares have shown strong momentum, with a 59% price return over the past six months according to available market data. The stock closed at $54.86 on October 14, 2025, representing a 1.2% increase for the day and sitting well above its 52-week low of $29.84.

Quarterly Performance Highlights

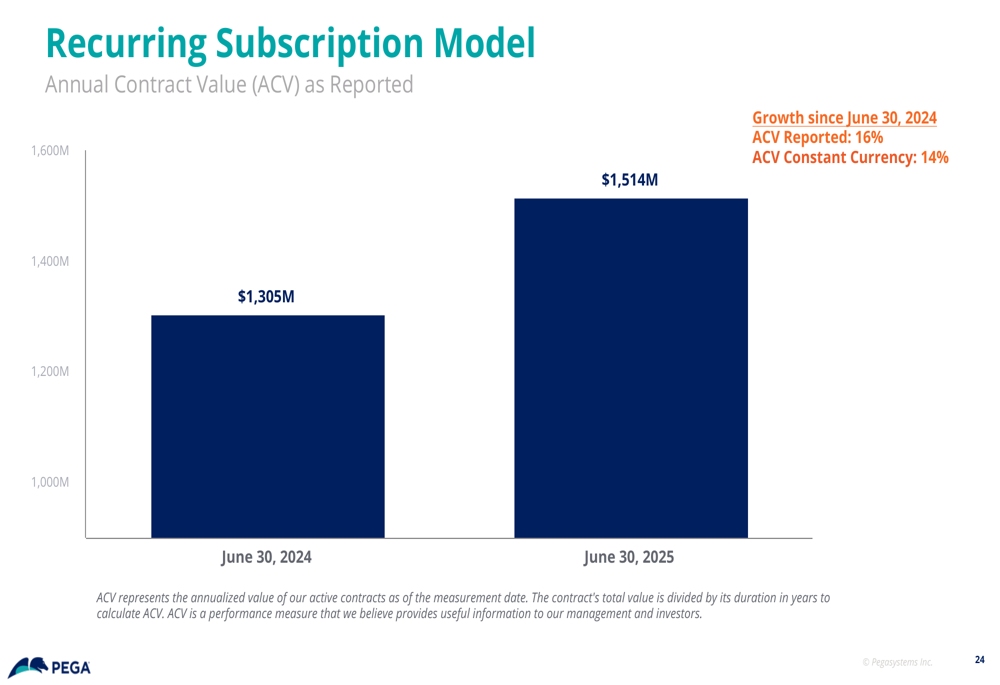

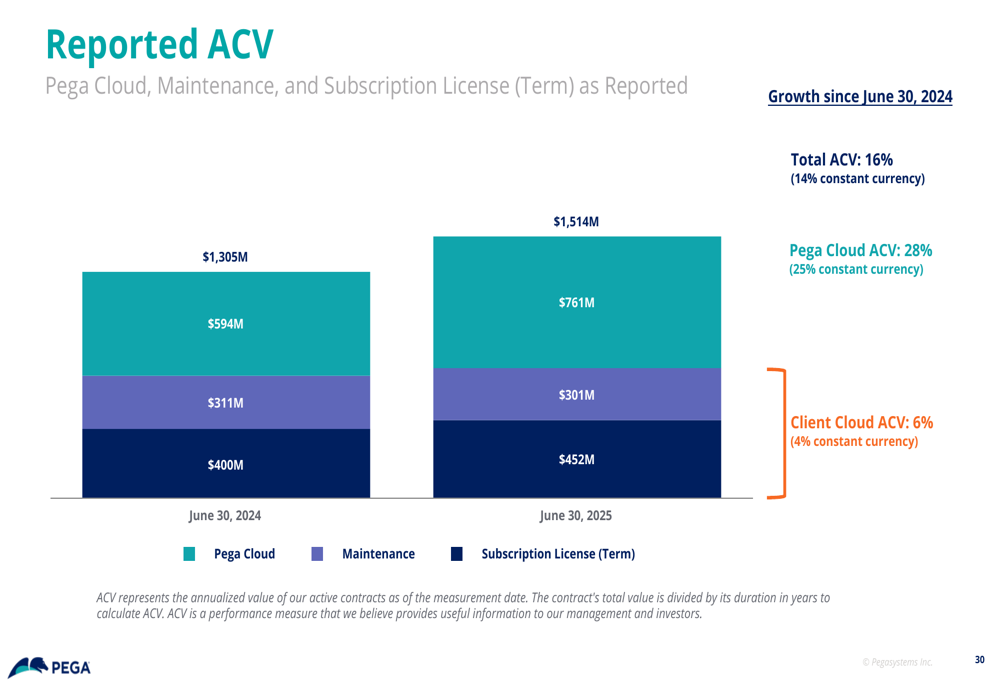

Pegasystems reported impressive financial results for Q2 2025, with Annual Contract Value (ACV) exceeding $1.5 billion for the first time in company history. Total ACV reached $1,514 million as of June 30, 2025, representing a 16% increase from $1,305 million reported a year earlier.

As shown in the following chart of ACV growth:

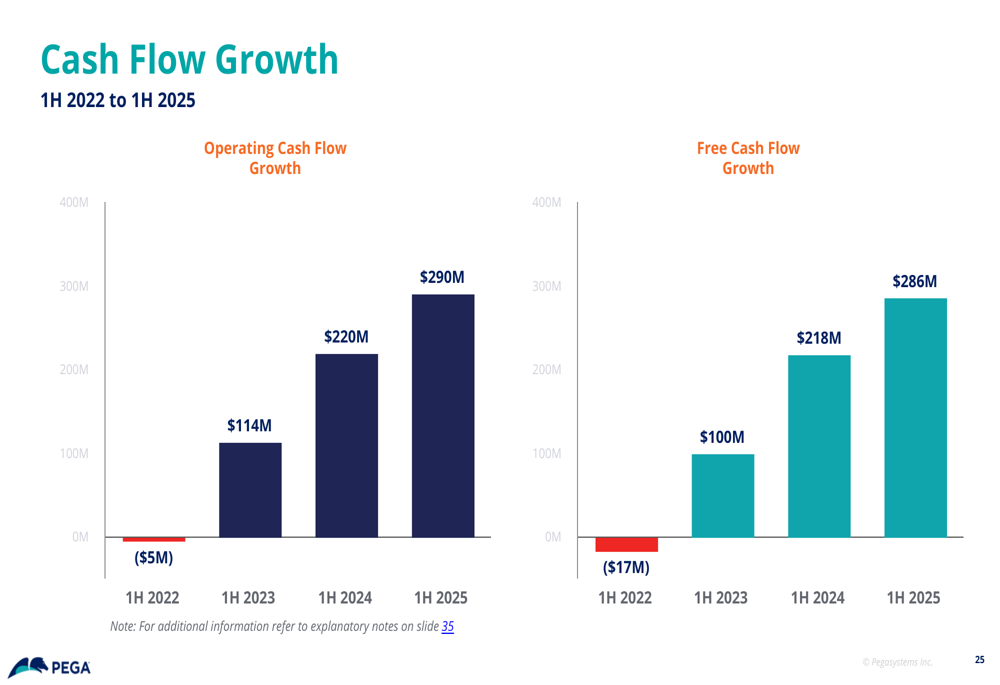

The company’s free cash flow reached $286 million in the first half of 2025, continuing a strong positive trend from previous years. This represents a significant improvement compared to $218 million in 1H 2024 and $100 million in 1H 2023.

The cash flow improvement is clearly illustrated in this multi-year comparison:

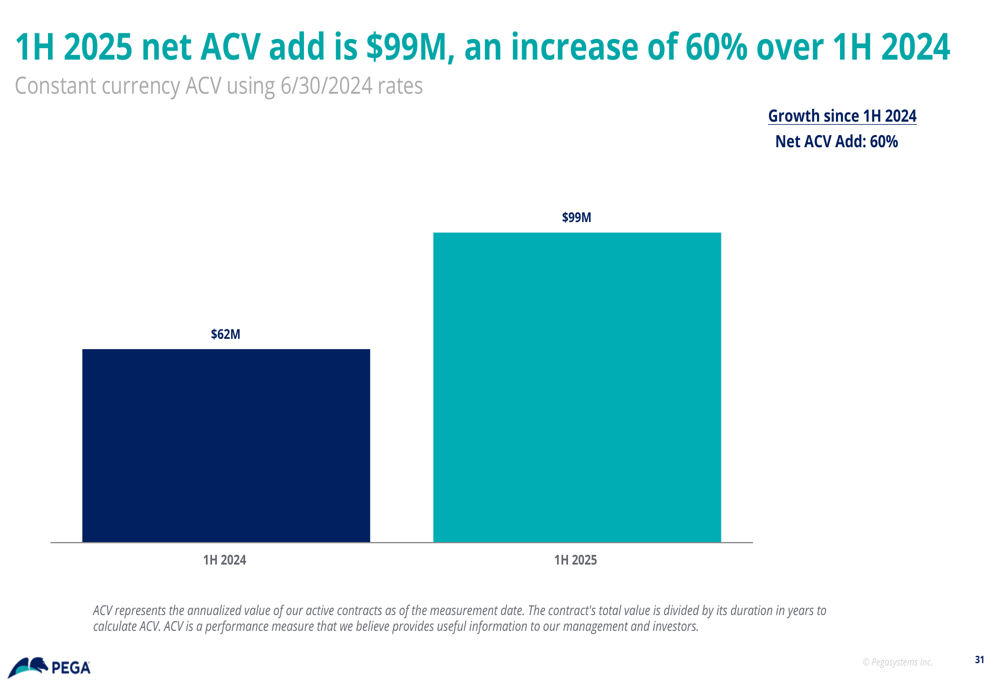

Net ACV add for the first half of 2025 was $99 million, representing a 60% increase over the same period in 2024. This acceleration demonstrates the company’s success in winning new business and expanding relationships with existing customers.

The net ACV growth is visualized here:

Cloud Transition Success

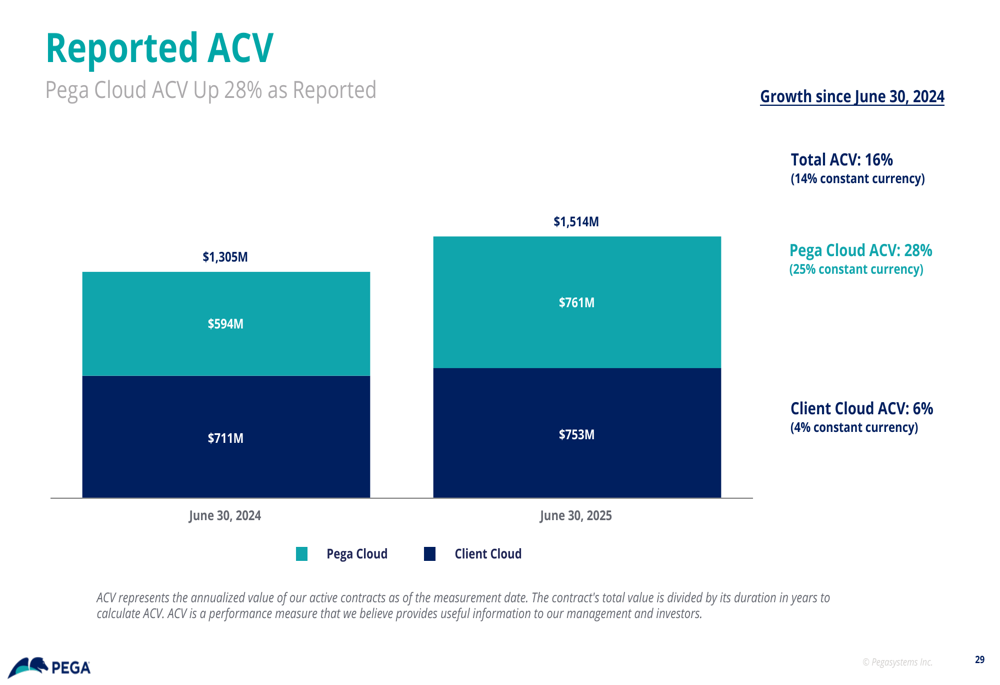

Pegasystems’ strategic shift toward cloud-based offerings continues to drive growth, with Pega Cloud ACV increasing by 25% year-over-year in constant currency. As of June 30, 2025, Pega Cloud ACV reached $761 million, compared to $594 million a year earlier.

The breakdown of the company’s ACV between Pega Cloud and Client Cloud shows the growing importance of cloud revenue:

When examining ACV by revenue type, the transition to subscription-based models becomes even more apparent:

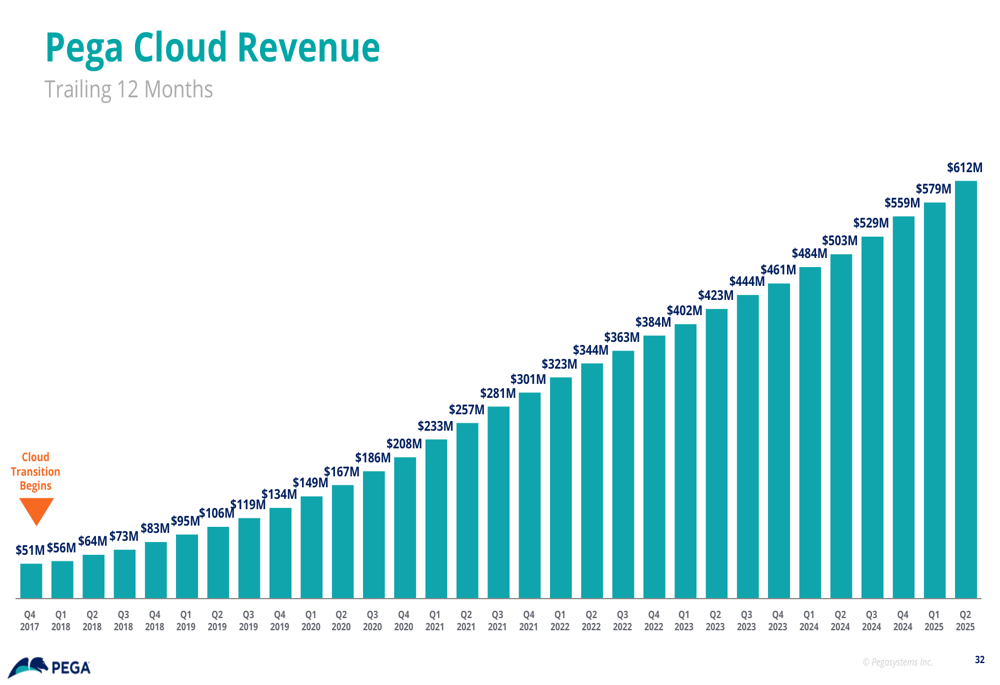

Pega Cloud revenue has grown substantially over the years, reaching $612 million on a trailing twelve-month basis by Q2 2025. This represents a remarkable increase from just $51 million in 2017, highlighting the company’s successful pivot to cloud services.

The profitability of Pegasystems’ cloud business has also improved significantly, with Pega Cloud gross margins expanding from 51% in 2019 to 78% in 2024. This margin expansion demonstrates the scalability of the cloud business model and the company’s operational efficiency improvements.

Strategic Positioning and Market Opportunity

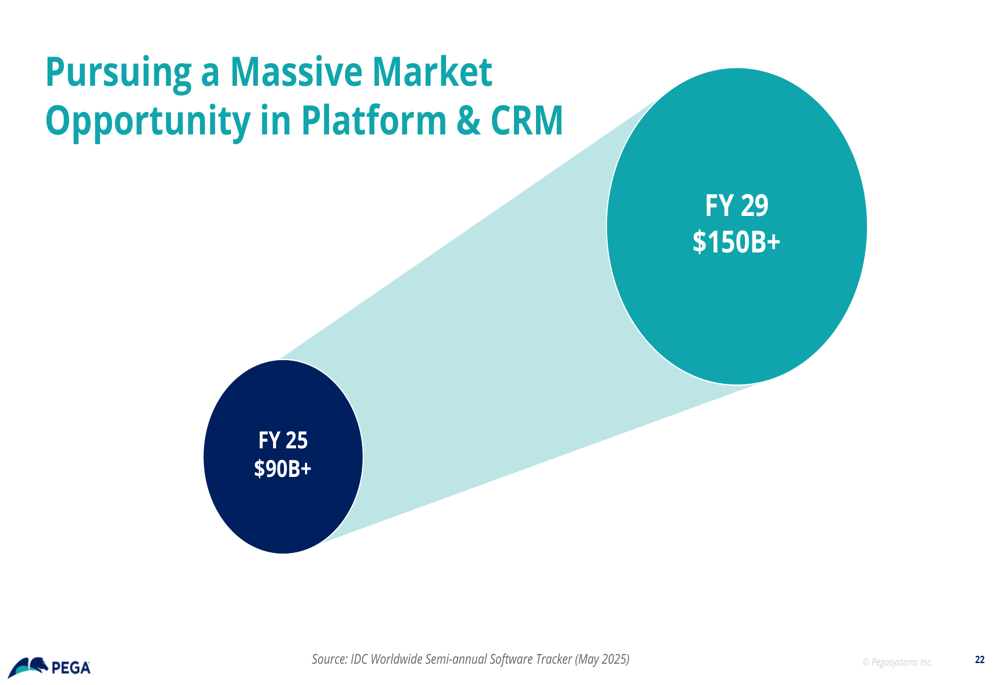

Pegasystems positions itself in a large and growing market, estimating its total addressable market for platform and CRM solutions at over $90 billion in fiscal year 2025, with potential growth to $150 billion by fiscal year 2029.

As illustrated in this market opportunity overview:

The company’s business strategy focuses on three key areas: one-to-one customer engagement, customer service, and intelligent automation. Pegasystems differentiates itself through its AI-powered decisioning capabilities and workflow automation platform, serving large enterprise clients across financial services, insurance, telecommunications, healthcare, manufacturing, and public sectors.

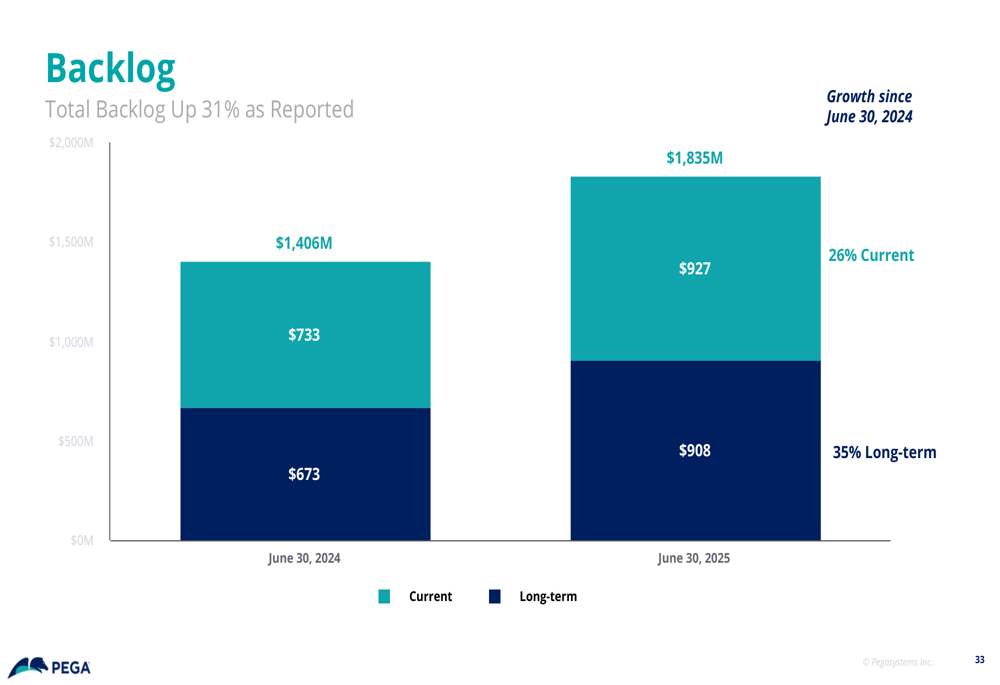

The company’s backlog, which represents contracted but not yet recognized revenue, has grown to $1,835 million as of June 30, 2025, compared to $1,406 million a year earlier. This 31% increase provides visibility into future revenue growth.

Pegasystems has received recognition from industry analysts, being named a leader in multiple Gartner Magic Quadrants and Forrester Wave reports, including Enterprise Low-Code App Platforms, Real-Time Interaction Management, and AI Decisioning Platforms.

Forward-Looking Statements

Looking ahead, Pegasystems is focused on continuing its transition to a recurring revenue model while expanding margins and increasing cash flow. The company’s presentation emphasized its "Rule of 40" mindset, which aims to have the sum of revenue growth rate and profit margin exceed 40%.

As stated in the presentation, Pegasystems aims to "strive to build a growing, recurring business to drive increased value" with a focus on sustaining growth, expanding margins, increasing cash flow, and driving shareholder value.

According to the earnings call transcript, the company anticipates typical seasonal softness in Q3 but remains committed to AI innovation, including the recently launched Pega GenAI Blueprint and a strategic collaboration with AWS. The company has also hinted at potential share buybacks, reflecting confidence in its financial position.

While the presentation highlights Pegasystems’ strengths and opportunities, investors should note potential challenges including seasonal fluctuations, competition from major players like Salesforce and ServiceNow, and execution risks in rolling out new AI innovations.

With its improving financial metrics, growing cloud business, and strategic focus on AI-driven transformation, Pegasystems appears well-positioned to capitalize on the expanding market for enterprise automation and customer engagement solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.